Market Overview: PFAS-Free Coatings, Renewable Energy Adoption, and Strategic M&A Drive Chemical Surface Treatment Market

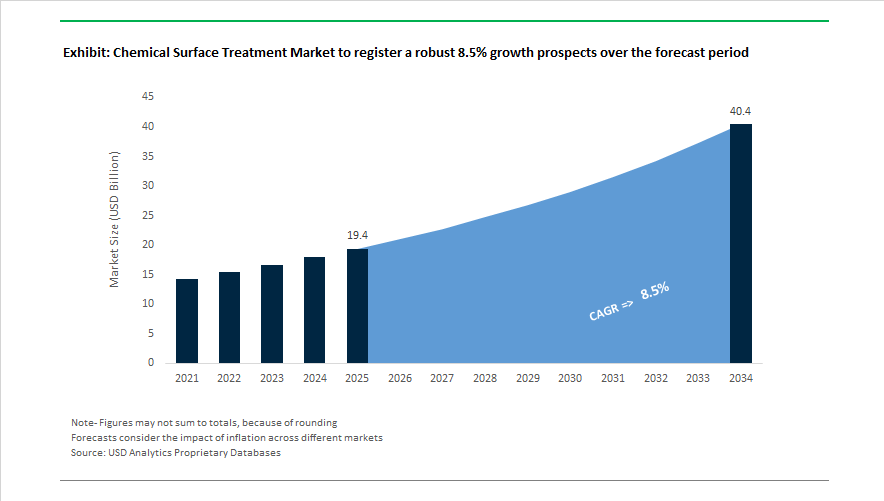

The Chemical Surface Treatment Market is forecast to grow from USD 19.4 billion in 2025 to USD 40.4 billion by 2034, advancing at a CAGR of 8.5% as sustainable metal finishing chemicals, PFAS-free coatings, advanced pretreatment technologies, and aerospace-grade corrosion protection solutions gain rapid adoption. Market consolidation began in January 2024 when SurTec International acquired the bonded coatings business of OKS Spezialschmierstoffe, integrating top coats and sealants for fastener surface treatment systems. Leadership restructuring followed in November 2024 when Quaker Houghton appointed Joseph Berquist as CEO, with a strategic focus on Fluidcare chemical management and EV battery surface treatment chemistries. Capacity and technology localization accelerated in January 2025 as Oerlikon opened its Smart Integrated Surface Solutions Centre in Tumakuru, India, combining PVD coatings and thermal spray technologies to serve automotive and aerospace clusters.

Portfolio expansion intensified in April 2025 when Quaker Houghton completed the acquisition of Dipsol Chemicals, strengthening its electroplating chemicals and functional surface coatings presence across automotive electronics and semiconductor manufacturing. In May 2025, MKS Instruments brand Atotech inaugurated a strategic facility in Spain to support sustainable aluminum pretreatment for die-cast and lightweight structural parts. Sustainability leadership advanced in the same month as BASF’s Chemetall transitioned its Langelsheim production site to 100% renewable electricity, reducing annual CO2 emissions by about 620 tons. Aerospace recognition followed in September 2025 when Chemetall earned the Airbus SQIP award for high-performance sealants and corrosion protection solutions. Also in September 2025, PPG Industries introduced ENVIROLUXE PFAS-free powder coatings derived from recycled plastics, addressing tightening environmental regulations in construction and consumer goods.

Technology innovation defined late 2025 and early 2026. In November 2025, Oerlikon launched the INSPIRA carbon coating platform using S3p plasma technology, enhancing wear resistance and productivity of precision components. Atotech unveiled advanced aluminum pretreatment solutions in December 2025 for EUROGUSS applications, tailored to EV motor housings and lightweight vehicle architectures. Digital and sustainability tools gained prominence in February 2026 when Henkel expanded its HEART environmental reporting platform to include use-phase CO2 modeling for bonding and surface treatment processes. Commercial expansion continued in January 2026 as PPG became the sole coatings supplier to Quality Collision Group in the United States, deploying waterborne refinish systems and digital color technologies.

Chemical Surface Treatment Market Trends and Opportunities Accelerating Regulatory Compliance, Lightweighting, and Sustainable Manufacturing

The Chemical Surface Treatment Market is transitioning from legacy all-purpose chemistries toward substrate-specific, regulation-ready formulations as aerospace, automotive, and industrial manufacturers respond to hazardous substance bans and next-generation material requirements. Regulatory pressure on hexavalent chromium, rapid EV platform evolution, and lightweighting mandates are reshaping pretreatment chemistry, conversion coatings, and water management strategies.

At the same time, OEMs are prioritizing process sustainability, adhesion reliability, and lifecycle performance, creating demand for advanced non-chrome systems, EV battery enclosure coatings, smart steel pretreatments, and closed-loop rinse water recovery. These forces are unlocking premium opportunities for suppliers offering compliance-driven, application-tailored surface treatment solutions.

Market Trend: Aerospace OEMs and MROs Fast-Track Non-Hex Chrome Systems Ahead of Regulatory Deadlines

The aerospace sector is accelerating its exit from hexavalent chromium as European Chemicals Agency advances restrictions on thirteen Cr(VI) compounds, potentially enforceable by 2027 to 2028. While transition costs are significant, long-term health benefits materially outweigh compliance expenses, reinforcing the shift toward trivalent and chrome-free alternatives.

Major OEMs including Airbus and Boeing have validated Cr(III) and chrome-free chemistries, with MIL-DTL-5541 Type II now standard for new aluminum components. TCP-based systems increasingly match legacy salt-spray performance, driving strong adoption of non-hex pretreatments across aerospace MRO and component supply chains.

Market Trend: EV Battery Enclosures Driving Advanced Conversion Coatings and Adhesion Technologies

Electric vehicle battery enclosures demand coatings that balance corrosion resistance, dielectric insulation, flame retardancy, and adhesive compatibility. In April 2025, Henkel introduced surface treatments for EV systems engineered to enhance structural adhesive bonding up to 12 MPa while enabling disassembly for recycling.

Cell-to-Body and Cell-to-Chassis designs now require conversion coatings capable of bonding aluminum to composites under thermal runaway conditions. Zirconium-based systems are replacing zinc phosphates for aluminum trays, forming nanometer-scale layers that cut sludge generation by roughly 90%. This shift improves ESG performance while supporting lightweight battery packs exceeding 450 kg, accelerating demand for EV-specific surface treatment chemistries.

Market Opportunity: Specialized Cleaners for Third-Generation AHSS Enable Automotive Lightweighting

Third-generation Advanced High-Strength Steels introduce selective oxidation challenges that disrupt galvanizing and coating adhesion. Grades such as Fortiform® from ArcelorMittal and jetQ® from thyssenkrupp feature complex martensitic-austenitic microstructures with elevated silicon and aluminum content.

This drives demand for acidic and alkaline cleaners that selectively remove surface oxides without inducing hydrogen embrittlement. Optimized pretreatment is essential for steels exceeding 1,200 MPa tensile strength to preserve hole-expansion formability and crash performance. As automakers target 25% component weight reduction, smart AHSS pretreatments represent a high-margin growth avenue for chemical formulators.

Market Opportunity: Closed-Loop Rinse Water Recovery Systems Create ESG-Driven Differentiation

Surface treatment remains among the most water-intensive manufacturing steps, making circular water systems a strategic priority. In 2025, global manufacturers began formalizing circular-water milestones in ESG disclosures, with industrial effluent treatment emerging as the fastest-growing water reuse segment through 2030.

Advanced reverse osmosis and ion exchange packages now enable recovery of up to 95% of rinse water, supporting Zero Liquid Discharge in water-stressed hubs across Mexico and Asia-Pacific. Although capital intensive, well-maintained closed-loop systems operate with annual water losses below 10%, reducing freshwater procurement and hazardous waste disposal costs while strengthening sustainability credentials for surface treatment operations.

Chemical Surface Treatment Market Share and Segmentation Insights

Cleaners and Plating Chemicals Anchor Surface Preparation Value Chains Amid Regulatory Transition

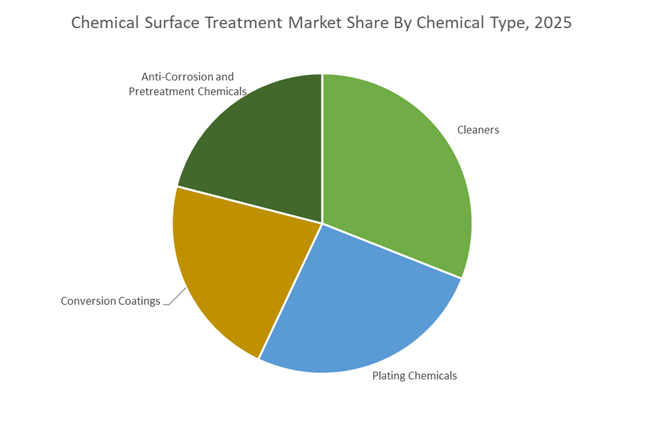

Cleaners command 31% of the chemical surface treatment market in 2025, reflecting their foundational role in surface preparation prior to plating, coating, and finishing operations. Alkaline cleaners, acid pickling solutions, and aqueous degreasers are critical for removing oils, oxides, and contaminants across automotive manufacturing, aerospace assembly, and electronics production. The transition toward VOC-free, phosphate-free, and bio-based cleaning chemistries is accelerating under REACH and global environmental compliance mandates. Plating chemicals represent the second-largest segment, spanning electroplating and electroless plating systems such as copper, nickel, chromium, zinc, and precious metals. Demand is closely linked to automotive component production and PCB manufacturing. Conversion coatings remain essential for corrosion resistance and paint adhesion, while zirconium- and silane-based chrome-free technologies are gaining share. Anti-corrosion and advanced pretreatment chemicals are the fastest-growing category, driven by thin-film nanotechnology and multi-metal compatibility requirements.

Automotive Dominates End Use as Electronics and Aerospace Drive High-Specification Coating Demand

Automotive accounts for 38% of total surface treatment demand, supported by body-in-white pretreatment, electrocoating (e-coat), decorative chrome plating, and corrosion-resistant finishes. The electric vehicle transition is reshaping coating specifications, particularly for battery enclosures, e-motor housings, and lightweight aluminum components requiring multi-metal pretreatment systems. Electronics is the fastest-growing end-user segment, with electroless nickel immersion gold (ENIG), copper plating, and tin-silver finishes critical for high-frequency PCBs, semiconductor packaging, and ADAS modules. Industrial machinery maintains steady consumption of hard chrome alternatives and wear-resistant coatings aligned with capital equipment investment cycles. Aerospace and defense require NADCAP-certified anodizing, chromate conversion coatings, and high-temperature protective finishes. Construction demand is tied to architectural aluminum anodizing and coil coating pretreatment, while consumer appliances and healthcare sustain niche growth through decorative plating and antimicrobial surface technologies.

Competitive Landscape of the Chemical Surface Treatment Market

The global Chemical Surface Treatment Market in 2026 is being driven by rapid electrification, lightweight materials adoption, and tightening VOC and carbon regulations across automotive, aerospace, electronics, and architectural coatings. Market leaders are competing on chromium-free pretreatments, water-based conversion coatings, digital bath management, EMI shielding, and energy-efficient application technologies. Growth is concentrated in EV aluminum anodizing, flexible electronics, aerospace sealants, and sustainable metal pretreatment, with suppliers differentiating through AI-enabled process control, zero-VOC chemistries, and closed-loop manufacturing models. Strategic M&A, digitalization, and sustainability-led portfolios are defining competitive advantage as OEMs demand lower total cost of ownership and regulatory-ready surface solutions.

Henkel accelerates dominance in flexible substrates and EV-grade surface chemistries

Henkel AG & Co. KGaA enters 2026 as the most aggressive consolidator in specialty surface treatment, strengthening its footprint through the €2.1 billion acquisition of Stahl Group and the January 2026 purchase of ATP Adhesive Systems. Its BONDERITE® portfolio now includes Bonderite M-AD 2000A, optimizing aluminum anodizing for EV and architectural applications. Henkel also launched an advanced EMI shielding film that replaces heavy metal housings in autonomous vehicle sensors. Over 90% of its 2026 acquisitions focus on water-based, zero-VOC technologies, positioning Henkel to navigate EU CBAM requirements while expanding into electronic miniaturization, flexible materials, and sustainable surface pretreatment.

BASF Chemetall leads aerospace and digital surface management with AI-driven control

BASF, operating through its Chemetall brand, remains the 2026 benchmark for aerospace and conversion coating technologies. The company expanded Naftoseal® aircraft sealant capacity at Langelsheim to meet rising narrow-body jet demand, while introducing Near-Zero SVOC dispersions for healthier interior surfaces. BASF’s Global Digital Hub in Hyderabad now delivers AI-powered bath optimization and real-time chemical monitoring, reducing waste across global customer sites. Through its Verbund integration, Chemetall links surface treatment chemistries with battery recycling at Schwarzheide, creating a closed-loop supply chain for EV manufacturers. This combination of digital services and circular chemistry anchors BASF’s leadership in high-reliability surface systems.

PPG advances precision pretreatment with automation and sustainably advantaged coatings

PPG Industries, Inc. dominates 2026 through automated, energy-efficient surface technologies tailored for automotive OEMs. A new 250,000-sq-ft Tennessee facility supports high-efficiency pretreatment, while over 41% of sales now come from sustainably advantaged products such as ENVIRO-PRIME® EPIC, enabling lower bake temperatures and major energy savings. PPG’s LINQ™ and MOONWALK® digital platforms reduce mixing errors and cut chemical waste by up to 15% . Via its Advanced Surface Technologies joint venture, PPG is scaling dry-applied paint films that replace traditional spray booths, reinforcing its position in precision application, material efficiency, and next-generation automotive surface protection.

Nippon Paint deploys functional coatings for climate resilience and hygienic interiors

Nippon Paint Holdings leads Asia-Pacific in 2026 with surface treatments designed for social impact, from heat-shielding greenhouse coatings to antiviral interior finishes. Its “Perfect Interior Air Clean” series is being deployed across transit and healthcare facilities, while chromium-free and fluorine-free treatments for beverage cans are reducing industrial wastewater burdens. Through its “Resonate 2026–27” strategy, Nippon Paint integrates color science and surface texture to enhance wellness in senior living environments. Participation in drone-applied agricultural coatings further expands its footprint in intelligent surfaces, positioning the company as a key innovator in climate-adaptive and public-health-driven surface treatment solutions.

Quaker Houghton specializes in low-sludge metal pretreatment to cut industrial TCO

Quaker Houghton remains the 2026 specialist in metalworking fluids and pretreatment, focused squarely on lowering total cost of ownership for heavy industry. Its DEXBOND SZR sludge reduction technology is replacing traditional phosphodegreasing, cutting hazardous sludge generation by up to 90% while simplifying wastewater handling. This approach delivers measurable savings for steel processors, automotive suppliers, and machinery manufacturers facing stricter environmental compliance. By combining process chemistry with application expertise, Quaker Houghton enables cleaner production lines, reduced downtime, and safer operations, reinforcing its role as a performance-driven partner for industrial surface preparation and metal finishing.

India: Industry 4.0 Surface Treatment Expansion and “Beyond Paint” Sustainability Acceleration

India’s chemical surface treatment industry is scaling rapidly on the back of advanced manufacturing investments, green building mandates, and automotive localization. In July 2024, Henkel Adhesive Technologies completed Phase III of its Kurkumbh facility near Pune. The LEED Gold-certified site integrates Industry 4.0 architecture and Automated Storage and Retrieval Systems (ASRS) to support surging domestic demand for high-performance Loctite® surface treatments, metal pretreatment chemicals, and industrial bonding technologies. In June 2025, Nihon Parkerizing Co., Ltd. announced a new Chennai plant to localize automotive-grade phosphating and surface modification systems, strengthening Southern India’s automotive finishing ecosystem.

Sustainability-led innovation is accelerating. In December 2025, Nippon Paint India unveiled its “Beyond Paint” portfolio at IGBC Mumbai, introducing Cool Tec heat-reflective coatings and N-Shield protective films for climate-positive infrastructure. Production Linked Incentive (PLI) schemes realized over ₹2 lakh crore in investments by September 2025, indirectly driving demand for corrosion-resistant coatings in electronics and specialty steel sectors. Adoption of bio-based degreasers under the “Zero Effect Zero Defect” (ZED) framework is rising among MSMEs, while IGBC and LEED certifications have triggered a 15% increase in chemical sealers and water repellents for high-rise concrete infrastructure by early 2026.

China: Low-VOC Mandates, HCFC Ban, and Semiconductor-Grade Surface Chemistry

China’s chemical surface treatment market is undergoing structural reform through stringent hazardous substance regulation and green production mandates. Effective June 1, 2026, GB 30981.1-2025 and GB 30981.2-2025 introduce strict hazardous substance limits for architectural and industrial coatings, accelerating nationwide conversion to water-based coatings and powder coatings. The Ministry of Ecology and Environment has also implemented a full HCFC ban for industrial cleaning and surface preparation effective July 1, 2026, eliminating legacy chlorinated solvent degreasing.

To support semiconductor self-sufficiency targets under the 15th Five-Year Plan, China is expanding ultra-pure electronic-grade etching chemicals and surface cleaning agents. MIIT’s late-2025 “Green Production” plan targets 300 billion yuan in green revenue, incentivizing low-VOC pretreatment lines and neutral pH biodegradable chemistries across Shanghai and Gulei chemical parks. Under Montreal Protocol compliance, 90% of SMEs transitioned from ODS to hydrofluoroethers (HFE) by late 2025. These regulatory-driven upgrades are reshaping China’s metal finishing, pickling, and pretreatment landscape toward environmentally compliant, export-ready chemistries.

Germany: Chromium-Free Passivation, Digital Twin Plating Lines, and Low-Carbon Hydrogen Integration

Germany remains Europe’s technology anchor for advanced chemical surface treatment. In 2024, Chemetall inaugurated its Global Aluminum Competence Center, centralizing R&D for anodizing and lightweight aluminum pretreatment technologies critical for aerospace and automotive sectors. In October 2025, Chemetall launched Gardolene® D, the first chromium- and fluoride-free copper foil passivation technology aligned with EU Regulation 2023/1542 battery passport requirements, enabling compliance in electric vehicle (EV) battery manufacturing.

German decarbonization infrastructure is reinforcing specialty surfactant synthesis. BASF’s 54 MW Ludwigshafen electrolysis plant (operational 2025) supplies low-carbon hydrogen for metal finishing intermediates. Producers are deploying Digital Twin plating lines to optimize bath concentration and temperature in real time, cutting chemical waste by 12% . Under the High-Tech Strategy 2025, R&D tax incentives (FzulG) have stimulated SME innovation in self-healing anti-corrosion coatings. Simultaneously, Dow’s upstream rationalization in Europe is shifting focus toward higher-margin, low-carbon surface intermediates to stabilize EBITDA by 2027.

United States: PFAS Regulatory Pressure, Waterborne Coating Investment, and Aerospace Growth

The U.S. chemical surface treatment sector is being reshaped by PFAS regulation, aerospace demand, and strategic manufacturing investments. In 2025, more than 200 PFAS-related bills were introduced across 30 states, with Maryland and Illinois banning intentionally added PFAS in certain treatments effective 2026. On January 6, 2025, the EPA expanded the Toxic Release Inventory (TRI) to 205 reportable PFAS compounds, intensifying disclosure requirements for surface treatment facilities.

Industrial reinvestment remains strong. In May 2024, PPG Industries committed $300 million to expand sustainable waterborne coatings capacity in Tennessee—the first such plant in 15 years—supporting automakers’ transition to low-VOC systems. PPG’s aerospace segment reported record performance in early 2025, driven by demand for chrome-free primers that reduce aircraft weight and fuel consumption. In April 2024, Henkel acquired Seal for Life Industries, strengthening MRO protective coatings for renewable energy and water infrastructure. Strategic stockpiling by firms such as Lakeland Industries further bolstered domestic supply resilience amid tariff volatility.

Japan: ¥500 Billion Electroplating R&D and Automotive Coating Transformation

Japan’s chemical surface treatment industry is anchored in precision electroplating and automotive innovation. By 2026, Japanese firms are projected to invest approximately ¥500 billion in automated pulse plating and eco-friendly electroplating technologies to improve efficiency and reduce wastewater generation in electronics manufacturing. The automotive sector is allocating nearly ¥3 trillion to EV and autonomous vehicle technologies, driving demand for LiDAR-compatible black coatings and advanced in-mold surface treatments.

Nippon Paint recently launched oil-repellent surface technologies for industrial and residential applications using proprietary dispersion systems to reduce grease accumulation. In September 2025, Chemetall and Azelis expanded ASEAN distribution partnerships to serve automotive and aluminum finishing hubs. Regulatory updates under Japan’s Industrial Safety and Health Act in 2025 mandate detailed permeation documentation for high-hazard surface sealants, reinforcing technical transparency across industrial coating operations.

Thailand: Bio-Based Surfactant Hub and Chromium-Free EV Passivation Leadership

Thailand is emerging as Southeast Asia’s bio-circular surface treatment hub. In November 2025, BASF expanded its Alkyl Polyglucosides (APG) plant in Bangpakong, reinforcing Thailand’s role in supplying bio-based surfactants for industrial surface cleaning and pretreatment applications. The country has also become a strategic launch market for chromium-free passivation technologies such as Gardolene D to support its expanding EV battery manufacturing sector.

At the Surface & Coatings 2025 exhibition in Bangkok, over 100 new electrostatic painting, chemical polishing, and corrosion protection technologies were showcased to more than 83,000 industry professionals. Thailand’s Bio-Circular-Green (BCG) economic model is accelerating adoption of low-VOC and biodegradable metal finishing chemistries, positioning the nation as a competitive regional base for automotive and electronics surface treatment solutions.

Chemical Surface Treatment Market Report Scope

Chemical Surface Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.4 Billion

|

|

Market Size (2034)

|

$40.4 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Chemical Type (Cleaners, Plating Chemicals, Conversion Coatings, Anti-Corrosion and Pretreatment Chemicals), By Base Material (Metals, Plastics and Polymers, Wood and Composites, Concrete and Glass), By Treatment Method (Chemical Treatment, Electrochemical Treatment, Thermal and Vacuum Treatment, Mechanical Treatment), By End-User Industry (Automotive, Aerospace and Defense, Construction, Electronics, Industrial Machinery, Consumer Appliances and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, BASF SE, PPG Industries, Inc., Nippon Paint Holdings Co., Ltd., Akzo Nobel N.V., The Sherwin-Williams Company, Kansai Paint Co., Ltd., Dow Inc., OC Oerlikon Corporation AG, Quaker Chemical Corporation, Sika AG, Element Solutions Inc., Nouryon Chemicals Holding B.V., Hempel A/S, Jotun A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Surface Treatment Market Segmentation

By Chemical Type

- Cleaners

- Plating Chemicals

- Conversion Coatings

- Anti-Corrosion and Pretreatment Chemicals

By Base Material

- Metals

- Plastics and Polymers

- Wood and Composites

- Concrete and Glass

By Treatment Method

- Chemical Treatment

- Electrochemical Treatment

- Thermal and Vacuum Treatment

- Mechanical Treatment

By End-User Industry

- Automotive

- Aerospace and Defense

- Construction

- Electronics

- Industrial Machinery

- Consumer Appliances and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chemical Surface Treatment Industry

- Henkel AG & Co. KGaA

- BASF SE

- PPG Industries, Inc.

- Nippon Paint Holdings Co., Ltd.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- Dow Inc.

- OC Oerlikon Corporation AG

- Quaker Chemical Corporation

- Sika AG

- Element Solutions Inc.

- Nouryon Chemicals Holding B.V.

- Hempel A/S

- Jotun A/S

*- List not Exhaustive