UV Curable Resins and Formulated Products Market Overview 2025–2034: $16.3 Billion to $38.8 Billion at 10.1% CAGR Fueled by Energy-Curing Innovation, Circular Coatings, and EV Electronics

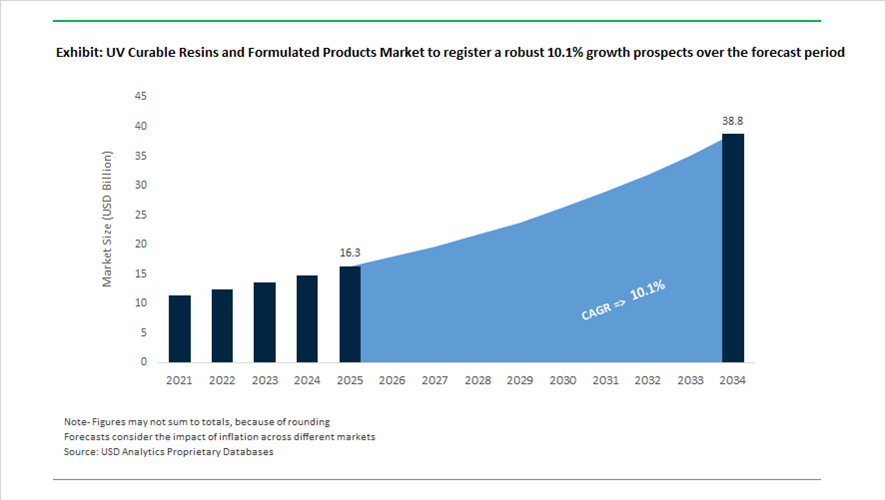

The global UV Curable Resins and Formulated Products market is valued at $16.3 billion in 2025 and is projected to reach $38.8 billion by 2034, advancing at a strong CAGR of 10.1%. Expansion is driven by accelerating demand for UV-curable acrylate resins, polyurethane acrylates (PUA), epoxy acrylates, photoinitiators, UV-LED/EB-curable coatings, low-VOC industrial finishes, energy-curing monomers, and sustainable graphic arts formulations. The shift from solvent-borne to energy-curable technologies in wood coatings, flooring, electronics, automotive components, digital printing, and EV battery systems is structurally transforming the coatings value chain. Regulatory pressure to reduce VOC emissions, combined with circular economy targets and increasing electrification, is amplifying adoption of UV-curable resins with enhanced toughness, dielectric performance, scratch resistance, and low-migration compliance.

Between 2024 and 2026, major producers expanded capacity and reinforced sustainable production platforms. In May 2024, Allnex introduced a high-performance waterborne UV-curable polyurethane acrylate resin for pigmented wood topcoats, delivering scratch resistance with reduced VOC emissions. In 2024, Arkema secured ISCC PLUS certification for its UV-LED-EB resin production sites in Virginia and Pennsylvania, enabling supply of bio-attributed Sartomer® monomers and oligomers with traceable renewable content. In January 2025, Arkema opened a Graphic Arts Center of Excellence in Wetherby, UK, focusing on UV/LED/EB-curable solutions for digital printing and recyclable packaging systems, including de-inking technologies. In late 2025, BASF completed capacity expansion for its Laromer® acrylate resin line in Ludwigshafen to meet high-growth demand in flooring and furniture coatings. In December 2025, Covestro finalized its strategic partnership with XRG P.J.S.C., supported by a €1.17 billion capital increase, accelerating its transition toward circular and sustainable UV-curable coating systems. Effective January 2026, iGM Resins entered an exclusive distribution partnership with IDCC Global Chem to strengthen penetration of Omnirad® photoinitiators and Photomer® energy-curing resins in the Indian subcontinent. Leadership realignment also signaled strategic acceleration. In January 2026, Allnex appointed a new CEO and intensified its green growth strategy, including production expansion at Mahad, India, targeting the regional industrial UV coatings market.

Technology differentiation is increasingly centered on performance durability and regulatory-safe formulations. In March 2025, iGM Resins introduced PHOTOMER® 4184 U, addressing mechanical toughness limitations in flexible UV coatings. In December 2025, the company expanded its glyoxylate photoinitiator portfolio with Omnipol® BL 582, a polymeric low-migration photoinitiator engineered for food packaging compliance. In April 2025, SKSHU Paint disclosed a UV-curable battery insulating coating based on modified polyurethane acrylate resin, replacing PET films in EV battery cells while enhancing dielectric strength and adhesion. In 2025, HumiSeal launched UV550, an acrylate elastomer-based coating delivering superior thermal shock resistance for new energy vehicle circuit boards, overcoming the brittleness typically associated with UV-curable systems. These advancements highlight how UV-curable resins are penetrating high-growth sectors such as electric mobility, printed electronics, flexible packaging, and advanced industrial coatings. The convergence of bio-attributed monomers, low-migration photoinitiators, waterborne UV systems, and EV-focused insulating coatings positions the market for sustained double-digit expansion through 2034, driven by performance engineering and circular materials innovation.

Trends and Opportunities in the UV Curable Resins and Formulated Products Market

Strategic Decarbonization Through Bio-Based Feedstock Integration

The UV curable resins and formulated products market is undergoing a structural shift from voluntary sustainability claims to balance-sheet-level decarbonization strategies. Resin manufacturers are increasingly embedding renewable carbon into core product portfolios to reduce exposure to petrochemical price volatility while aligning with mandatory climate disclosures under EU CSRD and comparable global ESG frameworks.

In January 2025, allnex achieved ISCC PLUS certification across multiple global sites, including its Drogenbos facility in Belgium, enabling mass-balance production of polyester, polyether, and polyurethane acrylates with traceable bio-attributed content. This approach allows formulators to deliver consistent UV curing performance while targeting a verified 30% CO2 emissions reduction by 2030, a metric increasingly scrutinized by OEM procurement teams.

Bio-based innovation is also moving upstream through proprietary feedstock partnerships. In September 2025, Arkema entered a strategic collaboration with Catalyxx to establish a low-carbon acrylic resin value chain. This follows Arkema’s global ISCC PLUS certification of its acrylic monomer assets, enabling Sartomer® UV liquid resins with up to 90% bio-attributed content for energy storage, e-mobility, and sustainable coatings. Complementing this, hubergroup introduced UV oligomers with 50% bio-based content derived from sugar alcohols such as sorbitol in March 2025, demonstrating that high bio-content resins can match or exceed fossil-based benchmarks in stain resistance and surface durability.

Vertical Integration Accelerating Adoption in Electronics and 5G Manufacturing

Demand growth in the UV curable resins market is increasingly concentrated in electronics, 5G infrastructure, and wearable devices, where performance tolerances are narrow and process reliability is critical. Resin suppliers are responding by moving downstream into application-specific, formulated systems rather than supplying commoditized oligomers.

To support 5G and advanced electronics assembly, Arkema doubled Sartomer® photocure resin capacity at its Nansha, China facility during late 2023 and early 2024. This expansion is explicitly targeted at high-purity UV and LED-curable materials required for semiconductor packaging, antenna modules, and advanced display technologies across Asia-Pacific. These formulations are engineered for fast cure kinetics, low ionic contamination, and stable dielectric performance under thermal cycling.

Vertical integration is also evident in equipment and process control. At Electronica 2025, Henkel demonstrated its Sonderhoff DM 90 modular dosing platform, tightly integrated with LOCTITE® UV-curable adhesives. By combining resin chemistry, automated dispensing, and IIoT-enabled process monitoring, Henkel is positioning itself as a solution provider for thin-film circuitry, miniaturized sensors, and lightweight wearable electronics. This model captures higher margins while embedding UV-curable systems deeper into customer production lines, raising switching costs and strengthening long-term supply relationships.

UV-Curable Matrices Enabling Solid-State Battery Manufacturing Scale-Up

Solid-state batteries represent one of the most disruptive growth opportunities for UV curable resins, as manufacturers seek solvent-free, high-throughput alternatives to conventional slurry-based electrode processing. UV curing is emerging as a key enabler for scalable solid-state electrolyte and electrode layer fabrication.

In 2025, Arkema introduced advanced UV-curable polymer matrices specifically designed for semi-solid and solid-state battery architectures. These materials enable rapid formation of uniform electrolyte films without the need for large drying ovens, potentially reducing manufacturing footprint requirements by up to 70%. The solvent-free nature of UV curing also improves layer uniformity, supporting higher energy density and longer cycle life.

Industrial trials conducted in 2024–2025 indicate that UV-cured electrolyte films can be produced at line speeds exceeding 30 meters per minute, far surpassing the throughput limitations of solvent evaporation-based coating methods. For automotive OEMs targeting commercial solid-state battery deployment between 2027 and 2030, this processing speed is a decisive factor. UV curable resins are therefore shifting from experimental materials to strategic enablers within next-generation EV battery supply chains.

Regulation-Driven Substitution in Architectural and Industrial Maintenance Coatings

Regulatory pressure on VOC emissions and hazardous stabilizers is creating a forced substitution cycle in architectural and industrial maintenance coatings, directly benefiting UV curable resins and formulated products. In January 2025, updated U.S. EPA National VOC Emission Standards and California’s SCAQMD Rule 1113 effectively capped many architectural coatings at below 50 g/L VOC. This threshold eliminates large segments of solvent-based industrial maintenance coatings, which typically emit 250–450 g/L VOC, from regulatory compliance.

As a result, 100% solids UV-curable systems and UV powder coatings are becoming the default solution for factory-applied and maintenance coatings where durability and rapid turnaround are critical. This regulatory momentum intensified further in August 2025 when the European Commission formally added UV-328 to the Persistent Organic Pollutants list under Amendment EU 2025/843. The immediate reformulation requirement for automotive, infrastructure, and heavy steel coatings has opened a large substitution opportunity for non-benzotriazole UV-curable resin platforms that meet the new 100 mg/kg limit without compromising long-term weatherability.

UV Curable Resins and Formulated Products Market Share and Segmentation Insights

Resin Type Market Share: Acrylic Resins Lead with Fast Cure Kinetics and Versatile Performance Properties

Acrylic resins dominate the UV curable resins market with a 48.60% share in 2025, driven by their rapid free-radical polymerization, excellent adhesion, and strong chemical and mechanical properties. These resins are widely used in coatings, inks, and electronics due to their formulation flexibility and performance consistency. Oligomers and monomers, epoxy resins, specialty resins, and vinyl ethers support specialized applications with tailored characteristics. A key trend is the development of bio-based acrylic resins, where renewable feedstocks are incorporated into formulations, enabling sustainable UV-curable systems that align with environmental regulations and growing demand for eco-friendly materials.

End-Use Industry Market Share: Industrial Manufacturing Leads with High-Productivity UV Coating Systems

Industrial manufacturing accounts for 28.40% of the UV curable resins market in 2025, supported by widespread use in coating metal, plastic, and wood substrates across machinery, consumer goods, and furniture production. UV-curable systems enable rapid curing, reduced processing time, and elimination of VOC emissions, improving operational efficiency. Packaging and printing, electronics and electrical, automotive and transportation, construction, and healthcare sectors contribute additional demand. A key growth driver is the integration of UV curing into Industry 4.0 manufacturing environments, where automated production lines leverage consistent curing performance to enhance throughput, reduce waste, and support just-in-time production models.

UV Curable Resins and Formulated Products Market Competitive Landscape

The UV Curable Resins and Formulated Products market in 2026 is shaped by molecular decarbonization, bio-attributed resin systems, and waterborne UV-LED hybrids that deliver low-VOC, SVOC-free performance while meeting stringent regulatory standards and Product Carbon Footprint transparency requirements across coatings, electronics, and additive manufacturing.

Arkema Advances Bio-Attributed UV Resins with Sartomer® and Additive Manufacturing Leadership

Arkema is reinforcing its leadership in the UV Curable Resins market through its Sartomer® portfolio, focusing on bio-attributed and high-performance energy-curable materials. ISCC PLUS certification at its Gissi facility enables mass-balanced, low-carbon UV resin production across its global network. The company is advancing additive manufacturing with N3xtDimension® resins engineered for flame resistance and thermal stability in aerospace-grade 3D printing. Strategic collaboration with Catalyxx is accelerating the development of bio-based acrylic feedstocks, reducing lifecycle emissions of UV-curable monomers. Arkema’s global UV-LED-EB production footprint provides drop-in sustainable resins with strong adhesion and reactivity on complex substrates. This combination of decarbonized feedstocks and advanced application performance strengthens its specialty materials positioning.

BASF SE Integrates Low-SVOC UV Resin Technologies with Infrastructure Durability Solutions

BASF SE is expanding its role in the UV Curable Resins market through Verbund integration and sustainability-driven formulation technologies. Price increases on key acrylic monomers such as BA and 2-EHA reflect supply chain pressures while supporting ongoing innovation in UV-curable systems. The company is leveraging Tinuvin® stabilizers to enhance durability of UV-cured components in floating solar infrastructure, extending service life beyond 30 years. Its Near-Zero SVOC dispersion technology supports indoor UV coatings compliant with LEED and WELL standards. BASF’s VALERAS® portfolio provides transparent Product Carbon Footprint data, enabling customers to quantify emissions reductions from UV-curable transitions. This integration of durability, compliance, and sustainability data reinforces BASF’s competitive strength.

Covestro Drives Bio-Based and Low-Migration UV Resins for Circular Packaging

Covestro AG is positioning itself as a leader in circular UV-curable resin systems with high bio-based content and low-migration performance. Its AgiSyn™ and NeoRad™ portfolios include resins with up to 83% renewable content, designed to match the performance of fossil-based materials in coatings and flooring applications. AgiSyn™ 717 delivers controlled polymerization and reduced migration for food-contact packaging, addressing stringent regulatory requirements. The company’s hybrid resin systems support both LED and mercury curing, enabling gradual transition to energy-efficient curing technologies. Covestro is advancing self-initiating resin architectures that eliminate external photoinitiators, reducing SVHC exposure and VOC emissions. This innovation aligns with global demand for safer, sustainable packaging materials.

Evonik Enhances UV Ink and Coating Performance with Advanced Additives and Methacrylates

Evonik Industries AG is strengthening its position in the UV Curable Resins market through high-performance additives and specialty methacrylate monomers. The launch of TEGO® Dispers 695 improves pigment dispersion and color vibrancy in UV-LED inks while reducing energy requirements during curing. Expansion of hydroxyl-terminated polybutadiene capacity supports demand for UV-curable elastomers and adhesives in automotive and electronics applications. Strategic distribution partnerships in North America enhance technical service and market penetration. The VISIOMER® methacrylate range enables formulators to fine-tune glass transition temperature and mechanical flexibility in cured systems. This focus on formulation precision and performance optimization positions Evonik as a key enabler of next-generation UV technologies.

iGM Resins Expands Energy-Curing Portfolio with Safer Photoinitiators and Flexible Resin Systems

iGM Resins is advancing the UV Curable Resins market through a total-system approach combining resins, photoinitiators, and additives. Its partnership with IDCC Global Chem strengthens distribution in India, targeting rapid growth in packaging and printing applications. The company is leading regulatory adaptation by developing safer alternatives to reclassified photoinitiators such as Omnirad 184, aligning with evolving GHS standards. PHOTOMER® 4184 U addresses brittleness challenges in high-hardness coatings by delivering enhanced flexibility and durability. Investment in a cryogenic nitrogen plant at its Italy facility reduces production emissions, supporting its green energy curing strategy. This integration of regulatory compliance, product innovation, and sustainable manufacturing enhances its competitive positioning.

China UV Curable Resins and Formulated Products Market Driven by Mandatory Green Standards and Electronics Scale-Up

China represents the most regulation-led growth engine within the UV curable resins and formulated products market, with compliance mandates directly reshaping coating chemistries and capacity deployment. In 2025, the State Administration for Market Regulation issued GB 30981.1-2025 and GB 30981.2-2025, effective June 1, 2026, establishing the most stringent VOC and hazardous substance limits yet for industrial and architectural coatings. These standards are forcing a rapid shift away from solvent-based systems toward UV-curable and hybrid waterborne technologies across wood coatings, industrial flooring, and protective metal finishes. As enforcement tightens, UV curing is increasingly positioned as the default compliance pathway rather than a niche alternative.

Capacity expansion is accelerating in parallel with regulation. In late 2025, Arkema reached full operational scale at its expanded Nansha facility, effectively doubling regional output of Sartomer specialty UV and LED-curable resins to serve 5G infrastructure, renewable energy components, and electronics manufacturing. Downstream demand is reinforced by China’s 2025–2026 Building Materials Industry Growth Plan, which incentivizes large-scale adoption of green building materials, including UV-curable wood and floor coatings that deliver rapid curing, low emissions, and high abrasion resistance. Technology depth is also advancing. In November 2025, BASF commissioned a controlled free radical polymerization-based dispersant line in Nanjing to support pigment stability in UV-curable digital inks, a critical requirement for electronics printing and decorative surfaces. Semiconductor alignment further strengthens demand, as UV resins are increasingly tailored for photoresists and chip packaging, while BASF’s loopamid nylon 6 recycling facility in Shanghai provides circular feedstocks for UV-curable textile coatings.

Japan UV Curable Resins Market Positioned as a Strategic Semiconductor and National Security Asset

Japan’s UV curable resins market is being shaped by semiconductor sovereignty and advanced materials innovation. In December 2025, Toray Industries announced a negative photo-definable polyimide sheet for glass core substrates. This UV-curable material enables ultra-fine via processing, significantly reducing copper plating requirements in next-generation AI chip packaging and reinforcing Japan’s leadership in high-density interconnect technologies.

Epoxy and UV resin capacity is also being scaled under government oversight. DIC Corporation received approval from the Ministry of Economy, Trade and Industry for a new epoxy resin expansion at its Chiba plant, aimed at securing domestic semiconductor supply chains. This policy support is reinforced by Japan’s designation of epoxy and UV-curable resins as Strategic Materials under the Act on the Promotion of Ensuring National Security, unlocking direct subsidies for localized production. At the application level, Japanese manufacturers are advancing the chemitronics model, integrating chemical formulation with electronic performance. UV resins with extreme thermal stability and ultra-low signal loss are being engineered specifically for emerging 6G hardware and advanced packaging substrates.

United States UV Curable Resins Market Fueled by Bio-Based Policy Support and Additive Manufacturing

The United States UV curable resins and formulated products market is increasingly shaped by federal sustainability programs and defense-driven qualification of advanced materials. In 2025, the expansion of the USDA BioPreferred Program enabled certification of new flexible acrylate oligomers such as Sarbio 7407, incorporating high levels of bio-based content. This policy signal is accelerating adoption of renewable UV-curable systems across packaging, coatings, and consumer-facing applications.

Additive manufacturing is a central growth vector. Throughout 2025, the U.S. Department of Defense and aerospace contractors qualified new flame-retardant UV resins for on-demand manufacturing, marking a transition from prototyping to functional end-use parts. Infrastructure investment is also indirectly stimulating demand. Funding under the Bipartisan Infrastructure Law has increased specification of fast-cure UV coatings for bridges and public transport assets, where rapid return-to-service minimizes disruption. Digitalization is strengthening formulation selection. Dymax and Arkema launched AI-enabled digital material selection platforms in 2025, allowing engineers to match UV oligomers precisely to mechanical performance, cure speed, and durability requirements.

South Korea UV Curable Resins Market Aligned with Smart Cities and Display Leadership

South Korea’s UV curable resins market is closely tied to national semiconductor and urban modernization strategies. Under the government’s 2025–2030 Compound Semiconductor Roadmap, development of UV-curable barrier films and OLED encapsulation resins has been prioritized to protect the country’s dominance in display manufacturing. These materials demand high optical clarity, moisture resistance, and rapid curing to support next-generation screens.

Infrastructure and urban development further support demand. Protective coatings for buildings and public assets are increasingly specified as UV-cured systems to meet durability and sustainability targets associated with large-scale modernization projects. South Korea’s Smart City initiatives mandate anti-graffiti and self-cleaning coatings for public infrastructure, leveraging UV-curable formulations that offer fast application, long service life, and reduced maintenance. The convergence of electronics expertise and advanced polymer chemistry positions South Korea as a high-value innovation market rather than a volume-driven producer.

Germany UV Curable Resins Market Defined by Additive Manufacturing and REACH Leadership

Germany remains Europe’s technical and regulatory anchor for UV curable resins and formulated products. At Formnext 2025 in Frankfurt, multiple European suppliers unveiled water-soluble and flame-retardant UV resins designed for volumetric additive manufacturing, a support-free 3D printing technology that enables complex geometries and rapid production cycles. These launches highlight Germany’s role in translating laboratory-scale resin chemistry into industrialized additive manufacturing platforms.

Regulatory pressure continues to shape product design. Germany is leading the transition toward REACH-compliant photoinitiators, with companies such as iGM Resins expanding their Photomer portfolio to eliminate substances under increasing regulatory scrutiny, including TPO and 369. Decentralized manufacturing is another defining trend. Carl ROTH expanded its range of custom-formulated, low-VOC UV resins in 2025, targeting localized industrial 3D printing hubs and research-driven production environments. Germany’s market influence lies in setting formulation benchmarks that ripple across the wider European UV curing ecosystem.

Summary of Country-Level UV Curable Resins and Formulated Products Market Dynamics

UV Curable Resins and Formulated Products Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Core Application Focus

|

Market Role

|

|

China

|

Mandatory green standards and electronics policy

|

Coatings, semiconductors, green buildings

|

Regulation-led scale and circular integration

|

|

Japan

|

Semiconductor security and chemitronics

|

Advanced packaging, 6G materials

|

High-value strategic materials hub

|

|

United States

|

Bio-based policy and additive manufacturing

|

Infrastructure coatings, aerospace, 3D printing

|

Innovation-led demand expansion

|

|

South Korea

|

Display leadership and smart cities

|

Encapsulation resins, urban coatings

|

Electronics-centric specialty market

|

|

Germany

|

REACH compliance and advanced AM

|

Photoinitiators, volumetric 3D printing

|

Regulatory and technical benchmark

|

UV Curable Resins and Formulated Products Market Report Scope

UV Curable Resins and Formulated Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.3 Billion

|

|

Market Size (2034)

|

$38.8 Billion

|

|

Market Growth Rate

|

10.1%

|

|

Segments

|

By Resin Type (Acrylic Resins, Epoxy Resins, Vinyl Ethers, Oligomers and Monomers, Specialty Resins), By Curing Technology (Free Radical UV Curing, Cationic UV Curing, LED UV Curing, Hybrid and Dual Curing), By Application (Coatings, Inks and Graphic Arts, Adhesives and Sealants, 3D Printing and Additive Manufacturing, Electronics), By End-Use Industry (Industrial Manufacturing, Electronics and Electrical, Packaging and Printing, Automotive and Transportation, Construction and Woodworking, Healthcare and Medical Devices)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arkema S.A., BASF SE, Allnex GmbH, Covestro AG, DIC Corporation, Dymax Corporation, Resonac Corporation, iGM Resins B.V., Dow Inc., Evonik Industries AG, Toagosei Co. Ltd., Miwon Specialty Chemical Co. Ltd., Eternal Materials Co. Ltd., Jiangsu Nata Opto-electronic Material Co. Ltd., Sanmu Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Curable Resins and Formulated Products Market Segmentation

By Resin Type

Urethane Acrylates

Epoxy Acrylates

Polyester Acrylates

Polyether Acrylates

- Epoxy Resins

- Vinyl Ethers

- Oligomers and Monomers

- Specialty Resins

By Curing Technology

- Free Radical UV Curing

- Cationic UV Curing

- LED UV Curing

- Hybrid and Dual Curing

By Application

- Coatings

- Inks and Graphic Arts

- Adhesives and Sealants

- 3D Printing and Additive Manufacturing

- Electronics

By End-Use Industry

- Industrial Manufacturing

- Electronics and Electrical

- Packaging and Printing

- Automotive and Transportation

- Construction and Woodworking

- Healthcare and Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the UV Curable Resins Industry

- Arkema S.A.

- BASF SE

- Allnex GmbH

- Covestro AG

- DIC Corporation

- Dymax Corporation

- Resonac Corporation

- iGM Resins B.V.

- Dow Inc.

- Evonik Industries AG

- Toagosei Co. Ltd.

- Miwon Specialty Chemical Co. Ltd.

- Eternal Materials Co. Ltd.

- Jiangsu Nata Opto-electronic Material Co. Ltd.

- Sanmu Group

*- List not Exhaustive