Defoamers and Defoaming Agents Market in Water and Wastewater Processing: Industry Growth Analysis and Value Forecast to 2034

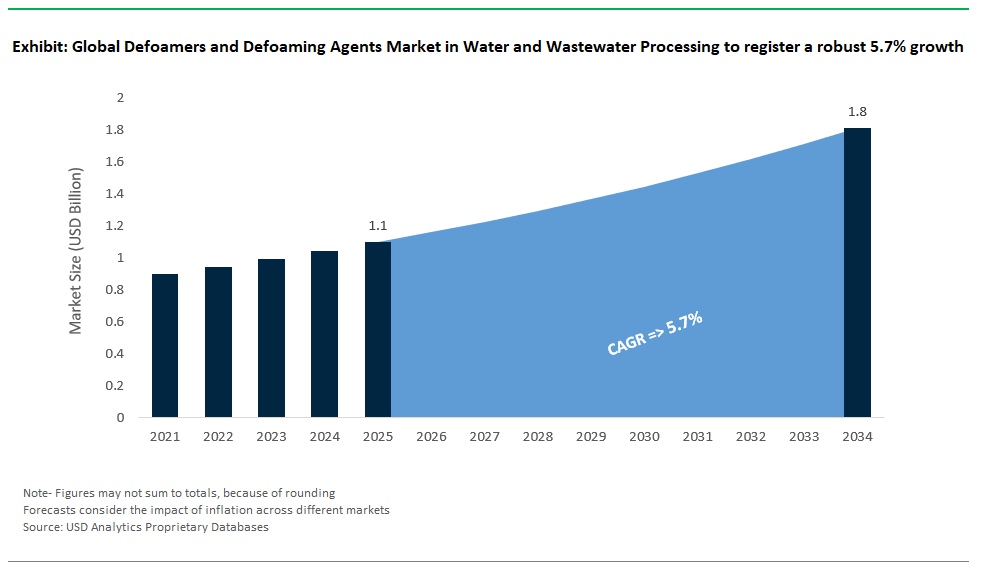

The defoamers and defoaming agents market in water and wastewater processing market is valued at $1.1 billion in 2025 and projected to reach $1.8 billion by 2034, reflecting a CAGR of 5.7%. This market is a critical enabler of process stability across diverse sectors from pulp and paper to high-temperature boiler systems where foam formation compromises throughput, contaminates product streams, and destabilizes biological treatment units. The market is primarily divided between silicone-based and non-silicone formulations, each with distinct performance profiles. Silicone emulsions, widely adopted for their rapid foam knockdown, can achieve complete foam collapse in under 10 seconds at dosing levels between 1–100 ppm, in line with TAPPI standards, making them indispensable in high-velocity fluid systems such as pulp washers and filtration loops.

On the other hand, non-silicone defoamers especially polyglycol-based blends are increasingly preferred in applications requiring biodegradability, with favorable BOD₅/COD ratios exceeding 0.5 per OECD 301D criteria. This positions them as the default choice in environmentally sensitive discharges and food-adjacent processing. In wastewater operations, particularly biological systems like activated sludge, persistent surface foam can disrupt aeration and solids separation.

For high-temperature applications such as boilers exceeding 200°C, thermal stability becomes a limiting factor, necessitating defoamers with flash points above 250°C as required under ASME Section VII. This has pushed formulators to develop hybrid agents that combine high-temperature resistance with low surface tension and minimal emulsification. With operational reliability, environmental compliance, and thermal compatibility all driving purchasing decisions, the defoamer market is transitioning from commodity products to engineered chemical solutions tailored for process-specific thresholds. Suppliers who can deliver targeted performance under variable pH, temperature, and surfactant load conditions are gaining traction across both legacy industries and emerging water reuse systems.

Sustainability and Process Optimization Reshape the Defoamers and Defoaming Agents Market in Water and Wastewater Processing

Market Trend: Rise of Silicone-Free and Bio-Based Defoamers Driven by Ecolabel Compliance and Operational Performance

The defoamers and defoaming agents market in water and wastewater treatment is undergoing a rapid shift away from traditional silicone-based formulations toward plant-derived, biodegradable, and process-optimized alternatives. This transformation is fueled by tightening environmental regulations, sludge disposal concerns, and escalating demand for defoamers that do not interfere with downstream biological or filtration processes. Leading chemical manufacturers are responding with high-performance bio-based solutions. BASF’s Foamaster® BIO, formulated with rapeseed oil esters, has delivered 90% foam reduction in municipal anaerobic digesters while complying with EU Ecolabel toxicity and biodegradability benchmarks enabling safer sludge handling and enhanced biogas productivity. In industrial effluents, Kemira’s BioFoamX, derived from lignin waste streams, has demonstrated dual-functionality by not only controlling foam but also reducing COD in pulp and paper processing, enhancing compliance with effluent discharge norms. In parallel, the advent of smart dosing systems such as Evoqua’s FoamSense AI operational in Coca-Cola's wastewater facilities has enabled real-time adjustment of defoamer dosage based on optical monitoring of foam height, leading to a reduction in chemical use and enhanced process stability. These developments signal a fundamental market realignment: buyers seek defoamers that are not only effective in extreme foaming conditions but also compatible with membrane systems, ZLD targets, and sludge valorization strategies. With plant-based defoamers proving more cost-effective than silicone emulsions, and international paper mills reporting higher throughput under non-silicone regimes, green and precision-controlled defoaming is becoming a critical component of modern water treatment infrastructure.

Market Opportunity: High-Temperature and Complex Industrial Effluents Drive Demand for Specialized, Non-Silicone Defoamers

A substantial growth opportunity in the defoamers market lies in high-temperature, chemically complex industrial wastewater streams particularly from the textile, landfill, and biopharma sectors where conventional silicones fail due to emulsification, membrane fouling, or regulatory constraints. In the textile sector, where dyeing operations can exceed 90°C, Archroma’s polyether-polyester-based formulation, is delivering stable defoaming in harsh thermal and surfactant-laden environments while saving in operational costs. India’s growing network of textile parks under Zero Liquid Discharge (ZLD) mandates further accelerates demand for defoamers compatible with ultrafiltration and reverse osmosis, where silicone carryover can impair membrane performance.

In landfill leachate treatment, where anaerobic digestion of protein-rich organic loads causes chronic foaming, mineral oil-free formulation demonstrate an increase in biogas yield by stabilizing digester conditions addressing both operational and energy recovery targets. The opportunity extends to biopharmaceutical and vaccine production, where foam control is vital in sterile fermentation. Merck’s Antifoam C, a polyethylene glycol-based agent, has been adopted in mRNA vaccine manufacturing lines to prevent foam-related contamination without compromising cell viability highlighting the importance of FDA-compliant, inert formulations in aseptic environments. China's national ZLD push, particularly in chemical and pharma clusters, is projected to create over $200 million in annual demand for high-efficiency, heat-resistant defoamers in evaporators and crystallizers applications where traditional products degrade rapidly. As water reuse, energy recovery, and contamination prevention take center stage in industrial wastewater treatment, the market for next-generation defoamers is expanding from a niche maintenance chemical to a strategic enabler of performance, sustainability, and compliance in process-critical environments.

Competitive Landscape: Defoamers and Defoaming Agents Market (Water & Wastewater Processing)

The defoamers market for water and wastewater processing is very competitive. Leading chemical manufacturers use their expertise in silicone chemistry, formulation science, and water treatment to gain market share. Companies that control silicone production, such as BASF SE, Wacker Chemie AG, Dow Chemical Company, and Shin-Etsu Chemical, have a strong advantage due to vertical integration and unique formulation skills. These companies are leaders in the silicone-based defoamer segment, which is popular for its wide-ranging effectiveness and compatibility with various industrial effluent conditions.

At the same time, companies like Clariant AG, Croda International, and Ashland Global are finding their own spaces in the market with silicone-free, polymer-based, and oil-based defoamers designed for situations where silicone contamination is a concern or sustainability is important. These companies focus on environmental performance, providing products with low volatile organic compound (VOC) content, bio-based oils, or better biodegradability. These features are increasingly sought after in eco-sensitive markets and areas with strict discharge regulations.

Integrated water treatment providers, including Ecolab Inc. (Nalco Water) and Kemira Oyj, also set themselves apart by incorporating defoamers into wider chemical, monitoring, and service solutions. Ecolab uses real-time digital control systems (like 3D TRASAR) and predictive analytics to optimize defoamer dosing, cut down on chemical waste, and enhance operational reliability. Similarly, Kemira has a strong presence in pulp and paper wastewater treatment, reflecting its deep understanding of recurring foam problems caused by biological and fibrous loads.

Regional and niche players, such as SAN NOPCO (Japan), Accepta Ltd. (UK), and Elementis PLC, focus on specific customer segments with customized offerings and local technical support. These firms often concentrate on smaller-scale formulation and distribution, allowing them to quickly respond to unique application challenges, regulatory requirements, and buying preferences in their markets.

Defoamers and Defoaming Agents Market in Water and Wastewater Processing – Segmentation Insights (2025–2034)

By Type: Silicone-Based Defoamers Lead the Market While Water-Based Formulations Grow Fastest

Silicone-based defoamers dominate the global defoamers and defoaming agents market in water and wastewater processing, accounting for approximately 39.2% of the market in 2025. Their leadership is supported by superior surface activity, long-lasting foam suppression, and exceptional stability under a wide range of pH and temperature conditions, making them highly effective in both municipal and industrial treatment systems. These characteristics are especially valuable in aeration tanks, digesters, and chemical dosing units where persistent foaming can disrupt operations. In contrast, water-based defoamers are emerging as the fastest-growing type, expanding at a CAGR of 6.9% during the forecast period. Their rise is fueled by growing environmental regulations, increased demand for low-VOC formulations, and user-friendly handling, making them an attractive choice for facilities emphasizing sustainability and safety. Polyether-based defoamers are also gaining traction due to their excellent compatibility with diverse wastewater compositions, while oil-based defoamers are gradually declining in use, constrained by regulatory scrutiny and environmental performance concerns. Niche segments like powder defoamers and fatty alcohol-based variants continue to serve specific applications where traditional liquids may not perform optimally.

.png)

By Application: Municipal Wastewater Treatment Leads; Industrial Segment Sees Strongest Growth

Municipal wastewater treatment represents the largest application segment, contributing around 43.8% of the market share in 2025. This segment's dominance stems from widespread foam generation in biological treatment processes such as activated sludge systems, where uncontrolled foaming can hinder oxygen transfer, cause operational delays, and overflow hazards. Silicone-based and polyether defoamers are commonly used here due to their rapid action and resilience in fluctuating flow and contaminant loads. Meanwhile, the industrial wastewater treatment segment is expanding at the fastest pace, registering a CAGR of 7.1% between 2025 and 2034. Growth in this area is driven by rising industrial output, increased chemical and pharmaceutical manufacturing, and tightening discharge standards requiring precise process control including effective foam management. Water treatment, including boiler feedwater and cooling tower applications, maintains steady demand for defoaming agents, particularly in scenarios where foam impacts efficiency or causes carryover. As facilities upgrade infrastructure and adopt stricter operational protocols, the demand for high-performance and eco-friendly defoamers continues to expand across all application areas.

United States Advances Defoamers and Defoaming Agents Market with Regulatory Action and Smart Water Innovation

The United States stands at the forefront of the global defoamers and defoaming agents market, driven by robust regulatory enforcement and a wave of technological innovation. The U.S. Environmental Protection Agency (EPA) continues to raise the bar on wastewater discharge standards, making the deployment of highly effective defoaming agents essential across municipal and industrial treatment facilities. In 2025, the U.S. market witnessed a shift toward low-VOC and environmentally friendly formulations, exemplified by Allnex’s launch of a high-efficiency, silicone-free defoamer for industrial applications. The adoption of AI and IoT-enabled real-time monitoring systems is streamlining chemical dosing and minimizing waste, delivering smarter, more sustainable water treatment.

High-foam sectors such as pulp and paper, textiles, and food and beverage remain key growth drivers, as these industries depend on precision foam control to maintain process stability and product quality. This dynamic landscape positions the U.S. as both a market leader and an innovation hub in the global defoamers and defoaming agents industry.

China Drives Defoamers and Defoaming Agents Demand with Infrastructure Expansion and Green Technology

China is a significant growth engine in the defoamers and defoaming agents market, fueled by unprecedented investment in environmental infrastructure and strict pollution control policies. The government’s National Development and Reform Commission is spearheading large-scale wastewater treatment plant construction, creating robust demand for defoamers in sludge management and aeration tank operations. The nation’s “War on Pollution” continues to tighten environmental standards, prompting both municipal and industrial sectors to prioritize foam control solutions that improve treatment efficiency.

The market has seen a notable rise in non-silicone and biodegradable defoamer development, reflecting the country’s commitment to sustainability and regulatory compliance. Surging demand for defoamer surfactants, especially in the months leading up to major manufacturing periods, highlights the close integration of defoaming agents with China’s industrial growth and seasonal production cycles.

Germany Leads Sustainable Defoamers Market with Smart Water Management and Regulatory Compliance

Germany’s defoamers and defoaming agents market is synonymous with high-tech innovation and environmental responsibility. The market is shaped by the EU Water Framework Directive and rigorous German environmental standards, which favor the use of benign, food-safe, and biodegradable chemical solutions. BASF’s commissioning of a new production unit for food-grade defoamers in March 2025 exemplifies the country’s commitment to both regulatory alignment and technical excellence.

German companies are leveraging automation and data analytics to enable precise, demand-driven dosing of defoamers, optimizing operational costs and reducing environmental impact. Core applications include municipal wastewater treatment, chemical and textile manufacturing, and any process where foam suppression is vital to consistent quality and efficiency. Germany’s integrated, sustainability-first approach cements its position as a leader in next-generation defoamer technology.

India Accelerates Defoamers Market with Policy-Driven Growth and Localized Manufacturing

India’s defoamers and defoaming agents market is experiencing significant expansion, propelled by national water missions such as the “Jal Shakti Abhiyan” and aggressive infrastructure development. The rehabilitation and expansion of water and wastewater treatment facilities are creating new opportunities for both international and domestic suppliers of defoaming chemicals. In 2025, Shin-Etsu Chemical’s supply chain partnership to localize antifoam agent production in southern India highlights the trend toward self-sufficiency and cost-effective distribution.

R&D in India is focused on developing affordable, high-performance defoamer solutions suited to diverse industrial applications and local water chemistries. Pulp and paper, detergents, and textiles remain the top consumer industries, where effective foam management is essential for environmental compliance and operational stability.

Japan Innovates High-Performance Defoaming Agents for Advanced Industrial Applications

Japan’s market for defoamers and defoaming agents is defined by sophisticated product development and a focus on high-performance, low-impact chemistries. Leaders like Shin-Etsu Chemical are setting the standard in advanced silicone-based defoamers, known for their stability and effectiveness in challenging environments. These agents are widely used in Japan’s high-tech manufacturing sectors such as electronics, semiconductors, and precision engineering where uninterrupted processes are crucial.

There is also a strong national focus on sustainability, with R&D targeting defoamers that meet strict environmental and safety standards while providing excellent process control. The pulp and paper industry remains both a driver and a test bed for next-generation defoaming solutions, reflecting Japan’s blend of tradition and innovation in industrial water management.

Brazil Expands Defoamers Market with Sanitation Reform and Industrial Investment

Brazil’s defoamers and defoaming agents market is on a strong upward trajectory, boosted by sweeping reforms in sanitation and increasing investment in water infrastructure. The new regulatory framework has catalyzed private sector participation, resulting in the construction of modern water and wastewater treatment plants that rely heavily on defoaming technologies. The pulp and paper sector is a standout, with companies like Kemira Oyj entering exclusive supply agreements to provide cutting-edge defoamer and drainage technologies.

Brazilian municipalities are expanding biological treatment processes in wastewater plants, where foam control is critical to operational efficiency and environmental performance. As the country continues to industrialize, the demand for high-quality, effective defoamers is expected to grow across both municipal and key industrial segments.

South Korea Advances Defoamers Market with Tailored Industrial Solutions and Technology Integration

South Korea’s defoamers and defoaming agents market is distinguished by a strong emphasis on industrial productivity and the creation of process-specific solutions. The nation’s advanced manufacturing base including electronics, chemicals, and automotive requires high-performance defoamers to ensure wastewater treatment reliability and production efficiency. Local companies are investing in research to engineer products that address unique challenges, such as temperature extremes and variable pH, characteristic of South Korea’s industrial processes.

Expansion and modernization of urban wastewater treatment plants are further driving demand for reliable, specialized chemical solutions. The market is expected to benefit from ongoing investments in plant automation and process optimization, reflecting South Korea’s focus on advanced, integrated water management.

Russia Increases Defoamers Demand with Industrial Modernization and Oil & Gas Expansion

Russia’s defoamers and defoaming agents market is driven by the country’s expansive industrial base, notably in oil and gas, pulp and paper, and chemical production. The oil and gas sector is a primary consumer, utilizing defoamers to manage foam in drilling, gas processing, and water treatment operations. The large-scale pulp and paper industry, especially in northern Russia, depends on defoaming agents to optimize production and improve operational efficiency.

Efforts to modernize industrial infrastructure and align with higher environmental standards are fueling demand for advanced water treatment chemicals. Supportive government policies aimed at increasing industrial output and efficiency further boost the adoption of process-specific, innovative defoaming solutions across Russia’s key sectors.

Defoamers and Defoaming Agents Market in Water and Wastewater Processing Report Scope

Defoamers and Defoaming Agents Market in Water and Wastewater Processing

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.8 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Silicone-based Defoamers, Oil-based Defoamers, Polyether-based Defoamers, Water-based Defoamers, Powder Defoamers, Fatty Alcohol Defoamers, Other Organic Defoamers), By Application (Water Treatment, Wastewater Treatment (Municipal), Industrial Wastewater Treatment), By End-User Industry (Municipalities, Power Generation, Oil and Gas, Chemical and Petrochemical, Pulp and Paper, Food and Beverage, Textile, Pharmaceutical, Mining and Metallurgy, Other Manufacturing and Process Industries), By Function (Defoamers (Foam Breakers), Antifoaming Agents

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Evonik Industries AG (Germany), Ashland Global Holdings Inc. (U.S.), The Dow Chemical Company (U.S.), Wacker Chemie AG (Germany), Clariant AG (Switzerland), Kemira Oyj (Finland), Ecolab Inc. (U.S.), Shin-Etsu Chemical Co., Ltd. (Japan), Accepta Ltd. (UK), Elementis PLC (UK), Elkem ASA (Norway), Croda International Plc (UK), SAN NOPCO LIMITED (Japan),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Defoamers and Defoaming Agents in Water and Wastewater Processing Market Segmentation

By Type

- Silicone-based Defoamers

- Oil-based Defoamers

- Polyether-based Defoamers

- Water-based Defoamers

- Powder Defoamers

- Fatty Alcohol Defoamers

- Other Organic Defoamers

By Application

- Water Treatment

- Cooling Towers

- Boiler Water Treatment

- Desalination Plants

- Raw Water Treatment

- Clarifiers/Settling Tanks

- Membrane Filtration Systems

- Sludge Digesters/Anaerobic Digesters

- Equalization Tanks

- Final Effluent Processing

- Biofilm Control

- Nitrification/Denitrification Systems

- Wastewater Treatment (Municipal)

- Aeration Basins/Activated Sludge Process

- Secondary Treatment Systems

- Sludge Dewatering

- Biological Treatment Processes

- Landfill Leachate Treatment

- Lift Stations/Pumping Stations

- Industrial Wastewater Treatment

- Pulp and Paper Wastewater

- Textile Dyeing Wastewater

- Oil and Gas Produced Water/Wastewater

- Food and Beverage Processing Wastewater

- Chemical and Petrochemical Wastewater

- Mining Wastewater

- Pharmaceutical Wastewater

- Automotive Industry Wastewater

- Other Industrial Effluents

By End-User Industry

- Municipalities

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- Pulp and Paper

- Food and Beverage

- Textile

- Pharmaceutical

- Mining and Metallurgy

- Other Manufacturing and Process Industries

By Function

- Defoamers (Foam Breakers)

- Antifoaming Agents

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Defoamers and Defoaming Agents Market in Water and Wastewater Processing

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Ashland Global Holdings Inc. (U.S.)

- The Dow Chemical Company (U.S.)

- Wacker Chemie AG (Germany)

- Clariant AG (Switzerland)

- Kemira Oyj (Finland)

- Ecolab Inc. (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Accepta Ltd. (UK)

- Elementis PLC (UK)

- Elkem ASA (Norway)

- Croda International Plc (UK)

- SAN NOPCLIMITED (Japan)

* List Not Exhaustive

Research Coverage

This report investigates the global defoamers and defoaming agents market in water and wastewater processing, delivering in-depth analysis reviews, highlights of technological breakthroughs, and a comprehensive overview of the evolving regulatory and sustainability landscape. The study provides actionable intelligence on the competitive dynamics, adoption trends, and market drivers shaping the transition from conventional silicone-based to bio-based and process-optimized defoaming solutions. Developed by USDAnalytics, this report is an essential resource for utilities, manufacturers, industry professionals, and investors seeking to understand global trends, regional opportunities, and the strategic positioning of leading suppliers across more than 25 countries worldwide.

Scope Highlights:

- Segmentation:

- By Type: Silicone-based Defoamers, Oil-based Defoamers, Polyether-based Defoamers, Water-based Defoamers, Powder Defoamers, Fatty Alcohol Defoamers, Other Organic Defoamers

- By Application: Water Treatment, Wastewater Treatment (Municipal), Industrial Wastewater Treatment

- By End-User Industry: Municipalities, Power Generation, Oil and Gas, Chemical and Petrochemical, Pulp and Paper, Food and Beverage, Textile, Pharmaceutical, Mining and Metallurgy, Other Manufacturing and Process Industries

- By Function: Defoamers (Foam Breakers), Antifoaming Agents

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: BASF SE (Germany), Evonik Industries AG (Germany), Ashland Global Holdings Inc. (U.S.), The Dow Chemical Company (U.S.), Wacker Chemie AG (Germany), Clariant AG (Switzerland), Kemira Oyj (Finland), Ecolab Inc. (U.S.), Shin-Etsu Chemical Co., Ltd. (Japan), Accepta Ltd. (UK), Elementis PLC (UK), Elkem ASA (Norway), Croda International Plc (UK), SAN NOPCO LIMITED (Japan).

Methodology

USDAnalytics employs a robust, multi-source research methodology, integrating primary interviews with industry experts and end users, alongside comprehensive secondary research from company reports, patents, regulatory bodies, and technical publications. Market sizing, share, and forecasts are constructed using proprietary analytical models and validated through cross-referencing with actual industry data. Qualitative trend mapping and regional insight gathering ensure the report provides actionable, accurate, and reliable intelligence for stakeholders in the defoamers and defoaming agents market.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements