Water Desalination Equipment Market Overview: Global Insights, Size, and Growth Drivers

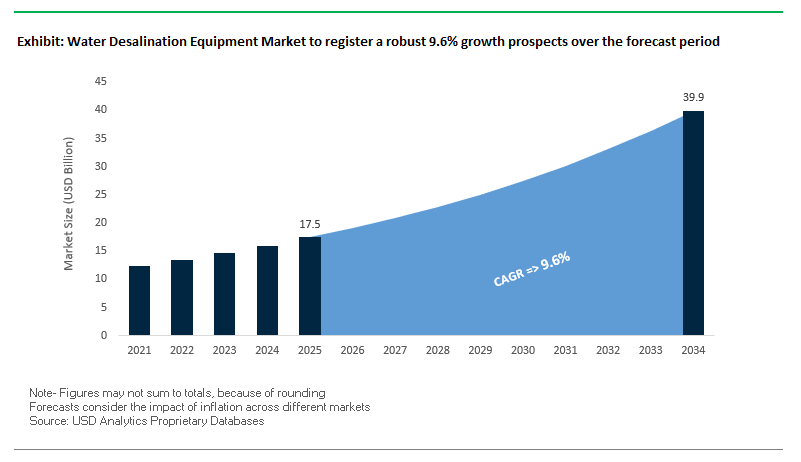

The global water desalination equipment market is on a strong growth trajectory, projected to rise from USD 17.5 billion in 2025 to USD 39.9 billion by 2034, representing an impressive CAGR of 9.6%. The growth is fueled by escalating water scarcity, particularly in arid and densely populated regions, alongside technological innovations that have significantly reduced energy consumption and operational costs in desalination processes.

One such motivating factor is widespread use of reverse osmosis (RO) technology associated with higher effectiveness, chemical and biological stability, and low energy requirements. Desalination patents have grown drastically since 2008, signifying innovation rivalry in the sector. Seawater still remains key feedstock for desalination owing to supply abundance and provision of most world desalinated water capacity.

Growing hybrid systems combining RO with thermal techniques like multistage flash (MSF) are gaining mainstream acceptance. Such technologies prolong RO membrane lifespans, boost efficiencies, and minimize maintenance downtimes like the Ras Al-Khair power and desalination plant in Saudi Arabia. The Middle East and North Africa (MENA) continues to be the highest adopter due to severe water shortages and rapid population growth, leading to massive investments in large-scale desalination facilities across governments and independents.

Key Insights:

- Reverse Osmosis (RO) holds the largest technology share due to its efficiency and reduced operating costs.

- Seawater accounts for the majority of global desalination capacity.

- Hybrid RO–thermal plants are gaining traction for performance optimization.

- MENA remains the largest and fastest-growing regional market for desalination infrastructure.

Market Analysis: Strategic Developments and Investment Trends

Market forces are fueled further by high investments, geographic diversification, and technological innovation. ACWA Power and Gulf Investment Corporation (GIC) signed a historic joint venture in August 2025 valued at a record USD 4 billion to build the Az-Zour North 2 & 3 power and water megaproject in Kuwait. With a production capacity of more than 120 million imperial gallons a day, this plant will form the core of ensuring water supply in the region.

In June 2025, Veolia opened a new PFAS treatment plant in the United States valued at USD 35 million, treating regulated drinking water contaminants and solidifying its reputation as a leader in advanced water treatment solutions. Previously, in February 2024, Veolia launched PoIaris™ 2.0, a high-capacity distillation and steam generation system designed to target pharmaceutical applications, while in March 2024 it increased its mobile water services in Malaysia with new modular RO systems is a move to serve both industrial and municipal customers who need quick-response solutions.

Government-led investments continue to be central. In October 2024, Algeria pledged USD 3 billion to six new desalination plants by 2030 within a larger USD 5.4 billion climate-driven water shortage mitigation plan. On the supply side of technology, DuPont membranes were chosen in July 2021 for Israel's Sorek B desalination plant and LG Chem, via an April 2021 collaboration between LG Chem and CaribDA, provided SWRO membranes in a St. Vincent disaster relief mission exemplifies the humanitarian side of desalination technology.

Notably, March 2025 was a pivotal moment where ACWA Power announced Shanghai Innovation Centre for boosting desalination–renewable energy integration to create a market shift in sustainability-driven solutions.

Trends and Opportunities in Water Desalination Equipment Market

Trend 1: Shift to Renewable-Powered Desalination

Water desalination plant market is experiencing a shift towards renewable-energy-driven systems, solar, wind, and hybrid power increasingly being used to decrease operational expenditure and environmental footprint. State-of-the-art seawater reverse osmosis (SWRO) facilities achieve a level of specific energy consumption as low as 3.0 kWh/m³, and coupled with renewable energy sources, this drastically reduces energy costs that otherwise make up a large percentage of desalination plant operational expenditure. Decentralized plants like Elemental Water Makers' solar-driven system in the Philippines generate 11 m³/day of fresh water while cutting CO2 emissions by 11 tons yearly and local collection costs of water by 43%. Hybrid configurations such as the Canary Islands wind-solar coupled desalination plant provide resilient-water-supply assurance regardless of intermittent energy supply due to fluctuations in energy inputs, showcasing renewable-driven desalination's ability to be a reliable source even in off-grid or distant locations. The shift is a response to increasing global efforts to adopt sustainable water supplies and is making renewable-driven desalination a major growth engine in the market.

Trend 2: Brine Minimization & Resource Recovery

Environmental rules and sustainability mandates are driving desalination operators to use technology that reduces brine effluent and facilitates resource recovery. Brine, a highly concentrated desalination byproduct, has recoverable valuable minerals like lithium, magnesium, and potassium. Desalination operators are implementing technology such as advanced vacuum membrane distillation (AVMD) and crystallization systems to recover salts and high-grade minerals from brine streams. A sample case is Aquatech's lithium recovery plant in Nevada, which demonstrates how brine can be converted into revenue and decrease environmental impact. Such technology supports ESG targets and regulatory mandates while fostering a circular economy practice where desalination byproducts serve industrial applications, reduce ecological footprinting, and improve the viability of desalination ventures. Isolated communities and distant islands are finding small-scale, module-based desalination units to be economical and easily deployable water solutions. Plug-and-play desalination systems in a containerized format provide fast installation, flexibility, and redundancy to provide freshwater supply at places where infrastructures are limited.

Opportunity 1: Small-Scale Modular Desalination for Islands

Remote islands and isolated communities are increasingly adopting small-scale, modular desalination units as cost-effective and rapidly deployable water solutions. Containerized, plug-and-play desalination systems enable quick installation, scalability, and redundancy for freshwater supply in locations with limited infrastructure. For example, a remote island municipality deployed a 500 m³/day solar-powered modular system, ensuring uninterrupted water availability while reducing dependence on large, centralized plants. These modular units offer lower total cost of ownership, reduce the need for extensive distribution networks, and provide a flexible solution for regions facing water scarcity, making them highly attractive for local governments, tourism hubs, and remote industrial facilities.

Opportunity 2: Industrial Desalination for Data Centers & Hydrogen

High-water-user industries like data centers and green hydrogen facilities are driving on-site desalination demand to ensure sustainable supplies and achieve corporate ESG ambitions. Data centers consume high quantities of water to be cooled, and advanced reverse osmosis and brine concentrators can be used to achieve water reuse and treat minimal discharge. Green hydrogen production involves ultrapure water in the process of electrolysis, where an estimated feedwater requirement will range between 14–33 liters per kilo hydrogen. Desalination coupled in an integrated manner into an industry process like harnessing data centers' waste heat to drive desalination demonstrates both economics and environment synergies. The trend highlights increasing desalination technology use in industry applications within sustainable and resilient approach to water management.

Water Desalination Equipment Market Share Insights

Reverse Osmosis Technology Cementing Dominance in Desalination

Reverse Osmosis (RO) systems are projected to capture nearly 70% of the global water desalination equipment market by 2025, underscoring their role as the undisputed market leader. RO’s rise is driven by lower energy consumption compared to thermal technologies, scalability, and advances in membrane efficiency and energy recovery devices. The technology has become the default choice for new greenfield desalination projects worldwide, particularly in the Middle East, North Africa, and coastal Asia. With governments and private operators seeking cost-effective and modular solutions, RO continues to displace traditional thermal processes, setting the benchmark for future desalination capacity additions.

.png)

Thermal Distillation Technologies Retaining Strategic Niches

While thermal technologies are losing ground to RO, they still account for a notable portion of the market. Multi-Stage Flash (MSF) distillation holds about 15%, largely in legacy plants across the Middle East where cogeneration facilities make it viable. In contrast, Multi-Effect Distillation (MED) retains a 10% share, offering higher energy efficiency than MSF and thriving in industrial applications where waste steam is available, such as refineries and power plants. These technologies remain relevant in regions with abundant energy and in applications where high-salinity feedwater challenges RO’s efficiency, but their market share is gradually eroding in favor of membrane-based systems.

Specialized Role of Electrodialysis in Brackish Water Treatment

Electrodialysis (ED/EDR) systems, representing around 5% of the market, are not competitive in seawater desalination but remain strategically important for brackish water treatment. Their advantage lies in energy efficiency at lower salinity levels, making them attractive for inland industrial sites and regions where brackish groundwater is the dominant source. Although niche, ED technology is expected to see steady demand as industries and municipalities explore low-energy desalination options for non-seawater applications.

Large-Scale Plants Leading Global Capacity Expansion

By capacity, large-scale desalination plants exceeding 20,000 m³/day dominate with around 60% of the market, representing the backbone of national water security strategies. These municipal-scale installations deliver the bulk of global desalinated water output, often backed by multi-billion-dollar government contracts in arid regions such as the Gulf states, Israel, and parts of North Africa. Their scale ensures lower unit costs, making them the preferred choice for rapidly growing urban populations. The segment will remain the primary driver of global desalination infrastructure investment, especially as climate stress heightens water scarcity in coastal regions.

Industrial and Medium-Scale Installations Offering Steady Growth

Medium-scale desalination systems (5,000–20,000 m³/day) hold about 25% of the market, with strong traction in industrial complexes, power plants, and large islands. Their flexibility allows them to deliver both process water for industries and potable water for semi-urban regions, particularly in Asia-Pacific and Latin America. The segment is stable and attractive for industries seeking on-site, independent water supplies, reducing reliance on municipal sources. In contrast, small-scale modular units (<5,000 m³/day) capture 15%, primarily serving remote resorts, offshore platforms, and emergency response operations, where portability and ease of deployment are critical.

Municipal Sector Dominating Demand with Urban Water Security Needs

The municipal sector represents nearly 65% of global desalination equipment demand, reflecting its central role in securing potable water for cities in water-scarce regions. Governments in the Middle East, California, and Australia are heavily investing in large-scale RO facilities to ensure urban water supply resilience. Public utilities are the primary purchasers of long-term desalination capacity, often entering into multi-decade build-operate-transfer agreements. Municipal adoption is expected to accelerate as more coastal urban centers face mounting water stress, making the the anchor end-user segment for future market growth.

Industrial Desalination as a Strategic Niche Segment

The industrial sector accounts for around 25% of the market, led by oil & gas, power generation, and mining industries. These sectors demand high-purity water for boiler feed, cooling, and process operations, often in remote or water-stressed locations. On-site desalination systems allow industries to maintain operational independence while mitigating risks associated with water scarcity. With industrial water demand projected to rise, particularly in Asia-Pacific and the Middle East, The segment remains a high-value niche with stable long-term growth prospects.

Commercial and Hospitality End-Users Expanding in Remote Regions

The commercial and hospitality sector contributes approximately 10%, driven by resorts, cruise ships, and military bases. Luxury island resorts rely on compact desalination units to provide reliable water for operations while meeting sustainability goals. Cruise ships function as self-contained floating desalination plants, ensuring continuous freshwater production for thousands of passengers. Meanwhile, military installations in arid or remote zones deploy robust desalination systems to guarantee water security and operational readiness. Though smaller in scale, The segment is strategically important for mobility, reliability, and high-value contracts.

Country Analysis of the Water Desalination Equipment Market

Saudi Arabia: Vision 2030 Accelerates RO Desalination Expansion

Saudi Arabia’s water desalination equipment market is primarily driven by large-scale government investments under Vision 2030, with the Saline Water Conversion Corporation (SWCC) allocating over $6.6 billion for new desalination projects in 2023. The SWCC plans to commission five new plants by 2027, while the Saudi Water Partnership Company (SWPC) is working to achieve 100% private sector participation in desalination projects by 2030. Major players like ACCIONA Agua are actively enhancing operational efficiency through advanced technologies such as turbidity prediction systems at plants including Al Khobar 1 and 2, and Madinah 3. A key focus is converting existing multi-stage flash (MSF) and multi-effect distillation (MED) plants to energy-efficient reverse osmosis (RO) systems. Projects like the Rabigh 3 Independent Water Project (IWP), with a 600,000 m³/day capacity, highlight the increasing adoption of advanced RO desalination equipment integrated with renewable energy sources for sustainable water production.

United Arab Emirates (UAE): Large-Scale Solar-Powered Desalination Initiatives

The UAE is rapidly advancing its water desalination equipment market through mega projects aligned with the Water Security Strategy 2036. The Taweelah Desalination Plant, with a capacity of 909,200 m³/day, and the Hassyan seawater desalination plant, set to become operational in 2027, are benchmarks for efficiency and sustainable operation. Veolia, through its subsidiary SIDEM, is engineering pre- and post-treatment solutions at Hassyan, including two-pass SWRO membranes and two-phase pretreatment. Additional projects like the Umm Al Quwain Desalination Plant, with 681,900 m³/day capacity, further underline the UAE’s commitment to modular and energy-efficient desalination technologies, ensuring continuous, high-quality water supply for urban and industrial applications.

Israel: Global Leader in Seawater Desalination and Technology Export

Israel's desalination industry shows global competitiveness in the market for water desalination plant equipment, with key facilities such as Sorek 1 and 2, Hadera, and Ashkelon. IDE Water Technologies has recently handed over the Sorek 2 – Be'er Miriam Desalination Plant, which was the first large-capacity steam-driven SWRO plant anywhere in the world. The firm has also won a contract for Israel's seventh large desalination plant in Western Galilee to produce 100 million cu m a year. Israel's large-desalination success serves both domestic water requirements and makes this country a leading exporter of desalination technology and know-how while promoting global use of innovative RO systems and seawater treatment applications.

China: Strategic Integration of AI, Nuclear, and Advanced Membrane Technology

China's water desalination plant market is growing in response to the 14th Five-Year Plan to achieve 3.5 million m³/day desalinated water production by 2025. State-of-the-art facilities like Qingdao Baifa Desalination Plant apply predictive algorithms powered by AI and machine learning to foretell membrane fouling and streamline pressure such that operational expenses decrease by 15%. Guangdong Nuclear Desalination Initiative is Asia's first nuclear-based desalination plant that applies multi-effect distillation (MED) combined with nuclear power to provide desalinated water to adjacent industrial centers. Scientists at Zhejiang University increased water flux by 30% employing graphene oxide membranes to exemplify Chinese efforts at high-capacity, energy-efficient desalination technology application in both municipal and industrial applications.

United States: Brackish Water Treatment and Public-Private Partnerships

The U.S. water desalination equipment market is increasingly leveraging reverse osmosis (RO) and brackish water treatment solutions to address regional water scarcity. Facilities like the H2OAKS Center in Bexar County, Texas, and the Southmost Regional Water Authority in Cameron County utilize RO systems to supply potable water from brackish aquifers, covering over 40% of local demand. IDE Water Technologies has been selected for a mega desalination and water recycling project in Fort Lauderdale through a public-private partnership. Across states such as California, Texas, and Florida, desalination and water reuse technologies are being deployed to mitigate drought impacts, showcasing growing adoption of modular and scalable desalination equipment.

Japan: Innovation in RO Membranes and Solar-Powered Desalination

Japan’s desalination market emphasizes innovation in water desalination equipment and RO membrane technology. Toray has introduced RO membranes to 76 countries, supplying water for over 420 million people. Science Tokyo researchers have developed solar-powered methods using liquid metal tin to purify seawater while recovering valuable metals from brine. Kurita Water Industries contributes through membrane cleaners, scale inhibitors, and dispersants that enhance RO plant efficiency. The Kurita Innovation Hub, established in 2022, serves as a dedicated R&D center for testing new desalination solutions, reflecting Japan’s strategic focus on advanced, energy-efficient, and sustainable water treatment technologies.

Competitive Landscape – Key Players and Strategic Focus

The global water desalination equipment market is characterized by a mix of large multinational corporations and regional specialists competing on technology innovation, project execution scale, and operational efficiency.

ACWA Power – Expanding Mega-Scale BOT Desalination Projects

ACWA Power focuses on large Build-Operate-Transfer (BOT) desalination and power schemes involving integration of renewable energy to enhance sustainability. Its 109 assets in 15 nations have recently inked a number of deals including a green-powered largest-ever desalination scheme in Senegal for West Africa and a USD 10 billion desalination plant in Indonesia. The Kuwait megascheme solidifies MENA market dominance.

Veolia Environnement S.A. – Leader in Modular and Hybrid Desalination

Veolia targets ecological change, and it supplies MED, MSF, and RO technology with a special focus on mobile and module-based systems. Its introduction of PoIaris™ 2.0 and development of mobile RO services in Malaysia solidifies its footing in rapid-deployment and special applications. Advanced pretreatment technology incorporation by Veolia maximizes RO effectiveness and makes it a sought-after partner in complicated desalination applications.

SUEZ S.A. – Pioneer in Hybrid and Energy-Efficient Solutions

SUEZ delivers RO, nanofiltration, and thermal distillation products, but has a competitive advantage in hybrid desalination plants like those used at Ras Al-Khair, Saudi Arabia. Its worldwide presence and solid municipal–industrial customer base is reinforced by a concentration on energy efficiency and circular methodologies on water.

DuPont Water Solutions – Innovating High-Performance Membranes

DuPont is a global leader in separation and purification technology; FilmTecTM RO and NF membranes can be installed in municipal and industrial applications worldwide. New product introductions such as dry SWRO membrane elements provide installation ease and flexible operations. DuPont's part can be observed in a high-capacity, efficiency-driven desalination plan such as Israel's Sorek B project.

LG Chem – Advanced SWRO Membranes for Efficiency and Reliability

LG Chem applies material scientific knowledge to create energy-efficient SWRO membranes having a high level of salt rejection. Its collaboration with CaribDA to provide disaster relief in St. Vincent exhibits adaptability in implementing solutions to both commercial and disaster relief requirements. Further product innovation and collaborative strategies cement global market penetration.

Water Desalination Equipment Market Report Scope

Water Desalination Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.5 Billion

|

|

Market Size (2034)

|

$39.9 Billion

|

|

Market Growth Rate

|

9.6%

|

|

Segments

|

By Technology (Reverse Osmosis (RO) Systems, Multi-Stage Flash (MSF) Distillation, Multi-Effect Distillation (MED), Electrodialysis (ED/EDR)), By Capacity (Small-Scale (<5,000 m³/day), Medium-Scale (5,000-20,000 m³/day), Large-Scale (>20,000 m³/day)), By End-User (Municipal Sector, Industrial Sector, Commercial & Hospitality, Hotels, resorts, cruise ships, Military bases, Other Commercial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., ACCIONA, IDE Technologies, Aquatech International LLC, Evoqua Water Technologies (now part of Xylem), Abengoa S.A., Doosan Heavy Industries & Construction Co., Ltd., DuPont, Hitachi Ltd., Kurita Water Industries, VA Tech Wabag Ltd., Thermax Limited, Biwater Holdings Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Desalination Equipment Market Segmentation

By Technology

- Reverse Osmosis (RO) Systems

- Multi-Stage Flash (MSF) Distillation

- Multi-Effect Distillation (MED)

- Electrodialysis (ED/EDR)

- Emerging Technologies

- Forward Osmosis (FO)

- Membrane Distillation (MD)

- Solar Desalination

- Capacitive Deionization (CDI)

By Capacity

- Small-Scale (<5,000 m³/day)

- Medium-Scale (5,000-20,000 m³/day)

- Large-Scale (>20,000 m³/day)

By End-User

- Municipal Sector

- Industrial Sector

- •Power Generation

- •Oil & Gas

- •Mining

- •Food & Beverage

- •Pharmaceuticals

- •Pulp & Paper

- Commercial & Hospitality

- Hotels, resorts, cruise ships

- Military bases

- Other Commercial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Desalination Equipment Market

- Veolia

- SUEZ

- Xylem Inc.

- ACCIONA

- IDE Technologies

- Aquatech International LLC

- Evoqua Water Technologies (now part of Xylem)

- Abengoa S.A.

- Doosan Heavy Industries & Construction Co., Ltd.

- DuPont

- Hitachi Ltd.

- Kurita Water Industries

- VA Tech Wabag Ltd.

- Thermax Limited

- Biwater Holdings Limited

* List Not Exhaustive

Research Coverage

This report investigates the Global Water Desalination Equipment Market, offering analysis reviews of growth drivers, technological breakthroughs, and strategic investments shaping the industry. Published by USDAnalytics, it highlights how escalating water scarcity, innovation in energy-efficient reverse osmosis (RO) systems, and the emergence of hybrid desalination plants are driving large-scale adoption across municipal, industrial, and commercial applications. The study explores landmark government and private investments, renewable-powered desalination initiatives, and sustainability-focused solutions such as brine minimization and resource recovery. With in-depth insights on competitive strategies, capacity expansions, and emerging opportunities across high-demand regions such as the Middle East, North Africa, and Asia-Pacific, this report highlights innovation pathways, corporate positioning, and future-ready opportunities. This report is an essential resource for equipment providers, utilities, policymakers, and investors evaluating long-term prospects in the global water desalination equipment market.

Scope Includes:

- Segmentation: By Technology (RO, MSF, MED, Electrodialysis, Hybrid Systems), By Capacity (<5,000 m³/day, 5,000–20,000 m³/day, >20,000 m³/day), and By End-User (Municipal, Industrial, Commercial & Hospitality).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies: Profiles and analysis of 15+ leading players in the water desalination equipment industry.

Methodology

The research methodology adopted by USDAnalytics integrates both primary and secondary research to provide reliable and actionable insights. Primary data was collected through interviews with manufacturers, technology suppliers, government agencies, and end-users across municipal, industrial, and commercial sectors. Secondary research utilized company reports, regulatory publications, patent filings, and peer-reviewed journals to validate market dynamics. Market sizing and forecasts were developed using top-down and bottom-up approaches, reinforced by data triangulation and scenario analysis. Expert validation ensured that findings are consistent, accurate, and aligned with real-world industry developments, making this report a trusted reference for strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Desalination Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights

1.3. Global Market Snapshot

2. Water Desalination Equipment Market Overview, Size, and Growth Drivers (2025–2034)

2.1. Introduction to the Desalination Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $17.5 Billion

2.2.2. Forecasted Market Size (2034): $39.9 Billion at 9.6% CAGR

2.3. Market Drivers and Key Insights

2.3.1. Escalating Water Scarcity

2.3.2. Technological Innovations

2.3.3. Reverse Osmosis (RO) and Seawater Desalination

2.3.4. Growing Hybrid Systems

2.3.5. MENA as the Highest Adopter

3. Market Analysis: Strategic Developments and Investment Trends

3.1. Overview of Market Forces

3.2. Recent Strategic Investments and Projects

3.2.1. ACWA Power & GIC's Az-Zour North Megaproject

3.2.2. Veolia's PFAS Treatment Plant and PoIaris™ 2.0 Launch

3.2.3. Algeria's Desalination Plant Pledge

3.3. Technology and Humanitarian Developments

3.3.1. DuPont Membranes for Sorek B Desalination Plant

3.3.2. LG Chem's SWRO Membranes in Disaster Relief

3.4. Sustainability-Driven Innovation

3.4.1. ACWA Power's Shanghai Innovation Centre

4. Trends and Opportunities in Water Desalination Equipment Market

4.1. Trend 1: Shift to Renewable-Powered Desalination

4.1.1. Reducing Operational Costs and Environmental Footprint

4.1.2. Solar- and Wind-Powered Systems

4.2. Trend 2: Brine Minimization & Resource Recovery

4.2.1. Recovering Valuable Minerals from Brine

4.2.2. Converting Brine into a Revenue Stream

4.3. Opportunity 1: Small-Scale Modular Desalination for Islands

4.3.1. Rapidly Deployable and Cost-Effective Solutions

4.3.2. Benefits for Remote Islands and Communities

4.4. Opportunity 2: Industrial Desalination for Data Centers & Hydrogen

4.4.1. Ensuring Sustainable Water Supplies for High-Water-User Industries

4.4.2. Integrated Desalination and Waste Heat Utilization

5. Water Desalination Equipment Market Share Insights

5.1. By Technology

5.1.1. Reverse Osmosis (RO) Systems

5.1.2. Multi-Stage Flash (MSF) Distillation

5.1.3. Multi-Effect Distillation (MED)

5.1.4. Electrodialysis (ED/EDR)

5.2. By Capacity

5.2.1. Large-Scale Plants (>20,000 m³/day)

5.2.2. Medium-Scale (5,000–20,000 m³/day)

5.2.3. Small-Scale Modular Units (<5,000 m³/day)

5.3. By End-User

5.3.1. Municipal Sector

5.3.2. Industrial Sector

5.3.3. Commercial & Hospitality

6. Country Analysis of the Water Desalination Equipment Market

6.1. Saudi Arabia: Vision 2030 and RO Desalination

6.2. United Arab Emirates (UAE): Solar-Powered Desalination Initiatives

6.3. Israel: Global Leadership in Seawater Desalination

6.4. China: AI, Nuclear, and Advanced Membrane Technology

6.5. United States: Brackish Water Treatment and Public-Private Partnerships

6.6. Japan: Innovation in RO Membranes and Solar Desalination

6.7. Other Country Analysis (e.g., Algeria, Kuwait)

7. Water Desalination Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology, Capacity, and End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology, Capacity, and End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology, Capacity, and End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology, Capacity, and End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology, Capacity, and End-User

8. Company Profiles: Top Companies in Water Desalination Equipment Market

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. ACCIONA

8.5. IDE Technologies

8.6. Aquatech International LLC

8.7. Evoqua Water Technologies (now part of Xylem)

8.8. Abengoa S.A.

8.9. Doosan Heavy Industries & Construction

8.10. DuPont

8.11. Hitachi Ltd.

8.12. Kurita Water Industries

8.13. VA Tech Wabag Ltd.

8.14. Thermax Limited

8.15. Biwater Holdings Limited

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations