Market Overview: Bio-Organic Acid Market Scale-Up Centered on Lactic Acid, PLA Integration, and Low-Carbon Fermentation Platforms (2025–2034)

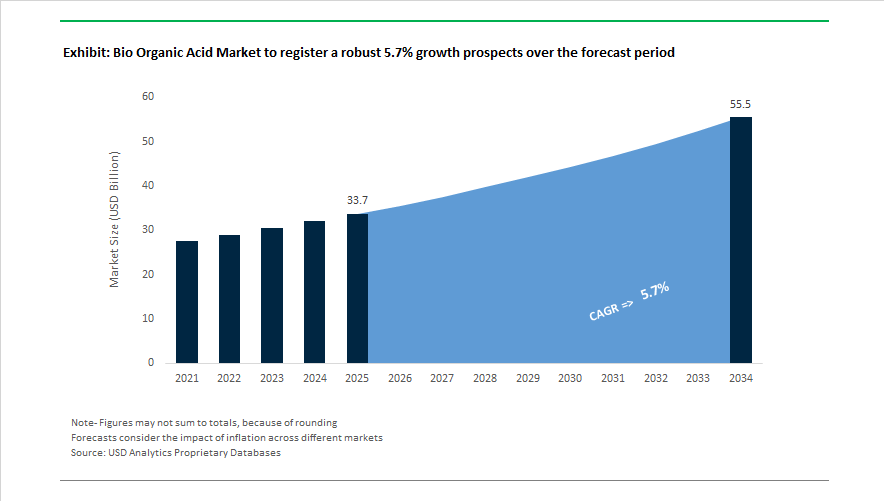

The bio organic acid market is projected to grow from USD 33.7 billion in 2025 to USD 55.5 billion by 2034, registering a CAGR of 5.7% , supported by rising demand for lactic acid, citric acid, gluconic acid, bio-based intermediates, and fermentation-derived building blocks used in bioplastics, food preservation, pharmaceuticals, and specialty chemicals. Production capacity expansion accelerated in 2024 and 2025 as leading manufacturers shifted toward fully integrated fermentation and polymer value chains. In April 2024, CovationBio marked 20 years of PDO production and announced a 33,000-tonne expansion to serve global demand for fermentation-derived propanediol. During Q2 2024, Corbion divested its emulsifiers division to focus on lactic acid and algae platforms. This strategic focus materialized in January 2025 when Corbion commissioned a 125,000-tonne per year lactic acid plant in Rayong, Thailand, designed to supply Polylactic Acid bioplastics and clean-label preservatives. In October 2025, NatureWorks confirmed its integrated Ingeo PLA complex in Thailand remained on schedule for full production by late 2025 to early 2026, combining fermentation and lactide conversion units.

Innovation in fermentation routes and derivative applications is broadening market scope. In January 2024, Nature’s Fynd launched fungi-derived nutritional products using liquid-air interface fermentation, generating high-purity organic acids as metabolic outputs through non-traditional pathways. In March 2025, Roquette expanded its Singapore innovation center to advance bio-citric and gluconic acid use in nutrition and pharmaceutical formulations across Asia. In May 2025, Cargill partnered with Arizona State University to study Priamine bio-amines derived from dimer acids for semiconductor material performance, illustrating expansion of organic acid derivatives into high-technology manufacturing. Sustainability investments continued in December 2025 when Corbion completed energy-efficient boiler upgrades across ester production facilities to lower emissions linked to acid distillation.

Integrated biorefinery models and regional supply chain localization are strengthening long-term resilience. In late 2024, the ADM-LG Chem joint venture secured regulatory approvals for a U.S. lactic acid and PLA production project supported by PTTGC feedstocks, establishing a domestic North American supply base. In January 2026, PTT Global Chemical demonstrated its integrated biorefinery converting waste oils and agricultural residues into bio-organic intermediates for sustainable polymers. In February 2026, BASF introduced biomass-balance ethyl acrylate and related intermediates derived from bio-organic acids at Plastindia, targeting lower-carbon plastics for packaging and agriculture. Corbion’s December 2025 EcoVadis Gold Medal recognition further highlighted supply chain transparency and renewable feedstock sourcing.

Trends and Opportunities Reshaping the Bio Organic Acid Market

Market Trend: Bio-Succinic Acid Re-Positioning as a Strategic Feedstock for Bio-PU and TPU

The Bio Organic Acid Market is undergoing a structural shift as bio-succinic acid transitions from a commodity biofuel precursor into a high-value performance monomer for bio-polyurethanes (Bio-PU) and thermoplastic polyurethanes (TPU). This reflects a pivot toward high-durability, premium applications where sustainability and performance must coexist.

In October 2024, Oleon’s acquisition of A. Azevedo Oleos (Brazil) marked a notable consolidation move enabling vertically integrated diacid and biopolyol supply chains. By securing bio-based feedstocks at source, manufacturers are positioned to produce bio-succinic-derived polyester polyols that support automotive coatings, corrosion-resistant materials, and marine sealants. Industrial datasets from early 2025 further demonstrate that bio-succinic acid blends outperform traditional adipic-acid-based polyols by up to 15% in hydrolysis resistance, positioning it as a strategic enabler for outdoor infrastructure, transportation assets exposed to moisture, and next-gen marine-grade elastomers.

Market Trend: Lactic Acid Diversification Unlocking Electronics and Low-Toxicity Solvent Applications

The historical focus on PLA has expanded into a wider value pool, driven by the evolution of high-purity lactate esters serving as environmentally safe solvents for semiconductor fabrication and microelectronics. This trend is fueled by regulatory pressures to eliminate legacy VOC solvents and improve workplace safety benchmarks.

As of December 2025, the high-purity lactate ester segment is projected to reach approximately USD 850 million. These esters are increasingly used for wafer cleaning, photoresist removal, and low-toxicity precision cleaning. Strategically, Europe’s first fully integrated biorefinery under construction by Futerro in Normandy (125,000 tons/year lactic acid capacity) is expected to supply industrial-grade lactate feedstocks and biodegradable chelating agents designed to replace phosphonate-based water treatment chemicals. This plant reinforces Europe’s aim to build circular chemical economies aligned with EU Green Deal requirements.

Market Opportunity: Bio-Itaconic Acid Driving the Emergence of Biodegradable Superabsorbent Polymers (SAP)

The hygiene and personal care categories—valued at USD 9.8 billion for SAP applications—represent a transformational opportunity for bio-based organics. The pressure to eliminate microplastics in disposable products is accelerating demand for biodegradable SAPs using bio-itaconic acid as a co-monomer.

A key breakthrough occurred in July 2024 when ZymoChem launched BAYSE™, the world’s first fully bio-based and biodegradable SAP. Performance testing confirms liquid retention comparable to petrochemical sodium polyacrylate. Future scalability could also be driven by advancements in microbial carbon utilization. A September 2025 Green Chemistry study demonstrated that synthetic Pichia pastoris can convert captured CO₂ directly into itaconic acid at titers of 12 g/L—introducing a possible carbon-negative feedstock pathway that improves both sustainability metrics and geographic feedstock optionality.

Market Opportunity: Bio-Based Gluconic Acid Supporting Low-Carbon Construction and Circular Infrastructure

Bio-gluconic acid and sodium gluconate are expanding beyond food and pharmaceutical uses to become critical additives in low-carbon construction chemistry. As concrete decarbonization accelerates, gluconates are helping LEED-compliant builders reduce cement intensity while maintaining structural reliability.

The COP30 Biofuture Platform (November 2025) recognized bio-based construction chemicals as priority materials for Net Zero 2050 roadmaps. Sodium gluconate functions as a hydration retarder that enables a 15 to 25% reduction in cement content. Complementing this, research conducted at the University of Stuttgart (May 2025) demonstrates microbial biomineralization processes that use bio-organic acids to produce concrete with compressive strength above 50 MPa. Bio-gluconates therefore form the backbone of an emerging wastewater-to-infrastructure circular economy model, where industrial byproducts feed directly into structural materials.

Bio Organic Acid Market Share and Segmentation Insights

Market Share by Product Type: Bio Lactic Acid Leads While Succinic and Adipic Acids Signal Next-Phase Growth

Bio lactic acid commands the largest share of the Bio Organic Acid Market at 42% in 2025, driven by rapid expansion of PLA bioplastics across compostable packaging, 3D printing filaments, and textile fibers. Producers are increasingly adopting second-generation lignocellulosic feedstocks to reduce food crop competition and improve sustainability metrics. Bio citric acid holds the second-largest position, widely used as an acidulant, preservative, and pH regulator in food, beverages, and pharmaceuticals, with production concentrated in China via molasses and starch fermentation. Bio acetic acid remains a mature platform chemical supporting bio-based solvents, esters, and vinyl acetate monomer, though petrochemical price competition constrains margins. Bio succinic acid is emerging as a high-growth building block for PBS bioplastics and polyurethanes, supported by capacity additions in Europe and North America. Bio gluconic acid serves niche industrial roles, while bio adipic acid targets future bio-nylon value chains and bio fumaric acid remains limited by fermentation economics.

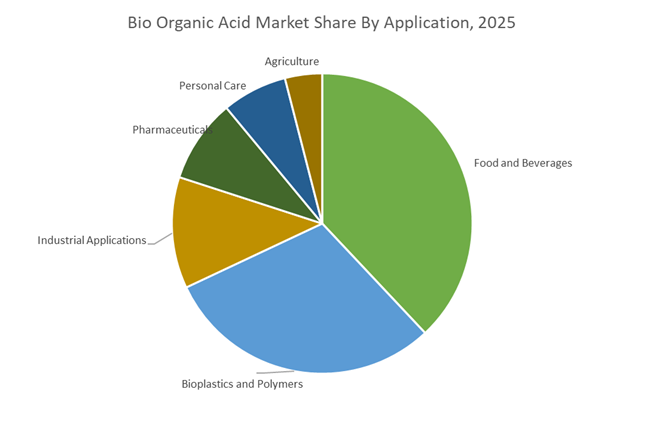

Market Share by Application: Food Leadership Gives Way to Rapid Bioplastics Adoption

Food and beverages represent the largest application segment with a 38% share in 2025, anchored by citric, lactic, and acetic acids used as preservatives, flavor enhancers, and pH adjusters. Clean-label positioning and natural ingredient sourcing are accelerating the shift toward bio-based organic acids. Bioplastics and polymers form the fastest-growing demand center, led by PLA from lactic acid, followed by PBS from succinic acid and PHA, as single-use plastic bans and corporate net-zero commitments drive material substitution. Industrial applications consume gluconic acid for metal chelation, alongside organic acids in concrete admixtures, leather tanning, and textile processing, tracking manufacturing output. Pharmaceuticals utilize bio organic acids as excipients and formulation aids, favoring fermentation-based supply for purity assurance. Personal care demand is rising for lactic, citric, and gluconic acids in skincare and oral care, while agriculture remains an emerging niche through silage additives, plant growth promoters, and biodegradable films.

Competitive Landscape Analysis of the Bio Organic Acid Market

The bio organic acid market is accelerating as food manufacturers, polymer producers, and industrial formulators pivot toward fermentation-derived intermediates with lower carbon footprints. Competition is centered on vertically integrated feedstock access, advanced microbial engineering, mass balance production models, and downstream biomaterials integration. Market leaders are differentiating through predictive preservation tools, large-scale fermentation hubs, biodegradable polymer development, and AI-enabled bio-manufacturing. Strategic priorities in 2026 include localized production to reduce Scope 3 emissions, expansion of lactic and succinic acid capacity in Asia-Pacific, and tighter integration between agriculture, biotechnology, and specialty chemicals to serve clean-label food, sustainable packaging, textiles, and next-generation biomaterials.

Corbion leads lactic acid innovation with vertically integrated fermentation platforms

Corbion enters 2026 under its BRIGHT 2030 strategy, positioning itself as a global leader in lactic acid and algae-based fermentation. The company commissioned a world-scale lactic acid facility in Thailand during late 2025 and early 2026, strengthening Asia-Pacific supply for bio-based food and biomaterial applications. Corbion scaled its Natural Mold Inhibition Model, enabling bakeries to eliminate synthetic propionates while preserving shelf life in clean-label breads. Through its vertical fermentation model, Corbion integrates algae-derived nutrition with lactic acid preservation systems, delivering multifunctional food solutions. Its BRIGHT roadmap targets higher-margin specialty ingredients and disciplined capital deployment toward biomaterials.

Cargill powers global bio organic acid production through agricultural feedstock control

Cargill leverages unmatched agricultural supply chain access to support large-scale bio-manufacturing of organic acids. In 2026, the company earned the BIG Innovation Award for deploying AI and predictive analytics across bio-industrial operations. Cargill broke ground on a major Beijing plant expansion, adding independent production lines for functional food systems and fermentation components. It remains a dominant supplier of dextrose feedstocks used in global succinic and lactic acid production. Cargill’s strategy combines global expertise with localized bio-manufacturing hubs in China and India, reducing Scope 3 emissions while supporting rapid growth in regional clean-label and bio-industrial markets.

BASF scales bio organic intermediates via mass balance and Verbund integration

BASF is advancing the green transformation of chemicals by integrating bio-based feedstocks into its Verbund manufacturing network. Using its mass balance approach, BASF produces drop-in organic acids from bio-naphtha with reduced carbon intensity. In October 2025, the company partnered with International Flavors & Fragrances to develop next-generation bio-based polymers and enzymes for sustainable home care and textiles. BASF also introduced biodegradable polymers derived from bio-succinic acid for agricultural films and apparel applications in 2026. Its core strength lies in combining biotechnology, protein engineering, and global infrastructure to rapidly scale new bio organic acid pathways.

Archer Daniels Midland expands low-carbon organic acids through nutrition-focused biomanufacturing

Archer Daniels Midland has repositioned itself as a nutrition and bio-solutions leader, producing bio-based citric, lactic, and acetic acids at industrial scale. Its Industrial BioSolutions segment delivers plant-based emulsifiers and solvents for agrochemical and industrial use. ADM partnered with Solugen to build a low-carbon organic acid facility in Marshall, utilizing high-purity dextrose as a renewable carbon source. With over 450 crop procurement locations and 330 manufacturing plants, ADM operates one of the world’s most extensive bio-feedstock logistics networks. In 2026, ADM is aligning capital deployment with evolving US bio-product policies to strengthen its clean-label ingredient leadership.

NatureWorks integrates bio organic acids into global PLA production ecosystems

NatureWorks, a joint venture between Cargill and PTT Global Chemical, is the world’s leading producer of polylactic acid and a major downstream consumer of bio organic acids. In late 2025 and 2026, the company partnered with ABB to automate its Thailand greenfield facility, integrating sugar fermentation, lactic acid distillation, and polymerization into a single site. NatureWorks launched Ingeo 3D Series and Ingeo Extend in 2026, delivering high-performance bio-polymers with up to 80% lower greenhouse gas emissions. Its PLA platforms dominate sustainable packaging, 3D printing, and medical fiber applications, reinforcing demand for fermentation-derived organic acids.

Genomatica licenses industrial microbes to accelerate global bio organic acid adoption

Genomatica operates as a bio-manufacturing technology provider, licensing high-efficiency microbial strains to chemical producers worldwide. Its commercial-scale-first approach enables fermentation volumes exceeding 600 cubic meters for bio-based intermediates. During 2025 and 2026, Geno expanded its Bioengineering Solutions group to support yeast fermentation customers producing food ingredients and organic acids. The company also extended its BioBDO partnership with BASF, raising licensed production to 75,000 metric tons and adding Southeast Asian sites. Geno’s 2026 strategy focuses on pathway diversification, moving into adipic acid, bio-butadiene, and nylon intermediates to address a multibillion-dollar bio-organic chemicals opportunity.

United States Bio Organic Acid Market: Corn-to-Chemicals Scale-Up and Policy-Backed Decarbonization

The United States bio organic acid industry is advancing through commercial-scale commissioning, nearshoring incentives, and decarbonization credits tied to regenerative agriculture. In July 2025, Qore, a joint venture of Cargill and HELM AG, commissioned its USD 300 million facility in Eddyville, Iowa. The plant produces 66,000 metric tons per year of QIRA, a bio-based 1,4-butanediol derived from locally sourced dent corn. As a drop-in replacement for fossil-based intermediates, QIRA enables apparel and automotive manufacturers to decarbonize polymer value chains without retooling.

Trade and climate policy are reinforcing domestic investment. New import duties on synthetic organic acids introduced in early 2025 have incentivized nearshoring, contributing to a reported 24% increase in domestic supply-chain investment by U.S. specialty chemical firms seeking tariff insulation. At the same time, the United States Department of Energy updated its Bio-economy Framework in 2025 to allow enhanced carbon-capture credits for producers using regenerative agriculture feedstocks. This policy directly improves the cost competitiveness of bio-succinic and related acids, accelerating adoption across packaging, coatings, and performance materials.

Thailand Bio Organic Acid Market: Integrated PLA Platforms and Bio-Circular Feedstock Economics

Thailand has emerged as a Southeast Asian hub for bio organic acids through integrated infrastructure and a national Bio-Circular-Green model. NatureWorks, jointly owned by PTT Global Chemical and Cargill, secured USD 350 million in financing in late 2024 from Krungthai Bank to complete its fully integrated Ingeo PLA complex. The site, reaching full operations in 2025–2026, includes dedicated lactic acid fermentation and polymerization units, anchoring regional supply for bio-based polymers and acids.

Feedstock proximity is a structural advantage. The Nakhon Sawan Biocomplex sources sugarcane within a 50-kilometer radius, reducing Scope 3 emissions for lactic acid production by an estimated 30% versus traditional sourcing. Foreign direct investment is reinforcing capacity depth. Corbion announced construction of a new concentrated lactic acid facility in Thailand to serve rising demand for high-purity preservatives across Asian food and beverage markets. Together, integrated assets and localized biomass position Thailand as a cost-competitive exporter of bio organic acids.

India Bio Organic Acid Market: BioE3-Led Scale-Up and O2C Integration

India’s bio organic acid industry is being catalyzed by the BioE3 policy and ecosystem-level scaling mechanisms. Approved in August 2024, the BioE3 framework prioritizes bio-based chemicals and enzymes as core pillars for national self-reliance, shifting industrial models from petrochemical dependence to circular biomanufacturing by 2026. This policy clarity has accelerated investment across fermentation-derived organic acids used in pharmaceuticals, textiles, and food processing.

Capacity formation is supported by institutional expansion. The Office of the Principal Scientific Adviser announced in 2025 the expansion of Science and Technology clusters from 8 to 25 hubs, with Maharashtra and Gujarat designated for bio organic acid manufacturing to bridge startup innovation and industrial scale. Energy majors are aligning upstream feedstocks with biomanufacturing. Reliance Industries Limited has begun integrating bio organic acid modules into its oil-to-chemical refineries, targeting bio-adipic acid synthesis for sustainable textiles. This convergence of policy, infrastructure, and feedstock security is positioning India as a competitive producer for both domestic and export markets.

China Bio Organic Acid Market: Bioeconomy Mandates and Controlled Technology Sovereignty

China’s bio organic acid industry is scaling under centralized bioeconomy mandates while protecting proprietary technologies. Under the 14th Five-Year Plan for Bio-economy Development, the National Development and Reform Commission mandated a steady increase in bioeconomy value by late 2025, with synthetic biology prioritized for organic acid production. This directive has accelerated fermentation capacity and downstream integration across multiple provinces.

Sustainable monomer production is moving from pilot to commercial scale. In early 2025, BASF commenced operations at its first commercial loopamid facility in Caojing, Shanghai, using bio organic intermediates and recycled monomers with Global Recycled Standard certification. At the same time, China tightened technology controls. Synthetic biology was added to the Catalogue of Technologies Restricted from Export during 2024–2025, underscoring the strategic value of proprietary microbial strains used in bio-acid fermentation. This combination of rapid scale-up and IP protection is shaping China’s competitive posture.

Germany and the European Union Bio Organic Acid Market: Energy Efficiency, Certified Biomass, and Catalytic Throughput

Germany and the wider European Union are advancing bio organic acids through energy efficiency investments, certified biomass availability, and catalytic innovation. At its Ludwigshafen site, BASF began constructing one of the world’s most powerful heat pumps in Q1 2025 to generate CO2-free steam. This infrastructure materially reduces the energy intensity of bio-succinic and bio-lactic acid purification, aligning production with EU decarbonization objectives.

Feedstock quality is improving alongside policy targets. Progress toward the EU’s Farm-to-Fork goal of 25% organic farming by 2025 has expanded access to non-GMO biomass, enabling German producers to command a premium for Bio-EU certified sustainable chemicals. Conversion efficiency is also rising. In November 2025, BASF unveiled its X3D® catalyst technology, using 3D-printed open structures to improve bio organic acid conversion throughput by up to 20% versus conventional catalyst shapes. These advances consolidate Europe’s role as a premium, compliance-driven market for bio organic acids.

Country-Level Strategic Snapshot: Bio Organic Acid Industry

Bio Organic Acid Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

United States

|

Nearshoring and decarbonization

|

QIRA bio-BDO commissioning, import duties, regenerative feedstock credits

|

|

Thailand

|

Integrated PLA and BCG model

|

Ingeo complex financing, localized sugarcane sourcing, lactic acid FDI

|

|

India

|

Policy-led biomanufacturing

|

BioE3 rollout, expanded S&T clusters, O2C bio-adipic integration

|

|

China

|

Bioeconomy scale with IP control

|

Five-Year Plan mandates, loopamid commercialization, export tech restrictions

|

|

Germany / EU

|

Energy efficiency and premium certification

|

CO2-free steam, organic biomass access, X3D catalyst throughput gains

|

Bio Organic Acid Market Report Scope

Bio Organic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.7 Billion

|

|

Market Size (2034)

|

$55.5 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Bio Lactic Acid, Bio Succinic Acid, Bio Citric Acid, Bio Acetic Acid, Bio Adipic Acid, Bio Gluconic Acid, Bio Fumaric Acid), By Production Process (Microbial Fermentation, Enzymatic Conversion, Catalytic Biomass Upgrading, Hybrid Biotic Chemical Synthesis), By Feedstock Source (First Generation Feedstocks, Second Generation Feedstocks, Third Generation Feedstocks, Waste to Acid Feedstocks), By Application (Bioplastics and Polymers, Food and Beverages, Pharmaceuticals, Personal Care, Agriculture, Industrial Applications), By End User Industry (Packaging and Consumer Goods, Healthcare and Nutrition, Agriculture and Animal Feed, Automotive and Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corbion, Cargill, NatureWorks, BASF, Archer Daniels Midland, Novonesis, Roquette, Praj Industries, Genomatica, Succinity, Qore, Wuhan Youji Industries, BBCA Group, Mitsubishi Chemical Group, Lotte Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bio Organic Acid Market Segmentation

By Product Type

- Bio Lactic Acid

- Bio Succinic Acid

- Bio Citric Acid

- Bio Acetic Acid

- Bio Adipic Acid

- Bio Gluconic Acid

- Bio Fumaric Acid

By Production Process

- Microbial Fermentation

- Enzymatic Conversion

- Catalytic Biomass Upgrading

- Hybrid Biotic Chemical Synthesis

By Feedstock Source

- First Generation Feedstocks

- Second Generation Feedstocks

- Third Generation Feedstocks

- Waste to Acid Feedstocks

By Application

- Bioplastics and Polymers

- Food and Beverages

- Pharmaceuticals

- Personal Care

- Agriculture

- Industrial Applications

By End User Industry

- Packaging and Consumer Goods

- Healthcare and Nutrition

- Agriculture and Animal Feed

- Automotive and Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bio Organic Acid Industry

- Corbion

- Cargill

- NatureWorks

- BASF

- Archer Daniels Midland

- Novonesis

- Roquette

- Praj Industries

- Genomatica

- Succinity

- Qore

- Wuhan Youji Industries

- BBCA Group

- Mitsubishi Chemical Group

- Lotte Chemical

*- List not Exhaustive