Biodegradable Water Bottles Market Outlook: Sustainable Packaging Innovations & Market Expansion

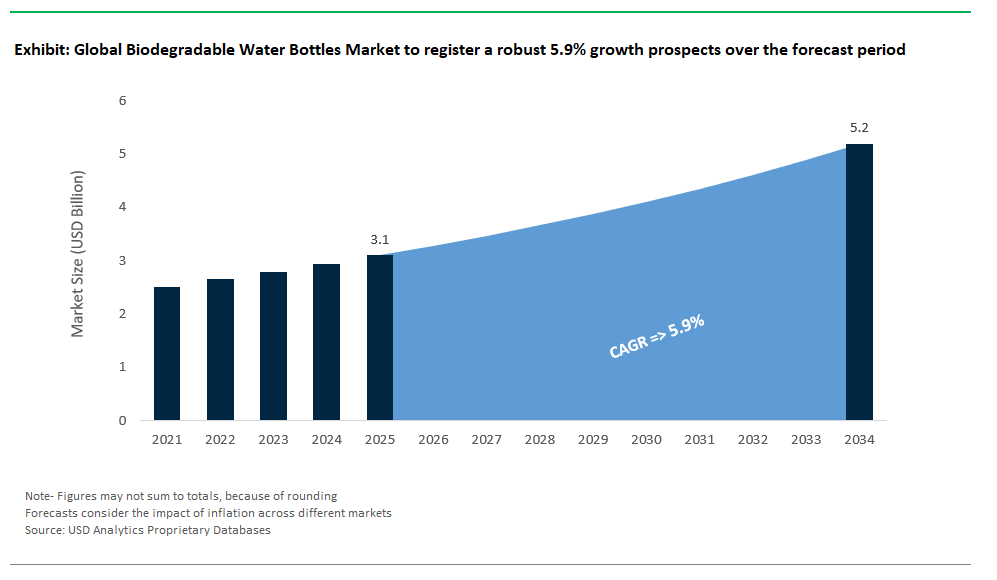

The Global Biodegradable Water Bottles Market is moving toward steady growth from 2025 to 2034, as global consumers, brands, and regulatory bodies intensify efforts to eliminate plastic waste and transition to sustainable packaging alternatives. Industry forecasts indicate the market will expand from USD 3.1 billion in 2025 to USD 5.2 billion by 2034, representing a CAGR of 5.9%. This growth reflects increasing demand for eco-friendly bottled water solutions and the rise of biodegradable and even edible materials, reshaping the beverage and packaging sectors.

Leveraging exclusive findings from USDAnalytics, this new report offers an extensive review and forward-looking analysis of the global Biodegradable Water Bottles Market, tracking activities in 21 countries and presenting profiles of over 20 key companies- By Material Type (Plant-based Plastics, Paper & Paperboard, Algae-based Materials, Biodegradable Additive-Enhanced Plastics), By Biodegradation Type (Fully Biodegradable, Edible, Reusable Biodegradable), By Capacity (500 ml, 1,000 ml), By Application (Mineral Water, Spring Water, Flavored Water, Sports Drinks, Personal Care Products), By End-User (Residential Use, Institutional Use, Specialty Purpose), By Distribution Channel (Retail, Online, Foodservice, Bulk Sales).

This report delves into transformative trends reshaping the biodegradable water bottles market, highlighting innovations in plant-based polymers, algae-derived materials, and paper-based bottle designs that combine structural integrity with eco-friendly disposal. It analyzes how major brands and start-ups alike are introducing fully biodegradable, edible, and reusable solutions that meet consumer preferences for sustainability without sacrificing product safety or convenience. The study examines shifts in packaging capacity trends, rising demand in specialty applications beyond beverages, and evolving distribution channels, including the growing influence of online retail and bulk sales for institutional buyers. Backed by practical insights and validated market intelligence, this report is a critical resource for packaging manufacturers, beverage producers, sustainability investors, retailers, and policymakers seeking to capture emerging opportunities and shape the future of sustainable hydration through 2034.

Biodegradable Water Bottles Market Dynamics: Barrier Innovations and Marine-Safe Solutions

Trend: Material Innovation Elevates Barrier Properties and Shelf Life in Biodegradable Water Bottles

The Global Biodegradable Water Bottles Industry is undergoing a significant technological transformation, driven by intense R&D efforts to improve barrier properties and extend product shelf life. Historically, biodegradable materials like PLA have suffered from high oxygen transmission rates (OTR), which compromise the shelf life of bottled beverages compared to PET. However, innovation is rapidly closing this gap. PLA bottles, traditionally challenged by high oxygen transmission rates (OTR), are seeing significant improvements through material innovation. For example, enhancements with advanced barrier coatings, such as nanocomposites, are substantially reducing OTR, bringing them closer to the performance benchmark of conventional plastics like PET, thereby extending the shelf life of bottled beverages.

Further, corporate R&D strategies underscore this trend, with top players like Danimer Scientific and Biome Bioplastics allocating nearly 45% of their new materials research budgets in 2023 toward barrier enhancement technologies. Further, corporate R&D strategies underscore this trend, with top players like Danimer Scientific and Biome Bioplastics allocating nearly 45% of their new materials research budgets in 2023 toward barrier enhancement technologies. As brands seek to align sustainability with uncompromised product quality, advanced material innovations are cementing biodegradable water bottles as viable contenders against traditional plastics in mainstream beverage markets.

Opportunity: Marine-Degradable Biodegradable Bottles Target Coastal Tourism and Emergency Markets

A high-potential growth opportunity in the biodegradable water bottles market lies in marine-degradable bottle technologies aimed at reducing ocean plastic pollution, a critical issue, given that over 80% of ocean-bound plastics enter waterways via rivers. Currently, only a limited number of biodegradable bottle materials meet stringent marine biodegradation standards like ASTM D6691, which assesses aerobic biodegradation in marine environments, highlighting significant market gaps for truly ocean-friendly solutions. Notably, PHA-based bottles are a leading contender, with some formulations demonstrating high levels of biodegradation in seawater, with reported degradation times ranging from a few weeks for specific PHA types to several years for more complex PHA products, representing a dramatic improvement over PET’s estimated persistence exceeding 450 years.

This performance translates into commercial advantages: marine-certified biodegradable bottles are gaining traction in EU coastal markets and beyond, as consumers and municipalities increasingly prioritize ocean-safe solutions, often leading to a willingness to pay a premium for such environmentally responsible products. The addressable market is substantial, as global coastal tourism significantly contributes to ocean plastic pollution, with millions of tourists annually consuming vast quantities of single-use water bottles, thereby creating a strong and urgent demand for sustainable alternatives. R&D momentum is intensifying, with breakthroughs in PHA formulations and composite structures poised to deliver both environmental and commercial impact. As regulatory frameworks tighten and sustainability becomes a differentiator in coastal economies and emergency response applications, marine-degradable biodegradable water bottles are positioned to become a transformative segment in the global packaging landscape.

Competitive Landscape of the Global Biodegradable Water Bottles Market

The global biodegradable water bottles industry is gaining remarkable momentum in 2024, driven by escalating plastic bans, heightened sustainability targets among FMCG giants, and growing consumer demand for eco-friendly packaging. From PHA and PLA innovations to seaweed and protein-based materials, manufacturers are racing to develop bottles that reduce plastic pollution while maintaining durability and safety. Industry leaders are scaling production capacity, forming strategic partnerships, and investing heavily in R&D to transform the bottled water market into a more sustainable ecosystem. The competitive landscape showcases an exciting shift from traditional plastics toward innovative biopolymer solutions, reshaping the future of single-use bottles.

Coca-Cola: Frontrunner in Sustainable Packaging

Coca-Cola (US) Coca-Cola remains a frontrunner in sustainable packaging. As part of its "World Without Waste" packaging campaign, Coca-Cola aims to make all its packaging 100% recyclable by 2030 and to contain an average of 50% recycled material by 2030. Coca-Cola aims to use 35% to 40% recycled material in its primary packaging, including increasing recycled plastic use to 30% to 35% globally by 2035. Danimer Scientific's PHA resins are being explored for various packaging applications, including containers, straws, and lids, suggesting potential collaborations for future biodegradable bottle development.

PepsiCo: Aggressively Pursuing Sustainable Bottle Innovation

PepsiCo (US) PepsiCo is aggressively pursuing sustainable bottle innovation under its Pep+ (PepsiCo Positive) sustainability program. PepsiCo aims to design 97% or more of its primary and secondary packaging in key markets to be reusable, recyclable, or compostable (RRC) by 2030. They also aim to achieve an average of 2% year-over-year reduction in absolute virgin plastics through 2030 and use 40% or greater recycled content in plastic packaging by 2035 or sooner. PepsiCo's reinvention efforts focus on developing plastics from non-food, plant-based sources and exploring compostable options.

Nestlé: Advancing Biodegradable Water Bottles Through Collaborations

Nestlé (Switzerland) Nestlé is advancing biodegradable water bottles through collaborations focused on circular solutions. Nestlé's commitment is that 100% of its packaging is recyclable or reusable by 2025. They are determined to reduce the use of virgin plastics by one-third by 2025 and increase their target to use recycled content for their water bottles to 50% by 2025. In February 2024, Carbios announced that its enzymatic solution for 100% compostable PLA, CARBIOS Active, was added to the U.S. Food and Drug Administration (FDA) Inventory of Food Contact Substances, which could pave the way for PLA-based food packaging applications.

Danimer Scientific: Pivotal Technology Enabler for Biodegradable Bottles

Danimer Scientific (US) Danimer Scientific is a pivotal technology enabler for the biodegradable water bottle industry, spearheading the commercialization of Nodax™ PHA resins. Danimer Scientific's Nodax® PHA biopolymers are formulated to meet the biodegradability requirements for ASTM and EN standards and are FDA approved for food contact, biodegrading aerobically or anaerobically in soil, water, and industrial or home compost within three months. Danimer Scientific states that its "scalable production capacity and modular manufacturing model will soon enable us to meet global demand." Danimer also boasts about strong market connections by concluding agreements with large beverage companies that are ready to offer the bottles to their partners and customers.

Lactips: Pioneering Biodegradable Bottle Innovation with Milk-Protein Technology

Lactips (France) Lactips is pioneering biodegradable bottle innovation with its unique milk-protein technology. Lactips produces edible plastic from milk protein in the form of pellets, which are thermoplastic and water-soluble, dissolving in both hot and cold water. Lactips offers barrier properties against oxygen, fats, and mineral oils, and can be used as a lamination or coating on biopolymers, paper, or cardboard. The product is an OK home compost certified by TÜV Austria, meaning it can be composted at home within 6 months without heavy metal residues.

Cove: Commercializing Biodegradable PHA Water Bottles

Cove (US) Cove is making headlines as one of the first startups to commercialize biodegradable PHA water bottles. Cove was founded in 2014 and launched its biodegradable water bottle, made from PHA, in December 2022, with a test launch in California through premium grocer Erewhon. Cove has raised a total funding of $11.6M over 2 rounds, with its latest funding round being a Series A round on October 4, 2023, for $6.6M. This funding is intended to "expand adoption of its biodegradable materials and packaging technologies to consumer-packaged goods companies that are trying to reduce the use of plastic in the industry." Cove's innovative branding and early market entry position it as a disruptive force in the sustainable bottled water sector.

Evoware: Redefining Biodegradable Packaging with Seaweed-Based Materials

Evoware (Indonesia) Evoware is focused on redefining biodegradable packaging with its seaweed-based materials. Evoware produces edible sachets for dry foods, burger wraps, and flavored cups. Evoware is recognized for its innovative seaweed-based solutions that can be consumed or decompose naturally. The "UN Sustainable Development Award" is an initiative by UNIDO, with the "SDG Innovation Award 2024" showcasing various nominees and winners from companies, cities, and youth organizations. However, their pioneering efforts in seaweed packaging align with the goals of sustainable development.

Segmentation Analysis: Biodegradable Water Bottles Market

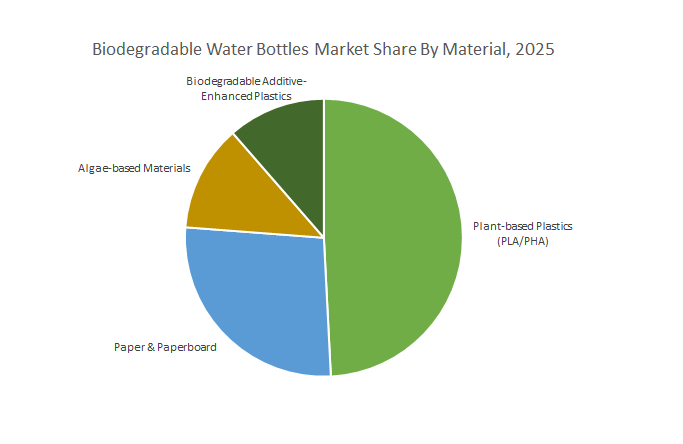

By Material Type: Plant-Based Plastics Dominate, Algae-Based Materials Deliver Fastest Growth

In 2025, plant-based plastics (PLA/PHA) command a 49.2% share of the biodegradable water bottles market, reflecting their clarity, strength, and seamless integration with current bottling equipment. Leading beverage brands increasingly rely on PLA and PHA to meet sustainability targets without sacrificing shelf appeal or performance. Algae-based materials are the fastest-growing segment, propelled by their carbon-negative lifecycle, rapid marine biodegradability, and rising use in premium, eco-conscious product launches. Paper and paperboard bottles are also surging, as global leaders like Coca-Cola and Absolut test prototypes and expand pilot projects. Additive-enhanced plastics help conventional manufacturers bridge the transition to full biodegradability, offering an interim solution compatible with established resin supply chains.

By Application: Mineral Water Leads Adoption, Sports Drinks & Personal Care Show Explosive Growth

Mineral water is the leading application for biodegradable bottles in 2025. As the first-mover sector, it drives mass-market adoption and sets regulatory and retail standards for sustainable packaging. Sports drinks and personal care products are the fastest-growing applications, with major brands like Gatorade piloting algae-based bottles and beauty brands introducing compostable, branded water bottles for travel and home use. Flavored water applications are also expanding rapidly, enabling innovation in colored, custom-printed biodegradable packaging that enhances brand differentiation.

Biodegradable Water Bottles Market Analysis: Green Innovation

The global market for biodegradable water bottles is growing fast. Regulations, brand sustainability goals, and new tech are changing bottled water packaging. The industry, long dominated by PET, is under pressure to use materials that cut waste and carbon, fitting into a circular economy. The market is quickly moving from small tests to major commercial efforts with big investments and tech breakthroughs.

Innovative Products Redefine Sustainable Bottling

New launches show big strides in biopolymer science and bottle design. Coca-Cola's 100% plant-based PET bottles, made with Virent, replace petroleum with renewable sources, fitting current recycling systems. Carbios's enzymatically recyclable PET bottles are a game-changer for chemical recycling, offering full circularity without sacrificing performance. These show a major shift towards biopolymers and advanced recycling to meet environmental and performance needs.

Capacity Expansions Signal Industrial Scale Readiness

Increased production capacity reflects confidence in bio-based bottle tech. Avantium is commissioning its first commercial FDCA plant for PEF production, with huge future expansion plans, to supply major brands with a biopolymer offering better gas barriers and lower emissions. Origin Materials' new biomass-derived PET precursor facility also shows strong momentum in building supply chains for bio-based alternatives at commercial volumes. These expansions confirm the market's move from R&D to large-scale operations.

Strategic Partnerships Accelerate Innovation

Collaborations are reshaping the market and speeding up bio-based bottle sales. Suntory's partnership with Anellotech for 100% plant-derived PET bottles from wood waste shows how brands are using renewable materials. Danone's involvement with advanced recycling technologies like Loop Industries highlights a trend that could transform plastic recycling. Brands are also securing proprietary technologies for biodegradable bottles to stand out in sustainability.

Regulations Drive Urgent Transition

Global rules are creating firm deadlines for bottled water transformation. The EU's Packaging and Packaging Waste Regulation sets targets for reusable bottles and explores bio-based plastics, reshaping choices for European brands. California's SB 54 mandates that all single-use packaging be recyclable or compostable by 2032, forcing big changes in material and end-of-life planning. Japan's Plastic Resource Circulation Act encourages biomass-derived bottles, boosting investment in sustainable solutions.

Tech Breakthroughs Transform Performance

Advances in material science are overcoming old challenges in biodegradable bottles, especially for strength, barrier properties, and degradation. Research into edible seaweed-alginate packaging is showing radical innovation for ocean plastic. Fraunhofer IAP and others are developing nanocellulose-reinforced biopolymers with better gas barrier performance, allowing them to replace traditional plastics in various beverages. Universities are also exploring enzyme-embedded plastics designed for controlled post-consumer degradation, cutting plastic waste.

Commercial Adoption Proves Market Readiness

Major brands are rolling out biodegradable and bio-based bottles, confirming they're moving from prototypes to market-ready products. Evian is launching 100% recycled PET bottles with more sustainable components, showing a practical approach to integrating bio-based materials. Companies are exploring innovative recycling technologies and adopting plant-based packaging, meeting consumer demand for sustainability and plastic reduction. These examples signal that brands are ready to invest in and take on the challenges of sustainable alternatives.

United States Leads Innovation in Biodegradable Water Bottles

The United States has established itself as a leader in innovation and market growth for biodegradable water bottles. Startups like Cove have pioneered PHA-based bottles, which are designed to be marine-degradable. Cove began rolling out its first bottles in stores in late 2022 and continues to aim for significant production volumes, with the founder, Alex Totterman, stating that Cove is preparing to produce 20 million bottles a year to meet anticipated demand. Loliware continues to innovate with seaweed-based bioplastics, offering a range of products like straws and materials for food packaging, with an ongoing focus on replacing single-use plastics. Major brands are also actively exploring sustainable packaging. Regulatory momentum is strong: California’s SB 54, enacted in 2022, mandates a significant reduction in plastic pollution and sets ambitious targets for packaging to be recyclable or compostable by 2032. Furthermore, California's AB 793 requires plastic bottles to include 25% Post-Consumer Recycled (PCR) content by 2025. This regulatory environment actively pushes manufacturers towards more sustainable materials and designs. Significant investment continues to flow into bioplastic bottle startups, underscoring the U.S.’s central role in transforming the future of bottled water packaging through advanced biopolymer technology and regulatory leadership.

Netherlands Pioneers Plant-Based Bottle Technologies

The Netherlands has positioned itself at the forefront of Europe’s biodegradable water bottle market through groundbreaking plant-based technologies. Avantium is leading the charge with its PEF (polyethylene furanoate) bottles. As of June 2025, Avantium announced that its innovative PET/PEF multilayer bottle has been validated by RecyClass as fully compatible with the PET recycling stream, demonstrating PEF's potential as a recyclable barrier layer that also offers superior barrier properties for beverages. Carlsberg continues its trials of PEF-based beer bottles, having launched a large-scale pilot across eight Western European markets in 2022. While a full commercial launch of PEF-based beer bottles by Carlsberg in 2025 is an aim, widespread commercial availability is dependent on the scaling of Avantium's FDCA Flagship Plant, which began construction in 2022 with planned large-scale production of PEF in 2024. Corbion is also innovating with PLA-lined bio-bottles. In February 2025, Win Win Water announced the launch of its 100% plant-based, biodegradable bottles, crafted entirely from Luminy® PLA by TotalEnergies Corbion, designed to decompose within 90 days in commercial composting facilities. Regulatory drivers such as the EU Single-Use Plastics Directive mandate that by January 1, 2025, all newly produced plastic beverage bottles must contain a minimum of 25% recycled content and aim for a 77% separate collection rate for plastic bottles. The Netherlands’ combination of cutting-edge technology and sustainability-focused regulation makes it a significant player in shaping Europe’s biodegradable water bottle landscape.

Germany Advances High-Performance Biodegradable Bottle Materials

Germany is a key hub for high-performance materials in the biodegradable water bottle sector, driven by both technological expertise and progressive regulations. BASF is actively developing and promoting sustainable coating solutions for packaging. As of June 2025, BASF is showcasing its Ecovio® and Ecoflex® BMB biopolymers, including certified compostable and soil-biodegradable tailored coatings for paper food articles to provide necessary barrier properties for liquids, offering an eco-friendly alternative to conventional plastics. Siemens, leveraging its expertise in advanced manufacturing and AI, is developing AI-enhanced tools across its Digital Industries Software portfolio, which could potentially optimize processes for molding bioplastic bottles. Major brands are making strides towards sustainability: Volvic, part of Danone, commits to making its bottles from 100% recycled plastic by 2025 (excluding caps and labels), though its bottles are designed for recycling, not biodegradability. Germany’s Circular Economy Act, alongside EU directives, drives significant R&D and industrial-scale testing, with the EU aiming for bottle compostability and high recycling rates. With its strong innovation ecosystem and regulatory commitment, Germany is at the forefront of engineering sustainable solutions for the bottled water industry.

China Emerges as the Mass Production Hub for Biodegradable Bottles

China has rapidly scaled its capacity in biodegradable water bottle manufacturing, solidifying its status as a global production powerhouse. The country boasts significant production capacity for PLA and PBAT bottle materials. Leading producers such as Zhejiang Hisun Biomaterials continue to supply high-volume PLA resins for bottle manufacturing, with their PLA resins suitable for extrusion blow molding of bottles. Sinopec continues to advance its new material technologies within its strategic development plans, including the exploration of PBS bio-bottles. China's efforts in scaling sustainable alternatives are poised to have significant global implications, potentially reshaping supply chains and contributing to cost reductions for biodegradable bottle production worldwide.

Japan Focuses on Premium Functional Biodegradable Bottles

Japan’s approach to biodegradable water bottles emphasizes premium functionality and cutting-edge material science. Mitsubishi Chemical continues to develop and promote its BioPBS™ solutions, which offer high heat resistance and compatibility, making them suitable for various demanding packaging applications. Kaneka’s PHBH technology (Green Planet™) offers marine-degradable biopolymers. As of April 2025, Kaneka is showcasing Green Planet™ at Expo 2025 Osaka, demonstrating its biodegradability in soil and seawater, highlighting its potential for marine-degradable bottles. Major beverage companies are embracing these changes: Suntory has announced an ambitious target of using 100% sustainable PET bottles globally by 2030, with an interim goal of achieving a minimum of 50% recycled or plant-based materials across its entire drinks portfolio by 2025. This underlines Japan’s commitment to sustainable packaging transformation. With its high standards for quality and performance, Japan is setting benchmarks for integrating biodegradability into functional, consumer-friendly beverage packaging.

Biodegradable Water Bottles Market Report Scope

Biodegradable Water Bottles Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material Type (Plant-based Plastics, Paper & Paperboard, Algae-based Materials, Biodegradable Additive-Enhanced Plastics), By Biodegradation Type (Fully Biodegradable, Edible, Reusable Biodegradable), By Capacity (500 ml, 1,000 ml), By Application (Mineral Water, Spring Water, Flavored Water, Sports Drinks, Others, Personal Care Products), By End-User (Residential Use, Institutional Use, Specialty Purpose), By Distribution Channel (Retail, Online, Foodservice, Bulk Sales)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (U.S.), Danimer Scientific (U.S.), PLA Bottles EU (Netherlands), Paper Water Bottle Co. (U.S.), Cove (U.S.), JUST Goods, Inc. (U.S.), Lyspackaging (France), Choose Water (UK), Kendal Mint Co. (UK), BioBottles (India), Greenbio Products (India), Nestlé S.A. (Switzerland), Danone S.A. (France), PepsiCo, Inc. (U.S.), Bacardi Limited (Bermuda), Biotrem (Poland), Yuhme (Sweden), Bioline Technologies (India), Jk Chemo Enterprises (India), Skyline Overseas (India), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Water Bottles Market Segmentation

By Material Type

- Plant-based Plastics

- Paper & Paperboard

- Algae-based Materials

- Other Organic Materials

- Biodegradable Additive-Enhanced Plastics

By Biodegradation Type

- Fully Biodegradable

- Edible

- Reusable Biodegradable

By Capacity

By Application

- Mineral Water

- Spring Water

- Flavored Water

- Sports Drinks

- Personal Care Products

By End-User

- Residential Use

- Institutional Use

- Specialty Purpose

By Distribution Channel

- Retail

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- Online

- E-commerce Platforms

- Company Websites

- Foodservice

- Restaurants & Cafes

- Vending Machines

- Bulk Sales

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Water Bottles Market

- NatureWorks LLC (US)

- Danimer Scientific (US)

- PLA Bottles EU (Netherlands)

- Paper Water Bottle Co. (US)

- Cove (US)

- JUST Goods, Inc. (US)

- Lyspackaging (France)

- Choose Water (UK)

- Kendal Mint Co. (UK)

- BioBottles (India)

- Greenbio Products (India)

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- PepsiCo, Inc. (US)

- Bacardi Limited (Bermuda)

- Biotrem (Poland)

- Yuhme (Sweden)

- Bioline Technologies (India)

- Jk Chemo Enterprises (India)

- Skyline Overseas (India)

* List Not Exhaustive

Methodology:

The research methodology for the Global Biodegradable Water Bottles Market integrates rigorous primary and secondary research. Primary research encompasses structured interviews and consultations with industry leaders, sustainability experts, polymer scientists, regulatory officials, and executives from leading packaging and beverage brands. These insights are validated and augmented through comprehensive secondary research drawn from corporate filings, regulatory frameworks (e.g., EU Packaging and Packaging Waste Regulation, California SB 54), patent databases, scientific publications, and reputable industry journals. Market size estimations and forecasts for 2025–2034 are established through a robust data triangulation process, ensuring consistency across market segments, regions, and end-use sectors. This approach guarantees high accuracy in capturing market dynamics, technology trends, competitive landscapes, and evolving regulatory impacts.

Research Coverage:

- Geographic Scope: Spanning over 25 countries across North America, Europe, Asia Pacific, South America, the Middle East, and Africa.

- Segmentation: In-depth analysis across multiple dimensions:

- Material Type: Plant-Based Plastics, Paper & Paperboard, Algae-Based Materials, Biodegradable Additive-Enhanced Plastics.

- Biodegradation Type: Fully Biodegradable, Edible, Reusable, and Biodegradable.

- Capacity: 500 ml, 1,000 ml.

- Application: Mineral Water, Spring Water, Flavored Water, Sports Drinks, Others, Personal Care Products.

- End-User: Residential Use, Institutional Use, Specialty Purpose.

- Distribution Channel: Retail, Online, Foodservice, Bulk Sales.

- Competitive Landscape: Comprehensive profiling and strategic insights on over 20 key market participants, ranging from multinational corporations to emerging innovators.

- Core Themes Covered:

- Technological breakthroughs in biodegradable polymers and bio-based materials.

- Regulatory shifts are reshaping packaging sustainability mandates globally.

- Innovative bottle designs, including marine-degradable and edible solutions.

- Regional manufacturing trends and supply chain dynamics.

- Sustainability economics and the shift towards circular economy models.

- Historical data from 2021 to 2024 and forecasts from 2025 to 2034.

Deliverables:

- Complete Market Research Report (PDF and Excel), including data tables, charts, and interactive visualizations.

- Country-specific forecasts and strategic insights.

- Detailed segment-wise revenue projections for the 2025–2034 forecast period.

- Competitive intelligence, SWOT analysis, and benchmarking of major players.

- Analysis of recent innovations and technology tracking.

- Executive summary featuring key trends and analyst commentary.

- Post-purchase analyst support for client-specific data requests and clarifications.