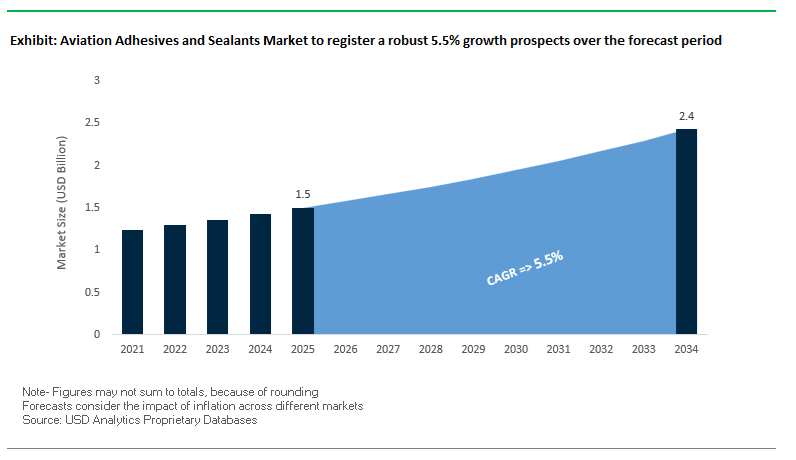

Aviation adhesives and sealants have become strategically central as aircraft programs increasingly prioritize composite-intensive structures, weight reduction, and environmentally compliant manufacturing. The market, valued at USD 1.5 billion in 2025 and projected to reach USD 2.4 billion by 2034 at a CAGR of 5.5%, is no longer driven solely by incremental fleet growth but by a fundamental shift in how airframes are designed, assembled, and maintained. OEMs and MRO organizations rely on advanced bonding and sealing chemistries to meet fatigue life targets, fuel-system integrity requirements, and long-term serviceability expectations across both commercial and defense platforms.

The core structural shift reshaping demand is the replacement of mechanically fastened metallic assemblies with bonded composite architectures and integrated sealing systems. Structural epoxy adhesives qualified for −65°C to +180°C service environments and delivering shear strengths above 5,000 psi have become the backbone of composite bonding, enabling reliable joining of CFRP skins, spars, and honeycomb panels while improving fatigue resistance under cyclic loads. In parallel, fluorosilicone and polysulfide sealants capable of maintaining adhesion and flexibility after prolonged immersion in jet reference fuel at 60°C are standard for engine nacelles and integral fuel tanks, where chemical resistance and thermal stability directly influence safety and maintenance intervals.

Material substitution is also being driven by regulatory and production realities. Polythioether-based sealants achieving up to 80% VOC reduction versus legacy solvent-borne systems are increasingly specified to align with REACH, EPA, and FAA environmental mandates without compromising sealing performance. At the same time, pre-catalyzed structural film adhesives offering open assembly times of up to 15 days are reshaping composite manufacturing workflows, reducing reliance on time-critical layups and autoclave bottlenecks for large structures.

The global aviation adhesives and sealants industry is undergoing an accelerated transformation, combining material innovation with sustainability and digital manufacturing advancements. Key players are expanding R&D footprints, integrating chromate-free chemistries, and scaling renewable-based formulations to meet both OEM efficiency goals and environmental compliance mandates.

In October 2025, Henkel and Dow deepened their strategic partnership to decarbonize adhesive manufacturing, introducing low-carbon feedstocks and renewable power into Henkel’s production processes. This initiative sets a precedent for reducing carbon intensity in aerospace-grade adhesives. The same month, a major North American aircraft OEM finalized a multi-year contract for non-chromated polythioether sealants, underscoring the rapid adoption of REACH-compliant, fuel-resistant sealant technologies across new-generation airliner programs.

August 2025 marked Hexcel Corporation’s expansion into the Urban Air Mobility (UAM) sector with a new high-temperature epoxy film adhesive range designed for composite and thermoplastic bonding — a critical requirement for electric vertical take-off and landing (eVTOL) vehicles. Similarly, 3M (June 2025) achieved qualification for a fast-curing, fire-retardant silicone sealant aimed at minimizing aircraft downtime in cabin interior MRO operations, improving turnaround efficiency for airlines.

The European aerospace supply chain continues to expand, with Solvay (April 2025) announcing capacity growth in its composite bonding adhesive line, driven by increased procurement from Airbus and defense contractors. In February 2025, PPG Aerospace launched a lightweight polyurethane fuel tank sealant, directly supporting aircraft fuel efficiency and emissions reduction goals. Huntsman (December 2024) further strengthened its high-performance epoxy portfolio by acquiring a European composites firm, integrating toughened epoxy technologies into its aviation materials suite.

Meanwhile, Henkel’s €35 million investment in a new Spanish aerospace adhesives facility (October 2024) positions it strategically within Europe’s manufacturing corridor, ensuring supply resilience and advanced process integration for next-generation lightweight and fuel-efficient aircraft programs.

The aviation industry’s pivot toward next-generation jet propulsion and hydrogen-fueled systems has elevated the thermal and chemical performance requirements of structural bonding materials. Traditional epoxies, once sufficient for sub-150°C service environments, are being replaced by polyimide, benzoxazine, and bismaleimide (BMI)-based adhesives engineered to maintain structural integrity under severe high-temperature and oxidative conditions.

New-generation jet engines and hydrogen propulsion systems operate at temperatures exceeding 250°C–300°C for prolonged durations, far surpassing the performance limits of conventional aerospace epoxies. In composite-rich engine sections, polyimide adhesives are demonstrating long-term mechanical retention—maintaining over 70% of their original shear strength after 2,000 hours of thermal aging at elevated temperatures. The leap in performance is enabling broader use of lightweight composite fan casings and nacelles in high-thrust, high-bypass engine designs.

Benzoxazine and BMI resin systems are at the forefront of high-performance adhesive chemistries. A recent aerospace-grade epoxy variant maintained 77% of room-temperature shear strength at 315°C (600°F) and 22% at 400°C (750°F), positioning it as a viable bonding solution for high-heat structures and turbine-related applications. These innovations directly align with the growing need for thermally stable, oxidation-resistant adhesives in next-generation aircraft engines and hypersonic vehicles.

With hydrogen-powered and hypersonic aircraft programs advancing, sealants must withstand cryogenic temperatures down to −253°C (for hydrogen storage) and thermal extremes up to 1,370°C (2,500°F) in propulsion zones. Advanced ceramic-based and hybrid polymer sealants are being tested to manage these dual-environment requirements, combining chemical inertness, gas impermeability, and structural flexibility. The emergence of these high-temperature materials is redefining aerospace sealing performance for zero-emission propulsion and defense systems.

The increasing dominance of carbon-fiber composite airframes in both commercial and defense aviation is driving the adoption of toughened structural adhesives designed to withstand impact, fatigue, and delamination stresses across bonded joints. These formulations are engineered to deliver enhanced fracture toughness and energy dissipation, ensuring structural integrity under cyclic mechanical loads.

Research confirms that the integration of 5–10 wt% thermoplastic modifiers (such as phenoxy resins or block copolymers) into neat epoxy matrices can significantly improve mode-I fracture energy (G_IC)—a critical indicator of crack resistance in composite joints. The performance improvement allows composite-heavy structures like the Boeing 787 and Airbus A350 to achieve higher fatigue lifespans while maintaining minimal structural weight penalties.

Nano-engineered adhesives incorporating carbon nanotubes (CNTs) and carbon nanofibers (CNFs) have shown marked improvements in mechanical interfacial strength and crack propagation resistance. Even a 0.1 wt% CNT inclusion in aerospace-grade epoxy systems can raise adhesive toughness without sacrificing shear strength—offering a lightweight reinforcement strategy with significant gains in damage tolerance and load transfer efficiency across bonded composite joints.

To support the modular assembly of composite fuselage and wing sections, film adhesives weighing as little as 75 g/m² are commercially available. These ultra-lightweight adhesives allow precise control over bondline thickness, curing uniformity, and joint performance—essential for meeting aerospace strength-to-weight ratio targets and achieving manufacturing consistency across large-scale composite assemblies.

The accelerating development of Unmanned Aerial Vehicles (UAVs) and Electric Vertical Take-Off and Landing (eVTOL) platforms is generating a dynamic new demand segment for fast-curing, lightweight adhesives tailored for modular, high-throughput production. These emerging aerospace categories require bonding materials that balance speed, reliability, and multifunctionality, especially for thermal management, vibration control, and electrical insulation.

The Urban Air Mobility (UAM) sector is rapidly shifting from low-rate prototype production to automated, high-volume manufacturing. The trend is driving adoption of Out-of-Autoclave (OOA) adhesives designed for consistent curing under lower pressure conditions. Fast-cure epoxies and acrylic structural adhesives are enabling cycle time reductions of up to 60%, supporting cost-effective assembly of eVTOL fuselages and UAV airframes.

With eVTOL platforms relying heavily on high-power lithium battery systems, thermally conductive adhesives and gap fillers have become essential for efficient heat dissipation and electrical safety. These materials offer dual-functionality—mechanical fixation and heat transfer—facilitating optimal battery performance under continuous high-load operation. Manufacturers are introducing silicone-free thermally conductive systems to ensure compatibility with sensitive electronic modules in electric propulsion environments.

The sustained aging of commercial and defense aircraft fleets is reinforcing the long-term strength of the Maintenance, Repair, and Overhaul (MRO) segment. With the average age of the global commercial fleet exceeding 13 years, demand for certified repair adhesives and sealants—particularly for composite structures and bonded joints—continues to grow exponentially.

Bonded repair methods offer key benefits over traditional riveted or bolted repairs, including weight savings of up to 25%, enhanced fatigue resistance, and single-side accessibility—critical for pressurized fuselage structures. Aerospace-approved epoxy adhesives used in bonded patches provide superior load distribution and crack arresting capability, prolonging the structural life of aging aircraft.

Both FAA and EASA have tightened certification protocols for bonded repairs, emphasizing primer thickness control (0.15–0.3 mil) and surface preparation standards to ensure bond reliability. The regulatory oversight is driving adoption of next-generation primer-integrated adhesives that streamline MRO workflows while ensuring compliance with stringent airworthiness directives.

Emerging robotic MRO systems capable of performing automated scarfing and adhesive patch placement are redefining composite repair efficiency. Studies indicate that automated bonded repair systems can reduce repair time by 60% compared to manual methods, a transformative improvement for large composite-intensive aircraft such as the Boeing 787 and military UAV platforms.

Aviation Adhesives and Sealants Market Share Insights, 2025-2034

The adhesives segment dominates the global aviation adhesives and sealants industry, holding approximately 60.4% of the market share in 2025, primarily driven by the growing reliance on bonded composite structures and lightweight materials in modern aircraft manufacturing. Structural adhesives—particularly epoxy, polyurethane, and acrylic-based systems—are at the heart of this dominance, providing the high strength, fatigue resistance, and temperature tolerance required for primary and secondary airframe bonding. As aircraft OEMs increasingly replace mechanical fasteners with bonded joints to reduce weight, improve aerodynamics, and minimize corrosion risk, the role of adhesives has expanded dramatically. Beyond the exterior structures, adhesives are integral in interior assembly applications, including panels, flooring, monuments, and overhead bins, where flammability, smoke, and toxicity (FST) compliance is mandatory. Furthermore, the surge in composite-intensive aircraft platforms such as the Boeing 787, Airbus A350, and new-generation eVTOLs has elevated adhesives from supporting materials to structural enablers of aerospace design evolution. The ongoing focus on fuel efficiency, sustainability, and advanced manufacturing automation—including preformed film adhesives and automated dispensing systems—further reinforces this segment’s leadership. As aerospace manufacturers pursue greater design flexibility and reduced assembly costs, the adhesive segment continues to command the highest value share through innovation, performance, and integration efficiency across airframe and interior applications.

The sealants segment, accounting for 39.6% of the global aviation adhesives and sealants market, remains indispensable due to its mission-critical role in safety, performance, and environmental protection. Aviation sealants are fundamental to aircraft integrity, ensuring fuel system sealing, cabin pressurization, corrosion prevention, and environmental durability across harsh operational conditions. Their application extends from fuel tank joints, windows, windshields, and fuselage seams to firewalls and engine components, where high-temperature resistance and chemical stability are essential. Modern sealants—such as polysulfide, silicone, and fluorosilicone-based formulations—are engineered to meet stringent aerospace standards including AMS-S-8802 and MIL-PRF-81733, offering superior flexibility and adhesion under thermal cycling and vibration. The ongoing replacement of older solvent-heavy sealants with low-VOC, fast-curing, and environmentally compliant formulations is transforming the segment. In addition, self-healing, UV-curable, and smart sealants are emerging as next-generation solutions to reduce maintenance downtime and extend aircraft life cycles. While adhesives often dominate by volume, sealants carry equally high technical value, as their failure directly impacts flight safety, pressurization, and corrosion control.

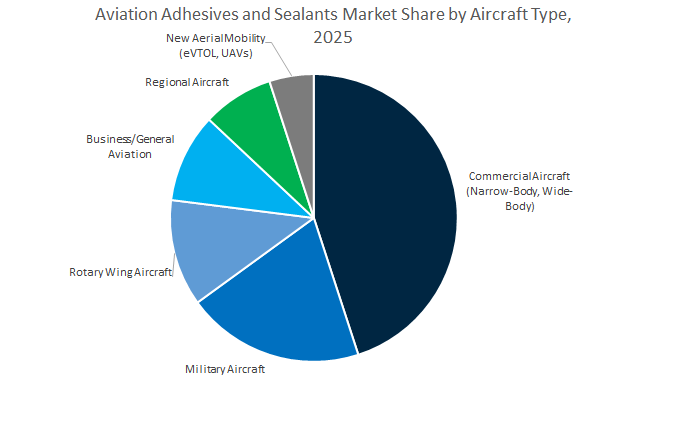

The commercial aircraft segment represents the largest share of the global aviation adhesives and sealants market, capturing approximately 45% of total demand in 2025. This dominance stems from the massive production volumes of narrow-body and wide-body aircraft and the extensive surface area requiring adhesive and sealant applications in each unit. Adhesives are extensively utilized in primary structures (wings, fuselage, control surfaces) and secondary assemblies (doors, interiors, cargo systems), while sealants play an indispensable role in fuel tank sealing, aerodynamic smoothing, and corrosion prevention. The continued production of high-volume platforms such as the Boeing 737 MAX and Airbus A320neo ensures consistent demand, while wide-body models like the A350 and 787 Dreamliner amplify the use of advanced composite bonding materials. With OEMs adopting automation and modular assembly to streamline production, the use of pre-catalyzed film adhesives and precision-applied sealants has risen sharply. The drive toward lightweighting, fuel efficiency, and extended service life also spurs the adoption of next-generation epoxy and silicone technologies, ensuring that commercial aviation remains the core revenue and innovation engine of the industry.

The military aircraft segment, accounting for around 20% of the market share, is defined by its demand for high-performance, mission-critical materials capable of withstanding extreme environmental, mechanical, and operational stresses. Adhesives used in this segment must deliver exceptional shear and peel strength, withstanding vibration, shock, and exposure to jet fuels, de-icing fluids, and hydraulic oils. Sealants play an equally vital role, particularly in fuel systems, canopy sealing, and radar-absorbing composite surfaces used in stealth aircraft. With defense modernization programs driving fleet upgrades, structural retrofits, and composite integration, demand for specialized, qualified bonding materials is growing. Military specifications such as MIL-A-46050 and MIL-PRF-81733 govern this segment, ensuring material consistency and reliability under battlefield conditions. Moreover, the increasing use of additive manufacturing, unmanned aerial vehicles (UAVs), and hypersonic platforms is broadening the market for ultra-high-temperature and low-outgassing adhesives and sealants. Military aviation’s emphasis on performance over cost ensures this segment remains a technologically intensive and strategically significant market, contributing to the overall advancement of aerospace material science.

The emerging aerial mobility segment—encompassing eVTOLs (electric vertical take-off and landing) and UAVs (unmanned aerial vehicles)—is poised to become the fastest-growing segment of the aviation adhesives and sealants industry. Though currently smaller in market size, this category is characterized by rapid technological disruption and intensive use of adhesives for lightweight, modular, and automated manufacturing. eVTOL aircraft, designed for urban air mobility, rely heavily on carbon fiber composites, thermoplastics, and bonded modular assemblies, where structural adhesives replace fasteners to minimize weight and improve aerodynamics. Sealants in this segment must provide environmental protection and electrical insulation for compact, battery-driven propulsion systems. The integration of flame-retardant, electrically insulating, and thermally conductive adhesives has become central to vehicle certification and safety. As the aerospace ecosystem embraces electrification, autonomy, and sustainability, aerial mobility applications are accelerating the adoption of hybrid adhesive-sealant systems, bio-based chemistries, and 3D-printable bonding materials. With major OEMs and startups investing heavily in this domain, this segment represents a transformational growth frontier, setting the pace for next-generation aerospace manufacturing practices.

The Aviation Adhesives and Sealants Market is characterized by technological specialization, sustainability integration, and deep OEM partnerships. The competitive ecosystem is led by Henkel, 3M, Huntsman, PPG Aerospace, and Solvay, each offering differentiated portfolios tailored to critical aerospace needs — from fuel system sealing to composite structural bonding and thermal protection.

Henkel remains the market’s leading provider of structural adhesives and aerospace-grade sealants, supported by its €35 million facility in Spain dedicated to sustainable, high-performance aviation materials. Its LOCTITE® film adhesives offer 15-day open assembly times, enabling flexibility in airframe assembly scheduling. With low-VOC primers such as LOCTITE EA 9258.1 AERO, Henkel continues to set benchmarks in environmental compliance and process stability. The company’s Mobility and Electronics business unit plays a key role in developing lightweight, electrification-compatible materials for next-generation aircraft and e-mobility systems.

3M commands a strong foothold in the aircraft sealants segment, with its AC-275 Class B polysulfide providing −65°F to +250°F continuous resistance and up to 360°F intermittent performance, ideal for engine and fuel tank applications. The AC-735 low-density, non-chromate polysulfide addresses both weight and corrosion concerns in fuselage sealing. Recent R&D achievements have reduced cure times while maintaining 30A hardness, enhancing maintenance turnaround. 3M’s balanced portfolio across epoxy bonding systems and silicone cabin sealants makes it a top choice for OEM and MRO customers seeking single-source reliability.

Huntsman is a leader in structural epoxy and polyurethane adhesives engineered for weight reduction and high fatigue resistance. Its solutions replace mechanical fasteners, achieving up to 75% weight savings in critical airframe joints. The company’s adhesives are qualified across major OEMs, including Boeing, Airbus, and Bombardier. Following its 2024 acquisition of a European composites innovator, Huntsman integrated toughened epoxy technologies for primary structure bonding and impact-resistant interior laminates. The company’s R&D pipeline also includes edge fillers and TPU films optimized for composite protection and transparent structural bonding.

PPG Aerospace dominates the aircraft fuel tank sealant segment with its PR-2001 polythioether range, certified for extreme temperature and chemical resistance. The company’s R&D focus remains on REACH-compliant, low-VOC formulations for OEM and MRO use, addressing tightening European regulations. PPG’s modular adhesive kits and rapid-application systems improve line assembly efficiency, while its specialized polyurethane windshield sealants deliver optical clarity under pressurization and altitude fluctuations. As a result, PPG remains a critical integration partner for OEM assembly lines globally.

Solvay continues to advance benzoxazine- and polyimide-based adhesives capable of withstanding temperatures exceeding 200°C, tailored for engine zone and high-stress composite bonding. Its 2025 capacity expansion in Europe supports rising demand from Airbus and defense manufacturers. Solvay’s portfolio integrates surface primers and film adhesives that reduce surface prep complexity in hybrid metal-to-composite bonding, improving process consistency. Its alignment with carbon fiber composite evolution positions Solvay at the forefront of lightweight aerospace assembly technologies.

The United States aviation adhesives and sealants market continues to lead globally, driven by intensive R&D investments, electric aviation innovation, and MRO infrastructure growth. Leading chemical companies such as 3M Company, Huntsman International LLC, and PPG Industries are spearheading the development of high-toughness epoxy and bismaleimide (BMI) film adhesives tailored for next-generation aircraft structures. The adhesives are critical for bonding large composite fuselage and wing assemblies, enhancing fatigue resistance and weight reduction.

The country’s electric aircraft and eVTOL (Electric Vertical Take-Off and Landing) ecosystem is also emerging as a pivotal growth frontier. Manufacturers are developing fire-retardant, thermally conductive encapsulant foams and sealants designed to prevent thermal runaway in high-density battery systems. Additionally, the U.S. government-backed expansion of MRO facilities is increasing demand for certified aviation-grade sealants, including corrosion-resistant peelable coatings for older commercial and defense fleets.

In parallel, leading manufacturers are collaborating with robotics and automation companies to design automated adhesive dispensing systems, integrating high-viscosity epoxy pastes into AI-guided robotic assembly lines for new-generation aircraft like the Boeing 737 MAX and next-gen regional jets.

Singapore continues to strengthen its position as Asia-Pacific’s premier MRO hub, with rapid advancements in aerospace sealant certification, automation, and additive manufacturing integration. GE Aerospace’s 2025 multi-million-dollar expansion at Seletar Aerospace Park marks a major leap in component repair and advanced MRO technology, significantly increasing demand for aviation polysulfide sealants, fuel tank coatings, and structural adhesives certified under international standards.

The investment also supports Singapore’s transformation into a technology incubation center, focusing on robotics-based repair techniques and precision adhesive applications for aviation structures. Furthermore, the adoption of new international safety and flammability standards (UL9540A-2025) for Energy Storage Systems is influencing material specifications for thermal management adhesives used in electric aviation components.

Singapore’s supply chain resilience strategy — aimed at securing regional sourcing of certified aerospace-grade sealants — aligns with government policies encouraging localized manufacturing and reduced dependency on global suppliers.

China’s aviation adhesives and sealants market is accelerating in tandem with the nation’s domestic aircraft manufacturing growth, especially through the Commercial Aircraft Corporation of China (COMAC). The C919 narrow-body program has triggered unprecedented demand for qualified structural adhesives and flame-retardant materials that meet both Western and Chinese aviation standards.

Government-backed R&D programs are enabling Chinese specialty chemical manufacturers to produce localized epoxy film adhesives and heat-resistant sealants, minimizing reliance on imports. The rapid expansion of UAV and drone sectors has further stimulated innovation in lightweight structural adhesives, gap-filling compounds, and carbon fiber bonding technologies, especially for complex unmanned aerial systems.

China is also harmonizing aviation flammability standards to align with international safety protocols, leading to increased adoption of low-smoke, low-toxicity interior adhesives and flame-retardant sealants across commercial aviation interiors. The country’s policy-driven localization of aerospace materials underscores its goal to achieve self-sufficiency in critical aviation components by 2030.

Germany and the wider European aerospace adhesives and sealants market are at the forefront of sustainable aviation materials and lightweight composite bonding technologies. The Airbus narrow-body production rate increase is driving the high-volume qualification of aerospace film adhesives and prepregs, optimized for automated fuselage and wing assembly.

Europe’s sustainability initiatives, particularly under EASA (European Union Aviation Safety Agency), emphasize the elimination of chrome-based primers and solvent-borne adhesives, encouraging R&D into water-based and 100% solids technologies. The eco-friendly solutions maintain mechanical strength while drastically reducing VOC emissions.

Cutting-edge R&D focuses on adhesives compatible with RTM (Resin Transfer Molding) and LCM (Liquid Compression Molding), allowing for efficient bonding of complex, large composite parts. Additionally, hydrogen aircraft research programs across Germany and France are developing cryogenic-resistant sealants capable of withstanding ultra-low temperatures and preventing hydrogen leakage, a critical step toward future zero-emission aviation.

India’s aviation adhesives and sealants industry is gaining momentum under the “Make in India” initiative, which promotes domestic manufacturing and MRO expansion. The government’s strong policy support for the indigenous aerospace ecosystem has catalyzed partnerships between global chemical firms and local aerospace suppliers to produce certified epoxy adhesives, sealant kits, and composite repair patches for both commercial and defense aircraft.

The country’s composites integration programs, notably through Hindustan Aeronautics Limited (HAL), are driving the adoption of advanced film adhesives and structural bonding systems across indigenous platforms. Concurrently, India’s fast-growing MRO segment is focusing on skill development and certification programs to ensure adherence to international standards for adhesive curing, surface preparation, and application.

The strategic focus on localized aerospace material production is positioning India as a cost-efficient hub for aerospace maintenance adhesives, gap-filling compounds, and aerodynamic smoothing sealants in South Asia.

France plays a pivotal role in advancing specialty polymer and adhesive technologies for the global aviation market, particularly through Arkema Group and its aerospace-focused subsidiaries. The country’s R&D focus is on high-performance polyamides and thermally resistant polymers that serve as critical inputs for engine bonding, fuselage sealing, and defense aviation applications.

Arkema and other French material science companies are also developing lightweight composite-compatible adhesives and sealants tailored for next-generation aircraft, including hybrid and hydrogen propulsion systems. With Airbus headquartered in Toulouse, France remains central to the European aerospace supply chain, focusing on sustainable formulations, flame-retardant materials, and low-emission production processes.

Aviation Adhesives and Sealants Market Report Scope

Aviation Adhesives and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Adhesives, Sealants), By Adhesives Resin Type (Epoxy, Polyurethane, Acrylic, Cyanoacrylate, Silicone, Polyimide, Other Resins), By Sealants Resin Type (Polysulfide, Silicone, Fluorosilicone, Polyacrylate, Polyurethane, Polythioether, Other Resins), By Technology (Solvent-Based, Water-Based, Hot Melt, Reactive, UV/Light Curable, Pressure Sensitive), By Aircraft Type (Commercial Aircraft, Regional Aircraft, Business/General Aviation, Military Aircraft, Rotary Wing Aircraft, New Aerial Mobility), By Application (Fuselage/Airframe Assembly, Wing Assembly, Interiors, Engine Components, Fuel Tanks, Flight Line/Field Repair, Aircraft Windshield & Canopy, Hydraulic/Fluid Systems Sealing), By End-User (OEM, MRO

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Huntsman International LLC, PPG Industries, Inc., Solvay S.A., Hexcel Corporation, Arkema Group, Dow Inc., Sika AG, Master Bond Inc., Permabond LLC, Wacker Chemie AG, DELO Industrial Adhesives, Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

By Adhesives Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Cyanoacrylate

- Silicone

- Polyimide

- Other Resins

By Sealants Resin Type

- Polysulfide

- Silicone

- Fluorosilicone

- Polyacrylate

- Polyurethane

- Polythioether

- Other Resins

By Technology

- Solvent-Based

- Water-Based

- Hot Melt

- Reactive

- UV/Light Curable

- Pressure Sensitive

By Aircraft Type

- Commercial Aircraft

- Regional Aircraft

- Business/General Aviation

- Military Aircraft

- Rotary Wing Aircraft

- New Aerial Mobility

By Application

- Fuselage/Airframe Assembly

- Wing Assembly

- Interiors

- Engine Components

- Fuel Tanks

- Flight Line/Field Repair

- Aircraft Windshield & Canopy

- Hydraulic/Fluid Systems Sealing

By End-Use Sector

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Huntsman International LLC

- PPG Industries, Inc.

- Solvay S.A.

- Hexcel Corporation

- Arkema Group

- Dow Inc.

- Sika AG

- Master Bond Inc.

- Permabond LLC

- Wacker Chemie AG

- DELO Industrial Adhesives

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how aerospace structural bonding and sustainable sealant chemistries are redefining OEM and MRO workflows across composite-intensive airframes and electric aviation platforms. Our analysis reviews temperature-rated epoxy films, fluorosilicone/polysulfide fuel-resistant sealants, and next-gen polythioether systems that compress cycle time while advancing REACH/VOC compliance. It highlights pre-catalyzed film adhesives with extended open time, lightweight toughened formulations for CFRP/Honeycomb, and high-thermal materials that safeguard propulsion and battery subsystems. Mapping certification pathways and cost-of-quality impacts, the study surfaces breakthroughs in nano-toughened epoxies, cryogenic-capable sealants, and automation-ready dispensing that raise first-pass yield and reliability. For engineering, sourcing, quality, and program managers, this report is an essential resource to benchmark performance, de-risk qualification, and align materials strategy with 2025–2034 fleet growth.

Scope Includes

- By Product Type: Adhesives; Sealants

- By Adhesives Resin Type: Epoxy; Polyurethane; Acrylic; Cyanoacrylate; Silicone; Polyimide; Other Resins

- By Sealants Resin Type: Polysulfide; Silicone; Fluorosilicone; Polyacrylate; Polyurethane; Polythioether; Other Resins

- By Technology: Solvent-Based; Water-Based; Hot Melt; Reactive; UV/Light Curable; Pressure Sensitive

- By Aircraft Type: Commercial Aircraft; Regional Aircraft; Business/General Aviation; Military Aircraft; Rotary Wing Aircraft; New Aerial Mobility

- By Application: Fuselage/Airframe Assembly; Wing Assembly; Interiors; Engine Components; Fuel Tanks; Flight Line/Field Repair; Aircraft Windshield & Canopy; Hydraulic/Fluid Systems Sealing

- By End-Use Sector: OEM; MRO

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.