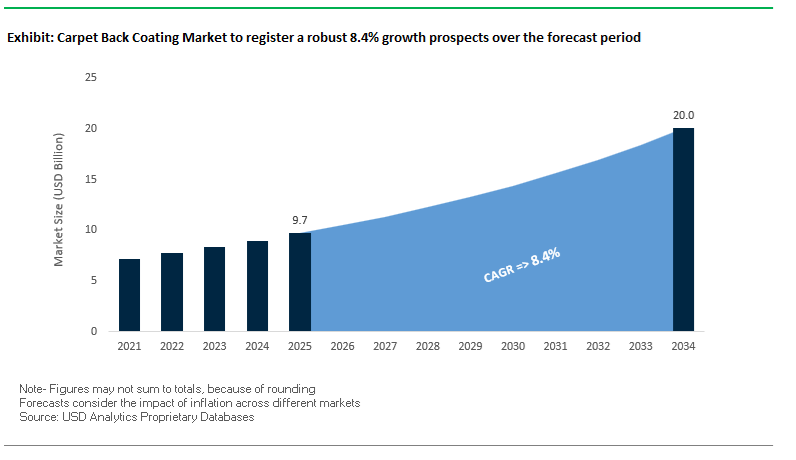

The carpet back coating market has become strategically important as flooring manufacturers respond to tightening indoor air quality standards, rising sustainability scrutiny, and demand for faster, cleaner installation systems in commercial interiors. Valued at USD 9.7 billion in 2025 and projected to reach USD 20 billion by 2034 at a CAGR of 8.4%, growth reflects the central role of back coating technologies in determining carpet durability, recyclability, acoustic performance, and total installed cost. For OEMs supplying offices, healthcare facilities, education campuses, and large-format commercial spaces, back coatings are no longer commodity layers but engineered systems that directly influence product certification, lifecycle performance, and installation productivity.

The core structural shift reshaping demand is the accelerated move away from bitumen and solvent-heavy backings toward low-VOC polymer dispersions, thermoplastic binders, and mono-material constructions compatible with circular recycling models. Polyurethane, polyolefin, and water-based latex dispersions are increasingly specified in both broadloom and modular carpet tile production, driven by compliance with LEED, BREEAM, and WELL building standards and by Eurofins indoor air quality requirements below 250 µg/m³ for public buildings. Manufacturers are redesigning backing architectures using non-phthalate plasticizers, recycled mineral fillers, and bio-based polymers to eliminate formaldehyde emissions while maintaining tuft bind strength, dimensional stability, and long-term performance under rolling loads and thermal cycling.

These material transitions are directly replacing legacy systems by enabling faster installation, reduced downtime, and improved in-use durability. Pre-applied pressure-sensitive adhesive (PSA) backings and hot-melt thermoplastic binders reduce on-site adhesive use, lower labor intensity, and support clean removal and replacement in high-churn commercial environments. Cushion polyurethane layers and advanced latex systems improve acoustic insulation and underfoot comfort while preserving stability under heavy traffic, reducing premature replacement and maintenance costs. As flooring OEMs scale circular product lines and align sourcing with closed-loop recycling infrastructures, competitive advantage in the carpet back coating market will increasingly depend on formulation consistency, recyclability-by-design, and certified low-emission manufacturing aligned with global green building and indoor health regulations.

The Global Carpet Back Coating Industry is witnessing rapid material innovation, production expansion, and circular economy adoption across major regions. In October 2025, BASF launched a low-VOC, low-CO₂ polymer dispersion production line in Türkiye, targeting construction and flooring markets across the Middle East and Africa (MEA). This investment marks a decisive step in localizing environmentally responsible adhesive and coating solutions that meet Eurofins and AgBB certification standards for low-emission interior applications.

In September 2025, Interface Inc. strengthened its sustainability leadership by partnering with a European waste management company to expand its CQuestBio® backing take-back program. The initiative aims to raise recycled and bio-based content in its carpet tile range from 88% to 92% within two years, reinforcing Interface’s carbon-negative product vision under its Climate Take Back™ commitment. Similarly, Shaw Industries announced in November 2024 the commercial launch of EcoWorx® Broadloom, a polyolefin-based, fully recyclable backing system, enabling closed-loop material recovery for wall-to-wall carpet installations.

Material transitions continue to accelerate. In June 2025, a leading North American manufacturer allocated $75 million to convert three broadloom lines from SBR latex to thermoplastic hot-melt backing, reducing natural gas usage and improving recyclability. Complementing this, Milliken & Company unveiled an updated TractionBack® system in May 2025, featuring a non-adhesive, high-friction polymer coating for moisture-prone subfloors—optimizing performance under high moisture vapor emission rates (MVER) common in commercial spaces.

Regulatory and chemical reforms are shaping product chemistry. The European Chemicals Agency (ECHA) proposal in December 2024 to restrict phthalate plasticizers used in PVC backing compounds has triggered widespread R&D into non-phthalate, bio-based polymer alternatives. Likewise, Lubrizol’s February 2025 introduction of a halogen-free flame-retardant polymer blend for automotive carpets demonstrates growing alignment with global FMVSS fire safety standards and the broader sustainable mobility shift.

The transition toward water-based polyurethane dispersions (PUDs) in carpet back coatings represents one of the most pivotal technological and regulatory shifts in the industry. Historically dominated by styrene-butadiene rubber (SBR) latex, the market is prioritizing PUD systems for their superior mechanical performance, flexibility, and ultra-low VOC emissions. Comparative performance studies show that while SBR latex provides adequate adhesion and abrasion resistance, polyurethane-based systems demonstrate 40–60% greater bond strength to fabric substrates and retain elasticity across wider temperature ranges. The flexibility translates into extended product life cycles and superior wear resistance, especially under dynamic loading and environmental fluctuations common in commercial installations.

The adoption of PUD back coatings is also being fast-tracked by regulatory compliance requirements. Green building certifications like LEED, WELL, and CRI Green Label Plus have set strict VOC thresholds, forcing manufacturers to abandon solvent-based and high-VOC formulations. Polyurethane dispersions align perfectly with these mandates, offering near-zero VOC emissions after full cure and eliminating the need for plasticizers or volatile coalescing agents. Additionally, PUD technology facilitates the development of PVC-free and bitumen-free backings, reducing environmental footprint while enhancing recyclability. As a result, global floor covering manufacturers are investing in waterborne PU systems as the future-ready standard for achieving both sustainability credentials and high-performance flooring solutions across commercial, hospitality, and healthcare sectors.

In an era where indoor environmental quality (IEQ) is a primary purchasing criterion, functional carpet backing technologies are rapidly gaining traction. The next generation of carpet back coatings is no longer limited to providing mechanical strength or dimensional stability—it functions as an active contributor to occupant health, air purity, and hygiene. The integration of antimicrobial and anti-mold additives, including zinc pyrithione, isothiazolinones, and thiabendazole compounds, is proving essential in preventing microbial growth within carpet structures. These solutions are particularly vital in institutional environments such as hospitals, schools, and offices where surface hygiene standards are strictly monitored.

Simultaneously, material innovation is steering toward low-emission, non-toxic formulations. Polymer manufacturers are introducing polyolefin elastomers (POEs) and olefin block copolymers (OBCs) that enable carpet coatings to be phthalate-free, PVC-free, and styrene-free, eliminating common sources of indoor volatile organic compounds. These formulations provide the dual benefit of enhanced thermal and acoustic comfort and reduced environmental exposure risk. Further, the global focus on green chemistry is pushing suppliers to design coatings that support circular manufacturing, comply with REACH regulations, and reduce exposure to persistent organic pollutants. Consequently, functional, health-driven coating design has become a key differentiator in premium flooring segments, aligning with long-term trends in sustainable architecture and occupant wellbeing.

The global shift toward circular economy principles is redefining material innovation in the carpet back coating market, emphasizing recyclability and resource recovery. One of the core barriers to carpet recycling has been the multi-layered polymer structure, which complicates material separation and decontamination at end-of-life. As a result, manufacturers are developing mono-material adhesive and backing systems that simplify recycling and maximize the recovery of high-value fibers such as Nylon 6 and PET.

The shift is supported by Extended Producer Responsibility (EPR) regulations, such as California’s Carpet Stewardship Program, which holds producers accountable for post-consumer waste collection and recycling. Under these frameworks, manufacturers are incentivized to design carpets that are easily separable and repulpable, minimizing contamination during polymer recovery. Studies show that recycling Nylon 6 from reclaimed carpet fibers reduces its carbon footprint by up to 90% compared to virgin material, underscoring the significant sustainability and economic impact of recyclable back coatings.

Future innovations are centered on Route 4 and Route 5 recycling pathways—reuse of mono-material polymers and chemical recycling “back to monomers.” These methods rely on back coatings engineered for clean deconstruction, allowing the face fiber and primary backing to be recovered without thermal or chemical degradation. As carpet manufacturers align with EPR, EU Green Deal, and ESG frameworks, demand for recyclable and de-bondable coating systems will continue to expand, transforming sustainability into a core business advantage rather than a regulatory burden.

The explosive growth of the Luxury Vinyl Tile (LVT) and Rigid Core Flooring markets has opened a new, adjacent frontier for carpet back coating technologies. These resilient flooring categories demand backing systems that deliver acoustic insulation, dimensional stability, and thermal comfort, creating strong synergies with innovations originally developed for carpet backings.

In high-density commercial and residential settings, acoustic performance is a critical specification. Advanced coating formulations are being engineered to improve Impact Isolation Class (IIC) and Sound Transmission Class (STC) ratings, reducing both airborne and impact noise. Materials such as cork composites, recycled rubber, and engineered polyurethane foams are increasingly used in back coatings to enhance sound absorption and footfall comfort. These integrated systems not only meet acoustic performance benchmarks but also contribute to green building certification credits under WELL and BREEAM for noise control and occupant comfort.

Simultaneously, dimensional stability remains a key technical challenge in LVT and Stone Polymer Composite (SPC) installations. Coating manufacturers are investing in elastomeric yet dimensionally stable polymers that can pass rigorous tests like ASTM D1204, ensuring resistance to curling, warping, and thermal expansion over the flooring’s service life. As LVT products continue to evolve toward larger format tiles and hybrid multi-layer constructions, high-strength back coatings will be essential to support their structural integrity and installation flexibility. The segment represents a high-margin opportunity for coating and adhesive suppliers capable of bridging the performance gap between traditional carpet backing and next-generation resilient flooring.

Carpet Back Coating Market Share Insights, 2025-2034

The Primary Backing segment dominates the global carpet back coating industry, accounting for approximately 53.6% of the total market share in 2025. Its leadership is driven by the sheer scale of use across tufted carpet production, which represents over 90% of global carpet output. Primary backing involves applying a latex, polyurethane, or PVC coating directly to the carpet’s base to anchor yarn tufts and ensure dimensional stability. This process is fundamental to carpet construction, as it prevents yarn pull-out, improves handling, and enhances performance during subsequent finishing processes. The widespread adoption of styrene-butadiene rubber (SBR) latex in primary coatings stems from its cost-effectiveness, adhesion performance, and compatibility with a broad range of fibers (nylon, polyester, polypropylene). With the continued dominance of tufted carpets in both residential and commercial flooring, the demand for robust primary coatings remains exceptionally strong. Moreover, technological innovations—such as low-VOC latex systems, bio-based binders, and filler optimization for weight reduction—are reinforcing this segment’s dominance, aligning with sustainability regulations in North America and Europe. Primary back coatings also play an increasingly important role in acoustic insulation and comfort enhancement, adding more functional value to modern flooring systems.

The Secondary Backing segment, holding roughly 40.9% of the global carpet back coating market, is driven by the increasing need for durability, stiffness, and moisture resistance in high-performance carpet applications. Secondary backings involve laminating an additional layer—commonly polypropylene (PP) woven fabric, felt, or PVC films—to the primary backing using a secondary layer of latex, polyurethane, or thermoplastic adhesive. This dual-layer structure significantly enhances the carpet’s mechanical strength, enabling it to withstand heavy foot traffic and extended wear cycles in commercial buildings, hospitality, educational institutions, and transportation interiors. The segment also benefits from the rise in modular carpet tiles, where secondary backing systems improve ease of installation, dimensional stability, and floor grip. With sustainability gaining prominence, recyclable thermoplastic backings and PVC-free alternatives are expanding rapidly, especially in Europe and the U.S. Furthermore, high-performance outdoor carpets and artificial turfs rely on secondary coatings for weatherproofing and UV stability, positioning this segment as critical for both function and longevity.

The Specialty Backings segment, while smaller in volume, represents a high-margin and innovation-driven niche in the global carpet back coating market. These backings are designed for specific functional or aesthetic requirements, such as integrated cushioning for enhanced comfort, anti-static coatings for data centers, anti-slip layers for hospitality and healthcare environments, and conductive backings for electronic facilities. Specialty backings are also gaining popularity in sports and event flooring, where high resilience and rapid installation are required. The segment is characterized by the growing use of custom-engineered polymer systems, including thermoplastic elastomers (TPE), silicone-based coatings, and polyurethane foams. As end-users demand multifunctional carpets—combining durability, safety, comfort, and sustainability—manufacturers are increasingly investing in smart and hybrid back coatings with features like antimicrobial performance and acoustic insulation.

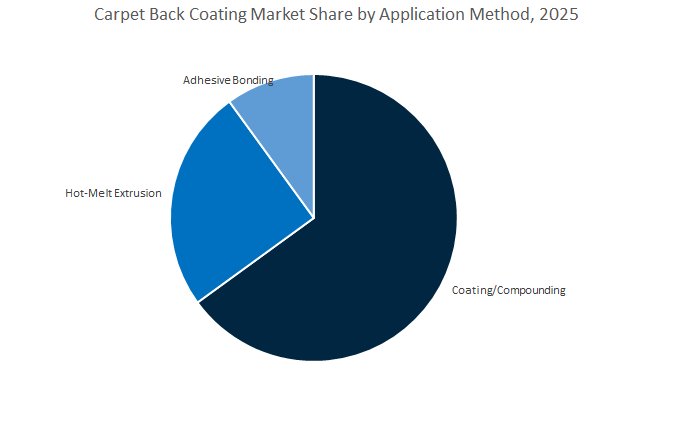

The Coating/Compounding method represents the largest and most established process in the global carpet back coating industry, accounting for over 61.5% of total applications in 2025. This method involves applying a liquid compound—commonly SBR latex, PVC plastisol, or polyurethane—via knife-over-roll coaters, followed by drying and curing in a controlled oven. Its dominance is rooted in its process flexibility, uniform coating distribution, and compatibility with both primary and secondary backings. The method’s ability to incorporate fillers like calcium carbonate or clay also helps manufacturers optimize weight, cost, and dimensional stability. Coating/compounding is the preferred process for tufted carpets, broadloom products, and carpet tiles, providing robust tuft lock strength and durability. Additionally, its adaptability to different polymer chemistries enables precise tuning of properties such as softness, adhesion, and moisture resistance. Recent advancements, such as energy-efficient infrared curing, bio-based latex alternatives, and digital control systems, are making this technology more sustainable and efficient. As demand rises for carpets with higher acoustic and thermal insulation performance, coating systems continue to evolve with enhanced formulations that align with the green building movement and international indoor air quality standards.

The Hot-Melt Extrusion method is rapidly gaining traction as a sustainable and high-speed alternative to conventional coating systems. Utilizing thermoplastic polymers such as polyolefins, thermoplastic elastomers (TPE), and polyurethanes, this process involves melting and extruding a continuous film or coating onto the carpet backing. Its key advantage lies in energy efficiency—it eliminates the need for drying ovens, reducing both production time and carbon footprint. Additionally, hot-melt extrusion allows for recyclable, solvent-free coatings with minimal VOC emissions, aligning with global sustainability regulations and circular economy goals. This method is particularly suited for secondary backings and carpet tiles, where precision thickness and fast lamination speeds are critical. It also enables the integration of functional layers such as moisture barriers and acoustic insulation in a single processing step. As global carpet manufacturers prioritize closed-loop recycling systems and eco-friendly production, hot-melt extrusion is expected to see accelerating adoption, especially in Europe, North America, and high-end contract flooring markets.

The Adhesive Bonding method holds an important, though smaller, share in the market, primarily serving high-performance carpet tile and composite flooring applications. This process involves laminating a pre-fabricated secondary backing (such as PVC, polyurethane foam, or bitumen felt) to the primary carpet base using specialized adhesive layers. It enables the production of dimensionally stable, easy-to-install modular carpet tiles, a segment experiencing strong growth in commercial and office interiors. Adhesive bonding is also vital for creating multi-layered structures with distinct functional properties, such as sound attenuation, moisture resistance, or underfoot cushioning. Manufacturers increasingly employ low-VOC reactive polyurethane and water-based adhesives to comply with green building standards while maintaining bond durability. The method’s precision and compatibility with automated lamination systems make it a preferred choice for carpet products that must meet stringent performance and sustainability benchmarks.

The Global Carpet Back Coating Market is characterized by high R&D intensity, integrated chemical supply chains, and sustainability-driven innovation. Major players such as Dow Chemical, BASF SE, The Lubrizol Company, Wacker Chemie AG, Interface Inc., and Shaw Industries dominate through advanced polymer technologies, global production footprints, and circular manufacturing models.

Dow Chemical maintains a strong global leadership position in SBR latex and acrylic dispersion systems for both primary and secondary carpet back coatings. The company’s expansion of its ELASTENE™ polyolefin elastomer line reflects its push into lightweight, flexible, and high-durability backing materials for both commercial flooring and automotive interiors. Dow’s ongoing Texas performance monomer expansion is designed to secure raw material availability for the carpet industry, while its low-ammonia, low-odor latex formulations improve manufacturing air quality and sustainability compliance.

BASF SE leads in polymer dispersions and resins, supplying its renowned Acronal® and Basonal® lines for pre-coat and final-coat applications. The company’s Mass Balance-certified products enable customers to achieve carbon-reduced production footprints, aligning with green procurement standards. BASF recently introduced a halogen-free flame-retardant additive for polyurethane cushion backings, improving fire safety and smoke suppression in commercial installations. The company’s integrated production network ensures consistent supply of acrylics, PU, and styrene-based materials for modular carpet systems worldwide.

Lubrizol specializes in TPU-based polymer resins and low-smoke, flame-retardant compounds for premium carpet back coatings. Its TempRite™ CPVC materials are widely adopted for transportation and public space flooring, offering superior flame resistance and low emissions. The company’s innovation strategy focuses on high-solid, low-VOC adhesives that shorten drying time and reduce manufacturing energy intensity. Recent R&D investments emphasize tunable polymer blends designed for enhanced tuft lock strength and acoustic insulation, supporting the expansion of cushion-backed carpet markets.

Wacker Chemie AG offers VAE (vinyl acetate ethylene) dispersions as a low-VOC latex alternative, recognized for superior aging resistance and low odor. Its SILRES™ silicone additives enhance stain resistance and water repellency, improving carpet longevity in commercial environments. The company’s ethylene-vinyl laurate (EVL) dispersion, launched recently, meets German AgBB and Blue Angel standards for ultra-low-VOC carpet production. By optimizing VAE binders for high filler compatibility, Wacker delivers cost-effective, durable secondary backing solutions for sustainable carpet manufacturing.

Interface Inc. is at the forefront of sustainable carpet innovation with its CQuestBio® and CQuestBioX® backings, which integrate recycled fillers and bio-based polymers to achieve carbon-negative footprints. Under its Mission Zero® and Climate Take Back™ initiatives, Interface aims to eliminate virgin petroleum usage in backing materials. Recent partnerships with chemical recyclers have strengthened supply consistency for post-industrial PVC and PET, expanding circular production capabilities across Europe and North America.

Shaw Industries continues to set the standard in closed-loop carpet recycling through its EcoWorx® Polyolefin backing platform, which enables cradle-to-cradle material recovery. The EcoWorx® Broadloom system, recently launched, extends Shaw’s recyclable technology from carpet tiles to wall-to-wall carpets, reducing overall shipping emissions by 30% due to its lightweight composition. Proprietary technologies such as Ultraloc® and LokDok® deliver superior tuft lock performance and dimensional stability, ensuring durability in high-traffic commercial spaces.

The U.S. remains a high-value hub for carpet back coating thanks to continual upgrades in performance backings, circular programs, and low-emission chemistries specified by LEED/WELL projects. In 2025, Shaw Industries launched new carpet styles featuring LifeGuard® Spill-Proof Technology backings that integrate a robust moisture barrier to stop liquid penetration into the pad—directly improving warranty outcomes, IAQ, and lifecycle costs in education, hospitality, and multifamily. Shaw also rolled out Pet Perfect+™ (ANSO® high-performance fibers + R2X® Stain & Soil Protection + LifeGuard®), purpose-built for pet-friendly residential and build-to-rent portfolios that demand odor control, stain defense, and watertight secondary backing.

Sustainability is embedded end-to-end: Shaw’s re[TURN]® Reclamation Program (nearly 1 billion pounds of carpet reclaimed since 2006) includes takeback for ReWorx® hybrid flooring and other Shaw resilient products—expanding feedstock security for recycled content backings. A 2024 strategic partnership with PPG extends Patcraft’s portfolio into resinous flooring, strengthening Shaw’s commercial surfaces and backing solutions ecosystem. On the procurement side, LEED/WELL preferences for low-VOC carpet tile backings continue to lift water-based polymer dispersions and mass-balance raw materials. Shaw’s 2024 renewable power investment (BHE Renewables’ Flat Top wind farm) reduces Scope 2 emissions on the path to 2030 net-zero operations, tightening the carbon profile of U.S. carpet backing supply chains.

Germany anchors the EU’s transition to eco-friendly carpet backing under REACH, the Circular Economy Action Plan, and DGNB/EPD procurement norms. Chemical leaders (Wacker Chemie, BASF) are accelerating water-based polymer dispersions and SB-latex alternatives with materially lower VOCs for carpet tile and broadloom secondary backings. Specifications routinely call for non-halogenated, low-odor, and mass-balance inputs to hit whole-building LCA targets and meet EPD transparency. The result: faster adoption of bio-based resins, recycled mineral fillers, and lower-temperature cure systems that cut embodied carbon without sacrificing tuft bind, dimensional stability, or telegraphing resistance.

Supply-chain synergies are also expanding: Shaw Industries’ 2023 strategic partnership with Classen Group (Germany) broadens hard-surface innovation and can unlock regional sourcing expertise for back-coating materials. European specifiers intensify demands for carbon-footprint disclosures, pushing mills and compounders toward audited EPDs, solvent-free binders, and circular design (monomaterial tiles; click-release backings). Germany’s leadership in DGNB projects further cements the market trajectory: low-emission polymer dispersions plus recycled-content backing constructions as standard for high-performance carpet tiles in offices, healthcare, and public buildings.

China’s rapid urbanization keeps it pivotal for carpet back coating scale-up. In May 2024, BASF added a second polymer dispersions line at Daya Bay (Huizhou) to serve surging demand across coatings and carpet backing; in March 2024 it rebranded Huizhou and Jiangsu dispersions plants to “BASF Specialty Material”, signaling diversification beyond paper to functional textiles and back-coating chemistries. Local and multinational formulators are investing in hot-melt adhesive systems and EVA-based backings tailored to Chinese climate and price points, balancing tuft bind, dimensional stability, anti-static performance, and recyclability.

Industrial growth in manufacturing parks and tech campuses is lifting carpet tile demand with anti-static and heavy-traffic backings, while municipal and A-grade office fit-outs push for low-VOC, odor-controlled systems. With code evolution and green-building incentives spreading nationwide, mills prioritize high-quality dispersions, precise roll-to-roll coating, and modular carpet tile backing that maintains flatness and telegraph resistance under long service intervals.

India’s dual engine—export leadership in rugs/carpets and accelerating domestic urbanization—is reshaping carpet back-coating demand. Government PLI programs strengthen textiles and component manufacturing, improving local availability of primary/secondary backing. Exports (~$1.37B in FY2023, CEPC) sustain steady throughput, requiring consistent tuft bind, caliper control, and latex/EVA stability across global climates. On the sustainability front, BASF India announced (Sept 2025) REDcert² certification for its Dahej and Mangalore dispersions plants—the first in India—enabling biomass-balanced, low-carbon water-based polymer dispersions for coatings and potential carpet backing use, a critical lever for EPD-aligned projects.

Domestically, a rising middle class is boosting spend on modern flooring in metros and tier-2 cities, increasing adoption of tufted/woven carpets with latex and synthetic backings for hospitality, corporate offices, and premium residential towers. Specifiers are beginning to request low-VOC, odor-light backings and recycled content to align with corporate ESG policies, while mills invest in precision coating and improved dimensional stability to compete on performance—not just price—against imports.

Türkiye is scaling as a regional supply hub for carpet backing chemistries across Türkiye, the Middle East, and North Africa. In October 2025, BASF started up a new line in Dilovası, expanding capacity for low-VOC, low-CO₂ dispersions targeted at architectural coatings and carpet back-coating customers. The plant is slated to operate on green electricity and utilize Mass Balance to deliver reduced-carbon dispersions, directly supporting mills pursuing EPD credits and green procurement.

Strategically positioned between Europe and MENA, Türkiye’s upgraded capacity enhances supply reliability and lead times for carpet tile and broadloom manufacturers. With commercial builds and mixed-use complexes rising in Istanbul, Ankara, and coastal tourism corridors, demand is growing for durable, dimensionally stable, and low-odor backings that withstand high footfall and seasonal humidity swings.

The UK’s carpet back-coating market is propelled by premium commercial renovations in office and hospitality, favoring acoustic and underfoot-comfort backings that deliver low noise, high resilience, and clean indoor air. Victoria PLC’s acquisition of Balta Group businesses (rugs, polypropylene carpet, non-wovens) enhances European vertical integration—supporting consistent secondary backing supply, modern calendering/slitting, and faster custom developments for designer-led specifications.

UK manufacturers increasingly specify post-consumer recycled PET/nylon in backing systems to meet government and corporate net-zero targets and public procurement standards. The result is broader availability of recycled-content carpet tiles with low-VOC dispersions, high tuft-bind, and telegraphing control—ideal for CAT-A/CAT-B office fit-outs, education, and healthcare. As London and regional cities accelerate refurb over rebuild, demand rises for fast-install carpet tiles with dimensionally stable backings that minimize downtime and deliver circularity credentials.

Carpet back coating market, carpet tile backing systems, water-based polymer dispersions, low-VOC carpet backing, recycled-content carpet tiles, spill-proof carpet backing, dimensional stability, tuft bind performance, biomass-balanced dispersions, EPD flooring materials, DGNB/LEED/WELL carpets, resinous flooring integration.

Carpet Back Coating Market Report Scope

Carpet Back Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.7 Billion

|

|

Market Size (2034)

|

$20 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Coating Material (Styrene-Butadiene Latex, Polyurethane Systems, Ethylene Vinyl Acetate, Polyvinyl Chloride, Other Polymers/Materials), By Backing Type (Primary Backing, Secondary Backing, Specialty Backings), By Application Method (Coating/Compounding, Hot-Melt Extrusion, Adhesive Bonding), By End-User (Commercial, Residential, Automotive/Transportation), By Carpet Type (Tufted Carpets, Carpet Tiles, Woven Carpets

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shaw Industries Group, Inc., Mohawk Industries, Inc., The Dow Chemical Company, BASF SE, Wacker Chemie AG, Interface, Inc., Milliken & Company, H.B. Fuller Company, Tarkett S.A., Victoria PLC, Freudenberg Group, Beaulieu Technical Textiles NV, Balta Group NV, Arkema Group, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Coating Material/Polymer Type

- Styrene-Butadiene Latex

- Polyurethane Systems

- Ethylene Vinyl Acetate

- Polyvinyl Chloride

- Other Polymers/Materials

By Backing Type

- Primary Backing

- Secondary Backing

- Specialty Backings

By Application Method

- Coating/Compounding

- Hot-Melt Extrusion

- Adhesive Bonding

By End-Use Sector

- Commercial

- Residential

- Automotive/Transportation

By Carpet Type

- Tufted Carpets

- Carpet Tiles

- Woven Carpets

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Shaw Industries Group, Inc.

- Mohawk Industries, Inc.

- The Dow Chemical Company

- BASF SE

- Wacker Chemie AG

- Interface, Inc.

- Milliken & Company

- H.B. Fuller Company

- Tarkett S.A.

- Victoria PLC

- Freudenberg Group

- Beaulieu Technical Textiles NV

- Balta Group NV

- Arkema Group

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

This comprehensive Carpet Back Coating Market report by USDAnalytics investigates the evolving landscape of low-VOC, thermoplastic, and circular carpet back-coating technologies shaping the global flooring industry. It presents an in-depth analysis of the market’s transition toward sustainable, performance-oriented polymer systems—examining innovations in polyurethane dispersions, hot-melt extrusions, and adhesive bonding applications. The report provides analytical reviews and breakthrough insights into leading coating systems, manufacturing processes, and the regulatory reforms driving next-generation carpet materials. It highlights the strategies of key industry players, from Dow Chemical and BASF SE to Shaw Industries and Interface Inc., as they navigate sustainability mandates, recyclability challenges, and shifting consumer preferences. Through comprehensive value-chain mapping, technological benchmarking, and cross-regional performance evaluation, this report is an essential resource for flooring manufacturers, polymer chemists, architects, and sustainability professionals seeking actionable intelligence to guide investment and product development strategies across both commercial and residential sectors. With meticulous attention to industry trends, lifecycle sustainability, and performance optimization, USDAnalytics ensures this study serves as a trusted reference for decision-makers in material innovation and circular economy integration.

Scope Highlights

- Segmentation: By Coating Material/Polymer Type (Styrene-Butadiene Latex, Polyurethane Systems, Ethylene Vinyl Acetate, Polyvinyl Chloride, Others); By Backing Type (Primary, Secondary, Specialty); By Application Method (Coating/Compounding, Hot-Melt Extrusion, Adhesive Bonding); By End-Use Sector (Commercial, Residential, Automotive/Transportation); By Carpet Type (Tufted, Carpet Tiles, Woven Carpets).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Covers historic data (2021–2024) and forecast estimates (2025–2034) for market size, growth rate, and technological evolution.

- Company Coverage: Detailed analysis and profiles of 15+ key players, emphasizing R&D pipelines, production expansion, and sustainability initiatives.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.