Zinc Chemicals Market Overview 2025–2034: $18.9 Billion to $31.7 Billion at 5.9% CAGR Anchored in Battery-Grade Zinc Oxide, Circular Sourcing, and High-Performance Coatings

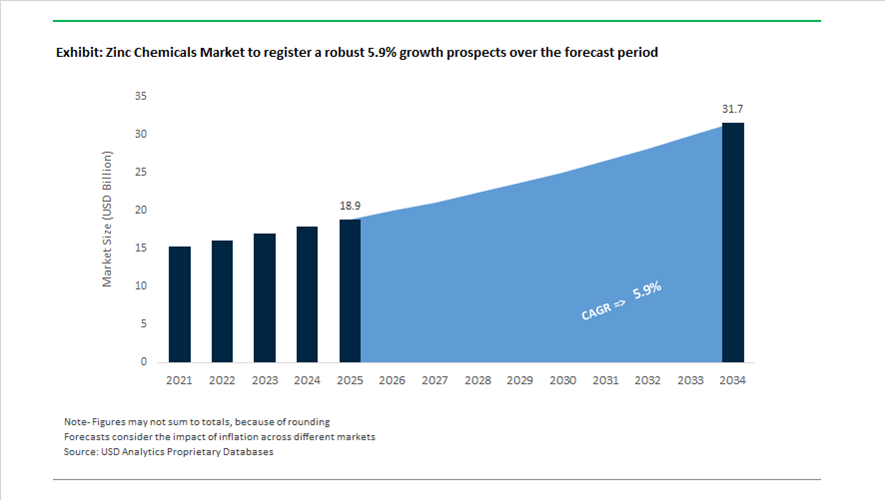

The Zinc Chemicals market is valued at $18.9 billion in 2025 and is projected to reach $31.7 billion by 2034, expanding at a CAGR of 5.9%. Zinc chemicals—including zinc oxide, zinc sulphate, zinc chloride, zinc carbonate, zinc stearate, and specialty zinc powders—serve critical roles across rubber vulcanization, agricultural micronutrients, pharmaceuticals, corrosion-resistant coatings, and increasingly, rechargeable battery systems. Market momentum is increasingly shaped by electrification, grid-scale storage deployment, sustainability mandates in automotive supply chains, and modernization of zinc smelting and refining infrastructure. Demand for high-purity and low-carbon zinc derivatives is redefining competitive positioning among producers.

Industry consolidation accelerated between 2024 and 2025. The integration of U.S. Zinc and EverZinc was finalized, creating a global zinc chemistry platform operating 14 facilities across North America, Europe, and Asia. In December 2025, EverZinc Corporation was acquired by affiliates of Cerberus Capital Management, providing capital to expand into rechargeable battery materials and high-value chemical segments. Zochem announced expansion of its Dickson, Tennessee facility, installing a low-carbon, high-output muffle furnace tailored for battery-grade zinc oxide production. In parallel, Grillo Chemicals restored operations at its Duisburg facility following a 2024 fire, commissioning a modernized sulfur dioxide plant to stabilize zinc sulphate supply into fertilizer and feed markets.

Battery ecosystem integration is a defining growth vector. In February 2026, registration opened for the R-Zinc 4.0 platform, underscoring commercialization momentum for rechargeable zinc battery technologies as safer and cost-competitive alternatives to lithium-ion systems for stationary storage. NextSource Materials advanced its UAE battery anode facility in February 2026, reflecting the growing role of zinc chemicals in Middle Eastern EV supply chains. Titan Mining reported record zinc output of 64.2 million pounds in 2025 while expanding into graphite concentrate production, signaling convergence between zinc mining and advanced battery material value chains. Nexa Resources’ 2026–2028 outlook highlighted improved Brazilian smelting stability, ensuring more consistent zinc oxide feedstock supply for chemical processors.

Sustainability and downstream diversification are strengthening structural demand. EverZinc’s 2023 Sustainability Report emphasized sourcing from third-party by-product streams, reducing reliance on virgin zinc and aligning with circular economy procurement standards required by Tier-1 automotive and pharmaceutical customers. Hindustan Zinc reported record revenues in early 2026 and maintained top ranking in the S&P Global Corporate Sustainability Assessment for metals and mining, reinforcing ESG-linked supply credibility. At PAINTINDIA 2026, Brenntag showcased eco-friendly zinc-based coatings delivering enhanced marine corrosion resistance while lowering environmental impact.

The zinc chemicals market is evolving toward battery-grade zinc oxide, circular raw material sourcing, low-carbon muffle furnace technologies, rechargeable zinc energy storage systems, and advanced anti-corrosion formulations. Electrification, agricultural micronutrient demand, pharmaceutical applications, and sustainable industrial coatings will collectively sustain mid-single-digit growth through 2034.

Technology-Driven Trends and High-Conviction Opportunities in the Zinc Chemicals Market

Trend 1: Strategic Reformulation Toward High-Efficiency, Nanoscale Micronutrients

Agrochemical formulators are rapidly moving away from conventional zinc sulfate toward nanostructured zinc oxide (ZnONPs) and chelated zinc formulations such as Zinc-EDTA, driven by efficiency, regulatory pressure, and nutrient-use optimization.

A September 2025 peer-reviewed study published in Catalysts demonstrated that wheat and barley seeds treated with biosynthesized ZnONPs achieved 100% germination, compared with 65–68% for chlorine-treated effluents. The same trials recorded 30–50% increases in shoot and root length, confirming that nanoscale zinc delivers materially higher bioavailability at significantly lower application dosages.

From a policy and compliance standpoint, the OECD-FAO Agricultural Outlook 2025–2034 underscores the need for a 15% productivity improvement by 2034 to address global undernourishment. This is accelerating the adoption of Zinc-EDTA, which offers superior solubility, compatibility with fertigation and drip irrigation systems, and lower risk of soil accumulation and runoff compared to zinc sulfate. As a result, zinc chelates are increasingly positioned as regulatory-compliant micronutrients for precision and climate-resilient agriculture.

Trend 2: Performance Intensification via Nano-Zinc Activators in Rubber and Tires

The tire and rubber industry is intensifying its reliance on high-surface-area and surface-treated zinc oxides to meet durability, efficiency, and sustainability benchmarks, particularly in electric vehicle applications.

According to March 2025 industry data from Smithers, the tire sector accounts for approximately 50% of global zinc oxide consumption. To comply with stricter tire labeling and rolling resistance standards, manufacturers are shifting toward Active Zinc Oxide, which delivers superior dispersion and vulcanization efficiency. This enables a reduction in zinc loading levels without compromising tensile strength, abrasion resistance, or heat stability.

Technical evaluations released in December 2025 confirm that nanostructured ZnO enables faster vulcanization cycles and improved aging resistance, a critical requirement for EV tires that must endure higher torque, greater vehicle mass, and elevated operating temperatures. This trend structurally favors suppliers capable of delivering controlled-particle-size, low-impurity zinc oxides tailored for advanced rubber compounding.

Opportunity 1: High-Purity Zinc Compounds for Water-Based Anticorrosion Coatings

The global shift toward low-VOC and water-based protective coatings is creating sustained demand for zinc-based anticorrosive pigments, particularly zinc phosphate and its advanced derivatives.

By November 2025, water-based anticorrosion coatings maintained an estimated USD 9 billion market footprint, driven by bridge rehabilitation, marine infrastructure upgrades, and energy asset protection. High-purity zinc phosphate has become the preferred pigment due to its ability to form a stable galvanic barrier while avoiding the environmental and regulatory liabilities associated with chromate-based systems.

The expansion of offshore wind, solar frames, and transmission infrastructure is further accelerating demand, with zinc-based coating consumption growing at 15–20% annually in renewable energy applications. In saline and high-humidity environments, materials such as zinc hydroxyphosphite and nano-enhanced zinc pigments are increasingly specified for long-term corrosion resistance, positioning high-purity zinc chemicals as mission-critical materials for infrastructure longevity.

Opportunity 2: Scaling Zinc-Based Chemistries for Grid-Scale Battery Storage

The push for safer, non-flammable energy storage solutions is bringing aqueous zinc-ion batteries (aq-ZIBs) into commercial focus, unlocking a high-growth avenue for high-purity zinc chemicals.

In September 2024, Enerpoly inaugurated a landmark zinc-ion battery manufacturing facility in Sweden, targeting 100 MWh of annual capacity by 2026. The plant relies on high-purity zinc electrolytes and anode materials, positioning zinc chemicals as the backbone of a European, lithium-independent stationary storage supply chain.

On the technology front, researchers at the University of Technology Sydney reported in June 2025 that aqueous zinc-ion systems achieved over 5,000 stable charge-discharge cycles, addressing historical concerns around dendrite formation and electrolyte degradation. This progress, combined with U.S. Department of Energy funding announcements in January 2025 for next-generation battery materials, signals a structurally durable growth opportunity for producers of battery-grade zinc chloride and zinc acetate.

Zinc Chemicals Market Share and Segmentation Insights

Product Type Market Share: Zinc Oxide Leads with Versatility in Rubber, Coatings, and Personal Care Applications

Zinc oxide holds a 42.8% share in the zinc chemicals market in 2025, driven by its multifunctional role in rubber compounding, anticorrosive coatings, ceramics, and personal care formulations such as sunscreens. Its effectiveness as a vulcanization activator and pigment supports widespread industrial adoption. Zinc sulfate, zinc stearate, zinc chloride, chelated zinc, and other derivatives serve specialized applications across agriculture, chemicals, and manufacturing. A key trend is the strong linkage to tire industry demand, where global automotive production and replacement cycles sustain zinc oxide consumption, alongside growing adoption of nano-zinc oxide in advanced applications requiring enhanced reactivity and performance.

Application Market Share: Rubber Compounding Leads with Global Tire Production and Vulcanization Demand

Rubber compounding and vulcanization account for 38.6% of the zinc chemicals market in 2025, reflecting the essential role of zinc oxide in sulfur curing systems used in tire manufacturing and industrial rubber products. Paints and coatings, agriculture, chemical intermediates, ceramics, pharmaceuticals, textiles, and energy storage applications contribute to diversified demand. A key market trend is zinc oxide particle size optimization, where nano and coated grades enable improved dispersion, higher reactivity, and reduced zinc usage while maintaining performance. This supports environmental compliance and enhances tire durability, aligning with evolving performance and sustainability requirements in the rubber industry.

Zinc Chemicals Market Competitive Landscape

The Zinc Chemicals market in 2026 is shaped by operational decarbonization and value-added specialization, with manufacturers focusing on low-carbon zinc oxide production, nano-dispersions, and surface-treated ZnO for cosmeceuticals, pharmaceuticals, and advanced coatings, while integrating circular economy models and renewable energy sourcing.

EverZinc Expands Specialty Zinc Portfolio with Global Footprint and Battery-Grade Innovation

EverZinc continues to lead the specialty zinc chemicals market through its diversified high-performance product portfolio and global manufacturing footprint. The December 2025 acquisition by Cerberus Capital Management has strengthened capital access for expansion into rechargeable zinc batteries and specialty coatings. With 12 production sites across North America, Europe, and Asia, the company ensures supply chain resilience for its Zano® ultra-fine zinc oxide used in sunscreens and advanced formulations. EverZinc’s leadership in organizing R-Zinc 4.0 highlights its influence in next-generation energy storage applications. Its product range spans corrosion-resistant zinc powders to nano-scale ZnO dispersions. This multi-segment specialization enables strong positioning in high-margin, non-commodity zinc chemicals.

Hindustan Zinc Leads Low-Carbon Zinc Transformation with EcoZen and Digital Market Access

Hindustan Zinc Limited dominates the global zinc chemicals value chain through scale, integration, and sustainability leadership. The company reported record Q3 FY2026 performance with US$440 million PAT and 270 kt refined metal output, supported by smelter debottlenecking. Its EcoZen low-carbon zinc brand, with emissions below 1 tonne CO2 per tonne, sets a new benchmark for green zinc chemicals. The launch of Zinc Moolya digital marketplace enhances pricing transparency and MSME access. Strategic investment in zinc tailings recycling with CIMIC strengthens circular resource recovery. This integration of digitalization and decarbonization reinforces HZL’s leadership in sustainable zinc oxide and derivative markets.

Zochem Strengthens North American Supply with Low-Carbon Furnace Expansion and Battery Market Focus

Zochem is advancing its leadership in French Process zinc oxide through sustainability-driven capacity expansion in North America. The installation of a low-carbon muffle furnace at its Tennessee facility adds 15,000 metric tons capacity, targeting battery storage and agriculture sectors. Its use of conductive refractory and low-NOx burners improves carbon efficiency metrics, aligning with ESG-driven procurement standards. The company is diversifying into zinc sulfate and fertilizer-grade products using Waelz oxide feedstocks. Proximity to the US Battery Belt and Great Lakes manufacturing hubs ensures logistical efficiency. This positions Zochem as a preferred supplier for automotive, chemical, and energy storage industries.

Silox India Drives Active Zinc Oxide Innovation with Low-Carbon Feedstock Integration

Silox India is emerging as a key player in high-performance zinc chemicals through its focus on active-grade zinc oxide and sustainable sourcing. The ₹300–360 crore Dahej expansion project aims to scale inorganic chemical production capacity. Its adoption of EcoZen low-carbon zinc significantly reduces product carbon footprint across its portfolio. Active ZnO products enable up to 40% dosage reduction in rubber and tire manufacturing, enhancing cost and environmental efficiency. The company is capitalizing on supply gaps created by competitor exits in hydrosulfide segments. This strategic positioning strengthens its role in specialty zinc derivatives and industrial applications.

Grillo-Werke Advances Circular Zinc Chemistry with Energy Storage and Recycling Integration

Grillo-Werke is reinforcing its position in the European zinc chemicals market through circular economy integration and advanced material innovation. Its EcoVadis Bronze and RIGK certifications validate its sustainable and transparent production practices. The company is developing scalable zinc-air battery systems for megawatt-level energy storage, targeting EV and grid applications. Registration of zinc sulphate monohydrate in the QS database enhances its credibility in food and agricultural sectors. Collaboration with Aurubis AG supports efficient zinc recovery from secondary raw materials. This closed-loop model strengthens Grillo’s footprint in sustainable zinc chemicals and energy storage solutions.

India Zinc Chemicals Market Anchored by Infrastructure Spend and Value-Added Shift

India’s zinc chemicals market reached an inflection point in FY2025, underpinned by record upstream availability and a decisive pivot toward higher-value downstream products. Hindustan Zinc Limited reported its highest-ever domestic zinc sales at 603 kt for the fiscal year ending March 2025, marking a 4% year-on-year increase. This surge was closely linked to aggressive infrastructure-led galvanization demand across highways, railways, and large bridge projects. The Union Budget 2025–26 reinforced this trajectory by allocating ₹11.20 trillion toward capital expenditure, structurally embedding zinc-intensive steel and corrosion-protection systems into national development plans. At the same time, India’s refined zinc consumption climbed to 783 kt in FY2025, outpacing domestic supply growth and signaling a clear requirement for additional zinc chemical processing capacity, particularly within PCPIR-linked industrial corridors.

A notable structural upgrade is underway in product mix. Sales of zinc value-added products reached a historic peak of 179 kt in early 2025, now representing 22% of primary zinc volumes. This shift is strategically aligned with the National Manufacturing Mission launched in 2025, which explicitly incentivizes domestic production of EV battery-grade zinc chemicals and inputs for solar PV cell manufacturing. From a cost perspective, the moderation of LME zinc prices to around $2,887 per tonne in March 2025 provided chemical producers with a favorable window to secure feedstock for agricultural zinc sulfate and micronutrient formulations. Collectively, these dynamics position India as both a high-growth consumption market and an emerging manufacturing hub for advanced zinc chemicals.

United States Zinc Chemicals Market Driven by Energy Storage and Reshoring Mandates

The United States zinc chemicals market is increasingly defined by long-duration energy storage deployment and supply chain localization policies. In July 2025, Eos Energy Enterprises reported a 243% year-on-year revenue increase, driven by commercial rollouts of zinc hybrid cathode batteries for grid-scale long-duration energy storage. This momentum has been reinforced by fiscal policy. The 2025 budget reconciliation legislation preserved the Section 45X production tax credit, allowing zinc battery manufacturers to claim up to $45 per kWh, with an additional 10% incentive for electrode active materials. These measures materially improve the economics of zinc-based chemistries relative to lithium-ion alternatives.

Federal financing support is accelerating capacity build-out. The Department of Energy Loan Programs Office committed $277 million toward expanding domestic zinc battery manufacturing, with over $68 million drawn down by Q2 2025. Beyond energy storage, agricultural demand remains a stable growth pillar. U.S. consumption of agriculture-grade zinc chemicals, particularly chelated zinc for precision foliar application, is projected to reach $93.9 million by late 2025. Importantly, new 2025 federal rules restricting incentives for projects sourcing from foreign entities of concern have triggered active reshoring of zinc oxide and zinc sulfate production from overseas suppliers. This policy-driven realignment is reshaping the U.S. zinc chemicals landscape toward domestic, traceable supply chains.

China Zinc Chemicals Market Shaped by Green Smelting and Regulatory Tightening

China’s zinc chemicals market is evolving under a dual mandate of industrial upgrading and regulatory enforcement. The Petrochemical Stable Growth Plan for 2025–2026, jointly issued by seven ministries, targets 5% annual growth in chemical sector value added, explicitly prioritizing high-end derivatives over basic refining. Zinc chemicals feature prominently within this agenda, particularly battery-grade salts and specialty oxides. Parallel regulatory pressure is intensifying. The second draft of the Hazardous Chemicals Safety Law released in September 2025 introduces stricter registration, labeling, and compliance requirements for zinc chemical producers and importers, with full enforcement scheduled for 2026.

Sustainability and circularity are becoming central themes. China’s non-ferrous metals roadmap for 2025–2026 emphasizes green smelting technologies for complex ores and supports the creation of recycling bases for zinc recovered from spent power batteries. Beijing has set an explicit target to lift domestic self-sufficiency for strategic chemical intermediates, including battery-grade zinc salts, above 90% by the end of 2026. Operational efficiency is also being addressed through digitalization. The Ministry of Industry and Information Technology has mandated AI-driven process optimization investments across Shandong’s zinc chemical clusters to reduce energy intensity in the French Process used for zinc oxide production. These measures collectively signal a transition from volume-driven output to regulated, technology-intensive zinc chemical manufacturing.

European Union Zinc Chemicals Market Led by Germany’s Regulatory and Defense Spend

Within the European Union, Germany is emerging as the principal driver of zinc chemicals demand through infrastructure, defense, and regulatory reform. Germany’s €500 billion investment package for 2025–2027 is expected to underpin approximately 2.9% annual growth in regional zinc chemical consumption, particularly for protective coatings used in transport, energy, and defense infrastructure. At the same time, regulatory changes are reshaping product specifications. New EU legislation on Maximum Residue Levels for agricultural products, fully applicable in 2026, is forcing zinc fertilizer manufacturers to deliver higher-purity, low-heavy-metal formulations to remain compliant.

Environmental regulation is further tightening usage patterns. Updates to the Water Framework Directive effective in 2026 impose stricter controls on zinc enrichment in soil and water, accelerating adoption of smart-release zinc granules that minimize runoff and bioaccumulation. On the compliance front, the International Zinc Association is coordinating the 2026 update of Zinc REACH Consortium dossiers, incorporating the latest bioavailability and toxicity data for industrial zinc salts. This process is raising documentation and testing thresholds, favoring suppliers with strong regulatory capabilities and reinforcing Germany’s position as a standards-setting market for zinc chemicals in Europe.

Zinc Chemicals Market Country Snapshot

Zinc Chemicals Market County Level Snapshot

|

Region / Country

|

Primary Growth Driver

|

Key Zinc Chemical Applications

|

Strategic Market Direction

|

|

India

|

Infrastructure capex and manufacturing incentives

|

Galvanization, fertilizers, EV-grade salts

|

Value-added expansion and capacity build

|

|

United States

|

Energy storage policy and reshoring mandates

|

Zinc batteries, chelated micronutrients

|

Domestic supply chain reinforcement

|

|

China

|

Green smelting and regulatory enforcement

|

Battery-grade salts, zinc oxide

|

High-end, self-sufficient production

|

|

European Union (Germany)

|

Defense spend and environmental regulation

|

Protective coatings, smart fertilizers

|

Compliance-led, high-purity focus

|

Zinc Chemicals Market Report Scope

Zinc Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.9 Billion

|

|

Market Size (2034)

|

$31.7 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Product Type (Zinc Oxide, Zinc Sulfate, Zinc Carbonate, Zinc Chloride, Zinc Stearate, Chelated Zinc, Other Zinc Derivatives), By Form (Powder, Granular, Liquid, Pellets), By Application (Rubber Compounding and Vulcanization, Agriculture and Animal Feed, Paints and Anticorrosive Coatings, Ceramics and Glass Manufacturing, Pharmaceuticals and Cosmetics, Chemical Intermediates and Catalysts, Energy Storage and Batteries, Textiles and Leather Tanning)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hindustan Zinc Limited, U.S. Zinc, EverZinc, Zochem Inc., Umicore N.V., Sinopec Corporation, BASF SE, Old Bridge Chemicals, Inc., TIB Chemicals AG, Global Chemical Co., Ltd., Hongshen Zinc Corporation, Eos Energy Enterprises, Zinc Nacional, Hakusuitech Co., Ltd., Pan-Continental Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Zinc Chemicals Market Segmentation

By Product Type

- Zinc Oxide

- Zinc Sulfate

- Zinc Carbonate

- Zinc Chloride

- Zinc Stearate

- Chelated Zinc

- Other Zinc Derivatives

By Form

- Powder

- Granular

- Liquid

- Pellets

By Application

- Rubber Compounding and Vulcanization

- Agriculture and Animal Feed

- Paints and Anticorrosive Coatings

- Ceramics and Glass Manufacturing

- Pharmaceuticals and Cosmetics

- Chemical Intermediates and Catalysts

- Energy Storage and Batteries

- Textiles and Leather Tanning

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Zinc Chemicals Market

- Hindustan Zinc Limited

- U.S. Zinc

- EverZinc

- Zochem Inc.

- Umicore N.V.

- Sinopec Corporation

- BASF SE

- Old Bridge Chemicals, Inc.

- TIB Chemicals AG

- Global Chemical Co., Ltd.

- Hongshen Zinc Corporation

- Eos Energy Enterprises

- Zinc Nacional

- Hakusuitech Co., Ltd.

- Pan-Continental Chemical Co., Ltd.

- *- List not Exhaustive

*- List not Exhaustive