Market Overview: Aerosol Paints Market to Reach $8.5 Billion by 2034 as Sustainable Formulations, MRO Demand, and DIY Customization Drive Expansion

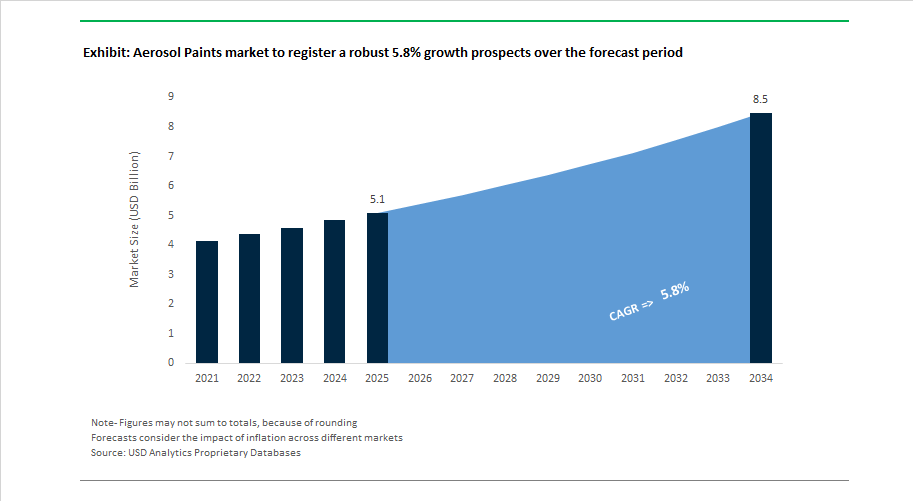

The global aerosol paints market is projected to grow from $5.1 billion in 2025 to $8.5 billion by 2034, registering a 5.8% CAGR supported by rising demand in automotive refinishing, aerospace MRO coatings, industrial maintenance, DIY home décor, and street art applications. Aerosol coatings continue to gain traction due to portability, precision application, quick-dry performance, and surface versatility across metal, plastic, wood, and composites. Growth is increasingly tied to low-VOC aerosol technology, recyclable packaging, water-borne spray systems, and high-solid formulations as regulators and consumers prioritize sustainability. Innovation in propellant systems, spray nozzles, and pigment dispersion technologies is improving coverage efficiency while reducing environmental impact, positioning aerosol paints as a flexible finishing solution across professional and consumer markets.

Manufacturing capacity and distribution channels evolved in April 2023 with Diamond Vogel integrating Sherwin-Williams’ N92 facility, strengthening private-label aerosol production. Digital retail expansion accelerated in February 2024 when Nippon Paint India partnered with Snapdeal to distribute its aerosol portfolio online, targeting India’s expanding DIY consumer base. Sustainability-focused product development gained visibility in February 2024 as Krylon introduced EcoBlend recyclable aerosol technology. Artistic and decorative segments expanded in April 2025 when Rust-Oleum launched its Rust-O street art line, while automotive refinishing engagement rose in June 2025 as Sherwin-Williams opened its 2026 automotive calendar contest. Consumer color innovation progressed in September 2025 as Dulux refreshed its aerosol range with 37 new shades and ergonomic applicators. Regulatory momentum shaped formulation strategy in August 2025 when the U.S. EPA extended VOC compliance deadlines to January 2027, allowing time for reformulation toward low-emission systems.

Industry consolidation and high-performance applications are reshaping market dynamics. In December 2025, AkzoNobel and Axalta Coating Systems announced a merger of equals, while AkzoNobel divested its Indian subsidiary to focus on high-margin industrial and aerospace segments. Trend-driven color marketing advanced in September 2025 with AkzoNobel’s Rhythm of Blues palette integrated into aerosol lines. Engineering innovation gained recognition in February 2026 at the ADF forum for aerosol component designs using bioplastic nozzles and low-pressure CO₂ propellants. Aerospace maintenance demand strengthened in February 2026 when PPG Industries introduced single-coat Aerobase aerosol coatings to reduce aircraft maintenance time and weight. These developments confirm aerosol paints as a technologically evolving, sustainability-focused segment serving both industrial precision needs and consumer creativity.

Strategic Market Trends and High-Value Growth Opportunities Reshaping the Aerosol Paints Market

The Aerosol Paints Market is undergoing a structural realignment driven by global emissions regulations, shifting material science, and the rise of automotive aftermarket repair and electrification infrastructure. Companies are now prioritizing compliance-led product reformulation, internalized aerosol filling capacity, and advanced functional coatings that deliver more than decorative value. Aerosol paints are increasingly positioned as engineered performance coatings that provide fire protection, dielectric insulation, surface restoration, and color accuracy. Below are the dominant forces reshaping market competitiveness and revenue expansion potential heading into 2030.

Market Trend: Regulatory Phase-Out of VOC Solvents and PFAS Propellants Forces Industry-Wide Reformulation

A key driver influencing innovation is the accelerated elimination of traditional VOC-rich solvents and PFAS propellants across the United States and European Union. Rather than simply reducing VOC content, regulators are adopting a reactivity-based compliance model, forcing aerosol paint manufacturers to redesign entire formulations to prevent ozone formation and meet environmental health thresholds.

On January 17, 2025, the U.S. EPA formally amended its National VOC Emission Standards for Aerosol Coatings, revising Product-Weighted Reactivity (PWR) limits and expanding the list of regulated compounds. These changes create non-negotiable compliance obligations for industrial fillers, contract suppliers, and global coating brands. In parallel, updated EU REACH and POPs regulations will prohibit intentionally added PFAS compounds in aerosol applications effective January 1, 2026, which is pushing manufacturers to shift toward compressed gases like nitrogen or CO₂, along with Hydrofluoroolefin (HFO)-based propellants.

Chemical innovation is accelerating as a result. AkzoNobel’s launch of Sikkens Autowave Optima in February 2025 demonstrates that waterborne aerosol technologies now provide viable commercial substitutes. Autowave Optima reduces coating process time by 50% and generates up to 60% lower carbon emissions, positioning water-based aerosol chemistry as a core trend in the coatings sector.

Market Trend: Vertical Integration and Global Capacity Expansion to Secure Supply and Protect Margins

Supply chain fragility during 2022–2024 triggered a strategic shift toward internal manufacturing and captive aerosol filling, reducing reliance on outsourced partners. This transition provides tighter control over lead times, raw-material qualification, and proprietary formulations.

Sherwin-Williams is leading this pivot. Its USD 300 million expansion in Statesville, North Carolina, completed in late 2024, added millions of gallons of capacity for specialty and architectural aerosols. Simultaneously, the company increased its European footprint through a capacity expansion in Tournus, France to meet EMEA demand while shortening regional freight cycles. In its 2025 Annual Report, Sherwin-Williams highlighted that internalizing aerosol production supported a 48.5% gross margin despite market volatility—demonstrating that supply chain ownership is evolving into a competitive advantage, not just a logistical strategy.

Market Opportunity: Automotive Aftermarket and AI-Enabled Precision Color-Matching Create a Premium Demand Stream

Aerosol paint is becoming a precision repair tool in the automotive aftermarket as aging vehicle fleets, complex OEM finishes, and consumer preference for "DIY professional-grade" touch-ups expand demand. The combination of AI chemistry development and digital color technology is transforming premium spray segments.

In October 2025, PPG Industries launched the Deltron Premium Glamour Speed Clear Coat, the first automotive aerosol formulation designed entirely using AI technology. The platform balances ultra-fast dry-time with long-term gloss retention, directly addressing the professional spot-repair market. PPG also reported an 8% increase in OEM automotive sales in Q3 2025, driven by its VISUALIZID digital-color-matching ecosystem, which is now being adapted into aerosol paint tools to deliver "perfect-match" finishes for pearlescent and multi-layer coatings.

The consumer upgrade path is also accelerating. Rust-Oleum introduced the Custom Spray 5-in-1 dial system, offering adjustable spray modes that imitate professional HVLP spray guns. This feature transforms aerosol cans into modular tools suitable for both garage-based DIY and dealership body shops, helping aerosol paints expand beyond their legacy retail-only market perception.

Market Opportunity: Functional Aerosol Coatings for Electrification, Battery Safety, and Renewable Infrastructure

The global shift to EVs, smart-grid systems, and distributed energy storage is driving demand for functional aerosols engineered to deliver fire resistance, dielectric insulation, corrosion protection, and thermal stability—capabilities that traditional decorative paints cannot provide.

Axalta Coating Systems’ Alesta e-PRO line, launched October 2025, introduces aerosols capable of withstanding up to 1,200°C to delay thermal propagation during EV battery cell failures. Complementing this, the e-PRO Dielectric Gray aerosol passes 6 kV hipot insulation tests, making it suitable for field-applied refurbishment of charging stations, switchgear, and battery cabinets.

As global EV sales surpass 20 million units by 2025, the maintenance and servicing ecosystem is emerging as a multi-billion-dollar aftermarket. Aerosol formats offer technicians a low-cost, no-equipment method to apply protective coatings in-field, particularly for solar inverter housings, grid transformers, and outdoor charging pedestals, positioning aerosols as a core maintenance material in the energy transition.

Aerosol coatings are evolving into a multi-functional material category driven by regulatory compliance, vertical integration, digital innovation, and electrification infrastructure. Producers with water-based compliant chemistries, internalized aerosol capacity, AI-optimized formulations, and certified functional coatings will control the top-tier growth segments of the global Aerosol Paints Market through 2030.

Aerosol Paints Market Share and Segmentation Insights

Market Share by Technology: Solvent-Based Aerosols Lead as Waterborne Formulations Accelerate

Solvent based aerosol paints account for approximately 64% of global aerosol paint demand in 2025, retaining dominance due to superior adhesion, faster drying, and stronger corrosion resistance versus water-based systems. Automotive aftermarket and industrial MRO users continue to favor solventborne coatings for their forgiving application window and compatibility with legacy substrates, despite rising VOC compliance pressure across California, the EU, and China. Water based aerosol paints are the fastest growing segment, supported by advances in acrylic emulsions and polyurethane dispersions that improve sprayability and film formation, alongside consumer preference for low-odor, eco-labeled products in DIY applications. High solids aerosol formulations hold the smallest share but are gaining traction in compliance-driven professional markets, meeting South Coast AQMD and EU solvent directives without full waterborne conversion. Hydrocarbon propellants remain standard, while compressed gases are increasing in consumer waterborne products, and DME maintains stable use as a co-solvent propellant.

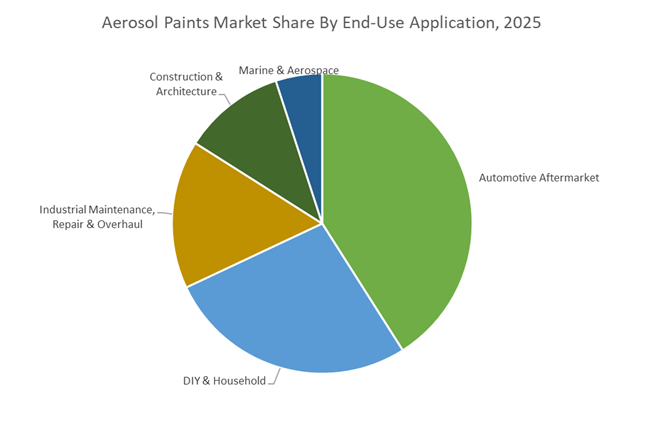

Market Share by End-Use Application: Automotive Aftermarket Drives Profitability While DIY Sustains Volume

Automotive aftermarket represents roughly 41% of aerosol paints consumption in 2025, making it the largest and most profitable segment, driven by touch-up painting, wheel refinishing, caliper coatings, and trim restoration. OEM color-code matching and premium pricing per ounce characterize this category, supported by aging vehicle fleets and rising adoption of paint pens and precision applicators. DIY & household rank second, fueled by furniture upcycling, hobby projects, and home decor trends, with chalk finishes and metallic effects emerging as high-growth niches. Industrial maintenance, repair, and overhaul delivers steady, non-cyclical demand for durable coatings, where solventborne and high-solids formulations dominate price-sensitive bulk purchases. Construction and architecture overlap with MRO, showing higher waterborne uptake due to occupied-building regulations. Marine and aerospace remain niche but high-margin, requiring saltwater resistance and OEM approvals, making this segment low volume yet structurally resilient.

Competitive Landscape: Sustainability, Customization, and Specialty Performance Reshaping the Aerosol Paints Market

The global Aerosol Paints Market is evolving rapidly as manufacturers prioritize low-VOC formulations, advanced spray ergonomics, and application-specific performance across DIY, automotive refinishing, aerospace MRO, and industrial maintenance. Competitive differentiation increasingly centers on eco-conscious propellant systems, color personalization platforms, and high-durability coatings engineered for extreme environments. Leading players are leveraging retail scale, cultural branding, and OEM integration while investing in waterborne aerosols, Bag-on-Valve technologies, and rapid customization services to capture growth across North America, Europe, and Asia-Pacific.

Sherwin-Williams scales low-VOC innovation through retail-driven aerosol platforms

Sherwin-Williams continues to lead the aerosol paints segment by combining its global retail footprint with eco-conscious product development. In early 2026, the company expanded its ColorShift aerosol technology, enabling tone-changing finishes under different lighting conditions while maintaining low-VOC compliance. Guided by its “Smarter, Healthier, Greener” strategy, Sherwin-Williams emphasizes indoor air quality certifications and non-toxic home applications. Key offerings include the EcoGloss line and the Krylon® professional and DIY ranges, widely adopted for craft and industrial spraying. Its FASTtrack system supports industrial customers with small-batch, pre-matched color delivery, minimizing downtime on automated finishing lines.

RPM International Inc. drives DIY adoption through Rust-Oleum ease-of-use technologies

RPM International, through its Rust-Oleum division, dominates DIY aerosol coatings with a strong focus on surface protection and user-friendly application. The company named “Satin Lagoon” its 2026 Color of the Year to stimulate consumer renovation trends, while expanding Custom Spray 5-in-1 nozzle technology across more SKUs for adjustable spray patterns. Rust-Oleum also delivers high-performance agricultural and industrial aerosols engineered for chemical resistance and harsh climates. Core applications span automotive refinishing and farm equipment maintenance, where its formulations bond directly to rusted or difficult substrates, reducing prep time and improving “time-on-farm” productivity.

AkzoNobel accelerates aerospace aerosol coatings with rapid MRO delivery

AkzoNobel is aggressively expanding its high-performance aerosol coatings portfolio, particularly for aerospace and industrial MRO. During 2025–2026, the company invested €50 million to upgrade its Waukegan, Illinois facility, establishing a Rapid Service Unit for faster customized aerosol and liquid coating supply. Its single-coat Aerobase system, launched in late 2025, reduces aircraft weight while improving application efficiency. AkzoNobel also proposed an all-stock merger with Axalta, targeting late 2026 or early 2027, which would create a coatings leader with approximately $17 billion in combined revenue, reinforcing its one-stop-shop aerospace strategy.

Nippon Paint Holdings advances APAC leadership with smart mobility and cultural color trends

Nippon Paint Holdings, supported by its NIPSEA Group operations, serves as the technical benchmark across Asia-Pacific. In 2026, the company unveiled its “Resonate” Color Trends with “Blue Planet” as Color of the Year, reflecting sustainability-driven consumer preferences. Recent innovations include Target Line Paint, an aerosol solution enhancing lane visibility for autonomous vehicle sensors. Nippon Paint supplies high-durability anti-corrosion systems such as Danziora and FASTAR for marine and infrastructure protection. Its asset-assembler model combines regional acquisitions with localized R&D, maintaining a strong presence across 28 markets.

PPG Industries embeds sustainability into automotive and industrial aerosol systems

PPG Industries is strengthening its aerosol paints portfolio under its “Sustainable by Design” framework, targeting a 50% carbon footprint reduction by 2030. The company is scaling waterborne aerosol technologies, with 2026 positioned as a pivotal deployment year. PPG is also expanding Bag-on-Valve adoption for technical sprays, enabling 360-degree application and near-total product evacuation. Its product range includes high-performance primers and topcoats for automotive aftermarket and industrial equipment. Deep integration with OEM and refinish channels supports precise color matching, a critical differentiator for automotive touch-up aerosols.

Montana Colors S.L. commands the creative aerosol segment with precision valve technology

Montana Colors, widely known as MTN, leads the global graffiti and professional mural segment through unmatched valve precision and high pigment loading. The company is expanding its Water Based aerosol line to comply with stringent European indoor air quality standards, supporting artists working in enclosed public spaces. Its specialty portfolio includes marbling effects, phosphorescent coatings, and high-heat-resistant sprays for urban infrastructure. Montana Colors reinforces brand loyalty through its MTN Shop network and deep engagement with street art communities, positioning itself as the cultural authority in premium creative aerosols.

United States Aerosol Paints Market: Extended Compliance Runway and Portfolio Consolidation

The United States aerosol paints market is navigating a pivotal compliance window that is enabling orderly reformulation while protecting near-term volumes. In mid-2025, the U.S. Environmental Protection Agency granted an extension for aerosol coatings compliance to January 2027. This has given manufacturers additional time to transition toward low-reactivity propellants such as HFO-1233zd(E), which carries a reactivity factor of just 0.04, materially reducing photochemical ozone formation risk. In parallel, leading producers are accelerating reformulation away from high-GWP HFC-134a toward hydrocarbons and HFO-1234ze to align with corporate Net Zero targets by late 2026.

Pricing and portfolio actions reflect ongoing cost pressure. Sherwin-Williams announced a 7% price increase effective January 1, 2026, citing sustained raw material and logistics inflation amid uneven demand. Capacity modernization continues to support high-precision spray applications, as PPG invests $380 million in a digitally enabled facility in North Carolina. Consolidation is accelerating, with RPM International reporting fiscal 2025 as its largest M&A year, including acquisitions such as The Pink Stuff and Ready Seal that expand specialized aerosol and maintenance offerings. To de-risk supply chains, U.S. players increased inventories in Q4 2025 in anticipation of potential 2026 tariffs on metal packaging and chemical precursors.

China Aerosol Paints Market: Mandatory Substance Limits and Propellant Realignment at Scale

China’s aerosol paints industry is entering a stricter regulatory phase that prioritizes hazardous substance control and propellant substitution. The State Administration for Market Regulation issued mandatory standards GB 30981.1-2025 and GB 30981.2-2025, effective June 1, 2026, which impose tighter limits on hazardous substances in coatings. These rules are accelerating reformulation across decorative and industrial aerosols and raising compliance thresholds for both domestic producers and exporters.

Propellant strategy is shifting rapidly. Manufacturers are adopting dimethyl ether and LPG blends to meet the national Green and High-Quality Development roadmap for 2025 to 2026. Food-contact applications are also expanding following the September 2025 release of GB 4806.10-2025, which broadened permitted raw materials from 105 to 346, directly impacting aerosol-applied lubricants and protective films. Industrial decarbonization is reinforcing competitiveness, as coastal chemical parks transitioned to 100% renewable electricity by late 2025, lowering the carbon footprint of exported aerosols. In marine and industrial maintenance, AkzoNobel extended its Chinese marine coatings partnership in December 2025, incorporating durable aerosol touch-up systems for shipping logistics.

India Aerosol Paints Market: Automotive Aftermarket Momentum and Water-Based Innovation

India’s aerosol paints market is expanding on the back of strong automotive aftermarket demand and policy-backed manufacturing incentives. Rising vehicle sales through 2025 have driven high consumption of industrial aerosols for engine degreasing, polishing, and rapid-dry touch-up paints. Urban infrastructure programs under the Smart Cities initiative are also increasing usage of aerosol paints for decorative stenciling and municipal maintenance, widening the demand base beyond automotive.

Policy support is catalyzing technology shifts. Under the Production Linked Incentive scheme, domestic manufacturers are investing in R&D for water-based aerosol technologies to reduce dependence on imported solvent-heavy formulations. Safety and standardization are advancing in parallel, as the Bureau of Indian Standards reviews updated protocols for pressurized containers to align with ISO aerosol standards by mid-2026. These changes are expected to improve consumer safety while raising entry barriers for non-compliant imports.

Germany Aerosol Paints Market: VOC Tightening, Bio-Based Resins, and MRO-Led Adoption

Germany continues to set the pace for environmentally progressive aerosol paint formulations in Europe. The Federal Ministry of the Environment has drafted updates to align with the latest EU VOC Paints Directive, targeting further solvent reductions for aerosol special finishes by 2026. This is pushing formulators to innovate with alternative binders and application technologies.

Bio-based materials are gaining commercial traction. During 2024 and 2025, German formulators integrated rapeseed- and pine-derived resins into aerosol lines for automotive interiors, supporting lifecycle carbon reduction without sacrificing performance. Production and application processes are also decarbonizing, highlighted by AkzoNobel inaugurating a hydrogen-powered spray booth at its automotive training center in late 2024. In maintenance and repair operations, German aerospace and automotive MRO providers are pioneering Bag-on-Valve technology, enabling 360-degree spraying and up to 99% product evacuation, which reduces waste and improves precision.

Brazil Aerosol Paints Market: Packaging Safety and High-Solids Transition

Brazil’s aerosol paints industry is undergoing a targeted transition toward safer internal coatings and higher-solids formulations. At Abralatas 2025, AkzoNobel introduced the Accelshield™ BPA non-intentional coating range, a move that is reshaping internal spray systems for beverage cans and metal packaging. This shift addresses growing scrutiny around bisphenol exposure while maintaining corrosion protection performance.

Regionally, Brazilian manufacturers are adapting to emerging Mercosur environmental standards by increasing adoption of high-solids aerosol formulations. This approach reduces solvent emissions and aligns local production with regional export requirements, positioning Brazil as a compliant supplier within South America’s evolving regulatory framework.

Country-Level Positioning in the Aerosol Paints Industry

Aerosol Paints market County Level Snapshot

|

Country

|

Primary Strategic Focus

|

Competitive Impact

|

|

United States

|

Compliance extension, HFO transition, M&A

|

Managed reformulation with portfolio expansion

|

|

China

|

Mandatory substance limits, DME and LPG propellants

|

Large-scale compliance and cost-efficient exports

|

|

India

|

Automotive aftermarket growth, water-based R&D

|

Demand-led expansion with technology localization

|

|

Germany

|

VOC tightening, bio-based resins, BoV adoption

|

Sustainability-driven premium formulations

|

|

Brazil

|

BPA non-intentional coatings, high-solids shift

|

Safer packaging and regional compliance

|

Aerosol Paints Market Report Scope

Aerosol Paints market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$8.5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Technology (Solvent Based Aerosol Paints, Water Based Aerosol Paints, High Solids Aerosol Formulations), By Propellant Type (Liquefied Petroleum Gas, Dimethyl Ether, Hydrofluoroolefins, Compressed Gases), By Packaging Material (Aluminum Cans, Tin Plated Steel Cans, Plastic and Composite Aerosol Containers), By End Use Application (Automotive Aftermarket, Construction and Architecture, Industrial Maintenance Repair and Overhaul, DIY and Household, Marine and Aerospace)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin Williams Company, AkzoNobel, RPM International, PPG Industries, Nippon Paint Holdings, Masco Corporation, Montana Colors, The Valspar Corporation, BASF, Kansai Paint, DuPont de Nemours, Aerosol Solutions, Plasti Dip International, Peter Kwasny, Sanan Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerosol Paints Market Segmentation

By Technology

- Solvent Based Aerosol Paints

- Water Based Aerosol Paints

- High Solids Aerosol Formulations

By Propellant Type

- Liquefied Petroleum Gas

- Dimethyl Ether

- Hydrofluoroolefins

- Compressed Gases

By Packaging Material

- Aluminum Cans

- Tin Plated Steel Cans

- Plastic and Composite Aerosol Containers

By End Use Application

- Automotive Aftermarket

- Construction and Architecture

- Industrial Maintenance Repair and Overhaul

- DIY and Household

- Marine and Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aerosol Paints Industry

- The Sherwin Williams Company

- AkzoNobel

- RPM International

- PPG Industries

- Nippon Paint Holdings

- Masco Corporation

- Montana Colors

- The Valspar Corporation

- BASF

- Kansai Paint

- DuPont de Nemours

- Aerosol Solutions

- Plasti Dip International

- Peter Kwasny

- Sanan Group

*- List not Exhaustive