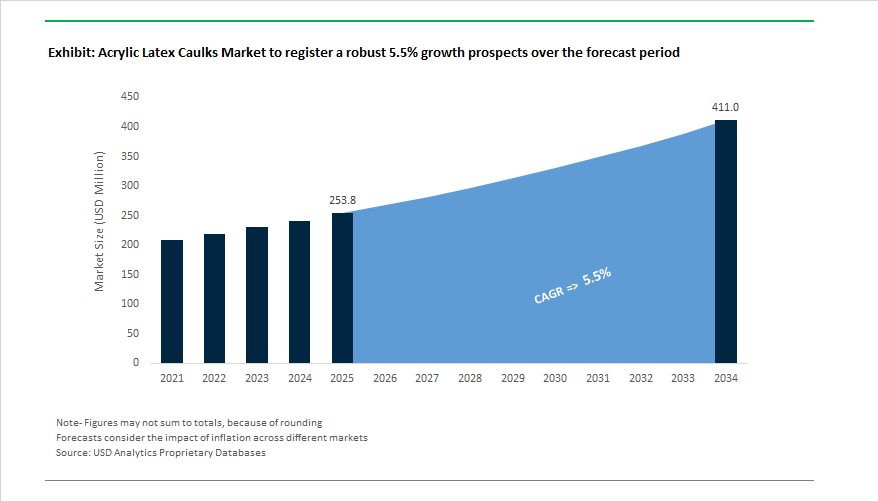

The global acrylic latex caulks market is expected to grow from USD 253.8 million in 2025 to USD 410.9 million by 2034, advancing at a 5.5% CAGR, supported by the structural shift toward water-based construction materials, low-VOC compliance, and interior finishing demand. From a manufacturer’s standpoint, acrylic latex caulks occupy a critical volume segment within the sealants portfolio—serving as the default solution for paintable, non-structural, interior sealing applications where ease of application, regulatory compliance, and cost efficiency are paramount.

Unlike silicone and polyurethane systems that compete on extreme performance, acrylic latex caulks are fundamentally chemistry-led volume products, formulated around waterborne acrylic emulsions that align directly with architectural coatings ecosystems. Major sealant and coatings manufacturers consistently position acrylic latex caulks as extension products of interior paint systems, enabling seamless paint adhesion, low odor, and water cleanup—features that strongly influence contractor preference and DIY adoption. This tight coupling with water-based paints structurally insulates acrylic latex caulks from substitution risk in interior construction and renovation cycles.

Regulatory compliance is another core demand anchor. Manufacturers have progressively reformulated acrylic latex caulks to meet stringent VOC thresholds, positioning them as default compliant sealants for residential and commercial interiors across North America, Europe, and parts of Asia-Pacific. Unlike solvent-based or reactive chemistries, acrylic latex systems allow formulators to meet regulatory limits without major cost penalties or processing complexity, preserving margins while maintaining scale.

From an application standpoint, demand remains concentrated in windows, doors, trim, drywall joints, baseboards, and siding transitions, where movement requirements are moderate and paintability is non-negotiable. Growth is therefore tied less to speculative infrastructure cycles and more to steady renovation activity, housing turnover, and interior refurbishment, especially in urban and suburban markets. For manufacturers, this translates into predictable, repeat-volume demand, high SKU turnover through retail and professional channels, and strong brand loyalty driven by contractor familiarity rather than specification-led procurement.

Key Industry Insights:

- Acrylic latex caulks are structurally linked to water-based architectural paint systems, reinforcing long-term demand stability rather than cyclical volatility.

- Low-VOC and low-odor compliance is no longer a differentiator but a baseline requirement shaping formulation strategy and raw material selection.

- Interior construction and renovation, not heavy infrastructure, remain the primary demand engines, favoring high-volume, cost-optimized production models.

- Paintability and application ease continue to outweigh extreme elasticity or weather resistance in purchasing decisions for acrylic latex caulks.

- Raw material exposure is concentrated in acrylic emulsions and additives, making supply security and formulation efficiency key competitive levers for manufacturers.

The Acrylic Latex Caulks Market is witnessing a robust wave of innovation and strategic restructuring as manufacturers respond to environmental mandates, raw material inflation, and infrastructure-driven demand. Over the past two years, industry developments have underscored a clear pattern—companies are emphasizing sustainability, cost competitiveness, and geographic expansion to capture emerging construction markets.

In February 2024, Mallard Creek Polymers introduced a next-generation water-based acrylic emulsion designed for functional barrier coatings, offering superior resistance to oil and grease. This innovation supports the evolution of high-performance acrylic latex caulk formulations tailored for demanding environments such as kitchen joints and food-contact applications, where durability and safety are paramount. Similarly, Henkel’s February 2023 product line expansion showcased new environmentally friendly caulks and sealants, underlining its commitment to sustainable, high-adhesion acrylic technologies in the construction sector.

The collaborative landscape has also shifted—Jesons Industries Limited partnered with Alberdingk Boley in July 2024, signaling a push into the polyurethane dispersions market in India. This expansion may reshape competition by introducing hybrid sealants that challenge pure acrylic latex caulks in flexibility and movement capability. On the policy front, the Government of India’s January 2025 infrastructure budget of USD 133 billion—including 1.18 crore sanctioned PMAY-U housing units—is expected to accelerate mass demand for low-cost, water-based caulks throughout Asia-Pacific’s construction ecosystem.

Additionally, rising input costs have realigned competitive pricing strategies. In Q3 2024, Dow Chemical announced a 5–10% increase in silicone spot prices, driven by chlor-alkali supply constraints. This development indirectly benefits acrylic latex caulk manufacturers, as cost-sensitive contractors shift toward affordable, non-structural acrylic alternatives. Meanwhile, Arkema’s May 2024 focus on synthetic latex R&D has advanced self-crosslinking acrylic systems, improving scrub resistance and durability—crucial for interior caulks in high-traffic areas.

Regulatory dynamics remain central to industry growth. In October 2024, North American manufacturers re-engineered formulations to meet VOC limits as low as 50 g/L, reaffirming the role of low-odor acrylic sealants as the compliant market standard. Lastly, in September 2025, Sika AG expanded its sealant production capacity in Southeast Asia, strengthening supply for fast-growing urban construction markets and aligning with regional infrastructure booms.

The transition toward low-VOC and VOC-free acrylic latex caulks has become one of the most defining shifts in the industry. With global regulatory tightening and increased awareness of indoor air quality, manufacturers are prioritizing environmentally responsible formulations. The transformation is being driven by the U.S. Environmental Protection Agency (EPA), whose emission standards (40 CFR Part 59) cap VOC content at 250 grams per liter for caulks and sealants. As a result, leading producers are reengineering product lines to comply with these limits without compromising performance.

Sherwin-Williams’ 2023 corporate sustainability report reported that more than 90% of its architectural paint and coating products sold in the U.S. and Canada are already low-VOC, and the company continues to expand the compliance across its caulk portfolio. Similarly, Momentive Performance Materials introduced VOC-compliant MS-polymer hybrid sealants tailored for regions like California, which enforce the strictest CARB standards. Henkel, through its "Purposeful Growth" strategy, allocated over half its R&D budget toward solvent-free technologies, signaling a deep corporate commitment to sustainability. The outcome is a new generation of acrylic latex caulks that deliver high adhesion and durability while aligning with green building certification programs such as LEED and BREEAM.

Another transformative trend in the acrylic latex caulks industry is the integration of advanced polymer systems designed to rival the performance of silicones and polyurethanes. Manufacturers are heavily investing in new acrylic dispersions, hybrid resins, and crosslinking systems to enhance elongation, flexibility, and adhesion in variable environmental conditions.

Dow Chemical’s 2023 breakthrough in acrylic binder technology demonstrated a 40% increase in elongation-at-break, addressing the common issue of cracking in traditional formulations. BASF’s €100 million expansion in China to boost acrylic dispersion production underscores the growing demand for premium, performance-based sealants in high-growth Asian construction markets. Similarly, 3M’s “Advanced Acrylic Sealant” introduced proprietary polymer blends capable of maintaining flexibility from -26°C to 82°C, achieving temperature resistance once limited to silicone-based products. Arkema’s acquisition of Ashland’s performance adhesives business further reflects a global shift toward high-durability, acrylic-based technologies.

As building envelopes increasingly demand longer lifespans and energy efficiency, these polymer advancements are enabling acrylic caulks to occupy a more dominant share in both residential and commercial applications. Enhanced tensile strength, UV stability, and substrate compatibility serve as differentiating performance metrics, allowing manufacturers to market acrylic latex caulks as viable, cost-efficient alternatives to premium elastomeric sealants.

The growing global emphasis on energy efficiency and infrastructure modernization is creating sustained growth opportunities for acrylic latex caulk producers. The U.S. Department of Energy (DOE), under the Biden-Harris Administration, allocated $250 million in 2023 toward building energy retrofits, directly stimulating demand for air-sealing solutions. The Inflation Reduction Act’s $4.3 billion rebate initiative (Section 50132) incentivizes whole-home efficiency upgrades, including caulking and weatherproofing—core applications for acrylic latex products.

Similarly, the $3.2 billion Weatherization Assistance Program (WAP) ensures ongoing consumption of sealants for cost-effective energy conservation in low-income housing. Across the Atlantic, the European Union’s Renovation Wave strategy aims to double annual renovation rates by 2030, extending the opportunity for acrylic caulks in high-volume sealing applications.

Manufacturers who align product development with these infrastructure and energy programs stand to benefit from multi-billion-dollar procurement channels. OEM partnerships, government supply contracts, and B2B retrofit programs are emerging as lucrative channels for high-volume acrylic sealant producers in both developed and developing markets.

Beyond the mass-market caulk segment, manufacturers are increasingly targeting professional-grade, niche applications that demand superior technical attributes and command premium pricing. The trend toward specialization enables companies to differentiate themselves in a commoditized market by addressing performance-specific requirements in construction, remodeling, and OEM manufacturing.

Sherwin-Williams’ “High Hide” and “Painter’s Caulk” lines have proven the profitability of specialized, immediate-paintability formulations, contributing to mid-single-digit segment growth above the market average. DuPont’s antimicrobial silicone-acrylic hybrid “Tile & Tub” sealant with Microban® technology demonstrates how functional additives can expand into bathroom and kitchen sealing applications, projected to capture 15% of the moisture-resistant segment by 2025. Similarly, PPG Industries’ collaboration with a leading window OEM for co-branded, color-matched acrylic sealants highlights how B2B partnerships are redefining value creation through tailored solutions.

GCP Applied Technologies’ R&D investments into low-shrinkage and fast-skinning formulations further highlight how innovation is pivoting toward contractor-driven usability improvements. The niche-focused approach supports both retail and industrial channels by combining enhanced aesthetics, faster curing, and application-specific functionality—ultimately redefining how the acrylic latex caulk market captures premium value across sectors.

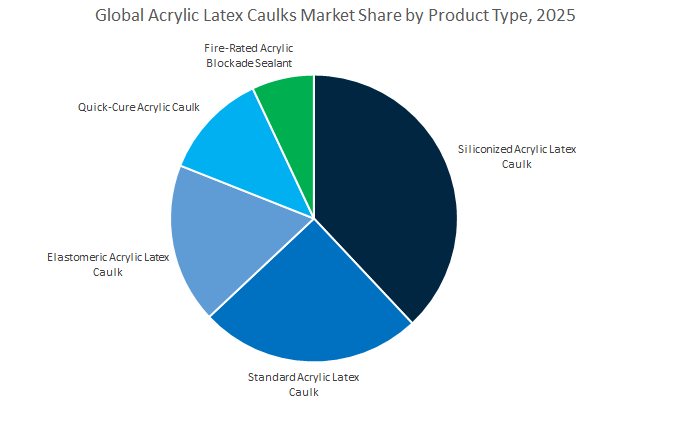

The siliconized acrylic latex caulk segment dominates the global acrylic latex caulks industry, accounting for an estimated 38% market share in 2025. This dominance stems from its balanced performance characteristics that offer the smooth application, easy cleanup, and paintability of acrylic latex with the superior adhesion and flexibility of silicone-based sealants. These hybrid formulations have become the preferred choice among both professional contractors and DIY enthusiasts for versatile use across interior and exterior sealing, window and door installations, and general construction projects. The growing global focus on durable, long-lasting sealants for moisture-prone environments, particularly in kitchen and bathroom renovation activities, further reinforces the segment’s leadership. Continuous innovation in UV-resistant and low-VOC siliconized caulks has also strengthened its share in the sustainable construction market.

The standard acrylic latex caulk segment, with around 25% share, maintains strong relevance due to its cost-efficiency and widespread availability. It continues to be a staple in low-stress interior applications, such as sealing minor wall cracks, joints, and trim work in residential environments. Its water-based nature, compatibility with a wide range of paints, and easy application process align with the growing DIY repair culture across developed and emerging markets. While it lacks the advanced weather resistance of premium types, its affordability ensures consistent volume demand, in particular, especially in regions with moderate climates and active home improvement retail channels.

The elastomeric acrylic latex caulk segment, projected at 18%, represents one of the fastest-growing, high-value categories within the market. These advanced sealants are often urethane-modified and provide superior elasticity and resilience under structural movement and temperature fluctuations. As infrastructure projects and smart buildings increasingly demand flexible, long-lasting sealants, elastomeric formulations are gaining traction among commercial developers. Moreover, the segment benefits from regulatory pressures emphasizing weatherproofing and air-sealing efficiency, particularly in North America and Europe, positioning it as a key growth engine for premium-grade caulks.

The residential building and DIY segment leads the global acrylic latex caulks market with an estimated 45% market share in 2025, reflecting the dominant role of the housing and home improvement sectors. The surge in renovation activities, particularly across North America and Europe, continues to fuel demand for easy-to-use, low-odor, paintable caulks. The DIY culture, accelerated by digital tutorials and e-commerce accessibility, has empowered homeowners to undertake small repair projects independently. Additionally, the post-pandemic preference for energy-efficient and aesthetic upgrades has further boosted consumption. The proliferation of eco-friendly, low-VOC caulks also resonates with environmentally conscious consumers, ensuring continued growth of this segment in the sustainable home improvement market.

The commercial building and construction segment, accounting for nearly 30%, represents the backbone of industrial demand. With the revival of office, retail, and institutional infrastructure projects, this sector heavily relies on acrylic latex caulks for façade joints, curtain walls, flooring, and drywall installations. Builders prefer siliconized and elastomeric variants for their flexibility and weather resistance, essential for maintaining long-term performance in large-scale structures. The adoption of green building standards and LEED-certified projects is driving greater use of low-emission sealants, positioning acrylic latex caulks as key contributors to sustainable commercial development. As construction rebounds in Asia-Pacific and the Middle East, the segment is expected to remain a major revenue generator.

The industrial segment, with an estimated 15% share, provides a stable base of demand rooted in HVAC systems, equipment assembly, and pipeline sealing applications. Industrial users prioritize functional properties such as high temperature tolerance, chemical resistance, and adhesion to diverse substrates. Although price sensitivity is higher compared to construction markets, manufacturers are focusing on customized, performance-grade acrylic caulks to capture industrial OEM and maintenance opportunities. The ongoing modernization of manufacturing facilities and rising demand for energy-efficient insulation systems further enhance this segment’s long-term stability.

The competitive landscape of the global acrylic latex caulks market is characterized by a blend of multinational chemical leaders and specialized sealant manufacturers pursuing sustainable product innovation, strategic acquisitions, and channel integration. Companies such as Henkel, Sherwin-Williams, H.B. Fuller, DAP Products, Franklin International, and Sika AG dominate through strong distribution networks, advanced R&D capabilities, and tailored product offerings that address both professional construction and DIY consumer markets.

Henkel remains a front-runner in the acrylic latex caulks industry, with brands like OSI and Loctite delivering high-performance and general-purpose sealants for diverse construction needs. Leveraging its global R&D leadership and extensive distribution network, Henkel’s focus on bio-based and low-VOC adhesives aligns with tightening environmental standards. Its February 2023 launch of durable, eco-friendly caulks reinforced its market dominance in sustainable construction sealants, while its vertically integrated operations ensure efficient supply across both professional and DIY channels.

Through brands such as DAP and Krylon, Sherwin-Williams offers one of the most comprehensive ranges of interior and exterior acrylic latex caulks. The company’s strength lies in architectural coatings compatibility, making it a top choice for professional painters and contractors. In late 2021, it implemented a 4% surcharge on its sealant portfolio to counteract raw material cost inflation. Sherwin-Williams’ control over its retail distribution network, including dedicated outlets, provides a powerful direct-to-pro and DIY sales advantage unmatched in the sector.

H.B. Fuller continues to focus on specialty, high-performance sealant systems based on acrylic dispersion technology. The company’s strategy of innovation through acquisition and targeted R&D ensures relevance across industrial, packaging, and infrastructure applications. Its commitment to sustainability and flexibility performance allows it to serve niche markets where high-flex, low-shrink caulks are essential. Strong integration with industrial B2B customers enhances Fuller’s ability to deliver tailored adhesive-sealant systems.

DAP Products Inc. specializes in general-purpose and professional-grade acrylic latex caulks, serving both consumer and contractor segments. Its wide retail distribution across North America ensures exceptional accessibility, while its continuous product innovation targets weatherability, flexibility, and ease-of-use. The company’s emphasis on paintable and water-based sealants positions it as a leading brand in home improvement and light construction markets, sustaining strong visibility among DIY users.

Franklin International is known for producing adhesives, polymers, and sealants that often serve private-label and industrial clients. With deep expertise in polymer chemistry and a strong reputation for quality control, Franklin caters to LEED and BREEAM-certified projects, aligning with global green building initiatives. Its integration within the industrial and OEM supply chain reinforces its role as a trusted provider of bulk acrylic latex sealant polymers to manufacturers and construction brands.

While Sika AG’s portfolio is heavily skewed toward polyurethane and silicone systems, its growing range of acrylic-based construction sealants demonstrates its adaptability. With a global presence and a strong foothold in weatherproofing and concrete repair solutions, Sika’s September 2025 expansion in Southeast Asia strengthens its ability to cater to infrastructure-driven demand. The company’s direct-to-contractor approach and bundling strategy enhance its competitiveness in both premium and economical acrylic caulk segments.

The United States acrylic latex caulks market continues to evolve as stringent environmental regulations and a mature DIY/construction culture fuel widespread adoption of low-VOC and high-performance acrylic sealant solutions. With the U.S. leading in synthetic latex polymer innovation, over 38% of new formulations in the coatings sector are water-based, reflecting a decisive industry shift toward eco-compliant building materials. The Environmental Protection Agency (EPA) and state-level emission standards have further accelerated the trend, prompting companies to enhance adhesion, flexibility, and weather resistance while minimizing VOC emissions.

Research and development remain the backbone of the U.S. market. 3M Company, a global pioneer in adhesives, has actively explored nanotechnology-enabled self-healing sealants, potentially redefining the durability expectations in acrylic caulks. Meanwhile, Illinois Tool Works (ITW) has strategically expanded its sealant manufacturing capacity through acquisitions, strengthening its specialty portfolio for both construction and automotive segments. The consolidation trend enhances domestic production resilience, with the U.S. currently accounting for 70% of North America’s synthetic latex polymer output.

Moreover, rising demand for water-based acrylic formulations across construction and automotive industries has increased penetration by more than 35% in the last five years. The acrylics segment—recognized for superior UV stability, flexibility, and adhesion—represents over half of the raw materials used in domestic caulk production.

China’s acrylic latex caulks market demonstrates a unique blend of manufacturing scale, customization capability, and technological acceleration. As a global production hub, Chinese firms are driving breakthroughs in fast-curing acrylic emulsions, notably from players such as Shandong Jiaobao New Material Co., Ltd.—to meet the rapid construction demands of domestic infrastructure and export markets. The innovation is vital for contractors seeking reduced project timelines and higher efficiency on large-scale builds.

The country’s green construction push has also catalyzed the transition toward low-VOC and solvent-free acrylic formulations, aligning with its “Dual Carbon” sustainability goals. With environmental regulations tightening, manufacturers are investing in eco-friendly polymer chemistry to meet both domestic standards and export compliance across Europe and North America.

Chinese manufacturers have also gained global traction through product customization—offering paintable, mildew-resistant, and flexible acrylic caulks suitable for varied climates and applications. At the same time, advancements in crystal-clear transparent formulations reflect growing demand from architectural and interior design sectors for aesthetic sealing finishes. With China contributing a dominant share of the Asia-Pacific synthetic latex polymer market, the nation’s position as a technology-forward and cost-competitive supplier of acrylic caulks remains unchallenged. The convergence of infrastructure growth, regulatory alignment, and manufacturing agility secures China’s pivotal role in the global acrylic sealant ecosystem.

Germany’s acrylic latex caulks industry stands out for its technological precision and sustainability-driven transformation. Underpinned by stringent EU environmental standards, the nation has shifted decisively from solvent-based to water-based polymer emulsions, spurring strong demand for eco-compliant acrylic latex caulks. The acrylic polymer segment dominates the German emulsions market, praised for its flexibility, UV resistance, and superior adhesion—key performance indicators for durable sealing solutions in construction and infrastructure.

Leading firms such as BASF SE are at the forefront of the green innovation wave, introducing Acronal® MB polymer emulsions that maintain high performance with a reduced carbon footprint, reinforcing Germany’s status as a global sustainability leader. Meanwhile, investments in bio-based emulsions from renewable feedstocks are opening a new era of low-carbon construction sealants designed for circular economy models.

The government’s commitment to building 400,000 housing units annually since 2022 has created a major boost for high-performance energy-efficient sealing materials, including acrylic latex caulks that improve insulation and moisture control. Additionally, specialist manufacturers such as PCI Augsburg GmbH are focusing on application-specific formulations for joints, masonry, and concrete, reflecting the market’s maturity and attention to niche performance needs. Germany’s mix of innovation, regulation, and renewable chemistry integration ensures its continued dominance in Europe’s sustainable sealant landscape.

Japan’s acrylic latex caulks market is propelled by an advanced R&D ecosystem that merges nanotechnology, electronics, and sustainable materials science. The rise of electric vehicles (EVs) and smart construction projects has accelerated the adoption of high-value acrylic sealant solutions tailored for demanding applications such as battery pack sealing, vibration damping, and thermal management. Automotive OEMs are increasingly relying on acrylic-based adhesives to achieve both lightweighting and environmental goals.

Japanese manufacturers are also leading in smart and functional materials, developing sealants with self-healing, thermally conductive, and sensor-enabled properties—a technological leap that supports future IoT-integrated construction systems. The next-generation acrylic latex caulks are critical for both structural monitoring and long-term performance in harsh environments.

Environmental consciousness remains central to Japan’s industrial strategy, with a growing emphasis on solvent-free, waterborne formulations that comply with the country’s strict emission control norms. The expanding electronics and precision manufacturing sectors also depend heavily on specialized sealing materials for miniaturized device protection, further broadening the acrylic caulk application spectrum. Backed by its intensive R&D infrastructure, cross-industry collaboration, and commitment to sustainability, Japan continues to shape the future of intelligent and eco-efficient acrylic sealant technology in Asia and beyond.

Acrylic Latex Caulks Market Report Scope

Acrylic Latex Caulks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$253.8 Million

|

|

Market Size (2034)

|

$410.9 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Standard Acrylic Latex Caulk, Siliconized Acrylic Latex Caulk, Elastomeric Acrylic Latex Caulk, Fast-Dry/Quick-Cure Acrylic Caulk, Fire-Rated Acrylic Blockade Sealant), By End-User (Residential Building & DIY, Commercial Building & Construction, Industrial, Automotive, Packaging, Others), By Resin Type (Pure Acrylic, Polymer & Co-Polymer Emulsion, Styrene-Acrylic, Vinyl Acrylic), By Packaging Type (Cartridges, Tubes/Squeeze Containers, Pails/Drums), By VOC Content (High-VOC, Low-VOC, Zero-VOC

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, DAP Global Inc., BASF SE, Sika AG, Bostik, Dow Inc., PPG Industries, Inc., RPM International Inc., ITW, DuPont de Nemours, Inc., Premier Building Solutions, Hodgson Sealants, Selena Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Standard Acrylic Latex Caulk

- Siliconized Acrylic Latex Caulk

- Elastomeric Acrylic Latex Caulk

- Fast-Dry/Quick-Cure Acrylic Caulk

- Fire-Rated Acrylic Blockade Sealant

By End-User

- Residential Building & DIY

- Commercial Building & Construction

- Industrial

- Automotive

- Packaging

- Other

By Resin Type

- Pure Acrylic

- Polymer & Co-Polymer Emulsion

- Styrene-Acrylic

- Vinyl Acrylic

By Packaging Type

- Cartridges

- Tubes/Squeeze Containers

- Pails/Drums

By VOC Content

- High-VOC

- Low-VOC

- Zero-VOC

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- DAP Global Inc.

- BASF SE

- Sika AG

- Bostik

- Dow Inc.

- PPG Industries, Inc.

- RPM International Inc.

- ITW

- DuPont de Nemours, Inc.

- Premier Building Solutions

- Hodgson Sealants

- Selena Group

*- List not Exhaustive

Research Coverage

This report investigates the global Acrylic Latex Caulks Market, offering a detailed examination of breakthrough technologies, evolving material trends, and market dynamics shaping the industry from 2025 to 2034. Through a blend of data analytics and qualitative assessments, USDAnalytics delivers in-depth analysis reviews of low-VOC sealant adoption, polymer innovation, and end-use diversification across residential, commercial, and industrial sectors. The study highlights emerging opportunities in sustainable construction, energy-efficient infrastructure, and high-performance caulk applications. By tracking company developments, product launches, and regional investments, this report is an essential resource for manufacturers, contractors, and investors seeking actionable intelligence on market trajectories, pricing trends, and regulatory impacts. With comprehensive coverage of 25+ countries, the study underscores how advancements in acrylic polymer chemistry, hybrid formulations, and emission-compliant technologies are transforming the competitive landscape of the acrylic latex caulks industry.

Scope of the study includes-

- Segmentation: By Product Type (Standard, Siliconized, Elastomeric, Fast-Dry, Fire-Rated), End-Use (Residential, Commercial, Industrial, Automotive, Packaging, Others), Resin Type (Pure Acrylic, Polymer & Co-Polymer, Styrene-Acrylic, Vinyl Acrylic), Packaging (Cartridges, Tubes, Pails), VOC Content (High, Low, Zero).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies: Analysis and profiles of 15+ key players including Henkel, Sherwin-Williams, H.B. Fuller, Sika, Dow, and BASF.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.