Market Overview: Production Rate Recovery, Lightweight Economics, and Automation Are Reframing the Aerostructure Materials Market

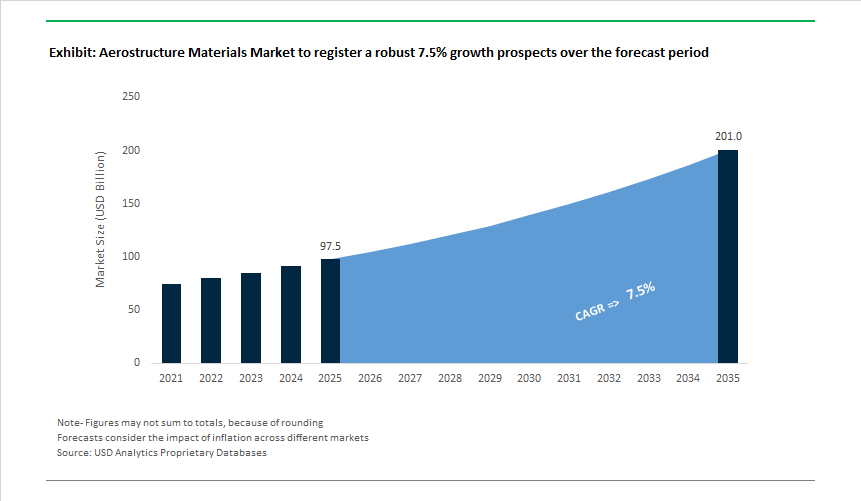

The Global Aerostructure Materials Market is valued at USD 97.5 billion in 2025 and is projected to reach USD 201.0 billion by 2035, expanding at a 7.5% CAGR as the aerospace sector transitions from post-cycle recovery into a sustained production upcycle. Market growth is being driven less by fleet expansion alone and more by structural changes in aircraft design, manufacturing economics, and lifecycle performance requirements.

At the core of this shift is the economics of lightweighting. Aircraft OEMs are increasingly designing platforms around materials that deliver permanent operating cost advantages through fuel burn reduction, extended range, and higher payload efficiency. Carbon-fiber-reinforced polymers (CFRPs) have moved beyond selective use and are now structural default materials for wings, fuselage sections, empennages, and interior structures in next-generation commercial and military aircraft. For airlines, even marginal weight reductions translate into measurable lifetime fuel savings, making composite penetration a commercial imperative rather than a design preference.

In parallel, titanium and advanced titanium-based alloys are reinforcing their strategic role across aerostructures. As composite usage increases, so does demand for titanium in load-bearing interfaces, landing gear components, engine pylons, and high-temperature zones where corrosion resistance and strength retention are non-negotiable. This creates a complementary materials dynamic rather than substitution, with titanium positioned as the metal of choice in composite-intensive airframes. Supply assurance, forging capacity, and cost stability are therefore becoming strategic considerations for both OEMs and Tier-1 suppliers.

Manufacturing transformation represents the third major growth lever. Aircraft production rates are rising, but traditional labor-intensive composite layup methods are no longer compatible with required throughput and cost targets. As a result, automated fiber placement (AFP), automated tape laying (ATL), resin transfer molding (RTM), and out-of-autoclave processing are becoming central to material adoption decisions. Materials that cannot scale efficiently within automated manufacturing environments are increasingly being designed out of future platforms. This places material suppliers under pressure to deliver not only performance, but manufacturability at rate.

The market is also seeing early shifts toward thermoplastic composites, hybrid metal-composite architectures, and recyclability initiatives. Thermoplastics, in particular, are gaining attention for their faster cycle times, weldability, and repair advantages-attributes aligned with high-volume narrowbody aircraft programs and defense platforms requiring rapid turnaround. While qualification timelines remain long, OEM roadmaps increasingly factor these materials into mid- to long-term platform strategies.

From a strategic perspective, the aerostructure materials market is transitioning from materials competition to ecosystem competition. Value is accruing to suppliers that can align material properties with production-rate economics, support multi-year qualification and certification processes, and integrate closely with OEMs and Tier-1s on design-for-manufacture and lifecycle cost reduction.

Market Analysis: High-Performance Composites, Thermoplastics Expansion, and Supply Chain Strengthening

Recent industry developments highlight significant advancements in carbon composites, thermoplastics, space-grade materials, and sustainability-driven innovations. In November 2025, Hexcel Corporation strengthened its strategic direction by appointing an Interim CFO, signaling leadership prioritization of financial resilience during aerospace supply chain volatility. In September 2025, Hexcel and HyPerComp unveiled a next-generation Composite Pressure Vessel at CAMX 2025, showcasing high-performance carbon overwrap solutions for defense and space applications where lightweight containment and pressure reliability are paramount. During the same month, Toray Advanced Composites launched Toray Cetex® TC1130 PESU, a thermoplastic engineered for lightweight, recyclable interior structures, contributing to aviation’s transition toward sustainable thermoplastic aerostructures.

Earlier in June 2025, Hexcel presented its HexPly® M51 prepreg technology at the Paris Air Show, a major advancement in ramp-up enablement for single-aisle aircraft, improving tack, drape, and cure cycle efficiency-critical for OEMs increasing build rates. In March 2025, analysts reported rapid experimentation with graphene-infused composites, which improve stiffness, damage tolerance, and conductivity while still delivering material-level weight reduction. In December 2024, Toray expanded its aerospace revenue streams by signing a long-term supply agreement with Airborne Aerospace B.V., offering space-grade composite materials for mega-constellation satellite solar arrays. This aligns with Toray’s strategy to diversify beyond commercial airframes into satellite and space infrastructure.

Additional technological milestones emerged in October 2024, when Toray announced capacity expansion across its thermoplastic composite portfolio, specifically targeting applications requiring rapid manufacturability and automation compatibility. In July 2024, Solvay and Spirit AeroSystems formalized a collaboration at the Aerospace Innovation Centre in Scotland, focusing on accelerating next-generation composite aerostructures for future commercial aircraft.

Aerostructure Materials Market Trends and Opportunities

Trend 1: Industrial-Scale Shift to Carbon Fiber Thermoplastic Composites

The aerostructure materials landscape is undergoing a decisive shift toward carbon fiber–reinforced thermoplastic composites as aircraft manufacturers push to reconcile higher production rates with structural performance and sustainability targets. Unlike traditional epoxy-based thermosets, high-performance thermoplastics such as LMPAEK and PPS enable true out-of-autoclave processing, fundamentally changing factory economics. Throughout 2024–2025, leading material suppliers expanded continuous-fiber thermoplastic offerings compatible with press forming and automated fiber placement, allowing complex structural parts to be consolidated and produced in minutes rather than hours. This reduction—often approaching 80% in cycle time—directly supports “Rate 60+” narrowbody production ambitions and reduces work-in-progress inventory on factory floors. From a performance standpoint, thermoplastic composites deliver substantial lightweighting benefits, with typical mass reductions of 20–50% versus metallic alternatives. Industry fuel-burn benchmarks show that every 100 kg removed from an airframe can save roughly 19,000 liters of fuel annually, making thermoplastics a strategic enabler for next-generation single-aisle aircraft, long-range variants, and emerging eVTOL platforms. Equally important is the acceleration of material qualification. By late 2025, public database inclusion through NCAMP had reduced certification risk for tier-1 suppliers, enabling thermoplastics to move from secondary brackets into load-bearing fuselage clips, ribs, and shear webs with significantly shorter adoption timelines.

Trend 2: Corporate Investment in Recycled Carbon Fiber Supply Chains

Sustainability strategies in aerostructures are evolving beyond reporting metrics into tangible supply chain redesign, with recycled carbon fiber (rCF) emerging as a commercially viable material stream. During 2024 and 2025, major OEMs formalized closed-loop recycling partnerships to reclaim high-value production scrap from composite-intensive programs, particularly widebody wings and fuselage sections. These initiatives demonstrate that aerospace-grade carbon fiber waste—once considered unusable—can be reprocessed and redeployed into structurally demanding, though non-primary, components. Industrial maturity has accelerated rapidly, with thermal recycling via pyrolysis becoming the dominant method due to its ability to preserve fiber tensile properties and modulus. By late 2025, rCF had progressed from interior panels to more complex secondary aerostructures, including fairings, access panels, and system supports. From an environmental perspective, corporate disclosures indicate that recycled carbon fiber carries a markedly lower carbon footprint than virgin fiber, enabling double-digit reductions in scope 3 emissions while also lowering material costs. Strategically, this dual benefit is driving OEMs to view rCF not as a compromise material but as a hedge against virgin fiber supply constraints and price volatility, particularly as composite content continues to rise in future airframes.

Opportunity 1: Advanced Thermoplastic Welding for Fastener-Free Assembly

The growing penetration of thermoplastic composites unlocks a transformative opportunity in fastener-free aircraft assembly through advanced welding technologies. Unlike thermosets, thermoplastics can be reheated and fused, enabling resistance, induction, and ultrasonic welding to replace thousands of mechanical fasteners traditionally required in metallic and epoxy-composite structures. This shift has profound implications for both weight and durability: eliminating fasteners reduces mass while also removing drilled holes that act as stress concentrators and fatigue initiation points. By 2025, aerospace integrators were deploying induction welding in production environments to create large, fully integrated subassemblies with fewer parts and simplified logistics. Validation from space and exploration programs has further accelerated confidence in these methods, with large-scale testing showing that optimized ultrasonic welds can retain up to 80% of base material strength. Parallel advances in automation are amplifying the opportunity. AI-enabled welding systems now monitor temperature, pressure, and fusion quality in real time, dynamically adjusting parameters to ensure consistency. This reduces reliance on post-process non-destructive inspection and can cut inspection-related energy and labor costs by up to 40%, positioning thermoplastic welding as a cornerstone technology for high-rate, digitally enabled aerostructure production.

Opportunity 2: High-Temperature Materials for Hybrid and Hydrogen Propulsion

Next-generation propulsion concepts are creating a strong demand signal for aerostructure materials capable of operating across unprecedented thermal extremes. Hybrid-electric architectures introduce sustained thermal loads from high-voltage power electronics—often exceeding 800 VDC—that challenge the limits of conventional aluminum alloys and epoxy composites. As a result, advanced resin systems, high-temperature dielectrics, and novel thermal interface materials are becoming essential elements of future nacelles and powertrain enclosures. At the upper end of the temperature spectrum, aerospace and defense programs are accelerating investment in ultra-high temperature ceramics such as zirconium diboride and hafnium diboride, which can withstand environments above 1,650°C where nickel superalloys lose structural integrity. These materials are increasingly specified for hypersonic leading edges and engine-adjacent structures exposed to extreme aerodynamic heating. At the opposite extreme, the push toward hydrogen propulsion introduces cryogenic challenges. Liquid hydrogen storage at −253°C requires aerostructure materials that maintain toughness without embrittlement, driving innovation in cryogenic-grade composites, aluminum-lithium alloys, and advanced joining techniques such as friction stir welding. Together, these propulsion-driven requirements are expanding the aerostructure materials market into a dual frontier—high-temperature and cryogenic—where material performance directly determines the feasibility of next-generation flight architectures.

Market Share Analysis: Aerostructure Materials Market

Market Share by Material Segment: Composite Materials as the Structural Core of Modern Aircraft

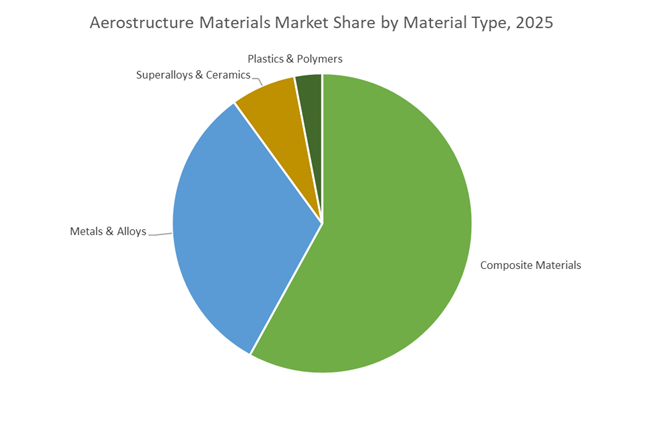

Composite materials, holding approximately 58% of the aerostructure materials market in 2025, have become the non-negotiable foundation of modern aircraft design as OEMs prioritize weight reduction, fuel efficiency, and lifecycle economics over traditional metal-intensive architectures. The transition from secondary to primary structural applications is now complete: flagship platforms from Boeing and Airbus—notably the 787 Dreamliner and A350 XWB—are composed of 50–53% composites by weight, establishing a de facto industry benchmark for next-generation programs. Financially, this dominance is reinforced by the scale of the aerospace composites sub-market, valued at $30.3 billion in 2025 and anchored by material suppliers such as Toray Industries and Hexcel. The economic logic is compelling: data from Syensqo shows that every 1% reduction in airframe weight delivers nearly a 3% improvement in fuel efficiency, while Teijin estimates that a 100 kg weight reduction through CFRP saves ~19,000 liters of fuel per aircraft annually. Under tightening Net-Zero 2050 mandates and sustained airline margin pressure, composites now represent the highest-ROI material choice, structurally locking in their majority market share.

Market Share by Manufacturing Process: AFP/ATL as the Industrial Backbone of Composite Aerostructures

Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) account for around 42% of aerostructure manufacturing processes, reflecting their role as the only scalable methods capable of translating composite material advantages into high-rate aircraft production. As OEM backlogs for platforms such as the A320neo and 737 MAX stretch into the next decade, manufacturers including Spirit AeroSystems have demonstrated that AFP-driven production lines deliver ~35% efficiency gains over manual layup, fundamentally reshaping cost curves and throughput. Adoption is already entrenched: roughly 70% of high-performance wide-body airframes now incorporate AFP in fuselage and wing structures, supported by an installed base of ~320 AFP systems globally, with 42% concentrated in North America—a critical signal for regional supply chain resilience. Beyond speed, AFP’s ability to enable fiber steering—placing fibers precisely along load paths—has become a decisive differentiator. Technical validations from Fujikura and Sumitomo Electric show 20–25% strength improvements without added mass, a performance leap unattainable through traditional forming or machining. As composite content continues to rise per aircraft, AFP/ATL has shifted from an enabling technology to the manufacturing backbone sustaining the aerostructure materials market’s next growth phase.

Competitive Landscape: Global Leaders in Carbon Composites, Thermoplastics, and Integrated Aerostructures

The Aerostructure Materials Industry comprises major composite suppliers, resin system innovators, and Tier-1 aerostructure integrators. Competition centers on material performance, automation compatibility, production scalability, thermoplastic adoption, and sustainability initiatives. Companies are intensifying long-term supply agreements, satellite diversification, and partnerships to support next-generation aircraft manufacturing.

Toray Industries, Inc. - Leader in Carbon Fiber Composites For Primary Aerostructures

Toray supplies the industry-defining Torayca® Carbon Fiber, widely used across Boeing and Airbus programs, notably forming the primary composite structure of the Boeing 787. Its portfolio spans both thermoset and thermoplastic prepregs with strong focus on OOA (Out-of-Autoclave) systems that reduce cure cycle costs and enable broader part geometries. The company’s late-2024 long-term agreement with Airborne Aerospace strengthens its position in space-grade composites, expanding into satellite infrastructure. Toray’s materials deliver up to 40% weight reduction compared to aluminum while maintaining exceptional tensile strength. With AS9100 and ISO 14001 certifications, Toray supports high-volume, precision aerospace production.

Hexcel Corporation - Innovator in Honeycomb Cores, Prepregs, and High-Rate Aerospace Composites

Hexcel’s product suite includes HexPly® prepregs, HexTow® carbon fiber, and HexWeb® honeycomb, used extensively in engine fan blades, nacelles, fuselages, and control surfaces. Its strategic investment in HexPly® M51 positions the company to support higher OEM production rates for next-generation single-aisle jets. The release of Flex-Core® HRH-302 adds a mid-temperature honeycomb solution for advanced thermal environments, especially within propulsion structures. With over 1,350 global patents, Hexcel remains a technology driver in adhesives and composite materials, maintaining its role as a foundational supplier to global aerospace OEMs.

Solvay - Advanced Resin System Pioneer Driving Cost-Effective Composite Adoption

Solvay provides high-performance resin systems (PEEK, PEKK) and advanced prepregs that serve both primary and secondary aircraft structures. Its strategic collaboration with SGL Carbon accelerates development of intermediate modulus carbon fibers that combine affordability with high mechanical performance. The 2024 joint R&D program with Spirit AeroSystems underscores Solvay’s commitment to enabling lower-cost, higher-rate composite manufacturing. Solvay's history of scaling carbon fiber production, including prior capacity doubling at its U.S. Piedmont facility, supports its role in next-generation aerostructures.

Spirit Aerosystems - Global Tier-1 Leader in Large-Scale Composite and Metallic Aerostructures

Spirit manufactures critical fuselage, wing, and nacelle assemblies for Boeing and Airbus, using advanced composite and metallic systems. Its leadership in automated aerostructure manufacturing supports OEMs seeking higher throughput and reduced takt time. The company’s Aerospace Innovation Centre in Scotland serves as a hub for collaborative research in future sustainable aircraft technologies, including composite optimization and recyclable structures. Spirit’s supply dominance includes major contributions to the Boeing 737 MAX fuselage and structural components of the Airbus A350, reinforcing its strategic importance in global aircraft production.

Triumph Group - Specialist in Aircraft Systems, Components, and Aftermarket Services

Triumph provides mechanical, electromechanical, and interior systems including actuation, geared components, and thermo-acoustic insulation solutions. Structured across five operating companies, Triumph supports diversified aerospace needs through build-to-print and complex assembly capabilities. The company’s recent strategic emphasis on MRO services strengthens aftermarket lifecycle revenues while ensuring reliability across commercial, military, and rotorcraft fleets. Triumph’s engineering expertise positions it as a leading Tier-2 supplier for specialized aircraft mechanisms and structural subassemblies.

The United States aerostructure materials market in 2025 is being structurally reshaped by re-shoring policies, record OEM backlogs, and automation-driven composite manufacturing. The expansion announced by Hexcel Corporation in September 2025 strengthens domestic availability of HexTow® IM9 24K carbon fiber, a grade increasingly specified for primary load-bearing aerostructures due to its optimized strength-to-cost profile. This move directly supports higher build rates for next-generation single-aisle and wide-body aircraft while reducing exposure to offshore composite supply disruptions.

Supply-chain stabilization has accelerated following Boeing’s USD 4.7 billion acquisition of Spirit AeroSystems, which entered a deep operational integration phase in 2025. The objective is to regain production predictability for composite fuselages and metallic wing structures, particularly for the 787 program. Parallel to this, FAA-aligned certification work led by National Institute for Aviation Research (NIAR) is advancing overbraided composite structures, enabling automated production routes that could reduce aerostructure labor costs by nearly 30%.

France – CORAC-Led Decarbonization and Thermoplastic Composite Ecosystems

France remains the European anchor for aerostructure material innovation, with national strategy in 2025 tightly aligned around decarbonization, recyclability, and thermoplastic composites. The renewal of the €285 million CORAC budget reaffirmed the government’s commitment to funding over 320 aerospace R&D projects, many of which focus on ultra-lightweight airframe materials and low-energy manufacturing routes.

The launch of GIFAS’ Team France Aerospace initiative has synchronized SMEs and primes such as Airbus and Safran around thermoplastic demonstrators like the HELUES project. These materials offer faster cycle times and inherent recyclability advantages over thermosets, making them central to Airbus’ next-generation single-aisle roadmap. Safran’s continued involvement in composite fan blade joint ventures further reinforces France’s role in engine-adjacent aerostructure materials, where weight reduction directly translates into fuel efficiency gains.

China – Composite Indigenization Backed by Strategic Mineral Control

China’s aerostructure materials market in 2025 is characterized by rapid indigenization combined with strategic leverage over raw materials. The January 2025 launch of China’s first domestically produced composite fan blade by Shanghai Aero Engine Composites, under the Aviation Industry Corporation of China (AVIC) umbrella, marked a critical step toward self-sufficiency in aero-engine-grade composites.

Simultaneously, China’s export controls on tungsten and antimony have reshaped global aerostructure supply dynamics. With control over roughly 80% of global tungsten production and up to 90% of rare earth processing, China retains decisive influence over high-strength steels, superalloys, and actuator systems used in landing gear and pylons. This dual-track approach—material innovation at home and mineral leverage abroad—is forcing Western aerostructure manufacturers to accelerate alternative alloy systems and rare-earth-light designs.

India – Make-in-India Scaling and Global Supply Chain Integration

India has emerged in 2025 as a high-growth aerostructure manufacturing hub, driven by defense indigenization mandates and expanding civil aviation demand. The Airbus–Tata Advanced Systems C295 program reached a structural milestone with the localized production of more than 14,000 aerostructure components, significantly reducing import dependence.

Defense exports reaching ₹23,622 crore (USD 2.8 billion) in FY 2024–25 underscore India’s growing credibility as a global aerostructure supplier. At Aero India 2025, Hexcel Corporation highlighted its rapid-curing HexPly® M51 prepreg, tailored for high-rate composite part production, aligning with India’s expanding narrow-body fleet and MRO ecosystem. India’s strategy increasingly combines cost-efficient manufacturing with certification-driven quality, positioning it as a long-term partner in global aerostructure supply chains.

Germany – Record Turnover and Buy-European Aerostructure Policy

Germany’s aerostructure materials market is benefiting from record aerospace turnover and rising defense expenditure. Data from BDLI shows €52 billion in sector revenue for 2024, with employment and R&D spending reaching historic highs. This economic momentum is translating into sustained demand for advanced composites, aluminum-lithium alloys, and next-generation metallic structures.

The German government’s application of the “Buy European” principle under the Sondervermögen defense fund is prioritizing EU-based suppliers for programs such as FCAS. Concurrently, German research centers announced recyclable epoxy resin systems in late 2025 that enable carbon fiber recovery from retired aerostructures—addressing one of the EU aerospace sector’s most critical sustainability bottlenecks.

Japan – High-Modulus Carbon Fiber and Closed-Loop Recycling Leadership

Japan continues to define the upper end of the aerostructure materials market, combining high-modulus carbon fiber leadership with circular economy innovation. In December 2025, Mitsubishi Chemical Group unveiled a solvent-dissolvable epoxy resin that allows near-complete recovery of aerospace-grade carbon fibers—an enabling technology for Japan’s net-zero aviation strategy.

Meanwhile, Toray Industries expanded aerospace prepreg capacity across Japan and the U.S. to support higher build rates of next-generation wide-body aircraft. Complementing this, DIC Corporation launched a heat-resistant epoxy in late 2025 designed to replace metallic components in high-temperature aerostructure zones, reinforcing Japan’s role as the global benchmark for lightweight, high-performance materials.

2025 Strategic Comparison: Aerostructure Materials National Matrix

Aerostructure Materials National Matrix

|

Country

|

Primary Material Driver

|

2025 Key Milestone

|

Application Focus

|

|

United States

|

Automated CFRP scaling

|

Hexcel Americas distribution expansion

|

Primary structures, 787 stabilization

|

|

France

|

Decarbonization R&T

|

€285M CORAC budget renewal

|

Thermoplastic composites

|

|

China

|

Indigenization & minerals

|

First domestic composite fan blade

|

Engines, controlled exports

|

|

India

|

Make-in-India aerospace

|

USD 2.8B defense export record

|

C295 structures, civil aviation

|

|

Germany

|

Defense modernization

|

€52B aerospace turnover

|

FCAS, recyclable resins

|

|

Japan

|

Circular high-modulus CFRP

|

Dissolvable epoxy for fiber recovery

|

Recyclable airframes

|

Aerostructure Materials Market Report Scope

Aerostructure Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$97.5 Billion

|

|

Market Size (2035)

|

$201 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Composite Materials, Metals & Alloys, Superalloys & Ceramics, Plastics & Polymers), By Component (Fuselage, Wings, Empennage, Nacelles & Pylons, Flight Control Surfaces, Nose), By Aircraft Type (Commercial Aviation, Military Aircraft, Business & General Aviation, Space & Hypersonics), By Manufacturing Process (AFP/ATL, Additive Manufacturing, RTM/VARTM, Traditional Machining & Forging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries Inc., Hexcel Corporation, Solvay S.A., Mitsubishi Chemical Group, Teijin Limited, Spirit AeroSystems, SGL Carbon SE, ATI (Allegheny Technologies), Howmet Aerospace Inc., Constellium SE, GKN Aerospace, Alcoa Corporation, Huntsman International LLC, AVIC, Aleris International (Novelis)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerostructure Materials Market Segmentation

By Material Type

- Composite Materials

- Metals & Alloys

- Superalloys & Ceramics

- Plastics & Polymers

By Component

- Fuselage

- Wings

- Empennage

- Nacelles & Pylons

- Flight Control Surfaces

- Nose

By Aircraft Type

- Commercial Aviation

- Military Aircraft

- Business & General Aviation

- Space & Hypersonics

By Manufacturing Process

- Automated Fiber Placement (AFP) / Automated Tape Laying (ATL)

- Additive Manufacturing

- Resin Transfer Molding (RTM) / VARTM

- Traditional Machining & Forging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aerostructure Materials Market

- Toray Industries, Inc.

- Hexcel Corporation

- Solvay S.A.

- Mitsubishi Chemical Group

- Teijin Limited

- Spirit AeroSystems

- SGL Carbon SE

- ATI (Allegheny Technologies)

- Howmet Aerospace Inc.

- Constellium SE

- GKN Aerospace

- Alcoa Corporation

- Huntsman International LLC

- Avic

- Aleris International (Novelis)

*- List not Exhaustive