Market Overview: Sustainability and E-Commerce Driving Corrugated Box Packaging Growth

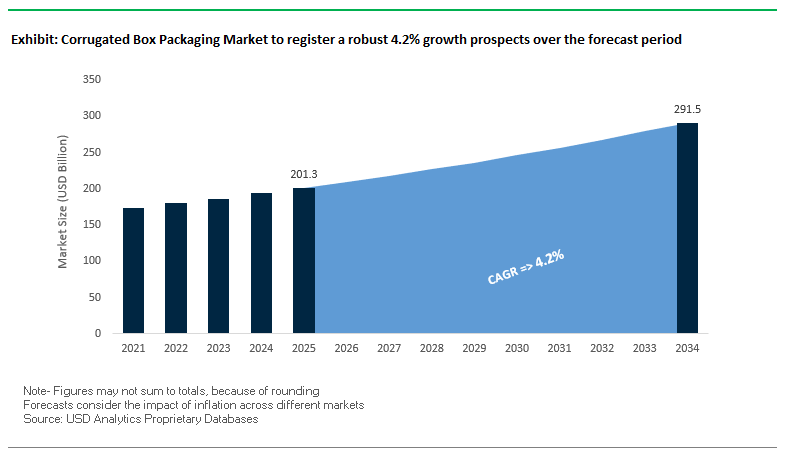

The Global Corrugated Box Packaging Market is valued at USD 201.3 billion in 2025 and is projected to grow to USD 291.5 billion by 2034, registering a CAGR of 4.2%. As the backbone of global logistics and consumer goods distribution, corrugated packaging continues to demonstrate resilience, fueled by rising e-commerce volumes, increased demand from the food and beverage sector, and its inherently sustainable nature. With over 90% recovery rates for old corrugated containers (OCC) in some regions, the industry plays a pivotal role in advancing the circular economy.

E-commerce is the largest growth catalyst, accelerating demand for lightweight corrugated boxes and fit-to-product (FTP) automated systems that minimize material use, reduce void fill, and cut shipping costs. Innovations such as digital printing technology are transforming corrugated packaging into a branding tool for direct-to-consumer businesses, enabling high-quality graphics that elevate the unboxing experience. The sector is also moving towards retail-ready packaging (RRP), helping retailers streamline supply chains by ensuring packaging transitions directly from warehouse to shelf with minimal handling.

Key Insights for Industry Professionals:

- 90%+ recovery rates for OCC underscore strong sustainability performance.

- E-commerce and D2C growth drive demand for fit-to-product automated corrugated boxes.

- Digital printing adoption transforms corrugated into a marketing asset.

- Retail-ready packaging (RRP) enhances supply chain efficiency and shelf visibility.

Market Analysis: Recent Strategic Developments in Corrugated Box Packaging

The corrugated box packaging industry is witnessing active restructuring, acquisitions, and innovation investments across 2025. In August 2025, International Paper announced a strategic pivot, divesting its Global Cellulose Fibers business for USD 1.5 billion while committing USD 250 million to convert an Alabama mill into containerboard production. This move highlights its intensified focus on core corrugated operations. Around the same time, advanced textured and embossed finishes gained traction, offering premium tactile unboxing experiences for e-commerce brands.

In July 2025, a U.S. FMCG major announced a transition to smart corrugated packaging integrating QR codes and NFC tags, reflecting the digitalization of packaging. The same month, the Amcor–Berry Global all-stock merger was finalized, creating a global powerhouse in consumer and dispensing packaging, impacting corrugated indirectly through synergies across material segments. Meanwhile, a June 2025 industry report highlighted a surge in M&A activity, with private equity firms actively targeting paper and corrugated segments.

Operational realignments are equally visible. In June 2025, International Paper announced closures of its Savannah containerboard mill and another packaging facility to streamline operations, reinforcing its cost-leadership strategy. In May 2025, reports noted the growing adoption of fit-to-product (FTP) automated technology in e-commerce, enabling custom-sized boxes to cut waste and logistics costs. Expanding its U.S. presence, Saica Group confirmed a USD 110 million investment in a new corrugated plant in Indiana in March 2025, capable of producing 110+ million m² annually, cementing its footprint in North America.

Key Trends and Emerging Opportunities Reshaping the Corrugated Box Packaging Market

Strategic Investment in High-Margin, Automated Performance Packaging

A defining trend in the corrugated box packaging market is the shift from commodity-grade boxes to high-performance, automated, and retail-ready packaging formats. Leading players are making significant capital investments in advanced manufacturing technologies to meet the rising demand from e-commerce and retail brands for shelf-ready and branding-enhanced corrugated solutions. Unlike standard boxes, these performance-engineered formats are designed to function as mobile billboards and enhance the consumer’s unboxing experience while also improving supply chain efficiency. Companies are rolling out fit-to-product (FTP) and box-on-demand systems, which eliminate the need for large inventories of standard-sized boxes and reduce filler use. This aligns with both cost reduction and sustainability goals for brand owners. For instance, one global packaging leader has launched a portfolio of shelf-ready corrugated packaging that integrates premium graphics and innovative structural designs, enabling products to be directly placed on retail shelves. This trend is carving out a high-margin product category, positioning corrugated box suppliers as value-driven partners who provide differentiation and efficiency, not just protective containers.

Rapid Adoption of AI and Machine Learning for Supply Chain Optimization

Another powerful trend driving the corrugated packaging industry is the rapid adoption of AI and machine learning to optimize supply chains. Beyond manufacturing efficiency, suppliers are offering AI-powered value-added services, including right-sizing packaging, pallet optimization, and predictive demand forecasting. Academic research has shown that AI-driven “right-size” algorithms can significantly cut material usage and improve shipping density, directly tackling the costly issue of shipping “air” in oversized packages. AI-enabled design tools are also accelerating the development of custom-fit and aesthetically appealing packaging by automating structural and graphic prototyping. This transforms packaging suppliers into strategic supply chain partners who help brands minimize waste, reduce logistics costs, and meet carbon reduction targets. Importantly, the rise of AI is forging new partnerships between packaging converters and technology providers, creating a more data-driven, transparent, and efficient value chain. The result is a corrugated packaging ecosystem that not only supports operational efficiency but also strengthens customer loyalty through smart, sustainable packaging design.

Development of Advanced Coatings for Recyclability in Challenging Applications

A significant growth opportunity for the corrugated box packaging market lies in the development of advanced barrier coatings that maintain recyclability while protecting contents from grease, oil, and moisture. Traditional coatings such as wax or polyethylene films hinder recycling, making boxes incompatible with standard repulping systems. In response, material scientists and packaging innovators are developing water-borne and repulpable barrier coatings that deliver both functionality and sustainability. For example, a chemical company has launched a 100% recyclable coating solution that provides oil and grease resistance while remaining fully compatible with paper recycling streams. R&D efforts are also focusing on application-specific coatings tailored to diverse product requirements such as high-fat foods versus low-moisture goods expanding the versatility of corrugated packaging in food, retail, and industrial sectors. As brands increasingly commit to sustainable, single-material packaging, suppliers who can deliver certified high-performance recyclable solutions will secure a competitive edge and open lucrative revenue streams in premium segments of the corrugated market.

Expansion of Integrated “Box-to-Box” Closed-Loop Recycling Systems

The expansion of closed-loop recycling models presents another transformative opportunity for corrugated box manufacturers. E-commerce and retail giants are seeking partners to implement regional “box-to-box” circular systems, where used corrugated boxes are collected, pulped, and remanufactured into new boxes within the same geography. This shortens the recycling loop, reduces transportation emissions, secures raw fiber supply, and demonstrates a tangible commitment to sustainability. Some packaging companies are already leading this shift by establishing customer-centric recycling programs that collect OCC (old corrugated containers) directly from retail and distribution centers to create new boxes. The benefits extend across the value chain brand owners reduce reliance on virgin materials, recyclers cut logistics inefficiencies, and converters gain a steady fiber input stream in a volatile raw materials market. However, realizing this opportunity requires strong collaboration between packaging producers, waste management firms, and retail partners, alongside investment in localized recycling infrastructure. Companies that successfully scale box-to-box circularity will not only reduce their environmental footprint but also reinforce their market positioning as leaders in sustainable corrugated packaging solutions.

Competitive Landscape: Leading Companies in Corrugated Box Packaging

The corrugated box packaging sector is consolidated among a few global leaders and expanding regional players, with strategies centered on sustainability, capacity expansion, and technology-driven solutions.

International Paper Company streamlines portfolio and focuses on containerboard

International Paper, reinforced by its acquisition of DS Smith, remains the global leader in fiber-based packaging. In August 2025, it announced the divestiture of non-core cellulose fibers and a USD 250 million investment in Alabama containerboard production. Earlier in July 2025, it divested five European corrugated plants to comply with regulatory conditions. With exploration underway for a new sustainable facility in Utah, International Paper is committed to streamlined operations and sustainable corrugated growth.

Smurfit Kappa Group PLC strengthens scale through merger with WestRock

As part of Smurfit WestRock, formed in October 2024, Smurfit Kappa leverages unmatched geographic and product diversity. The company specializes in everything from shipping containers to high-graphic POS displays, offering circular packaging solutions globally. In 2025, Smurfit Kappa has invested in mill expansions and corrugator upgrades, positioning itself as a leader in sustainable e-commerce and retail-ready packaging.

WestRock drives innovation in AI-enabled and sustainable corrugated solutions

Now operating under Smurfit WestRock, WestRock contributed deep expertise in materials science, packaging design, and automation. Its Box On Demand technology and AI-driven process improvements continue to help customers optimize packaging. With a focus on replacing plastic and enhancing recyclability, WestRock’s legacy innovations in moisture- and grease-resistant corrugated solutions remain integral to the combined portfolio.

DS Smith PLC integrates into International Paper’s global network

Previously a leader in retail-ready and display packaging, DS Smith has now been integrated into International Paper’s operations. By 2024, it had exceeded its 2025 target of eliminating 1B pieces of plastic, showcasing its circular design expertise. Its strength lies in customized corrugated solutions that improve retail efficiency and consumer engagement. DS Smith’s legacy of circular design metrics and sustainability-driven innovation is now reinforcing International Paper’s global ambitions.

Saica Group expands North American footprint with Indiana investment

Saica, a European leader with strong recycling capabilities, has accelerated its U.S. growth strategy. In March 2025, it invested USD 110 million in a new corrugated plant in Indiana, with capacity exceeding 110 million m² annually. Known for its recycled containerboard production and certifications for environmental performance, Saica is building a sustainable U.S. value chain supported by rail connectivity to cut logistics costs. Its strategy emphasizes circular economy leadership and international expansion.

Corrugated Box Packaging Market Share Insights

Slotted Containers Retain Market Share Leadership by Box Type in Corrugated Packaging

Regular Slotted Containers (RSCs) hold an overwhelming 55% share of the corrugated box packaging industry, a position rooted in unmatched efficiency, strength, and universality. Their standardized design delivers cost advantages, fast production, and broad adaptability, making them the default solution across logistics, retail, and e-commerce channels. This segment benefits heavily from digital printing and high-performance board grade innovation, which enhance both branding and functionality. While die-cut boxes and premium formats gain traction in retail and specialty markets, slotted containers remain indispensable for bulk logistics and last-mile delivery, particularly as global e-commerce volumes surge. Their market leadership illustrates how functional utility continues to outweigh premiumization in the corrugated space, despite rising sustainability and branding pressures.

E-commerce Dominates Market Share by End-Use Industry in Corrugated Box Packaging

E-commerce represents the largest and fastest-growing end-use segment in corrugated packaging, commanding approximately 35% of the market. Its dominance is structural, tied to the exponential growth of online retail and the operational demands of last-mile delivery. Corrugated packaging in this segment must balance durability, right-sizing, and brandability to minimize shipping damage, reduce void fill, and deliver an engaging "unboxing experience." Major retailers and marketplaces are driving demand for automated packaging solutions that optimize box size and reduce waste, while sustainability mandates push for recyclable adhesives, inks, and water-based coatings. As consumer expectations evolve, corrugated packaging in e-commerce is no longer just a logistics function but also a frontline branding and sustainability tool, securing its top market position.

United States Corrugated Box Packaging Market Accelerates Through EPR Regulations and Automation

The United States corrugated box packaging market is heavily shaped by a fragmented regulatory environment, with state-level Extended Producer Responsibility (EPR) bills driving manufacturers toward highly recyclable materials. Automation and robotics are transforming production lines, enabling companies to meet the surging e-commerce demand for just-in-time deliveries. Strategic investments, such as McKinley Packaging’s 500,000-square-foot facility in Lancaster, Texas, underscore the expansion of production capacities to serve growing online retail and home delivery sectors.

Corrugated boxes dominate applications in food and beverage, home goods, and e-commerce, supported by high sustainability standards. With a recycling rate of 91.4% for old corrugated containers (OCC) in 2021, the U.S. market exemplifies a circular economy model. Innovation in functionality is notable, including solutions like Graphic Packaging International’s KeelClip multi-packing system, providing recyclable alternatives to plastic rings. Additionally, consumer demand for customized and diversified box sizes is fueling product innovation, improving shipping efficiency and positioning corrugated boxes as a sustainable and versatile alternative to flexible mailers.

Germany Corrugated Box Packaging Market Thrives on Circular Economy Leadership and Industry 4.0

Germany’s corrugated box packaging market operates under stringent regulations, including the Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. These frameworks mandate fully recyclable or reusable packaging by 2030 and set specific recycled content standards, accelerating the adoption of corrugated boxes as a green solution. The country’s near-90% recycling rate further propels demand, positioning corrugated materials as a preferred choice for environmentally conscious consumers.

Technological innovation is driving efficiency and high-performance solutions, with machinery capable of producing sustainable corrugated boards in demand. Digitalization initiatives under “Plattform Industrie 4.0” integrate IoT and cyber-physical systems into manufacturing processes, enhancing productivity and supply chain optimization. Key applications in food and beverage, as well as retail, reflect Germany’s preference for high-end, aesthetically appealing packaging. Corrugated boxes are increasingly adopted for fine foods and artisanal products, highlighting Germany’s dual focus on sustainability and premium packaging functionality.

China Corrugated Box Packaging Market Expands Amid Green Transformation and Domestic Manufacturing Focus

China’s corrugated box packaging market is benefiting from the government’s “dual carbon” goals and the 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement. Regulatory reforms targeting excessive packaging, including layer and void ratio limitations, are directly impacting manufacturers serving food and cosmetics sectors. Integration of automation, AI, and “5G plus industrial internet” technologies is enhancing production efficiency and flexibility, enabling manufacturers to scale rapidly.

Domestic substitution of imported technologies is a key trend, with local companies expanding capacity to meet growing domestic demand for high-quality, circular packaging. The market is strongly supported by the rapid growth of e-commerce, fresh food, and food delivery industries, with platforms like Alibaba and JD.com promoting eco-friendly packaging solutions. High levels of research and development, evidenced by a significant number of patents, ensure that China remains a leader in packaging innovation and sustainable corrugated box solutions.

India Corrugated Box Packaging Market Boosted by Government Incentives and E-Commerce Growth

India’s corrugated box packaging market is supported by government initiatives, including Plastic Waste Management Rules and EPR requirements mandating 30% recycled content by 2025. In September 2025, the government reduced GST on corrugated paper and boxes to 5%, expected to increase affordability and stimulate demand across e-commerce and MSME sectors. Corporate investments, such as JPFL Films’ capital expenditure of over INR 700 crore for new BOPP, PET, and CPP lines, reflect a strong growth push in flexible and corrugated packaging segments.

Automation adoption is rising, with innovative solutions like plastic-free laminate films for lamination with paper and foil. Rapid growth in e-commerce, food and beverage, and pharmaceuticals is driving demand for high-quality corrugated boxes. Strategic partnerships like the CIRCLE Alliance, backed by Unilever, USAID, and EY with USD 21 million, promote circular packaging and reduce plastic waste. Expanding food processing sectors, particularly ready-to-drink beverages and processed foods, further fuel demand for sustainable and functional corrugated packaging in India.

Brazil Corrugated Box Packaging Market Expands Through Sustainability Initiatives and Strategic Investments

Brazil’s corrugated box packaging market is strongly influenced by the National Solid Waste Policy and new regulations banning single-use disposable items, with a 2030 target for fully compostable or recyclable packaging. Adoption of robotics and AI in production processes is enhancing operational efficiency and quality control. Innovations in biodegradable films, such as carboxymethyl cellulose (CMC) from sugarcane bagasse, are contributing to the growth of eco-friendly corrugated solutions.

Corporate investments, including Smurfit Westrock’s R$840 million expansion in Santa Catarina and Klabin’s BRL 188 million investment in Ceará, are increasing production capacity for sustainable corrugated boards. Key applications include food and beverage and cosmetics, with the expanding food processing industry driving demand for advanced packaging solutions. Corrugated boxes are emerging as an eco-friendly alternative to plastic mailers and foam-based packaging, aligning with Brazil’s sustainability initiatives and consumer preference for environmentally responsible packaging.

Corrugated Box Packaging Market Report Scope

Corrugated Box Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$201.3 Billion

|

|

Market Size (2034)

|

$291.5 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Box Type (Slotted Containers, Die-cut Boxes, Telescope Boxes, Folder Boxes), By Flute Type (Single Face, Single Wall, Double Wall, Triple Wall), By End-Use Industry (Food & Beverages, E-commerce, Home & Personal Care, Electronics, Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group plc, DS Smith plc, Mondi Group, Packaging Corporation of America (PCA), Cascades Inc., Oji Holdings Corporation, Shandong Century Sunshine Paper Group Co., Ltd., Rengo Co., Ltd., Georgia-Pacific LLC, Klabin S.A., Billerud AB, Greif, Inc., Allied Corrugated Box Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Box Packaging Market Segmentation

By Box Type

- Slotted Containers

- Die-cut Boxes

- Telescope Boxes

- Folder Boxes

By Flute Type

- Single Face

- Single Wall

- Double Wall

- Triple Wall

By End-Use Industry

- Food & Beverages

- E-commerce

- Home & Personal Care

- Electronics

- Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Box Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group plc

- DS Smith plc

- Mondi Group

- Packaging Corporation of America (PCA)

- Cascades Inc.

- Oji Holdings Corporation

- Shandong Century Sunshine Paper Group Co., Ltd.

- Rengo Co., Ltd.

- Georgia-Pacific LLC

- Klabin S.A.

- Billerud AB

- Greif, Inc.

- Allied Corrugated Box Co.

* List Not Exhaustive

Methodology

The Corrugated Box Packaging Market study by USDAnalytics has been conducted using a robust methodology that combines both primary and secondary research to deliver actionable insights for industry professionals. Primary research involved interviews with key stakeholders, including corrugated box manufacturers, converters, brand owners, sustainability experts, and regulatory authorities, to capture trends, challenges, and strategic priorities. Secondary research included company annual reports, press releases, government regulations, patent filings, industry journals, and trade associations to validate market dynamics and historical developments. Quantitative analysis was applied to assess market size, growth forecasts, and segmentation by box type, flute type, and end-use industry, while qualitative assessment examined emerging technologies, automation, AI integration, digital printing, and circular economy initiatives. USDAnalytics also evaluated M&A activity, sustainability adoption, retail-ready packaging innovations, and supply chain optimization strategies to ensure a holistic understanding of global competitive landscape, investment opportunities, and future market trajectories.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.