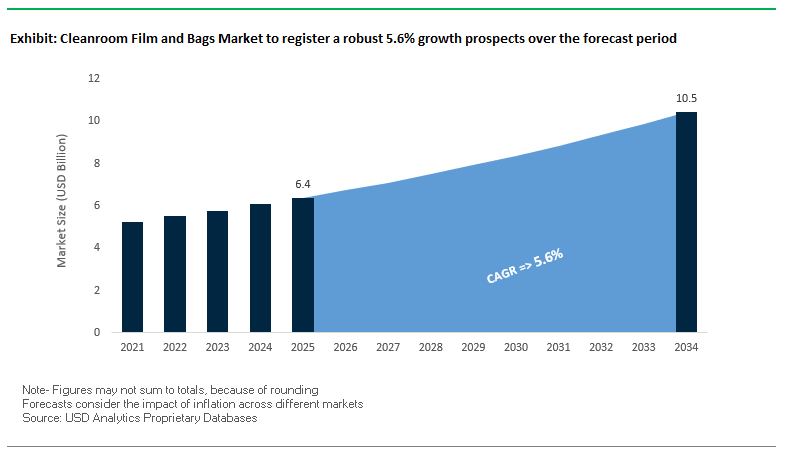

Cleanroom Film & Bags Market to Hit $10.5B by 2034 at 5.6% CAGR on Sterility, ESD Protection and Regulatory Compliance

Executive overview. The global cleanroom film and bags market is expanding as pharma, semiconductor, and medical device manufacturers tighten particle control, demand sterile, single-use packaging, and require ESD/antistatic protection for sensitive electronics. Procurement teams are prioritizing materials that withstand sterilization (e.g., gamma, EtO), document lot traceability, and comply with FDA/EMA frameworks. Growth is reinforced by capital investments in cleanroom converting and multilayer blown films, plus a steady stream of ISO-classified product launches targeting high-barrier, low-outgassing performance.

Key Insights for buyers & operations leaders

- Particle control is paramount: Cleanroom films/bags are produced in controlled environments to minimize particulates for aseptic filling, device kits, and wafer handling.

- Single-use dominates: One-and-done sterile bags reduce cross-contamination risk and cleaning validation burden.

- Specialized materials: ESD/ESD-safe and static-dissipative structures protect electronics; medical films are engineered for gamma/EtO compatibility and sterile barrier integrity.

- Regulatory imperative: FDA/EMA expectations drive documentation (CoC/CoA), biocompatibility, extractables/leachables rigor, and full traceability.

Market Analysis: Sterile Automation, ESD Performance, and Capacity Expansions Shape Demand

The near-term outlook is supported by automation and robotic aseptic handling that reduce particulate generation and human intervention. In September 2025, Steriline announced it would debut a robotic 3D Control & Picking Solution (3D CPS) at Fachpack to lower particle release during capping and crimping an upstream driver that intensifies demand for low-shed, cleanroom-grade primary/secondary packaging. In August 2025, Graphic Packaging International introduced child-resistant paperboard for detergent pods, signaling cross-industry “paperization”; while not a direct substitute for sterile pouches, it reinforces brand-owner pressure to decarbonize secondary packaging adjacent to cleanroom supply chains. July 2025 saw Amcor launch the Hector child-resistant closure with up to 100% PCR, underscoring a broader push to lightweight and circularize rigid components used alongside sterile film and bag systems.

On the capacity and technology front, suppliers expanded cleanroom converting to address high-barrier and ESD needs in semiconductors and life sciences. In March 2024, Cleanroom Film & Bags (CFB) rolled out CFB CleanTronics Advanced Packaging for the semiconductor/microelectronics segment, while in January 2024 TekniPlex Healthcare began multilayer blown-film manufacturing inside an ISO Class 7 cleanroom at Puurs, Belgium, targeting higher-barrier sterile applications. Industry consolidation continues: October 2023, Thomas Scientific acquired Quintana Associates to strengthen distribution of cleanroom packaging; and in March 2023, Millstone Medical Outsourcing added 5,000 sq ft of cleanroom manufacturing in Massachusetts to support medical OEM kitting and sterile barrier workflows.

Upstream material science also matters. Biopolymer investments (e.g., March 2025 Teknor Apex acquisition of Danimer Scientific) indicate future options for bio-based, low-outgassing cleanroom films provided they meet sterility, ESD, and leachables/extractables thresholds. Buyers should pressure-test suppliers on sterilization modality compatibility, ESD decay, ionic/anion contamination, FTIR/GC-MS profiles, and lot-level traceability to de-risk audits and shorten validation timelines.

Strategic Trends and High-Value Opportunities Driving the Cleanroom Film and Bags Market

Accelerated Adoption of Recycled and Bio-Based Polymer Content

A notable trend in the cleanroom film and bags market is the accelerated integration of post-consumer recycled (PCR) content and bio-based polymers. This shift is largely driven by stringent ESG goals and potential regulatory pressures, moving the market beyond superficial sustainability claims into verifiable, large-scale adoption. Traditional polymers carry a high environmental footprint, prompting material suppliers to explore bio-based LDPE alternatives and advanced mechanical recycling processes to maintain the high purity required in cleanroom environments. Companies like Jarrett Industries have introduced bio-based cleanroom bags under the “Pristine Green Clean Bags” line, combining sustainability with strict contamination control standards. Research studies highlight challenges in maintaining polymer quality during recycling, yet ongoing innovations in additives and processing are mitigating these issues. This trend represents a major growth avenue, enabling suppliers to gain a competitive advantage by offering certified, sustainable packaging solutions without compromising cleanroom performance.

Strategic Vertical Integration and Onshoring of Critical Packaging Supply Chains

The onshoring and vertical integration of cleanroom packaging is gaining momentum, driven by geopolitical uncertainties and legislation such as the U.S. CHIPS and Science Act of 2022. Critical industries including semiconductors, aerospace, and defense are emphasizing domestic manufacturing and tighter control over raw material supply chains to mitigate disruption risks. Companies are responding by promoting fully integrated U.S.-based manufacturing, sourcing resin domestically, and maintaining in-house extrusion and conversion capabilities. This trend addresses supply chain vulnerabilities exposed during the COVID-19 pandemic and ongoing geopolitical tensions. Cleanroom packaging suppliers that can offer end-to-end domestic solutions and guaranteed supply are positioned to capture market share, particularly from clients seeking to de-risk operations while complying with government mandates.

Development of High-Barrier Films for Advanced Semiconductor Nodes

The emergence of sub-3nm semiconductor nodes has created a direct need for ultra-high-barrier cleanroom films to prevent contamination from particles and chemical outgassing, such as amines, that can severely impact chip yields. Material scientists are developing co-extruded and monolayer films with superior gas and particle barrier properties, including specialized nylon and metalized films. Industry research emphasizes the importance of ultra-low outgassing and particle-shedding films, crucial for high-performance semiconductor fabrication. The deployment of these high-barrier films represents a high-value growth segment, as companies capable of producing and certifying such materials will dominate a critical niche in the semiconductor packaging market. Semiconductor fabricators underline the role of cleanroom packaging in controlling static, particulates, and out-gassing, highlighting its importance in protecting advanced wafers.

Expansion into High-Growth Cell and Gene Therapy Packaging

The rapid growth of the cell and gene therapy (CGT) market presents a compelling opportunity for specialized cleanroom bags designed for cryogenic storage and transport. CGT products demand ultra-low temperature maintenance (as low as -196°C) while preserving sterility and product integrity. Packaging solutions must withstand freezing, storage, and transport stresses, requiring single-use, sterile, and durable cleanroom bags. Companies are innovating cryogenic-ready bags, manufactured in certified cleanrooms, to meet the rigorous requirements of living cell therapies. This sector represents a high-growth avenue for the cleanroom film and bags market, providing opportunities for suppliers to develop advanced materials and expand into a rapidly evolving biotech segment, positioning themselves at the forefront of cold chain and therapeutic packaging innovation.

Competitive Landscape: Leaders Scale ISO-Class Production, ESD Controls, and High-Barrier Sterile Packaging

A concentrated group of material-science and converting specialists is competing on ISO-classified capacity, device-grade documentation, ESD performance, and gamma/EtO stability. Below, each company profile emphasizes differentiators important to sourcing teams.

TekniPlex Healthcare scales ISO-Class multilayer blown film

TekniPlex’s healthcare division focuses on cleanroom-manufactured films, bags, and laminates for pharma and medical devices, aligning with global demand for high-barrier, low-particulate packaging and complete traceability. In January 2024, TekniPlex commissioned a multilayer blown film line within an ISO Class 7 cleanroom in Puurs, Belgium, boosting regional supply for sterile barrier and device kit applications. The company’s strength lies in applied material science and custom formulations engineered for gamma/EtO sterilization with controlled COF and tear/peel design. Cleanroom products are typically double/triple-bagged for point-of-use transfer and individually labeled to support UDI and lot genealogy. TekniPlex’s consultative approach helps OEMs reduce validation time and align with FDA/EMA documentation practices.

CFB targets semiconductor ESD with CleanTronics platform

Cleanroom Film & Bags (CFB) a C-P Flexible Packaging division specializes in non-particulating, static-dissipative cleanroom packaging for electronics, medical, and aerospace customers. In March 2024, CFB launched CleanTronics Advanced Packaging tailored to semiconductor/microelectronics device handling, complementing its May 2023 expansion in nylon cleanroom packaging. The portfolio spans films, bags, and tubing engineered for ESD control, ionic cleanliness, and low outgassing, critical for wafers, PCBs, and precision optics. CFB’s strategic focus is process cleanliness + ESD stability, supplying certified cleanliness levels and documentation packages that accelerate incoming inspection and reduce yield loss. Key applications include die attach, front-end fabs, and medical electronics.

Amcor advances sustainable, cleanroom-grade healthcare packaging

Amcor supplies flexible/rigid healthcare packaging from high-barrier laminates to sterile pouches backed by a global network and sustainability roadmap targeting recyclable/reusable solutions. In July 2025, Amcor introduced the Hector child-resistant closure leveraging up to 100% PCR, showing how rigid components can advance circularity alongside sterile films and bags. Amcor’s cleanroom-grade offerings emphasize sterilization compatibility, validated seal integrity, and global regulatory alignment for pharmaceuticals and devices. Differentiators include scalable capacity, global tech support, and the ability to harmonize material specs across regions reducing change-control risk for multinational programs and simplifying supplier qualification.

Sealed Air (SEE) supports high-barrier Cryovac formats

Sealed Air delivers Cryovac high-barrier, multilayer films used in controlled environments across food, medical, and facility hygiene with a product-protection heritage applicable to cleanroom workflows. The company continues to invest in lightweighting and materials innovation (2024 initiatives) to reduce resin use while maintaining barrier and mechanical performance beneficial for cleanroom secondary packaging and sterile supply chains where waste reduction is scrutinized. SEE’s strengths include global service coverage, application engineering, and validated barrier specs for moisture/oxygen control vital for shelf-life-sensitive medical components and diagnostic consumables. Buyers value its quality systems and established change-notification rigor.

Pristine Clean Bags® elevates ISO-Class 5 purity and ESD options

Pristine Clean Bags® (Jarrett Industries) manufactures cleanroom PE and specialty bags/tubing with options for antistatic/ESD performance, serving medical, semiconductor, and aerospace programs. Products are produced in an ISO Class 5 cleanroom and certified to IEST-STD-CC1246D, addressing stringent particle limits. The firm offers bio-based LDPE options that pair sustainability with low-outgassing requirements, plus non-animal origin and surfactant-free materials for sensitive applications. Custom convert-to-order capabilities include double-bagging, cleanroom labeling, and lot traceability, simplifying line clearance and audit readiness for regulated customers.

DuPont leverages Tyvek sterile barrier leadership

DuPont brings deep science to sterile barrier markets via Tyvek, widely specified for medical device packaging where porosity + microbial barrier and sterilization compatibility are critical. The company invests in lightweighting and sustainable materials while maintaining the mechanical strength, porosity, and cleanliness profile that has made Tyvek a standard in device packaging. Its global R&D footprint and materials characterization expertise support risk-based design, helping OEMs validate peel performance, fiber-free opening, and post-sterilization integrity. DuPont’s breadth enables system solutions that pair Tyvek with compatible films, streamlining qualification and global change control.

Cleanroom Film and Bags Market Share Insights

Films & Wraps Lead Cleanroom Film and Bags Market Share by Product Type

By product type, films and wraps hold the dominant share of the cleanroom film and bags market in 2025, driven by their critical role in surface protection, component packaging, and contamination control in highly sensitive environments. Their widespread use across pharmaceutical cleanrooms, semiconductor fabs, and medical device manufacturing underscores their versatility and essential function in preventing particulate, microbial, and electrostatic contamination. Bags and pouches follow as the second-largest segment, widely adopted for sterile packaging of components, medical instruments, and sensitive electronic parts requiring moisture, static, and particulate barriers. Tubing solutions serve a growing niche, particularly in biotechnology and pharmaceutical sectors, where sterile transfer of liquids and powders under controlled environments is vital. Other formats, including specialty liners and covers, represent smaller shares but cater to highly customized applications. The leadership of films and wraps reflects the industry’s prioritization of barrier performance, durability, and compliance with ISO and FDA cleanroom standards.

Pharmaceuticals and Biotechnology Dominate Cleanroom Film and Bags Market Share by End-Use Industry

By end-use industry, pharmaceuticals and biotechnology represent the largest share of the cleanroom film and bags market in 2025, reflecting stringent GMP and FDA compliance requirements for sterility, contamination prevention, and secure handling of high-value drugs and biologics. Medical devices form another major share, as sterile barrier packaging is critical to maintaining product integrity through manufacturing, storage, and distribution. Electrical and electronics manufacturers also contribute significantly, with growing demand for electrostatic discharge (ESD)-safe bags and films to protect delicate semiconductors, printed circuit boards, and high-performance sensors. Aerospace and defense applications rely on cleanroom packaging for precision components requiring extreme protection during assembly and storage. The food and beverages sector represents an emerging area, adopting cleanroom-grade packaging to extend shelf life, ensure safety, and support contamination-free processing of high-value foods. Other industries, though smaller in share, showcase the versatility of cleanroom packaging in meeting specialized contamination-control needs. The dominance of pharmaceuticals and biotechnology highlights the sector’s role as the anchor for market growth, while electronics and medical devices reinforce diversification across technology-driven industries.

United States Cleanroom Film and Bags Market Strengthened by Regulatory Compliance and Advanced Material Innovations

The U.S. cleanroom film and bags market is strongly influenced by stringent regulations set by the FDA and ISO 14644 cleanroom standards, ensuring high purity and particulate control for pharmaceutical, medical device, and electronics applications. Strategic corporate investments are expanding domestic production capacity, exemplified by Millstone Medical Outsourcing’s Massachusetts facility expansion in March 2023 and Raumedic AG’s North Carolina expansion in February 2022.

Technological advancements are focusing on advanced polymers, nano-coatings, UV-resistant films, and heat-sealable & peelable materials to enhance barrier properties and reduce outgassing. Key applications include sterile pharmaceutical packaging, medical devices, and high-purity electronics components. The market is also experiencing consolidation, with Thomas Scientific acquiring Quintana Associates in August 2023 and PPC Flexible Packaging LLC acquiring StePac in February 2023, strengthening market presence. Geographical expansion in states like California and Massachusetts reflects regional medical industry growth, while material innovations in nylon, Aclar, and static shield foils address the specific requirements of microelectronics and aerospace sectors.

Germany Cleanroom Film and Bags Market Driven by Quality Assurance and Sustainable Practices

Germany’s cleanroom film and bags market operates under strict EU regulations, including the Packaging and Packaging Waste Regulation (PPWR) effective February 2025, alongside national GMP standards. Manufacturers emphasize rigorous quality assurance, producing products in ISO 14644 Class 5–7 cleanrooms and providing Certificates of Analysis to ensure compliance and traceability.

Technological innovation is centered on highly pure, low-particle solutions, exemplified by Bischof+Klein’s CleanFlex® packaging produced in Class 5 at-rest cleanrooms. The medical and pharmaceutical sectors dominate demand, with specialized sterilization bags made from Tyvek® for ethylene oxide and water vapor sterilization gaining traction. German companies maintain 100% in-house production for complete traceability, from raw materials to finished products. Sustainability is increasingly a focus, aligning with EU PPWR goals for recyclable and reusable cleanroom packaging solutions. Traceability and documentation capabilities, offering up to 10 years of data, reinforce Germany’s position as a quality-driven market.

China Cleanroom Film and Bags Market Expands with Green Policies and Domestic Innovation

China’s cleanroom film and bags market is propelled by the government’s “dual carbon” initiative, emphasizing green, low-carbon, and circular industrial growth. Regulatory reforms, including the May 30, 2025 “Limit of Harmful Substances of Coatings” standard effective June 1, 2026, enforce stricter controls on hazardous substances, aligning domestic packaging with global safety standards.

Technological advancements, such as AI integration and “5G plus industrial internet,” enhance production efficiency and flexible capacity. Domestic manufacturing is expanding to substitute imported technology, particularly for high-purity films and bags used in semiconductors, electronics, and pharmaceuticals. The growth of China’s semiconductor, electronics, and pharmaceutical industries drives demand for advanced cleanroom packaging, while active R&D and patent development support material innovation and high-performance production methods.

Brazil Cleanroom Film and Bags Market Focused on Sustainability and Advanced Material Solutions

Brazil’s cleanroom film and bags market is guided by the National Solid Waste Policy and new environmental laws, emphasizing material purity, sterility, and documentation. Compliance with ISO Class 5 and 7 cleanroom standards is mandatory, prompting investment in quality control and certification systems.

Technological advancements include high-barrier polymers, improved chemical resistance, and smart additive integration for real-time environmental monitoring. Sustainability is gaining prominence, with companies developing biodegradable and compostable materials while maintaining essential cleanroom properties. The pharmaceutical, medical device, and electronics sectors are key drivers, supported by governmental targets of 30% mandatory recycling in 2025 and 50% by 2040. Corporate initiatives involve investments in heat-sealable bags with superior integrity and incorporation of RFID tags and barcodes for enhanced traceability and efficiency.

South Korea Cleanroom Film and Bags Market Strengthened by High-Performance Films and Sustainability Initiatives

South Korea’s cleanroom film and bags market is shaped by broader government efforts to reduce plastic waste, signaling a shift toward sustainable materials. The country’s biaxially oriented film (BOPP) industry leads in high-purity technical film innovation, supplying optical, electronic, and new energy applications that require ultra-clean packaging.

Focus is on high-performance films and specialty products as local manufacturers compete with Chinese rivals in commodity films. Companies like SK Microworks and Kolon Industries are collaborating to enhance competitiveness in the high-performance segment. Key applications include semiconductor and electronics exports, leveraging South Korea’s leadership in high-purity technical films. Sustainability initiatives, such as APP Group’s aqua-dispersion coatings, demonstrate efforts to replace traditional plastic coatings and support circular packaging practices.

Cleanroom Film and Bags Market Report Scope

Cleanroom Film and Bags Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$10.5 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (Plastic, Paper & Paperboard), By Product Type (Films & Wraps, Bags & Pouches, Tubing, Others), By End-Use Industry (Pharmaceuticals & Biotechnology, Medical Devices, Electrical & Electronics, Aerospace & Defense, Food & Beverages, Others), By Cleanroom Class (ISO Class 5, ISO Class 6, ISO Class 7, ISO Class 8, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Tekni-Plex, Inc., Nelipak Healthcare Packaging, PPC Flexible Packaging, SteriPack, Teknipure, Cleanroom Film and Bags, Inc., Bischof + Klein, Rocaba Packaging Ltd., The Cleanroom Film and Bags, PPC Flexible Packaging LLC, Plitek, DuPont de Nemours, Inc., C-P Flexible Packaging, AeroPackaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cleanroom Film and Bags Market Segmentation

By Material Type

- Plastic

- Paper & Paperboard

By Product Type

- Films & Wraps

- Bags & Pouches

- Tubing

- Others

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Medical Devices

- Electrical & Electronics

- Aerospace & Defense

- Food & Beverages

- Others

By Cleanroom Class

- ISO Class 5

- ISO Class 6

- ISO Class 7

- ISO Class 8

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cleanroom Film and Bags Market

- Amcor plc

- Tekni-Plex, Inc.

- Nelipak Healthcare Packaging

- PPC Flexible Packaging

- SteriPack

- Teknipure

- Cleanroom Film and Bags, Inc.

- Bischof + Klein

- Rocaba Packaging Ltd.

- The Cleanroom Film and Bags

- PPC Flexible Packaging LLC

- Plitek

- DuPont de Nemours, Inc.

- C-P Flexible Packaging

- AeroPackaging

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, research-driven methodology to evaluate the global cleanroom film and bags market, combining primary and secondary sources for a comprehensive view. Primary research includes interviews and consultations with cleanroom packaging manufacturers, material suppliers, medical device and pharmaceutical companies, semiconductor fabricators, and regulatory experts to gain insights into evolving sterility requirements, ESD performance, and traceability expectations. Secondary research involves analysis of company reports, product launches, regulatory frameworks (FDA, EMA, ISO 14644), trade publications, and sustainability disclosures. Market sizing and projections cover material types (plastic, paper & paperboard), product formats (films & wraps, bags & pouches, tubing), end-use industries (pharmaceuticals, biotechnology, medical devices, electronics, aerospace), and ISO-class manufacturing environments. USDAnalytics also evaluates innovations in multilayer blown films, high-barrier polymers, bio-based materials, recycled content integration, cryogenic packaging, and cleanroom automation technologies. By combining regulatory trends, material science advancements, and competitive landscape analysis, USDAnalytics delivers actionable intelligence that guides procurement, operations, and innovation strategies for industry professionals navigating this highly specialized, regulated market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.