Market Overview: Durability and Reusability Define Corrugated Plastic Packaging

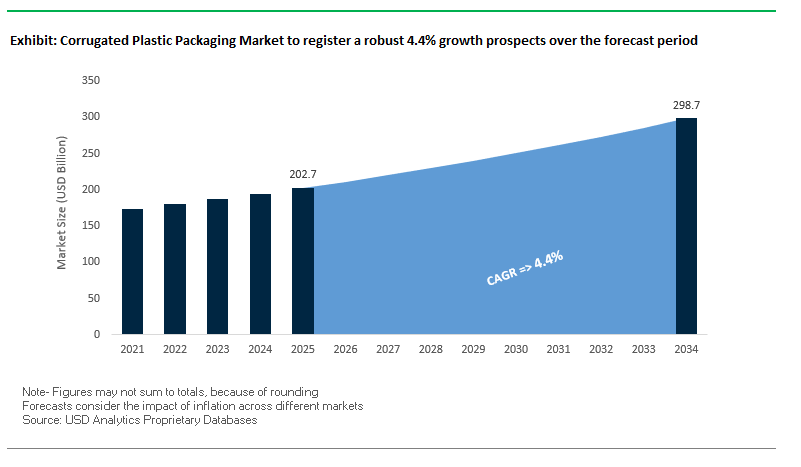

The Global Corrugated Plastic Packaging Market is projected to reach USD 202.7 billion in 2025 and grow to USD 298.6 billion by 2034, expanding at a CAGR of 4.4%. This market segment is increasingly recognized for its durability, moisture resistance, and reusability, offering a sustainable and long-lasting alternative to traditional corrugated fiberboard. Made primarily from polypropylene sheets (often branded as Coroplast), corrugated plastic has become a preferred choice for industries requiring robust packaging solutions that align with circular economy models.

Over 55% of industrial packaging applications now use corrugated plastic sheets due to their ability to withstand multiple cycles of use, drastically reducing waste compared to single-use cardboard. The food and e-commerce sectors are accelerating adoption, as reusable and moisture-resistant packaging reduces spoilage and improves reliability in transit. At the same time, UV-resistant corrugated sheets are witnessing 50% growth in outdoor commercial applications such as signage, point-of-purchase displays, and event branding. A notable innovation trend is the integration of RFID tags and embedded sensors for real-time tracking and extended reuse cycles, enhancing efficiency and visibility across global supply chains.

Key Insights for Industry Professionals:

- 55% of industrial packaging now relies on corrugated plastic sheets for reusability.

- E-commerce and food sectors drive demand for moisture-resistant and durable alternatives.

- Outdoor advertising adoption up 50% with UV-resistant corrugated plastics.

- Smart packaging integration (RFID, sensors) strengthens supply chain visibility.

Market Analysis: Recent Developments in Corrugated Plastic Packaging

The corrugated plastic packaging sector has seen a surge of strategic investments, partnerships, and product innovations in 2025, underscoring its growing importance in industrial, automotive, and consumer supply chains. In August 2025, reports highlighted strong adoption of corrugated plastic in automotive and industrial logistics, where durability and part protection are critical. That same month, Avery Dennison expanded its RFID inlay portfolio, designed for integration with corrugated plastics, enabling greater read range and real-time supply chain tracking.

The industry is also consolidating through mergers and acquisitions. In July 2025, the Amcor–Berry Global merger was finalized, creating a packaging giant with increased scope for sustainable and specialty packaging solutions. In parallel, Inteplast Group marked its first European expansion by acquiring German film producer Perga, strengthening its ability to serve diverse corrugated plastic applications globally. By June 2025, reports confirmed a 35% surge in polypropylene-based corrugated boards over the last five years, signaling sustained demand growth driven by resilience, water resistance, and lightweight attributes.

Strategic alliances and competitive pressures are reshaping the market landscape. In April 2025, Schoeller Allibert merged with IPL, creating a USD 1.4 billion global leader in reusable plastic packaging, enhancing capabilities in logistics and consumer packaging. Also in April, DS Smith introduced a 100% recyclable cooler from wax-free corrugated board as a direct competitor to plastic coolers, showcasing increasing competition between fiber-based and plastic-based reusable packaging. Earlier, in February 2025, DS Smith’s consumer research revealed that U.S. buyers are willing to pay a premium for intelligent and sustainable packaging, a demand trend that equally benefits corrugated plastics and high-performance fiber alternatives.

Emerging Trends and Strategic Opportunities in the Corrugated Plastic Packaging Market

Strategic Shift Towards High-Performance Recyclable Materials

A decisive trend in the corrugated plastic packaging market is the pivot toward recyclable mono-material polypropylene (PP) structures. This shift addresses the rising demand from both regulators and brand owners for packaging that seamlessly integrates into recycling systems without sacrificing durability or barrier properties. Europe’s extended producer responsibility (EPR) frameworks and circular economy directives are central to this trend, pushing manufacturers to innovate with PP solutions that can meet demanding performance criteria while supporting full recyclability.

Leading companies are already embedding 30–70% recycled content into corrugated PP sheets while maintaining structural integrity. Closed-loop programs, such as in-house take-back systems that reintegrate clean production scraps into new products, highlight the market’s progression toward circular manufacturing. In addition, R&D has yielded recyclable mono-material barrier packaging rated “AAA” with recyclability above 95%, proving that performance and sustainability can coexist. For manufacturers, this represents not only regulatory compliance but also a significant growth avenue, as brands with aggressive sustainability pledges seek durable, recyclable, and mono-material packaging to meet public commitments.

Integration of Advanced Automation and Digital Printing for Mass Customization

Digital printing and automated fabrication are transforming corrugated plastic packaging into a tool for personalized branding and agile supply chains. Unlike traditional printing, digital systems enable short-run, high-quality customization with complex graphics, QR codes, and serialized data crucial for direct-to-consumer (DTC) brands and e-commerce operators prioritizing customer experience.

Companies investing in AI-driven “Box on Demand” solutions are already producing made-to-fit packaging that reduces shipping costs and material waste. When combined with digital printing on corrugated plastic, these technologies allow brands to achieve flexible, on-demand customization without tooling delays or excessive inventory. This trend strengthens supply chain agility by allowing businesses to respond quickly to shifting consumer preferences and regional promotional campaigns. Moreover, the ability to provide mass customization at scale positions corrugated plastic packaging as a premium solution for industries seeking both protection and brand engagement, particularly in e-commerce, electronics, and FMCG sectors.

Development of Chemical Recycling-Compatible Material Streams

A major opportunity exists in engineering corrugated plastic packaging specifically for chemical recycling pathways, where polymers like polypropylene are broken down into virgin-quality feedstocks. Unlike mechanical recycling, which is limited by contamination and multi-layer complexity, chemical recycling can recover material from waste streams that would otherwise be landfilled.

The European plastics industry has announced €8 billion in investments by 2030 to expand chemical recycling capacity, highlighting its strategic importance for achieving circularity. By designing packaging optimized for this process, manufacturers can ensure their products have higher end-of-life value and meet ambitious recycling targets set by the EU and global governments. This shift will also foster new collaborations across the value chain uniting packaging manufacturers, chemical companies, and waste management firms into closed-loop ecosystems where packaging is no longer waste but a reusable resource.

Expansion into Reusable Transport Packaging (RTP) for Closed-Loop Logistics

The durability of corrugated plastic positions it as a strong candidate for Reusable Transport Packaging (RTP) systems, particularly for high-volume industries such as automotive, electronics, and fresh produce. RTP leverages corrugated plastic’s lightweight strength and reusability to create asset-tracked containers that can be sanitized, returned, and reused dozens or even hundreds of times.

Packaging providers are already offering reusable corrugated plastic trays and boxes with customized foam fitments for secure product transport. The economic value proposition is clear: RTP systems reduce the long-term cost of distribution packaging while lowering waste generation. With lifecycle reusability, distribution costs per trip fall below those of single-use alternatives, delivering measurable savings to large enterprises.

Competitive Landscape: Leading Companies in Corrugated Plastic Packaging

The corrugated plastic packaging industry is dominated by global players focusing on reusability, circularity, and performance innovation while strategically expanding across regions.

Inteplast Group expands global reach with Perga acquisition

Inteplast Group, through its IntePro and Coroplast brands, is a leading supplier of corrugated plastic sheets in North America. Its portfolio spans industrial packaging, signage, and reusable transport solutions. In July 2025, the company acquired Perga, marking its first European expansion and reinforcing its global footprint. With a focus on reusable, lightweight, and moisture-resistant packaging, Inteplast emphasizes sustainable production and integration across industries including automotive, food, and consumer goods.

Schoeller Allibert strengthens leadership with IPL merger

Schoeller Allibert is a European leader in returnable transit packaging (RTP) solutions. In April 2025, it merged with IPL, creating a USD 1.4 billion global leader in reusable plastic packaging. The company’s strength lies in sourcing a significant portion of its materials from recycled plastics, surpassing its 2026 targets ahead of schedule. Schoeller’s expertise in circular logistics solutions positions it as a preferred partner for corporations seeking to reduce packaging waste and carbon footprints.

DS Smith introduces fiber-based alternatives to compete with corrugated plastic

Although primarily fiber-focused, DS Smith remains a major competitor in sustainable packaging. In April 2025, it launched a 100% recyclable cooler made from corrugated board, directly targeting applications dominated by corrugated plastic. Now integrated into International Paper, DS Smith continues to drive circular economy strategies, with its “Now and Next” program ensuring designs prioritize recyclability, reuse, and plastic substitution. Its strength lies in sustainable innovation that competes head-to-head with plastic solutions.

Sealed Air transitions toward substrate-agnostic protective packaging

Sealed Air is a global leader in protective packaging with brands like LIQUIBOX® and Bubble Wrap®. The company is undergoing a business transformation with a focus on e-commerce, fresh food, and industrial packaging. Its strategy emphasizes becoming substrate agnostic, offering protective solutions across plastic, fiber, and hybrid materials. Sealed Air is optimizing its manufacturing footprint to enhance cost efficiency while advancing high-performance, sustainable protective packaging formats that complement corrugated plastic applications.

Corrugated Plastic Packaging Market Share Insights

Boxes & Containers Lead Market Share by Product Type in Corrugated Plastic Packaging

Boxes and containers dominate with 40% of the corrugated plastic packaging market, reflecting their pivotal role as reusable workhorses in supply chains requiring durability and extended life cycles. Unlike traditional corrugated paper, polypropylene-based plastic boxes withstand repeated trips, resist water, oils, and chemicals, and maintain structural integrity under harsh handling conditions. Their market leadership is most evident in closed-loop logistics systems in automotive, agriculture, and industrial manufacturing, where cost savings from reuse outweigh higher upfront costs. Increasing emphasis on circular packaging systems and corporate sustainability goals further consolidates their share, as businesses replace single-use packaging with rugged reusable formats that align with waste reduction mandates.

Industrial Sector Dominates Market Share by End-Use in Corrugated Plastic Packaging

The industrial segment holds the largest share at 35% of corrugated plastic packaging consumption, cementing its position as the sector’s core application. The demand is driven by heavy-duty material handling, protective sheets for equipment, and reusable totes optimized for factory and warehouse workflows. Corrugated plastic’s resilience against moisture and chemicals, combined with its ability to be sanitized and reused, makes it the preferred solution for cost-sensitive industries managing high-value goods under demanding conditions. Its stronghold is reinforced by industries shifting toward returnable transport packaging (RTP) to reduce overall packaging waste and operating costs. As global manufacturing expands, industrial users will remain the most consistent adopters of corrugated plastic packaging.

United States Corrugated Plastic Packaging Market Accelerates Through EPR Regulations and Reusable Solutions

The United States corrugated plastic packaging market is heavily shaped by a fragmented regulatory landscape, with state-level Extended Producer Responsibility (EPR) bills compelling manufacturers to focus on highly recyclable and reusable materials. Technological advancements are driving innovations in returnable packaging systems made from durable corrugated plastic, capable of multiple reuse cycles, reducing waste and transportation costs for industries such as automotive, electronics, and agriculture.

Corporate investments underscore this expansion, with major packaging firms investing millions in facilities dedicated to high-performance corrugated plastic products tailored for specialized shipping needs. Key applications span the automotive, logistics, and agricultural sectors, particularly through reusable plastic containers (RPCs) and protective sheets for fresh produce. Sustainability is at the forefront, with corrugated plastic offering a closed-loop solution that minimizes solid waste and lowers carbon footprints. Functional innovations, such as anti-static sheets for electronics and UV-resistant panels for outdoor use, further enhance market adoption across diverse industries.

Germany Corrugated Plastic Packaging Market Strengthened by Circular Economy Leadership and Industrie 4.0

Germany’s corrugated plastic packaging market operates under a strict regulatory framework, including the Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. These regulations mandate fully recyclable or reusable packaging by 2030, with requirements for recycled content, driving demand for reusable corrugated plastic solutions aligned with the circular economy. Germany’s well-established Extended Producer Responsibility (EPR) system further encourages innovation in returnable packaging and material transparency.

Technological innovation is a key growth driver, with new machinery and digital product passports enhancing recyclability and traceability. The market is particularly strong in automotive, logistics, and retail sectors, where reusable corrugated plastic containers facilitate efficient in-plant and inter-plant transport. Integration of digitalization and automation under “Plattform Industrie 4.0” enhances production efficiency and supply chain optimization, meeting demand for faster, sustainable delivery systems. Corporate adoption of advanced packaging solutions aligns with Germany’s focus on efficiency, sustainability, and high-performance logistics.

China Corrugated Plastic Packaging Market Expands Amid Green Transformation and Domestic Manufacturing Drive

China’s corrugated plastic packaging market is benefiting from the government’s “dual carbon” initiatives and the 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement, promoting recycling and sustainable material use. Regulatory reforms, effective September 2023, impose limits on packaging layers and void ratios, complemented by the State Post Bureau’s directive for express delivery companies to prioritize reusable and eco-friendly packaging.

Technological advancements, including automation, AI, and integration of “5G plus industrial internet,” are optimizing production efficiency and flexible manufacturing capacity. Domestic substitution of imported technology is driving local capacity expansions, meeting growing demand for high-quality, circular packaging. Key applications include e-commerce, fresh food, and automotive industries, with companies leveraging lightweight, reusable corrugated plastic solutions to meet sustainability goals and enhance product protection. The market is also witnessing significant innovation through local R&D in advanced, reusable packaging materials.

Brazil Corrugated Plastic Packaging Market Grows Through Regulatory Support and Technological Investments

Brazil’s corrugated plastic packaging market is strongly influenced by the National Solid Waste Policy and new laws targeting single-use disposable items, with a 2030 deadline for fully recyclable or compostable packaging. The adoption of robotics and artificial intelligence in production enhances efficiency and quality control, while the development of biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse supports eco-friendly packaging trends.

Corporate investments are increasing to meet rising local demand, particularly in logistics, agriculture, and food sectors. Key applications include reusable containers for automotive parts and protective packaging for food processing, aligning with Brazil’s sustainability agenda. Corrugated plastic is emerging as an eco-friendly alternative to single-use foam-based solutions, offering durability, reusability, and reduced environmental impact. The market’s rapid growth is fueled by the convergence of technological innovation, corporate investments, and strong regulatory support for sustainable packaging practices.

Corrugated Plastic Packaging Market Report Scope

Corrugated Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$202.7 Billion

|

|

Market Size (2034)

|

$298.6 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Material Type (Polypropylene, Polyethylene, Other Resins), By Product Type (Boxes & Containers, Sheets, Dividers & Partitions, Totes), By End-Use Industry (Automotive, Industrial, Food & Beverages, Electronics, Building & Construction, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DS Smith plc, Coroplast LLC, Prima Industrie S.p.A., Linyi Jinhai Corrugated Plastic Co., Ltd., American Container Corporation, Corex Plastics Australia, Karton s.p.a., Plasticor LLC, Shandong Jingyi Corrugated Plastic Co., Ltd., Oji Holdings Corporation, Pactiv Evergreen Inc., Great American Packaging, Twinplast Ltd., B&B Triplewall Containers Ltd., Allied Corrugated Box Co.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Plastic Packaging Market Segmentation

By Material Type

- Polypropylene

- Polyethylene

- Other Resins

By Product Type

- Boxes & Containers

- Sheets

- Dividers & Partitions

- Totes

By End-Use Industry

- Automotive

- Industrial

- Food & Beverages

- Electronics

- Building & Construction

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Plastic Packaging Market

- DS Smith plc

- Coroplast LLC

- Prima Industrie S.p.A.

- Linyi Jinhai Corrugated Plastic Co., Ltd.

- American Container Corporation

- Corex Plastics Australia

- Karton s.p.a.

- Plasticor LLC

- Shandong Jingyi Corrugated Plastic Co., Ltd.

- Oji Holdings Corporation

- Pactiv Evergreen Inc.

- Great American Packaging

- Twinplast Ltd.

- B&B Triplewall Containers Ltd.

- Allied Corrugated Box Co.

* List Not Exhaustive

Methodology

The Corrugated Plastic Packaging Market study conducted by USDAnalytics employs a comprehensive research methodology combining both primary and secondary data sources to provide an authoritative view for industry professionals. Primary research involved interviews with key stakeholders, including corrugated plastic manufacturers, packaging converters, brand owners, supply chain managers, and sustainability experts, capturing market dynamics, adoption trends, and strategic priorities. Secondary research drew on company annual reports, press releases, regulatory filings, patent databases, industry journals, and trade publications to validate market size, growth projections, and competitive developments. Quantitative analysis assessed market valuation, CAGR, and segmentation by material type, product type, and end-use industry, while qualitative analysis explored innovations such as reusable transport packaging (RTP), chemical recycling-compatible materials, automation, AI-driven Box-on-Demand solutions, and smart packaging integration with RFID and sensors. USDAnalytics also evaluated M&A activity, regional regulatory frameworks, and circular economy initiatives to deliver a holistic perspective on global market trends, emerging opportunities, and future growth trajectories.

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.