Market Overview: Bromobenzene Market Growth Driven by Pharma Intermediates, Continuous-Flow Grignard Chemistry, and Supply Chain Realignment (2025–2034)

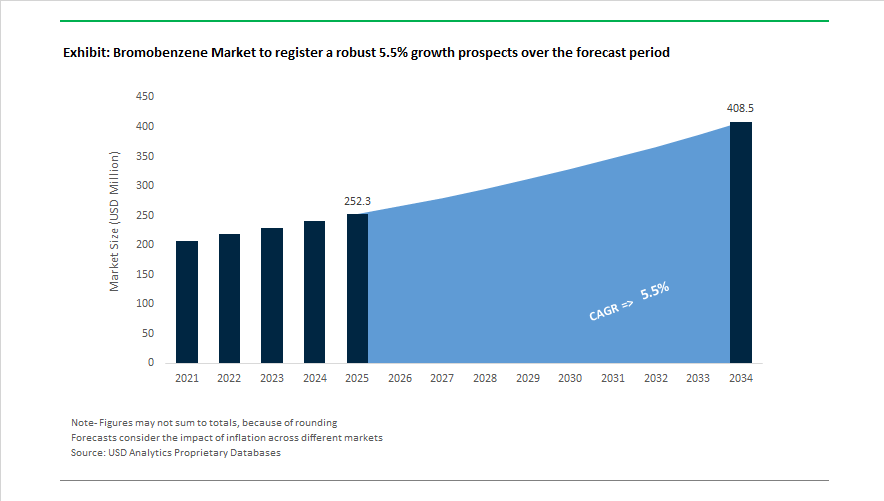

The bromobenzene market is projected to expand from USD 252.3 Million in 2025 to USD 408.5 Million by 2034, reflecting a CAGR of 5.5% supported by rising demand for brominated intermediates in pharmaceuticals, agrochemicals, OLED materials, and specialty organometallic synthesis. Capacity and technology shifts began in 2024 when LANXESS expanded European bromobenzene production focused on high-purity grades used in Suzuki and Heck coupling reactions. The same year, Cambridge Isotope Laboratories expanded output of deuterated benzene to support bromobenzene-d5 demand in OLED displays and advanced pharmaceutical labeling. In April 2025, new U.S. tariffs on Chinese chemical imports redirected bromobenzene supply chains toward Indian producers and domestic brine-based bromine operations, reinforcing regional supply security.

Industrial consolidation and upstream integration accelerated through 2025. In August 2025, Chemcon Speciality Chemicals Limited reported an 18% year-on-year increase in its organic chemicals segment driven by pharmaceutical intermediate demand. This momentum culminated in October 2025 when Chemcon finalized the acquisition of Shivam Petrochem Industries to expand bromobenzene capacity. Aarti Industries initiated a major capital expenditure program in 2025 to secure bromine feedstock through backward integration, stabilizing supply for bromobenzene and Grignard reagent production. Aether Industries strengthened export positioning in September 2025 through multi-year pharmaceutical contracts utilizing bromobenzene as a key building block. Navin Fluorine advanced debottlenecking of its Dahej multipurpose plant in 2025 to support long-term specialty intermediate contracts.

Process innovation and regulatory pressure define the 2026 outlook. The late 2025 EU REACH update increased compliance requirements for brominated aromatics, encouraging adoption of closed-loop bromine recovery. Producers across Asia and Europe began transitioning to continuous-flow Grignard production during 2025 and 2026, improving yields and safety while reducing waste. Early 2026 pilot programs in electrochemical bromination demonstrated high Faradaic efficiency, indicating a shift toward greener synthesis pathways. Deloitte’s December 2025 sector outlook highlighted pharmaceuticals and semiconductor materials as priority segments, guiding producers to shift away from commoditized grades.

Upstream Bromine Dynamics and Semiconductor–Pharma Alignment Driving Trends and Opportunities in the Bromobenzene Market

Bromine Supply Reallocation and Network Optimization Influence Bromobenzene Availability

Bromobenzene supply is closely tied to upstream elemental bromine production, making capacity decisions and production efficiencies a strategic factor across downstream derivatives. In August 2025, LANXESS announced operational optimization at its El Dorado production site in the United States, aimed at consolidating bromine output and stabilizing supply to high-value brominated intermediates, including bromobenzene. These network adjustments are emerging as a response to uneven global demand across flame retardants and specialty additives, prompting a shift in feedstock prioritization toward pharmaceutical and semiconductor intermediates. Meanwhile, regional shipment volatility and ocean freight route changes, such as rerouted vessels avoiding the Red Sea in May 2025, have added logistics-driven price pressure for bromine-based intermediates globally. U.S. market sentiment remained optimistic due to domestic upstream capacity, but reduced import flows continue to influence supply planning for buyers dependent on high-purity bromobenzene.

Pharmaceutical-Grade Bromobenzene Drives Market Direction Due to Purity-Critical API Synthesis

Growth in high-value pharmaceutical synthesis is positioning bromobenzene as a priority precursor for API manufacturers. Late 2025 data highlights that pharmaceutical-grade bromobenzene is the most rapidly expanding segment, driven by its indispensable role in producing the Grignard reagent phenylmagnesium bromide. This reagent is a foundational intermediate for manufacturing oncology, cardiovascular, and central nervous system drug molecules. Technical disclosures released by fine chemical suppliers in May 2025 underscore the regulatory focus on purity assurance, particularly for intermediates like Bromo-OTBN, where trace-level contaminants can create reaction failure, yield variability, or regulatory non-conformity. Batch authentication and impurity profiling are now procurement requirements in regulated markets where quality deviations can impact EMA and FDA submissions.

High-Refractive-Index Monomers Enable AR/VR Thin-Film Optics and Wearable Electronic Components

Bromobenzene is emerging as a strategic raw material for brominated monomers that contribute to High Refractive Index Polymers (HRIPs). These polymers are accelerating the development of lightweight optical layers essential for augmented and virtual reality headsets. Material research spanning 2024 to 2025 demonstrated brominated polymer films achieving refractive indices in the 1.7 to 2.07 range, supporting thin-film lens miniaturization and improved light control. Compared to inorganic coatings such as aluminum oxide or tantalum oxide, brominated thin films have delivered superior mechanical performance, maintaining optical clarity at tensile strains approaching 10%. This compatibility with flexible substrates aligns bromobenzene with the fast-growing sector of soft display components and wearable electronics.

Bromobenzene Derivatives Expand OLED Semiconductor and Advanced Coupling Applications

Bromobenzene is also essential to OLED material development, particularly through derivatives like 2-Bromoiodobenzene, which semiconductor manufacturers highlighted in October 2025 as a precision intermediate due to its ability to undergo sequential and selective coupling reactions. This dual-reactivity characteristic enables controlled formation of heterocyclic hole-transport layers and host matrices that enhance device luminance and stabilize power efficiency. As display manufacturers push limits on lifespan and brightness, suppliers are increasing purity targets toward 97 to above 99% for molecules derived from bromobenzene. High-purity requirements are linked directly to electronic transport performance, as semiconductor defects generated by micro-contaminants lead to charge-trap formation and shortened OLED operating life. Bromobenzene-enabled molecules are therefore gaining prominence in procurement pipelines for premium smartphone screens, television displays, and next-generation flexible OLED formats.

Bromobenzene Market Share and Segmentation Insights

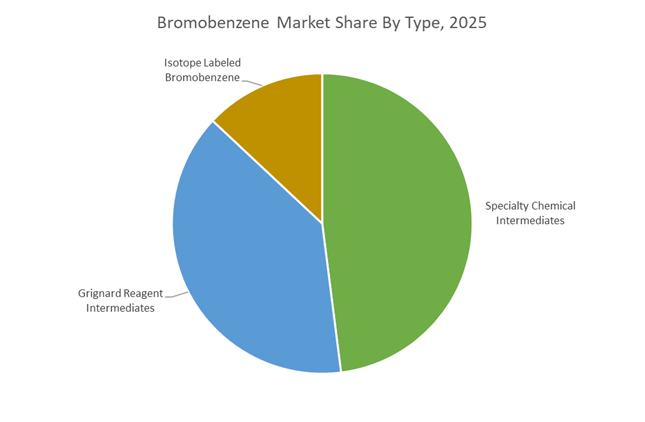

Market Share by Type: Specialty Intermediates Lead While Isotope Grades Capture High-Value Research Spend

Specialty chemical intermediates account for 48% of bromobenzene consumption in 2025, reflecting its role as a core aromatic building block in fine chemicals, pharmaceutical intermediates, and performance materials. Bromobenzene supports synthesis routes for phenyl magnesium bromide, diphenyl ethers, substituted aromatics, and polyphenyl compounds, with demand driven by contract manufacturing organizations serving diversified end markets. Grignard reagent intermediates form the second-largest segment, leveraging bromobenzene as a classic precursor for phenyl magnesium bromide used in carbon–carbon bond formation across specialty alcohols and API intermediates, closely aligned with medicinal chemistry activity. Isotope-labeled bromobenzene remains the smallest by volume but highest in value, supplying bromobenzene-¹³C and deuterated variants for NMR spectroscopy, bioanalytical standards, DMPK studies, and environmental fate research, supported by rising pharmaceutical R&D intensity and regulatory complexity.

Market Share by End Use Industry: Pharmaceuticals Dominate as Electronics Add Specialty Growth

Pharmaceuticals and biotechnology command 61% of bromobenzene demand in 2025, anchored by its use in synthesizing APIs including antihistamines, antipsychotics, antispasmodics, and anti-inflammatory drugs, as well as photostabilizers and UV absorbers for drug packaging. Generic manufacturing hubs in India and China remain primary demand centers, where high-purity grades with tight impurity control command pricing premiums. Agrochemicals represent the second-largest segment, utilizing bromobenzene derivatives in herbicides, fungicides, and insecticides, with volumes tied to crop cycles and patent expiries. Electrical and electronics applications are expanding in organic semiconductors, liquid crystal intermediates, and photoresist components for advanced lithography, supported by device miniaturization and 5G rollout. Automotive and aerospace remain niche users in specialty polymers and lubricant additives, constrained by substitution toward non-brominated chemistries in regulated markets.

Competitive Landscape of the Bromobenzene Market

The global bromobenzene market in 2026 is shaped by tightening pharmaceutical regulations, expanding agrochemical pipelines, and rising demand for high-purity brominated intermediates used in APIs, Grignard reagents, electronics materials, and specialty synthesis. Competition is increasingly defined by vertical bromine integration, certified sustainable grades, AI-enabled custom chemistry, and geopolitically secure supply chains. Leading producers are investing in capacity expansions, continuous-flow bromination, and biomass-powered facilities while positioning bromobenzene as a critical building block for oncology drugs, mental health therapeutics, green agrochemicals, and advanced electronic components.

Dead Sea vertical integration and certified sustainable bromobenzene from ICL Group

ICL enters 2026 as the world’s largest producer of bromine-based intermediates, leveraging exclusive access to Dead Sea brines to control the global bromobenzene cost curve. With annual bromine capacity near 280,000 tons, ICL supplies high-purity bromobenzene and derivatives, increasingly offering certified sustainability grades for pharmaceutical API manufacturing. Its SAFR® methodology is being adapted for chemical synthesis customers to evaluate environmentally stable brominated intermediates. Strategically, ICL is expanding bromobenzene-derived platforms for AgTech and FoodTech, moving innovations from pilot scale to commercial deployment in 2026, reinforcing its position as a vertically integrated supplier for resilient global specialty chemical value chains.

Secure North American bromobenzene supply for pharma growth from Albemarle Corporation

Albemarle dominates the North American bromobenzene market through its Arkansas brine assets, providing a geopolitically secure supply base for specialty chemicals. Following the 2025/early-2026 reorganization of its Albemarle Specialties unit, the company now focuses exclusively on high-margin bromine and lithium solutions. Albemarle is a key US supplier for Grignard reagent manufacturing, supporting carbon-carbon bond formation in oncology and mental health drug pipelines. Its 2026 strategy emphasizes “Connectivity and Health,” targeting electronics and pharmaceuticals while offering domestic CDMOs a reliable alternative to overseas precursors, reinforcing Albemarle’s role as a preferred Western-source bromobenzene partner.

AI-driven custom brominated intermediates from LANXESS AG

LANXESS leads Europe’s advanced bromobenzene intermediates market, serving tightly regulated pharmaceutical and agrochemical customers. After expanding European bromobenzene capacity in 2024/2025, its facilities reached full utilization in early 2026, driven by demand for green agrochemicals. Following its exit from Urethane Systems, LANXESS sharpened its focus on premium specialty niches, integrating AI into material development to cut custom synthesis R&D cycles by up to 40% . Through its Saltigo unit, bromobenzene supports bespoke projects for global Big Pharma innovators, positioning LANXESS as a high-purity, innovation-led supplier for EU-compliant brominated aromatics.

High-purity Asian bromobenzene anchored by Nanyo Complex at Tosoh Corporation

Tosoh anchors Asian bromobenzene supply via its Nanyo Complex, with its ¥10 billion bromine expansion now fully operational in 2026 to ease regional supply tightness. The company delivers high-purity brominated intermediates for electronics and life sciences while executing its FY2026 to FY2028 roadmap to expand value-added chlorine and bromine derivatives. Tosoh is investing in biomass-powered operations to lower carbon intensity and align with environmental protection goals. Its bromobenzene products are embedded in certified medical and electronic components, creating strong customer stickiness and stable revenue streams across Japan, South Korea, and China.

Large-scale industrial bromobenzene exports from Shandong Haiwang Chemical

Shandong Haiwang is China’s largest bromine producer, operating five major plants near Laizhou Bay with access to high-density underground brine. In 2026, it supplies technical-grade bromobenzene for heavy liquid solvents and motor oil additives while expanding its global footprint through Belt and Road bases in Laos and Djibouti. A new Dubai Jafza operations hub accelerates exports to Europe and the Middle East. With six product series and strong resource abundance, Haiwang delivers cost-competitive brominated intermediates at scale, supporting industrial customers across the world’s fastest-growing bromobenzene consumption markets.

Integrated benzene chemistry and CDMO bromination from Aarti Industries Limited

Aarti Industries leverages deep integration in benzene-based chemistry to become a leading global bromobenzene producer. Its co-product model reuses byproducts across chemical chains, enabling highly competitive pricing in 2026. Aarti is a dominant supplier to India’s pharmaceutical sector, where bromobenzene intermediates feed anti-inflammatory and anti-hypertensive drug manufacturing. The company is aggressively expanding its CDMO platform for Western clients, supported by continuous-flow nitration and bromination introduced in 2025. By 2026, these technologies deliver higher yields and safer processing, positioning Aarti as a cost-efficient, high-quality partner for complex aromatic synthesis.

China Bromobenzene Market: Feedstock Hedging and Cluster-Led Specialization

China’s bromobenzene industry is undergoing a structural upgrade driven by financial risk management, specialty chemical clustering, and tighter environmental oversight. A pivotal development occurred in June 2025 when the China Securities Regulatory Commission approved benzene futures and options trading on the Dalian Commodity Exchange. This step is strategically significant for bromobenzene producers, as it enables hedging against sharp feedstock volatility that reached 31% during 2025. The availability of derivatives has improved cost predictability for downstream bromination units, encouraging longer-term contracting with pharmaceutical, coating, and polymer customers.

On the supply side, the Nanjing Jiangbei New Material Technology Park commissioned a new 20,000-ton aromatic intermediates line in late 2025, explicitly targeting brominated precursors for automotive coatings, dispersants, and high-performance resins. Chinese manufacturers are also moving up the value chain through application-specific customization. In 2025, global polymer players active in China such as ELIX Polymers introduced more than 100 custom-color ABS alloy grades that rely on bromobenzene-derived intermediates for the medical device sector, where color consistency and regulatory compliance are critical. Environmental governance remains a decisive constraint. Continuous isotope monitoring rolled out by the Shandong Environmental Protection Bureau during 2024–2025 has forced producers to invest in closed-loop recovery and solvent reuse systems, raising compliance costs but also eliminating informal capacity. Export strategies have adjusted accordingly. Following new U.S. trade duties in 2025, Chinese bromobenzene suppliers redirected volumes toward ASEAN markets, increasing shipments to Vietnam and Indonesia by an estimated mid-teens percentage, reinforcing regional integration.

India Bromobenzene Market: API-Led Demand and Benzene Derivative Upgrading

India’s bromobenzene market is closely aligned with national ambitions to move from commodity chemicals toward complex, high-value intermediates. The July 2025 NITI Aayog strategy to expand India’s chemical sector to $450 billion by 2030 explicitly prioritizes advanced benzene derivatives over lower-margin chlorobenzenes. This policy signal has accelerated investment in bromination and downstream organometallic synthesis capacity, particularly in pharmaceutical and agrochemical corridors.

Demand fundamentals are anchored in pharmaceuticals. According to 2025 industry assessments, India’s growing role as a global API supplier is generating double-digit annual growth in the use of bromobenzene-derived Grignard reagents, especially for cardiovascular and central nervous system drug pipelines. Capacity additions are concentrated in Gujarat’s PCPIR, where new bromination units commissioned in August 2025 support the agrochemical sector’s transition toward bio-based and lower-toxicity formulations. Specialty producers such as Navin Fluorine have expanded organometallic synthesis lines to secure multi-year supply contracts with Western innovators, positioning India as a reliable export hub for oncology and fine chemical intermediates rather than a price-driven supplier.

United States Bromobenzene Market: Supply Security, TSCA Oversight, and Defense Applications

The U.S. bromobenzene industry is defined by supply security initiatives and intensifying regulatory scrutiny. In 2025, domestic bromine producers including Albemarle Corporation and LANXESS implemented efficiency upgrades at their El Dorado, Arkansas operations. These projects focus on improving bromine recovery yields, which directly stabilizes the availability and pricing of bromobenzene for domestic customers amid geopolitical uncertainty.

Regulatory pressure is increasing under the Toxic Substances Control Act. As of early 2026, EPA TSCA risk evaluations have extended deeper scrutiny to brominated aromatics, compelling manufacturers to deploy advanced VOC capture and abatement technologies for bromobenzene-based solvents. At the same time, selective demand is emerging from strategic sectors. In Q3 2025, the U.S. Department of Defense allocated funding for high-refractive-index optical coatings used in advanced sensor systems, where bromobenzene serves as a critical precursor. Productivity remains a competitive differentiator. Albemarle reported achieving $450 million in productivity improvements by November 2025, partly through optimization of its specialties portfolio, reinforcing the role of brominated intermediates as margin-supporting products within diversified chemical businesses.

Japan and Germany (European Union) Bromobenzene Market: Portfolio Rationalization and Electronics-Driven Demand

In Japan and the European Union, bromobenzene market dynamics are shaped by portfolio rationalization and electronics sector recovery. A defining move occurred on April 1, 2025, when LANXESS completed the divestment of its Urethane Systems business to UBE Corporation, marking its full transition toward pure specialty chemicals. Bromine specialties and industrial products, including bromobenzene, are now central to LANXESS’s strategic focus, supported by the consolidation of production into more competitive German clusters and the planned closure of higher-cost sites such as Widnes in the UK by 2026.

Japan’s demand profile is closely linked to advanced electronics. Stella Chemifa Corporation reported a 19.2% year-on-year increase in electronics-related chemical sales for the fiscal year ending March 2025, citing strong demand from advanced wafer fabrication facilities. Brominated intermediates, including bromobenzene-based doping and synthesis agents, are benefiting from this recovery. Across both Japan and Germany, the emphasis is less on capacity expansion and more on high-purity production, process reliability, and long-term customer qualification in electronics, optics, and specialty materials.

Comparative Snapshot of the Bromobenzene Industry by Country

Bromobenzene Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Strategic Direction

|

|

China

|

Automotive coatings, polymers, regional exports

|

Feedstock hedging, cluster expansion, ASEAN reorientation

|

|

India

|

APIs, agrochemicals, oncology intermediates

|

Shift to complex benzene derivatives, export positioning

|

|

United States

|

Defense optics, specialty solvents

|

Supply security, TSCA-driven compliance investment

|

|

Japan

|

Semiconductor chemicals

|

High-purity focus, electronics-led recovery

|

|

Germany / EU

|

Specialty industrial products

|

Portfolio rationalization, cost-competitive consolidation

|

Bromobenzene Market Report Scope

Bromobenzene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$252.3 Million

|

|

Market Size (2034)

|

$408.5 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Grade (Pharmaceutical Grade, Electronic Grade, Industrial Grade), By Type (Grignard Reagent Intermediates, Specialty Chemical Intermediates, Isotope Labeled Bromobenzene), By Application (Chemical Intermediates, Solvents, Electronics, Specialty Coatings), By End Use Industry (Pharmaceuticals and Biotechnology, Agrochemicals, Automotive and Aerospace, Electrical and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle Corporation, LANXESS, ICL Group, BASF, Tosoh Corporation, Stella Chemifa, Spectrum Chemical, Thermo Fisher Scientific, Navin Fluorine International, Heranba Industries, Neogen Chemicals, Shandong Fukang Group, Yancheng Longshen Chemical, Jiangsu Yoke Technology, Merck

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bromobenzene Market Segmentation

By Grade

- Pharmaceutical Grade

- Electronic Grade

- Industrial Grade

By Type

- Grignard Reagent Intermediates

- Specialty Chemical Intermediates

- Isotope Labeled Bromobenzene

By Application

- Chemical Intermediates

- Solvents

- Electronics

- Specialty Coatings

By End Use Industry

- Pharmaceuticals and Biotechnology

- Agrochemicals

- Automotive and Aerospace

- Electrical and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bromobenzene Industry

- Albemarle Corporation

- LANXESS

- ICL Group

- BASF

- Tosoh Corporation

- Stella Chemifa

- Spectrum Chemical

- Thermo Fisher Scientific

- Navin Fluorine International

- Heranba Industries

- Neogen Chemicals

- Shandong Fukang Group

- Yancheng Longshen Chemical

- Jiangsu Yoke Technology

- Merck

*- List not Exhaustive