Market Overview: Bismaleimide Monomer Market Growth Anchored in Aerospace Lightweighting, Hydrogen Pressure Vessels, and High-Temperature Adhesive Systems (2025–2034)

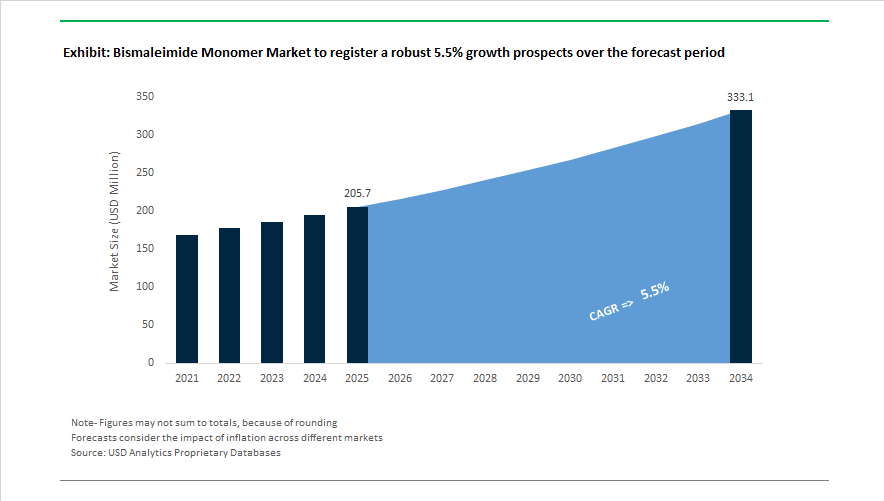

The bismaleimide monomer market is projected to grow from USD 205.7 Million in 2025 to USD 333 Million by 2034, reflecting a CAGR of 5.5% driven by demand for high-temperature composite resins, aerospace structural adhesives, advanced electronics materials, and hydrogen storage systems. Market evolution accelerated in April 2024 when Syensqo introduced a bio-based BMI resin family under the CYCOM brand, enabling aerospace OEMs to access sustainable alternatives while maintaining high glass transition temperatures required for engine nacelles and high-speed airframes. In late 2024, Evonik integrated new BMI monomer chemistry into its aerospace adhesives portfolio, enhancing moisture resistance and high-temperature bond durability for aircraft wings and fuselage structures. These innovations demonstrate how BMI resins are evolving beyond legacy thermoset roles into multifunctional structural materials.

Composite adoption expanded into emerging mobility and energy storage segments through 2025. In May 2025, Syensqo reported successful demonstration of BMI composites replacing titanium in select aerospace components, delivering 30 to 40% weight reduction while maintaining thermal stability. In June 2025, Syensqo partnered with MissionH24 to integrate BMI-based composites into hydrogen-powered endurance racing vehicles, highlighting BMI suitability for extreme thermal cycling environments. At CAMX in October 2025, Hexcel Corporation and HyPerComp Engineering showcased BMI-enriched composite pressure vessels designed for hydrogen storage, targeting aerospace and heavy-duty transport decarbonization. Supply chain localization became a defining factor in 2025 when expanded U.S. tariffs on specialty chemical imports encouraged regional BMI monomer sourcing to stabilize costs and logistics.

Market confidence strengthened entering 2026 as aerospace demand and technical performance improved. In January 2026, Hexcel highlighted BMI-based composite solutions at WINGS India to support regional aircraft manufacturing growth, and reaffirmed strong 2026 sales guidance tied to next-generation aircraft ramp-ups. During the same month, an ACS Applied Polymer Materials study introduced a phosphorus-siloxane toughening agent that improves BMI resin impact resistance and flame retardancy without reducing thermal performance, addressing a longstanding brittleness limitation. Structural portfolio realignment is also underway. In November 2025, Evonik reorganized its Advanced Technologies division to prioritize custom BMI formulations for 5G infrastructure materials, while in January 2026 Syensqo divested its Oil and Gas unit to focus capital on advanced materials and specialty polymers. Mitsubishi Chemical’s Kyushu expansion, scheduled for April 2026, further supports the advanced materials ecosystem by enhancing production infrastructure for high-purity specialty resin precursors used in electronics and composite systems.

Trends and Opportunities Reshaping the Bismaleimide Monomer Market

Market Trend: Shift Toward Allyl-Modified BMI Grades to Overcome Brittleness and Improve Processability

A major structural transition is underway as market leaders focus on optimized monomer chemistry. Standard MDA-based BMI, traditionally used for high-temperature aerospace composites, is being replaced by specialized allyl-modified derivatives that retain extreme heat resistance but add toughness and manufacturability.

In 2024–2025, approximately 46% of all industry R&D activity within the BMI landscape centered on “Hybrid Thermoset Matrices.” These hybrid systems combine diallyl-modified BMI with co-curing partners to create hot-melt, solvent-less formulations. This directly addresses the aerospace industry’s long-standing pain point of brittleness at elevated temperatures, while maintaining glass transition temperatures above 300°C. Recent NASA NTRS studies show BMI-2/IM7 systems now support Out-of-Autoclave (OoA) molten infusion at ~110°C—unlocking cost and energy reductions by eliminating the need for high-pressure cure cycles. The immediate commercial implication is a more scalable BMI processing ecosystem that lowers part-per-aircraft production cost, improving competitiveness against epoxy-based composites.

Market Trend: Aerospace-Driven Vertical Integration to Secure Monomer Supply and Quality Assurance

BMI monomer supply security is emerging as a strategic differentiator. Aerospace prime contractors and Tier-1 composite suppliers are consolidating upstream raw materials, stabilizing performance consistency for BMI-based prepregs used in airframe and propulsion-adjacent structures.

As of 2025, the top 10 global chemical producers control roughly 90.25% of the BMI resin market capacity. Companies such as Evonik (21.22% share) and Solvay are expanding internal monomer portfolios to reduce procurement reliance on third-party co-monomers like Diamino Diphenyl Sulfone (DDS). Simultaneously, Hexcel and Solvay have elevated BMI-based structural composites to over 48% of all BMI resin applications, supporting use across more than 3,000 active aerospace platforms. This vertical integration model ensures tight mechanical-electrical-thermal property compliance in demanding applications such as primary fuselage skins and engine-adjacent fairings, where BMI delivers up to 35% weight savings versus metallic alternatives.

Market Opportunity: BMI as the Enabling Matrix for Hypersonic Structures and Defense Radomes

Defense programs are becoming a major catalyst for BMI monomer demand, particularly where dielectric stability and heat tolerance must be preserved under extreme stress. BMI resin systems provide consistent dielectric performance across steep thermal gradients, making them ideal for radomes and hypersonic glide vehicle exteriors.

The U.S. DoD’s $45-million Hypersonic Infrared Target Sensing (HITS) project, initiated in October 2024, directly targets new material classes for >500°C operating environments. BMI composites used in prototype airframes are reported to reduce structural mass by roughly 21% , enabling extended range, better fuel efficiency, and higher maneuverability. As hypersonic missile development accelerates globally, procurement budgets are increasingly earmarked for BMI-carbon fiber composite adoption—presenting a multi-year pipeline of demand for specialty BMI monomers and curing agents.

Market Opportunity: BMI-Triazine (BT) Copolymers as the Backbone of 5G and AI Server PCB Growth

Global AI datacenter expansion is generating unprecedented demand for high-layer-count circuit boards, making BMI-Triazine (BT) chemistry one of the most commercially significant polymer systems for signal-critical electronics.

Industry data from December 2025 confirms AI-optimized servers require 50–60× more PCB material than legacy server designs. This increase has created monomer supply bottlenecks, extending laminate lead times from 8–12 weeks to more than 30 weeks. BT resins are prized for ultra-low dielectric loss (Df < 0.002) and their ability to withstand 260°C lead-free solder cycles without delamination. New Glass-Core PCB architectures launched in late 2025 now incorporate BMI-based redistribution layers to elevate signal transmission efficiency by 15–20% for 224G SerDes networking—evidence that BMI monomers are extending beyond aerospace into semiconductor infrastructure and AI hardware supply chains.

Bismaleimide (BMI) Monomer Market Share and Segmentation Insights

Market Share by Product Type: BDM Dominance Sustained as Liquid BMI Unlocks Advanced Processing

Bismaleimidodiphenylmethane (BDM) accounts for 52% of global BMI monomer consumption in 2025, reinforcing its position as the industry standard for high-performance thermoset resin systems. Its combination of high glass transition temperatures above 230°C, strong mechanical integrity, and excellent fatigue resistance makes BDM the preferred choice for aerospace composites and structural adhesives. Bisphenol ether bismaleimide holds the second-largest share, benefiting from improved toughness and processability through ether linkages, enabling impact-resistant applications without compromising thermal stability. Phenylmethane bismaleimide serves specialized electronic laminates and encapsulation materials where low dielectric loss and high purity are critical. Liquid bismaleimide monomers represent the fastest-growing segment, enabling resin transfer molding and out-of-autoclave processing that significantly reduce manufacturing costs for complex geometries. Phenylene bismaleimide remains a niche option, valued for oxidative stability and radiation resistance in defense and nuclear environments.

Monomer Market Share By Product Type, 2025.png)

Market Share by End User Industry: Aerospace Leadership Expands into Electronics and EV Power Systems

Aerospace leads BMI monomer demand with a 39% share in 2025, driven by widespread use in aircraft structures such as engine nacelles, wing leading edges, radomes, and thrust reversers, where conventional epoxy systems fail under sustained temperatures of 150°C to 230°C. Electrical and electronics is the second-largest and fastest-growing sector, supported by rising deployment of BMI resins in high-layer-count PCBs, IC substrates, and semiconductor encapsulation for 5G infrastructure, data centers, and ADAS platforms. Automotive represents an emerging growth channel, with BMI increasingly adopted in EV power modules, inverters, and structural battery housings as manufacturers shift toward 800V architectures and silicon carbide devices. Defense remains a stable, high-margin segment for missile systems and naval composites, while energy applications in wind, oil and gas, and nuclear sensors contribute niche but attractive revenue streams.

Competitive Landscape Analysis of the Bismaleimide Monomer Market

The bismaleimide monomer market in 2026 is defined by aerospace-grade qualification barriers, rising demand from EV electrification and advanced electronics, and a structural shift from commodity BMI supply toward formulated, application-specific systems. Competition increasingly centers on resin system integration, processing flexibility for RTM and filament winding, and toughness-modified chemistries that overcome traditional BMI brittleness. Market leaders differentiate through vertical integration into prepregs and carbon fiber, digital formulation tools, low-carbon production pathways, and regional supply chain expansion. High-growth end uses include aircraft engine structures, printed wiring boards, high-voltage EV components, and next-generation mobility platforms.

Evonik Industries sets the global benchmark for aerospace-grade BMI systems

Evonik remains the technological reference point for BMI chemistry through its Compimide portfolio, widely regarded as the gold standard for high-temperature thermosets. In 2026, Compimide 353 leads its offering, supplied as a resolidified eutectic melt optimized for resin transfer molding and filament winding. Late 2025 saw the launch of Compimide 1206R55, a BMI/epoxy hybrid enabling higher glass transition temperatures while retaining epoxy-like processability for printed wiring boards. Evonik’s strategic pivot toward systemized solutions now bundles BMI monomers with toughening modifiers to reduce composite brittleness. Backed by over three decades of certified aerospace heritage, Evonik’s materials are embedded across major global aircraft programs.

Hexcel vertically integrates BMI monomers into carbon fiber prepreg dominance

Hexcel operates as a fully integrated BMI powerhouse, producing monomers primarily to supply its HexPly resin systems and HexTow carbon fibers. These BMI prepregs are critical for high-load aerospace components including F-35 structures and Boeing 787 engine nacelles. During 2025 and 2026, Hexcel qualified new high-toughness BMI variants for the Boeing 737 MAX, achieving substantial engine noise reduction without weight penalties. At WINGS India 2026, Hexcel highlighted its Advanced Air Mobility initiative, positioning BMI composites for battery enclosures and motor housings in urban air taxis. The company dominates aerospace defense applications where flame, smoke, and toxicity compliance is mission-critical.

Huntsman accelerates BMI adoption through digital formulation and mobility platforms

Huntsman advances BMI monomers via its Advanced Materials segment, bridging industrial usability with extreme thermal performance. In early 2026, the company redirected R&D toward its Araldite Next-Gen platform, optimizing BMI systems for faster cure cycles in EV battery packs and high-speed rail. A digital formulation modeling tool introduced in late 2025 now enables customers to simulate BMI curing kinetics in real time, dramatically shortening composite development timelines. Huntsman also expanded distribution partnerships across Asia-Pacific and the Middle East to support regional electronics and 5G infrastructure growth. Its core strength lies in customer co-development, embedding technical teams with OEMs to accelerate BMI qualification.

Solvay advances low-carbon BMI monomers for sustainable aerospace programs

Following restructuring in 2024 and 2025, Solvay has intensified its focus on essential chemicals and high-performance BMI intermediates. Under the CYCOM brand, Solvay supplies BMI resin systems while promoting bio-based monomers derived from agricultural side-streams for green aerospace contracts. In late 2025, the company expanded BMI monomer capacity to stabilize global supply of 4,4′-bismaleimidodiphenylmethane, the industry’s dominant grade. Solvay’s 2026 strategy emphasizes decarbonization, phasing out coal-based energy at European sites to offer low-carbon BMI. Internal precursor integration with soda ash and peroxides protects margins from feedstock volatility.

Daiwakasei Industry supplies ultra-pure BMI monomers for high-voltage electronics

Daiwakasei Industry specializes in high-purity BMI variants for electronics and insulation markets, including BMI-6000 and BMI-8000 grades engineered for low moisture absorption. In 2026, the company is scaling its proprietary dioxanone-BMI hybrid technology, enhancing flexibility for molded components and flexible printed circuit boards. Daiwakasei is a key supplier for high-voltage cable insulation and heat-resistant varnishes used in automotive motors, supporting the transition to 800V and 1000V EV architectures. Unlike large Western producers, Daiwakasei excels in creative small-batch production, delivering custom-spec BMI monomers for niche research and precision electronics applications.

Sichuan EM Technology drives cost-competitive BMI scale for aerospace and industrial growth

Sichuan EM Technology represents the new wave of Asian BMI producers, rapidly moving from commodity chemistry into high-purity monomer specialization. EMT plays a strategic role in China’s aerospace autonomy, supplying BMI monomers for the C919 aircraft program and domestic military aviation. During 2025 and 2026, the company expanded high-purity lines to include 4-methyl-1,3-phenylene bismaleimide for export markets constrained by Western aerospace demand. EMT is also a major supplier of m-phenylene bismaleimide for rubber chemicals and high-temperature adhesives. Its defining advantage is cost-competitive scale, enabling broader BMI adoption across automotive and general industrial sectors.

United States Bismaleimide Monomer Market: Defense Procurement, AI Infrastructure, and Advanced Manufacturing

The United States bismaleimide monomer industry is being reshaped by defense procurement priorities, high-density computing requirements, and federal supply chain policy. In late 2025, the U.S. Department of Defense finalized updated procurement guidance under the National Defense Industrial Strategy that explicitly incentivizes domestic production of high-temperature resins. This has accelerated the adoption of BMI-based composites for stealth-capable uncrewed aerial systems and other mission-critical aerospace platforms. Parallel demand is emerging from the digital economy. To manage the extreme thermal loads associated with next-generation GPU clusters scheduled for 2026 deployment, U.S. laminate manufacturers are increasingly specifying BMI-modified epoxy systems for AI servers, where low thermal expansion and sustained heat resistance are essential.

Capacity and skills are scaling to meet this pull. Hexcel Corporation announced a mid-2025 capacity optimization program across its U.S. facilities to streamline BMI prepreg production, targeting higher throughput for programs such as the F-35 Lightning II and commercial space launch vehicles. Workforce depth remains a strategic asset, with the U.S. aerospace sector employing roughly 2.1 million professionals as of January 2026 and federal grants supporting specialized training in advanced composite layup using BMI resins. Upstream resilience is also being addressed. Under the CHIPS and Science Act frameworks, strategic material mapping for 2026 is focused on securing maleic anhydride and aromatic diamines, the critical chemical precursors for BMI monomers. Innovation is extending into manufacturing methods as well. In November 2025, a collaboration between a major U.S. aerospace OEM and a national materials laboratory demonstrated additive manufacturing of a complex BMI engine component, materially reducing tooling costs and shortening development cycles.

Japan Bismaleimide Monomer Market: Semiconductor Materials, Thermal Innovation, and Space Applications

Japan’s bismaleimide monomer market is anchored in electronics leadership, materials science innovation, and close alignment with space and automotive OEMs. In December 2025, Mitsubishi Chemical Group and Mitsui Chemicals reported the development of high-purity BMI monomers tailored for integrated circuit substrates, optimized for the low dielectric loss requirements of 6G telecommunications testing. This positions BMI as a critical enabler for next-generation signal integrity in advanced semiconductor packaging.

Thermal management innovation is a second pillar. In Q4 2025, Japanese material scientists unveiled a BMI-based phase change material that improves thermal energy storage capacity by up to 35% compared with traditional inorganic salts, addressing heat stabilization challenges in high-temperature industrial processes. Space-sector demand is reinforcing this trajectory. Teijin Limited and Teijin Carbon Europe launched the BIMAX TPUD braided fabric in November 2025, a BMI-based solution designed for scalable production of satellite components and rocket nozzles. Sustainability considerations are being embedded at the production level as well. Evonik Industries transitioned its Japanese specialty resin operations to 100% green electricity as of July 1, 2025, aligning BMI output with local ESG mandates. With Japan’s PCB output reaching approximately USD 6.1 billion by early 2026, domestic manufacturers are concentrating on high-end BMI laminates for medical and military electronics, supported by renewed investor funding for BMI-integrated thermal management solutions in AI server applications.

China Bismaleimide Monomer Market: Industrial Policy Execution and Electronics Scale

China’s bismaleimide monomer industry is advancing through state-led policy execution, electronics scale, and environmental upgrades. Under the final phase of Made in China 2025, the Ministry of Industry and Information Technology has prioritized self-sufficiency in strategic high-polymer materials. This policy support enabled the commissioning of a 2,000-ton BMI plant by Yinghui Energy in 2025, strengthening domestic availability for aerospace and electronics applications.

Trade and export controls are indirectly reinforcing BMI demand. In April 2025, the Ministry of Commerce of the People's Republic of China implemented licensing requirements for medium and heavy rare earths. This has increased the emphasis on lightweight, high-temperature polymer composites, positioning BMI systems as a substitute lever in aerospace structures. Electronics remains the dominant downstream. With China accounting for more than half of global PCB production in 2025, laminate producers are shifting toward low-Dk and low-Df BMI monomers to compete in high-speed server and data center markets. Environmental compliance is being upgraded in parallel, as chemical clusters in Shandong and Jiangsu modernized maleimide synthesis lines throughout 2025 to meet stricter discharge standards while preserving cost competitiveness. On the aerospace side, consolidation among more than 200 small-to-medium part manufacturers has driven standardization around BMI resin systems for 2026 satellite launch vehicles.

Germany Bismaleimide Monomer Market: Specialty Polymer Focus and Circular Compliance

Germany’s bismaleimide monomer landscape is defined by specialty polymer prioritization, sustainability targets, and EU compliance leadership. Evonik Industries, headquartered in Essen, revised its 2025–2026 strategy to emphasize high-margin specialty polymers such as BMI, offsetting weak demand in commodity chemicals and reinforcing its role in advanced aerospace and electronics supply chains. This strategic realignment reflects broader European demand for materials that combine thermal resilience with regulatory transparency.

Production sustainability is becoming a differentiator. Evonik’s Marl facility began operating coating and adhesive resin lines on green electricity in July 2025, targeting a 25% reduction in Scope 1 and 2 emissions by 2030. German BMI producers are also leading implementation of ISCC PLUS certified mass-balance monomers, enabling downstream aerospace customers to claim bio-circular material credits under EU Green Deal frameworks. This positions Germany as a preferred sourcing base for OEMs balancing performance requirements with audited sustainability claims.

Country-Level Strategic Snapshot: Bismaleimide Monomer Industry

Bismaleimide Monomer Market County Level Snapshot

|

Country / Region

|

Strategic Orientation

|

Key Developments

|

|

United States

|

Defense and AI-driven demand

|

DoD procurement incentives, AI server thermal needs, Hexcel capacity optimization, additive manufacturing

|

|

Japan

|

Semiconductor and thermal innovation

|

High-purity BMI for 6G, BMI-based PCM, space-grade fabrics, green electricity transition

|

|

China

|

Policy-led self-sufficiency

|

New BMI plant commissioning, PCB laminate upgrades, environmental compliance in clusters

|

|

Germany

|

Specialty polymers and circularity

|

Evonik portfolio realignment, green electricity at Marl, ISCC PLUS mass-balance adoption

|

Bismaleimide Monomer Market Report Scope

Bismaleimide Monomer Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$205.7 Million

|

|

Market Size (2034)

|

$333 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Bismaleimidodiphenylmethane, Phenylene Bismaleimide, Bisphenol Ether Bismaleimide, Phenylmethane Bismaleimide, Liquid Bismaleimide Monomers), By Physical Form (Crystalline Powder, Liquid, Granular), By Application (Composites, Electronics, Adhesives and Sealants, Molding Compounds, Thermal Management), By End User Industry (Aerospace, Defense, Electrical and Electronics, Automotive, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries, Hexcel Corporation, Solvay, Huntsman International, Teijin, Mitsubishi Chemical Group, Mitsui Chemicals, HOS Technik, Daiwakasei Industry, K I Chemical Industry, ABR Organics, Honghu Shuangma Advanced Materials, Puyang Willing Chemicals, Sichuan EM Technology, Atul

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bismaleimide Monomer Market Segmentation

By Product Type

- Bismaleimidodiphenylmethane

- Phenylene Bismaleimide

- Bisphenol Ether Bismaleimide

- Phenylmethane Bismaleimide

- Liquid Bismaleimide Monomers

By Physical Form

- Crystalline Powder

- Liquid

- Granular

By Application

- Composites

- Electronics

- Adhesives and Sealants

- Molding Compounds

- Thermal Management

By End User Industry

- Aerospace

- Defense

- Electrical and Electronics

- Automotive

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bismaleimide Monomer Industry

- Evonik Industries

- Hexcel Corporation

- Solvay

- Huntsman International

- Teijin

- Mitsubishi Chemical Group

- Mitsui Chemicals

- HOS Technik

- Daiwakasei Industry

- K I Chemical Industry

- ABR Organics

- Honghu Shuangma Advanced Materials

- Puyang Willing Chemicals

- Sichuan EM Technology

- Atul

*- List not Exhaustive