Market Overview: Butylated Triphenyl Phosphate Market Growth Driven by Low-VOC Formulations, Phosphorus Additive Capacity Expansions, and EV Fluid Adoption (2025–2034)

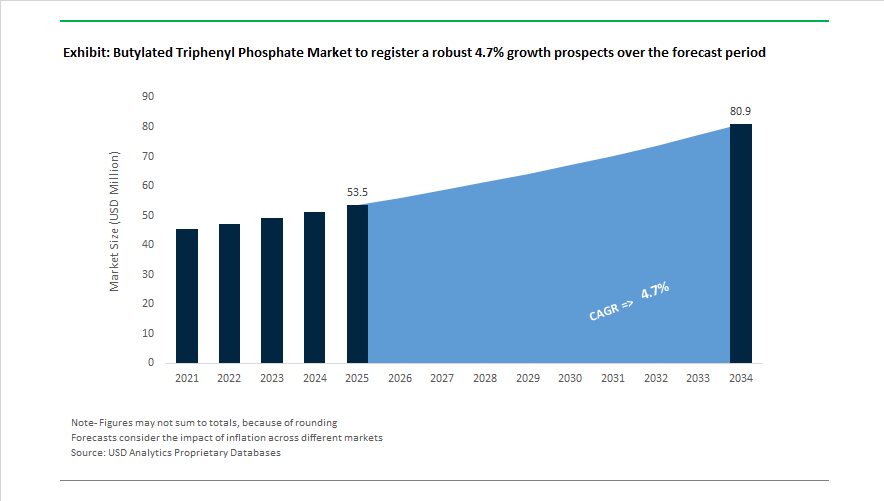

The butylated triphenyl phosphate market is projected to rise from USD 53.5 Million in 2025 to USD 80.9 Million by 2034, registering a CAGR of 4.7% supported by demand for non-phthalate plasticizers, phosphorus-based flame retardants, and fire-resistant industrial fluids. Regulatory alignment and product reformulation gained visibility in 2024 when EU REACH reviews prompted suppliers to update safety profiles for aryl phosphate esters, reinforcing handling and exposure standards for BTPP. In late 2025, LANXESS introduced Reofos BTP ECO, a lower-VOC grade designed for the European construction and electronics markets. The company further highlighted sustainable phosphorus additives at K 2025, emphasizing polymeric and reactive derivatives that reduce leaching and improve recyclability.

Capacity expansion and supply chain diversification defined 2025 market dynamics. During Q3 2025, ICL Group reported increased output of phosphorus-based solutions following US duties on Chinese imports, redirecting global supply toward Israeli production. Mid-2025 expansion by PCC Group in Europe strengthened availability of non-phthalate plasticizers and fire-resistant hydraulic fluid additives for aerospace and machinery applications. January 2025 tariff changes in the United States encouraged long-term supply agreements with producers in India and Israel, supporting sourcing diversification. India-based Tina Organics commissioned a new export-grade BTPP line in 2025 to serve Southeast Asian electronics hubs, while Zhejiang Wansheng introduced cost-optimized grades targeting flexible PVC for infrastructure wiring.

Application innovation and sustainability initiatives shape the 2026 outlook. BTPP adoption accelerated in EV e-transmission fluids during 2025 and 2026 due to its high flash point and chemical stability in thermal management systems. Radco Industries piloted a bio-based BTPP alternative in late 2025 using renewable phenol feedstocks for green building markets. In May 2025, LANXESS reported strong Specialty Additives performance with improved capacity utilization, while ICL redirected capital from its discontinued LFP cathode project in November 2025 to reinforce its phosphorus flame retardant portfolio.

High-Heat Performance, EPA Compliance Alignment, and Fire-Safety Expansion Driving Trends and Opportunities in the Butylated Triphenyl Phosphate Market

BTPP Displaces Conventional TPP in Engineering Plastics Due to Processing Stability and Moisture Resistance

Butylated Triphenyl Phosphate is becoming the preferred flame-retardant plasticizer in engineering-grade polymers where thermal and hydrolytic stability directly influence processing yield and end-use durability. Industrial data released in 2025 confirms that BTPP maintains phosphorus content and flame-retardant capability at temperatures above 220°C, which is essential for thin-wall polymer molding in electronics housings and precision components. Traditional Triphenyl Phosphate, by contrast, exhibits higher volatility and can vaporize during melt processing, causing material voiding and equipment fouling inside injection molding systems. BTPP also provides improved hydrolysis resistance, as validated in REACH-compliant dossiers for EC No. 700-990-0, preventing chemical leaching that can lead to stress cracking in PC/ABS and PBT blends. This is especially relevant for automotive cockpit trim, interior lighting housings, and climate control components exposed to humidity cycles over multi-year service lives.

U.S. EPA Safer Choice and DfE Framework Accelerate Institutional Adoption of BTPP

Corporate sustainability requirements and regulatory compliance are driving a structured shift toward BTPP in applications where environmental transparency has become a procurement prerequisite. Following major August 2024 revisions, the EPA Safer Choice program entered full adoption in 2025, increasing documentation requirements for flame retardant selection and chemical ingredient disclosure. Under these mandates, traditional TPP is facing reduced acceptance due to aquatic toxicity concerns, while butylated variants are being deployed as "informed substitution" materials that enable electronics OEMs to retain eco-labels such as EPEAT. This matters for supplier access to government procurement bids, as multiple federal and institutional purchasing contracts now tie qualification to Safer Chemical Ingredients listings. Tier-1 electronics producers are therefore reformulating housings, monitors, and laptop casings with BTPP-enabled flame retardants in order to maintain green-product certification continuity.

BTPP Unlocks High-Performance Plasticizers for Mission-Critical Cables in Transit, Mining, and Marine Installations

Infrastructure expansion across mining operations, shipbuilding, and mass-transit corridors is creating demand for cables capable of maintaining flexibility and insulation properties in extreme temperature conditions. BTPP operates as a flame-retardant plasticizer through a condensed-phase mechanism, promoting protective char formation that elevates Limiting Oxygen Index performance and supports UL-94 V-0 compliance. Its low volatility and chemical compatibility allow it to remain permanently integrated within PVC cable jackets, preventing brittleness during exposure to freezing mine shafts or heat exposure near ship engine rooms. This positions BTPP as a scalable replacement for legacy phthalate plasticizers, allowing OEMs to consolidate flame retardancy and plasticity into one additive and simplify raw material inventory planning.

Synergistic Acid Donor Role Positions BTPP as a Key Enabler of Thin-Film Intumescent Coatings

The modernization of commercial infrastructure and high-rise construction is strengthening demand for organic acid donors that enable efficient intumescence on structural steel. Butylated Triphenyl Phosphate is gaining traction as a preferred ingredient due to its high solubility, thermal durability, and compatibility with resin chemistries used in thin-film fireproofing. As coating producers such as Sherwin-Williams and PPG confirmed in October 2025 material releases, the industry is migrating from bulky cementitious coverings toward low-profile coatings engineered to expand rapidly under heat. BTPP enables these formulations to retain steel surface temperature below critical deformation thresholds for extended periods, supporting compliance with EN 13381-8 and similar global fire codes. Architectural regions such as the Middle East, including megaprojects like NEOM, are expected to adopt BTPP-containing systems due to the dual need for visible structural steel and stringent fire protection mandates.

Butylated Triphenyl Phosphate (BTP) Market Share and Segmentation Insights

Market Share by Function: Flame Retardant Leadership Reinforced by Plasticizer and Lubricant Performance

Flame retardant additive applications account for 47% of BTP consumption in 2025, positioning butylated triphenyl phosphate as a leading non-halogenated aryl phosphate ester for engineering plastics, PVC, and polyurethane foams. Its condensed-phase action promotes char formation while simultaneously plasticizing polymer matrices, aligning with regulatory pressure to replace halogenated systems. Plasticizer applications rank second, delivering flexibility, low-temperature performance, and reduced volatility in automotive interior films, wire and cable jacketing, and coated fabrics. Lubricant and hydraulic fluid additives form a significant segment, leveraging BTP’s thermal and hydrolytic stability in aviation hydraulic fluids and industrial systems, including fire-resistant phosphate ester fluids used in die casting and aerospace. Anti-wear functionality, though smaller, is expanding in gear oils and greases as high-performance machinery demands enhanced friction control.

Market Share By Function, 2025.png)

Market Share by End Use Industry: Electronics Lead While Automotive Electrification Accelerates Adoption

Electrical and electronics represent 31% of BTP demand in 2025, driven by its use as a flame-retardant plasticizer in connectors, enclosures, wire insulation, and PCB laminates, supported by miniaturization, higher power densities, and 5G infrastructure rollout under RoHS and REACH compliance frameworks. Automotive and transportation form the second-largest and fastest-growing segment, utilizing BTP in interior trim, under-hood components, and EV battery enclosures where low fogging, UV stability, and fire resistance are critical. Building and construction applications span PVC pipes, roofing membranes, and insulation foams, reinforced by fire safety codes and green building certifications. Industrial machinery consumes BTP in hydraulic systems and lubricants, while aerospace and defense remain high-value niches through phosphate ester hydraulic fluids for aircraft and flame-retarded cabin components. Marine and offshore applications persist at smaller scale, tied to shipbuilding and offshore energy investment.

Competitive Landscape of the Butylated Triphenyl Phosphate (BTPP) Market

The global Butylated Triphenyl Phosphate (BTPP) market in 2026 is defined by accelerating demand for fire-resistant hydraulic fluids, EV-grade flame retardants, aerospace composites, and low-VOC plasticizers, alongside tightening regulations on migration, toxicity, and lifecycle carbon footprint. Competition increasingly centers on vertical integration into phosphorus value chains, bio-based BTPP development, polymeric low-volatility derivatives, and AI-enabled manufacturing efficiency. Market leaders are differentiating through high-purity phosphate esters, controlled-release technologies, and application-specific formulations for power generation, data centers, electric mobility, and advanced electronics, positioning BTPP as a mission-critical additive for next-generation thermal management and fire safety systems.

Vertical phosphorus integration and turbine-fluid dominance by ICL Group

ICL leads the global BTPP landscape through its Fyrquel® and Phosflex® platforms, with Fyrquel® L serving as the 2026 benchmark fire-resistant fluid for steam turbine control systems in nuclear and thermal power plants. By shifting over 55% of revenue toward specialty chemicals in 2025/2026, ICL has strengthened its bromine and phosphate value-chain upgrades to support high-density AI data center cooling and lubrication. Ongoing debottlenecking of European and Israeli specialty phosphate assets is expanding capacity for EV battery-grade flame retardants. Its full vertical integration in phosphorus extraction provides unmatched supply security and cost stability, a decisive advantage as global demand for organophosphate esters accelerates.

Circular BTPP innovation for aerospace and eVTOL from LANXESS AG

LANXESS is a dominant force in high-performance BTPP additives, serving aerospace hydraulics and lightweight automotive composites. The launch of Reofos® BTP ECO in 2025/2026 introduced a bio-based butylated triphenyl phosphate designed to meet Green Building and Ecolabel standards for interior materials. Its 2026 strategy centers on high-molecular-weight BTPP derivatives with reduced migration and volatility, directly addressing regulatory scrutiny in Europe and North America. Integrated into LANXESS’s Lubricant Additives Business following the Chemtura acquisition, BTPP is now bundled with antioxidants and anti-wear agents in one-stop additive packages, supporting advanced thermoplastics for eVTOL aircraft and next-generation mobility platforms.

Low-VOC European supply resilience driven by PCC Rokita S.A.

PCC Rokita has emerged as Europe’s agile high-purity BTPP specialist through its Roflam® and Rostabil® portfolios, with 2026 demand led by flexible polyurethane foams for premium bedding and automotive seating. Its Brzeg Dolny expansion, completed in 2025, now operates as a regional hub for low-VOC phosphate esters aligned with stringent Clean Air automotive standards. PCC’s strategy emphasizes regional resilience, offering short lead times and localized technical support to EU OEMs reducing Asian sourcing exposure. Deep integration into chlor-alkali and phosphorus chains enables efficient byproduct recycling and energy-optimized BTPP synthesis, positioning PCC Rokita as a preferred European partner for sustainable flame-retardant plasticizers.

Cost-efficient export-grade BTPP leadership from Tina Organics Pvt. Ltd.

Tina Organics has transformed India into a competitive export base for non-halogenated phosphate esters, becoming a 2026 value leader in BTPP for industrial lubricants and PVC compounds. Its ashless BTPP grades deliver combined fire protection and wear reduction for heavy machinery applications. Expanded ISO 14001 certification at its Alwar facility underscores its environmentally responsible manufacturing credentials. Tina differentiates through entrepreneurial agility, tailoring viscosity and air-release properties to customer-specific hydraulic systems. With aggressive expansion into North American and Middle Eastern markets, the company leverages cost-efficient production and customized formulations to compete directly with Western incumbents on both performance and price.

Ultra-clean BTPP for electronics and displays from Daihachi Chemical Industry Co., Ltd.

Daihachi Chemical specializes in high-purity BTPP for electronics, supplying flame-retardant epoxy resins used in AI chip encapsulation and advanced semiconductor packaging. Its 2026 portfolio emphasizes hydrolytically stable phosphorus esters, including a newly developed low-stress BTPP grade that prevents surface cracking in thin-wall polycarbonate and PPO alloys. Daihachi is a key supplier to the Asian display industry, supporting OLED and micro-LED light-guide plates and optical films. Strategically, the company is enhancing Limiting Oxygen Index performance to achieve V-0 ratings at lower additive loadings, preserving the mechanical integrity of engineering plastics used in consumer electronics and precision components.

Scale-driven global plastics supply by Zhejiang Wansheng Co., Ltd.

Zhejiang Wansheng commands the volume segment of the BTPP market as the world’s largest organic phosphorus flame retardant producer. In 2025/2026, the company implemented AI-driven reactor controls, cutting energy consumption by 12% across BTPP and TCPP lines while advancing intelligent manufacturing. Its multi-site Chinese production network, paired with new US and EU sales entities, supports global wire and cable customers supplying high-speed rail and urban infrastructure projects under Belt and Road initiatives. Wansheng’s cost-curve leadership, backed by massive economies of scale and advanced waste-gas treatment, sets the global benchmark for price-to-performance in butylated phosphate esters.

China Butylated Triphenyl Phosphate Market: EV-Centric Demand and Continuous Manufacturing Upgrades

China’s butylated triphenyl phosphate industry is being reshaped by electrification, electronics localization, and process modernization. With national automobile output projected to reach 35 million units by late 2025, domestic BTP consumption has pivoted toward electric vehicle battery thermal management systems and flame-retardant wire harnesses. These applications require non-halogenated, high-stability phosphate esters that can perform under elevated temperatures and vibration, positioning BTP as a preferred additive across EV platforms.

Supply-side capability is advancing in parallel. In 2025, the Zhanjiang Verbund site integrated advanced phosphorus-based intermediate lines to localize BTP supply for electronics and printed circuit board manufacturers, reducing lead times and logistics risk. Producers in Shandong Province have also deployed AI-driven purification systems to consistently achieve electronic-grade purity above 99.5 percent, a requirement for next-generation consumer electronics enclosures. Regulatory pressure is accelerating process change. Following the 2025 Green Manufacturing Mandates, legacy batch reactors are being replaced with continuous flow synthesis to minimize 2,6-DTBP effluents and improve yield consistency. Beyond electronics, demand is broadening into steel and mining, where industrial hubs in Hebei are adopting BTP-based hydraulic fluids to meet updated workplace safety codes. On the trade front, exporters are realigning toward ASEAN markets such as Vietnam and Thailand to offset tariff pressures and follow electronics assembly migration.

United States Butylated Triphenyl Phosphate Market: Fire Safety Codes, Defense Applications, and TSCA Scrutiny

In the United States, the BTP market is driven by building safety regulation, defense innovation, and tighter chemical oversight. Updated 2025 guidelines from Federal Emergency Management Agency and National Fire Protection Association have accelerated the use of BTP-based flame retardants in high-density residential construction materials, responding to rising urban fire risk and stricter performance benchmarks.

Advanced mobility and defense programs are reinforcing this trend. New funding allocated by the U.S. Department of Defense in Q3 2025 supports the development of high-stability BTP lubricants capable of maintaining viscosity at extreme altitudes, a critical requirement for next-generation aerospace turbine systems. At the same time, regulatory compliance is tightening. As of January 2026, the United States Environmental Protection Agency has intensified TSCA risk evaluations for phosphorus-based plasticizers, prompting investments in enhanced VOC capture and process containment during butylation. The November 2024 update to the Persistent, Bioaccumulative, and Toxic chemicals rule has also accelerated the replacement of deca-BDE with BTP alternatives in automotive interiors. To secure supply resilience, late-2025 investments in Arkansas and Texas are focusing on nearshoring phosphorus feedstocks, insulating U.S. BTP producers from global freight volatility.

India Butylated Triphenyl Phosphate Market: Battery Materials, Export-Ready Flame Retardants, and Corridor Investments

India’s butylated triphenyl phosphate industry is gaining momentum from energy storage, pharmaceuticals, and export-oriented manufacturing. The Production Linked Incentive scheme for advanced chemistry cells has catalyzed domestic BTP demand as a fire-retardant additive in lithium-ion battery electrolytes, aligning chemical manufacturing with India’s broader energy transition goals.

Specialty chemical producers are also expanding into higher-purity applications. Firms such as Tina Organics expanded production lines in mid-2025 to supply refined BTP intermediates for specialized pharmaceutical coatings, where thermal stability and low volatility are essential. Downstream demand is widening as well. Rapid growth in e-commerce logistics is driving consumption of BTP-plasticized PVC used in protective packaging and automated sorting belts. Structurally, new investments within the Dahej Petroleum, Chemicals and Petrochemicals Investment Region are prioritizing non-halogenated flame retardants, positioning Indian producers to meet rising export demand from European electronics original equipment manufacturers that require compliance with stringent sustainability standards.

European Union Butylated Triphenyl Phosphate Market: Sustainability Screening and Infrastructure Pull

Across the European Union, the BTP market is defined by regulatory screening, low-impact product innovation, and infrastructure investment. On January 21, 2025, the European Chemicals Agency added related organophosphorus compounds to the Candidate List of Substances of Very High Concern, triggering mandatory notification for articles containing more than 0.1% BTP. This has increased documentation intensity and accelerated demand for well-characterized, biodegradable grades.

Producers are responding with portfolio innovation. LANXESS launched the Reofos® BTP ECO line in late 2025, a biodegradable variant designed to align with the EU Chemicals Strategy for Sustainability. On the manufacturing side, German sites in Ludwigshafen have implemented 2025-compliant wastewater treatment systems to ensure zero-detectable organophosphate discharge under the Industrial Emissions Directive. Demand fundamentals remain supportive. Large-scale Trans-European Transport Network projects planned for 2025–2030 are boosting consumption of high-performance flame retardants in rail carriage interiors, sustaining BTP use in long-life infrastructure applications.

Comparative Snapshot: Butylated Triphenyl Phosphate Industry by Country

Butylated Triphenyl Phosphate Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Strategic Direction

|

|

China

|

EV safety systems, electronics

|

Continuous flow synthesis, electronic-grade purity, ASEAN export pivot

|

|

United States

|

Fire-safe construction, defense

|

TSCA-driven process control, nearshored feedstocks

|

|

India

|

Batteries, pharma coatings, packaging

|

PLI-led localization, export-ready non-halogenated grades

|

|

European Union

|

Sustainable materials, transport

|

SVHC screening, biodegradable BTP innovation

|

Butylated Triphenyl Phosphate Market Report Scope

Butylated Triphenyl Phosphate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$53.5 Million

|

|

Market Size (2034)

|

$80.9 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Type (High Purity Grade, Standard Industrial Grade, Technical Grade), By Function (Flame Retardant Additive, Plasticizer, Lubricant and Hydraulic Fluid Additive, Anti Wear Agent), By Application (Lubricants and Hydraulic Fluids, PVC Compounds and Resins, Engineered Plastics, Textiles and Coatings, Energy Storage), By End Use Industry (Automotive and Transportation, Aerospace and Defense, Electrical and Electronics, Building and Construction, Industrial Machinery, Marine and Offshore)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS, ICL Group, PCC Rokita, Radco Industries, Tina Organics, Zhangjiagang Yarui Chemical, Salius Pharma, Avantor, Mosaic Company, Songwon Specialty Chemicals, Triveni Interchem, Jiangsu Victory Chemical, Sandhya Group, Ketan Chemical Corporation, Peritum Innovations

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Butylated Triphenyl Phosphate Market Segmentation

By Type

- High Purity Grade

- Standard Industrial Grade

- Technical Grade

By Function

- Flame Retardant Additive

- Plasticizer

- Lubricant and Hydraulic Fluid Additive

- Anti Wear Agent

By Application

- Lubricants and Hydraulic Fluids

- PVC Compounds and Resins

- Engineered Plastics

- Textiles and Coatings

- Energy Storage

By End Use Industry

- Automotive and Transportation

- Aerospace and Defense

- Electrical and Electronics

- Building and Construction

- Industrial Machinery

- Marine and Offshore

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Butylated Triphenyl Phosphate Industry

- LANXESS

- ICL Group

- PCC Rokita

- Radco Industries

- Tina Organics

- Zhangjiagang Yarui Chemical

- Salius Pharma

- Avantor

- Mosaic Company

- Songwon Specialty Chemicals

- Triveni Interchem

- Jiangsu Victory Chemical

- Sandhya Group

- Ketan Chemical Corporation

- Peritum Innovations

*- List not Exhaustive