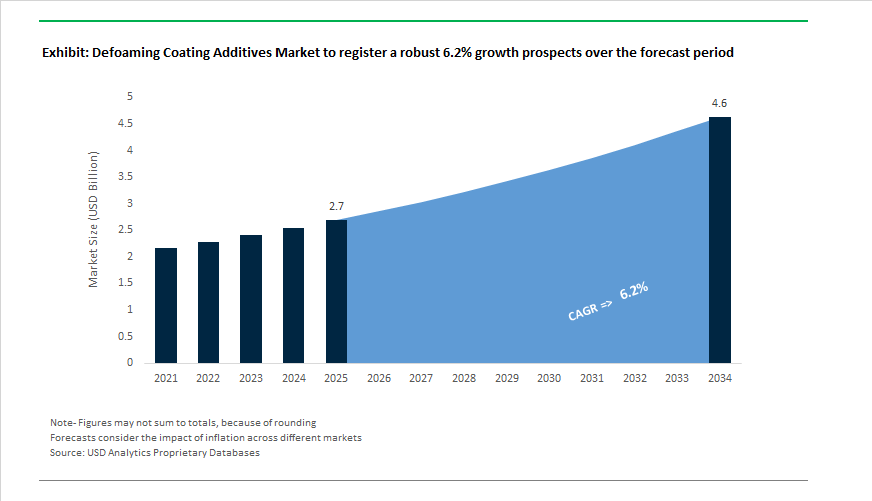

Defoaming Coating Additives Market to Reach $4.6 Billion by 2034 at 6.2% CAGR Driven by PFAS-Free Innovation and Waterborne Coatings Expansion

The Defoaming Coating Additives Market is projected to grow from $2.7 billion in 2025 to $4.6 billion by 2034, reflecting a CAGR of 6.2%. Growth is anchored in the rapid transition toward waterborne architectural coatings, high-solid industrial coatings, and solvent-free epoxy systems where foam control is critical to film integrity, gloss retention, and defect-free finishes. As global regulators tighten VOC, SVOC, and PFAS restrictions, coating formulators are actively replacing legacy mineral oil and fluorinated defoamers with bio-based siloxane and hybrid polymer technologies. The market is increasingly defined by sustainability metrics, compatibility with high-PVC systems, and the ability to perform under high-shear, high-speed application environments such as OEM automotive lines and automated spray systems.

Capacity expansions and sustainability-focused product development intensified through 2024. BASF completed a major defoamer production expansion at its Dilovasi facility in Türkiye in late 2024, increasing output of Foamaster® and Foamstar® additives to serve Southeast Europe, the Middle East, and Africa. In parallel, BASF boosted water-compatible additive production at its Nanjing site in 2024 to support China’s accelerating shift to low-VOC automotive and industrial coatings. Nouryon introduced its first partially bio-based lightweight filler in December 2024, designed to function synergistically with next-generation defoamers to reduce additive loading in sustainable architectural paint formulations. BYK scaled its automated High Throughput Screening facility in Wesel in December 2024, enabling testing of up to 220 samples within 24 hours, significantly shortening development cycles for customized defoaming coating additives tailored to automotive and electronics applications. Evonik strengthened its clean-label positioning throughout 2024 by expanding the adoption of TEGO® Foamex 8880, a hybrid bio-based polymer and polyether siloxane defoamer for waterborne inks and packaging coatings, gaining industry-wide recognition for effective foam suppression with minimal surface interference.

Innovation accelerated further in March 2025 at the European Coatings Show, where BYK introduced a PFAS-free defoamer portfolio including BYK-1810, BYK-1811, and BYK-1818, addressing regulatory pressure to eliminate per- and polyfluoroalkyl substances from industrial coating formulations. In July 2025, Evonik launched TEGO® Foamex 16 and TEGO® Foamex 11 for waterborne architectural coatings. TEGO® Foamex 16 incorporates 25% bio-based material in a siloxane concentrate, while TEGO® Foamex 11 is optimized for high-PVC decorative paints targeting both DIY and professional markets with near-zero VOC and SVOC emissions. Recognition of performance innovation was visible in August 2025, when BYK-1765 received a Ringier Innovation Award in Shanghai for resolving air-entrapment challenges in high-solid, solvent-free epoxy marine coatings without inducing crater formation or haze. Market structure evolved significantly in June 2025, when the JSW Group acquired AkzoNobel India’s decorative unit for €1.4 billion, transferring proprietary additive formulations and strengthening India’s domestic defoaming additives manufacturing base. Industry consolidation reached a global scale in November 2025, when AkzoNobel and Axalta announced a $25 billion merger, integrating R&D resources to accelerate smart coating additives and advanced foam-control technologies. Inflationary pressures impacted pricing dynamics, leading BYK to implement a 5.2% global price increase effective February 2026, reflecting rising raw material and energy costs associated with specialty silicone and polymer defoamer synthesis.

Trends and Opportunities in the Global Defoaming Coating Additives Market

Microfoam Control in High-Gloss Waterborne Coating Systems

- The accelerated shift toward water-rich and low-solvent coating formulations has significantly increased the risk of air entrapment, particularly micro-bubbles that are difficult to eliminate during application and curing. Industrial performance data released in mid-2025 shows that advanced silicone-polyether copolymers and hydrophobically modified silica dispersed in polyglycol carriers can rupture micro-bubbles in under 51 seconds, even in aggressive surfactant environments. This capability is critical for automotive and industrial high-gloss clearcoats, where entrapped air bubbles as small as 10 microns can reduce Distinctness of Image by more than 15 %, directly impacting perceived finish quality and OEM acceptance.

- Manufacturing robustness is becoming equally important. As coating producers increase line speeds and adopt high-shear dispersion processes, additive stability under mechanical stress has become a key procurement criterion. In response to this need, BASF expanded its Nanjing additives facility in 2024 to strengthen supply of next-generation defoamers engineered for high-shear grinding environments. These additives are designed to remain storage-stable while selectively destabilizing foam-forming surfactants at the molecular level, preventing defects such as fish-eyes and craters even at dosage levels below 0.2%.

Regulatory-Driven Shift Toward Low-VOC and PFAS-Free Defoaming Additives

- Global regulatory pressure is accelerating the transition away from alkylphenol ethoxylates, mineral oils, and persistent cyclic silicones in coating additives. Eco-label frameworks and chemical safety regulations are increasingly defining acceptable formulation standards rather than optional sustainability upgrades. In April 2024, Evonik introduced TEGO® Foamex 16, a siloxane-based defoaming concentrate containing approximately 25% bio-based material. This product reflects the emerging 2025 benchmark for near-zero VOC and SVOC content, targeting VOC levels around 0.08% while meeting stringent Ecolabel 2014/312/EU and Blue Angel certification requirements.

- Further reinforcing this trend, Evonik’s 2025 launch of TEGO® Foamex 11 provides a mineral-oil-free emulsion alternative for high-PVC architectural coatings. With around 15% active ingredients in a non-mineral carrier, this formulation supports lower carbon footprints while ensuring compliance with anticipated REACH 2025 restrictions on cyclic siloxanes. As regulators tighten scrutiny on persistent substances, mineral-oil-free and PFAS-free defoamers are becoming the default choice for architectural and decorative paint manufacturers seeking long-term regulatory resilience.

Ultra-Fast Defoaming Kinetics for UV and EB Radiation-Curable Systems

- Radiation-curable coatings and inks represent a rapidly expanding opportunity for precision defoaming additives. The near-instantaneous curing behavior of UV and electron beam systems leaves virtually no time for bubble migration or collapse, requiring defoamers with extremely fast kinetics. In July 2025, Sun Chemical and INX International launched high-speed UV-curable ink platforms capable of exceeding 20,000 impressions per hour. At these speeds, defoaming additives must act faster than the photoinitiation process, often in less than one second, to ensure pinhole-free coatings on non-porous metal and plastic substrates.

- Sustainability considerations are amplifying this opportunity. UV-curable inks, driven by regulatory pressure for circular and low-emission packaging, are projected to reach a market value of approximately USD 2.5 billion by 2026. This growth is creating strong demand for acrylate-compatible defoamers that do not inhibit curing reactions, cause delamination, or compromise food-contact safety in pharmaceutical and flexible packaging applications.

Defoaming Additives for High-Build Coatings in Extreme Climate Conditions

- Infrastructure expansion in coastal, high-humidity, and high-temperature regions is driving demand for high-build protective coatings that can withstand harsh application environments. In April 2025, Advanced Polymer Coatings secured contracts for its MarineLINE coating systems on new IMO-class tankers. These thick-film, chemically resistant coatings require specialized defoaming additives to prevent solvent popping and moisture-induced foaming during application in humid shipyard conditions, ensuring long-term corrosion protection and coating integrity.

- Urban climate adaptation is reinforcing this demand. The global push for cool roof and elastomeric coatings to mitigate urban heat island effects requires breathable, crack-bridging finishes that maintain high solar reflectance over extended lifecycles of 10 to 15 years. Defoaming additives in these systems are now engineered to precisely modify surface tension, enabling trapped gases to escape before film set. This functionality preserves reflective performance while supporting durability in extreme weather conditions, positioning advanced defoamers as essential enablers of climate-resilient coating technologies.

Defoaming Coating Additives Market Share and Segmentation Insights

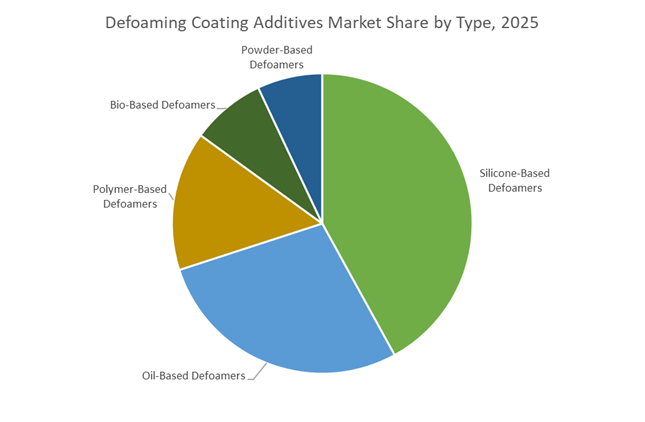

Defoaming Coating Additives Market Share by Type: Silicone-Based Technologies Lead as Bio-Based Alternatives Gain Momentum

Silicone-based defoamers command 42% of the defoaming coating additives market in 2025, reflecting their unmatched efficiency at low dosage and ability to deliver rapid foam knockdown with long-lasting control across wide pH and temperature ranges. These high-performance additives are extensively used in architectural paints and industrial coatings where flawless surface appearance is mandatory. Oil-based defoamers maintain a strong position in cost-sensitive decorative paints and adhesive formulations, offering reliable foam suppression at lower price points, although careful formulation is required to avoid cratering. Polymer-based defoamers, including polyacrylate and polyether chemistries, are increasingly specified in waterborne coatings for their excellent system compatibility and reduced risk of fish eyes. Bio-based defoamers are emerging as a sustainability-driven segment, derived from renewable vegetable oils and plant extracts. Powder-based defoamers serve a specialized role in powder coatings, preventing pinholes and outgassing defects during thermal curing on metal substrates.

Defoaming Coating Additives Market Share by End-Use Industry: Architectural Paints Dominate as Automotive and Industrial Demand Precision Performance

Architectural coatings account for 48% of global defoaming coating additive consumption, driven by high-volume production of waterborne interior and exterior paints where roller and brush application entrains air, making bubble-free finishes essential. Industrial and protective coatings represent a significant secondary segment, requiring defoamers capable of withstanding high-shear mixing while delivering defect-free films on machinery, pipelines, and infrastructure where surface flaws compromise corrosion resistance. Automotive and transportation applications demand the highest visual standards, with defoamers preventing microfoam in primers, basecoats, and clearcoats without disrupting intercoat adhesion, often favoring silicone-free solutions in refinish lines. Wood coatings rely on effective defoaming to preserve natural grain appearance in furniture and flooring. Printing inks and packaging coatings depend on defoamers for uninterrupted high-speed press operation, while adhesives and sealants utilize these additives to eliminate air entrapment that would otherwise weaken bond strength.

Competitive Landscape of the Defoaming Coating Additives Market

The Defoaming Coating Additives Market is highly innovation-driven, with leading manufacturers competing on bio-based chemistries, silicone-free technologies, AI-enabled formulation tools, and low-VOC compliance. As waterborne coatings, automotive finishes, industrial flooring, and decorative paints expand globally, suppliers are differentiating through mass-balanced production, vertical integration, and multifunctional additives that optimize cost, performance, and sustainability metrics.

Evonik leads bio-based defoaming coating additives with TEGO eCO portfolio

Evonik Industries AG remains the global benchmark in specialty defoaming coating additives through its high-performance TEGO® portfolio and strong sustainability pivot. In early 2025, Evonik introduced TEGO® Foamex 812 eCO, its first mass-balanced defoamer containing over 60% bio-carbon content while matching traditional siloxane performance. In February 2026, the company streamlined its North American distribution network to enhance supply chain efficiency for specialty additives. Operating across 104 production locations in 27 countries, Evonik’s eCO portfolio directly targets Scope 3 upstream emission reduction for coatings manufacturers. Its COATINO® digital platform further differentiates the company by enabling AI-driven additive selection tailored to specific resin systems and formulation challenges.

BYK solves micro-foam challenges in high-gloss automotive and industrial coatings

BYK-Chemie GmbH, part of Altana AG, is a technical powerhouse focused on eliminating micro-foam defects in high-gloss automotive and industrial finishes. The company’s BYK-0 series (silicone-based) and BYK-1 series (silicone-free) remain industry standards, with BYK-1642 emerging in 2026 as a cost-effective silicone-free defoamer for performance-driven industrial lines. Between 2024 and 2025, BYK introduced specialized defoamers for solvent-free floor coatings, addressing deaeration in thick-film epoxy and polyurethane systems. With 48 production sites and 63 research facilities globally, Altana ensures localized technical support. Its 2025–2026 CERAFLOUR family replaces PTFE-based additives with sustainable wax alternatives, reinforcing eco-compliance leadership.

BASF scales integrated defoamer production for waterborne and solids systems

BASF SE leverages its Verbund manufacturing model to provide cost leadership and high-volume reliability, particularly in architectural and industrial coatings. The company expanded its Dilovasi, Türkiye plant in 2023–2024 to meet strong demand for Foamaster® and Foamstar® products across MEA. In May 2024, BASF added a new production line in Nanjing, China, targeting dispersants and defoamers for the fast-growing Asian waterborne coatings market. Key products include Efka® PB 2744 for 100% solids industrial flooring systems and Efka® 2010 for silicone-sensitive lacquers. Backward integration into feedstock chemicals provides BASF resilience against raw material price volatility in global specialty additives markets.

Dow dominates silicone defoamer chemistry with low-loading innovation strategy

Dow Inc. commands leadership in silicone-based defoaming coating additives, a chemistry segment accounting for approximately 40% of global market share. Through its DOWSIL™ and ACUSOL™ product ranges, Dow delivers advanced foam control solutions for automotive OEM coatings and transportation finishes. The DOWSIL™ 8590 additive balances pigment wetting and foam suppression, ensuring mirror-finish clarity in basecoat and clearcoat systems. In early 2026, Dow launched the “Transform to Outperform” initiative, integrating AI-driven optimization across performance materials manufacturing. Its strategic emphasis on low-loading defoamers reduces dosage requirements, lowering total formulation costs for high-volume industrial clients while enhancing sustainability metrics.

Elementis advances multifunctional and zero-VOC foam control technologies

Elementis PLC differentiates through multifunctional rheology and foam control additives, often combining defoaming and leveling benefits within a single formulation to streamline additive complexity. The company holds a strong presence in Wood & Furniture and Decorative coatings, identified as the fastest-growing application segments in 2026. Elementis is expanding aggressively in Southeast Asia, particularly Vietnam and Malaysia, targeting the region’s large-scale furniture export industry. Recent innovation centers on zero-VOC mineral-oil-based defoamers that provide a cost-efficient alternative to silicone while complying with 2026 European ecolabel standards. Its hectorite clay technology strengthens performance in waterborne architectural and industrial coating systems.

China: Standards-Driven Reformulation and Circular Feedstock Integration

China’s defoaming coating additives market is entering a decisive compliance-led transition phase, anchored by stricter national standards and fiscal instruments. The release of GB 30981.1-2025 by the State Administration for Market Regulation in May 2025 represents a structural inflection point for architectural coatings. With enforcement scheduled for June 1, 2026, the regulation imposes stringent limits on SVOCs and related hazardous substances, forcing formulators to accelerate the adoption of high-efficiency, low-emission defoaming additives. This regulatory tightening is amplified by the December 2025 amendment to the Environmental Protection Tax Law, which expands VOC taxation under a pilot program. As a result, silicone-free and water-borne defoamers are becoming the default choice for mass-market architectural and industrial coatings, as manufacturers actively seek to minimize taxable emissions.

Parallel to regulation, China is embedding circularity and bio-based chemistry into additive supply chains. The completion of a chemical recycling facility by Mitsubishi Chemical Group and ENEOS in July 2025 has strengthened access to mass-balanced feedstocks for coating additives. Innovation recognition, such as the Ringier Technology Innovation Award granted in May 2025 to Evonik for TEGO® Wet 580 Terra, highlights rapid uptake of bio-based defoaming and wetting technologies. At the same time, lithium battery export controls introduced in December 2025 have redirected domestic R&D toward specialized defoamers for battery electrode coatings, reinforcing internal supply chain security. Looking ahead, Shanghai Pudong’s 2026 Green Chemistry hub, with subsidies for digital lab infrastructure and high-throughput screening, positions China as a fast-cycle innovation center for zero-VOC defoaming agents.

United States: VOC Alignment and PFAS-Free Qualification Cycles

The U.S. defoaming coating additives market in 2025 is shaped by regulatory harmonization and downstream qualification by OEMs. The EPA’s January 6, 2025 amendments to the National VOC Emission Standards for Aerosol Coatings align federal reactivity factors with CARB benchmarks, triggering widespread reformulation of defoamers used in spray-applied architectural and automotive coatings. This alignment has elevated demand for near-zero VOC and SVOC defoamers capable of performing under high pigment volume concentration systems without compromising surface quality.

Industry response has been rapid and portfolio-driven. At the American Coatings Show 2024/2025, Evonik introduced TEGO® Foamex 16 and TEGO® Foamex 11, targeting waterborne architectural coatings with minimal emission profiles. Simultaneously, the EPA’s 2026 HFC allowance allocations under the AIM Act have accelerated the phase-out of traditional blowing agents, indirectly increasing demand for PFAS-free defoaming stabilizers in foam-prone coating processes. Supply chain resilience is also improving, supported by Evonik’s late-2024 expansion of its Charleston, South Carolina precipitated silica facility, which underpins domestic production of powder-based antifoams. Qualification trends are evident in the automotive sector, where BYK’s PFAS-free BYK-1810 entered OEM approval cycles in early 2025, signaling a broader shift toward sustainability-screened additives.

Germany: Mass Balance Adoption and Safe-and-Sustainable Design

Germany remains the innovation benchmark for defoaming coating additives in Europe, with 2025 marking a transition from pilot concepts to commercialized sustainability frameworks. In March 2025, Evonik launched TEGO® Foamex 812 eCO, its first mass-balanced defoamer utilizing ISCC PLUS certified bio-attributed feedstocks. This approach allows coating manufacturers to reduce Scope 3 upstream emissions while maintaining unchanged production processes, a critical advantage for industrial formulators facing cost and performance constraints.

The European Coatings Show 2025 further underscored Germany’s leadership, with BYK presenting a new bio-based defoamer engineered for high-shear aqueous hybrid construction formulations. Regulatory momentum is reinforcing these innovations. Under the EU’s Safe and Sustainable by Design criteria, German manufacturers are increasing R&D investment in non-aromatic, polymer-based defoamers, with industry estimates indicating a 15% rise in spending during 2025 to meet evolving ECHA toxicity profiles. Complementing industrial R&D, the Fraunhofer Institute’s late-2025 breakthroughs in modified lignin carriers signal a medium-term pathway to eliminate mineral-oil-based carriers entirely by 2030, aligning Germany’s defoamer market with long-horizon circular economy objectives.

India: Capacity Localization and Infrastructure-Led Demand Pull

India’s defoaming coating additives market is advancing through a combination of localized capacity build-out and application-driven demand. In 2025, Nouryon commissioned a dedicated production line for high-performance defoamers, strengthening domestic supply for textile dyeing and infrastructure coatings. This expansion aligns with the maturation of India’s PLI Scheme 2.0 for specialty chemicals, which achieved a key milestone in 2025 by enabling local production of polyether-modified siloxanes and reducing import dependency by approximately 20%.

Domestic innovation is also accelerating at the SME level. In December 2025, Sakshi Chem Sciences introduced Addage Defoamer Liquid, a fast-acting formulation designed to suppress micro-foam in high-speed architectural paint filling lines, addressing a critical bottleneck in automated production. On the demand side, the PM Gatishakti Smart Cities budget for 2025–2026 has prioritized Cool Roof coatings, materially increasing consumption of thermally stable, weather-resistant defoaming additives.

Comparative Snapshot: Defoaming Coating Additives Market by Country

Defoaming Coating Additives Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Strategic Industry Response

|

Market Trajectory

|

|

China

|

GB 30981.1-2025 and VOC taxation

|

Low-SVOC, water-borne, bio-based defoamers

|

Regulation-accelerated reformulation

|

|

United States

|

EPA VOC alignment and AIM Act

|

Near-zero VOC, PFAS-free portfolios

|

OEM-led qualification and compliance

|

|

Germany

|

SSbD and ISCC PLUS adoption

|

Mass-balanced, polymer-based defoamers

|

Sustainability-driven differentiation

|

|

India

|

PLI Scheme 2.0 and Smart Cities

|

Local capacity and fast-cycle innovation

|

Infrastructure-led volume expansion

|

Defoaming Coating Additives Market Report Scope

Defoaming Coating Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type (Silicone-Based Defoamers, Oil-Based Defoamers, Polymer-Based Defoamers, Bio-Based Defoamers, Powder-Based Defoamers), By Technology (Water-Borne Systems, Solvent-Borne Systems, Radiation-Curing Systems, High-Solids Systems), By Application Stage (Grinding Stage Additives, Let-Down Stage Additives), By End-Use Industry (Architectural Coatings, Automotive and Transportation, Industrial and Protective Coatings, Printing Inks and Packaging, Wood Coatings, Adhesives and Sealants)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, BYK-Chemie GmbH, BASF SE, Dow Inc., Wacker Chemie AG, Elementis PLC, Shin-Etsu Chemical Co., Ltd., Arkema S.A., Nouryon, San Nopco Limited, Clariant AG, Mitsubishi Chemical Group Corporation, Fineotex Chemical Limited, Buckman Laboratories International, Inc., Hexion Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Defoaming Coating Additives Market Segmentation

By Type

- Silicone-Based Defoamers

- Oil-Based Defoamers

- Polymer-Based Defoamers

- Bio-Based Defoamers

- Powder-Based Defoamers

By Technology

- Water-Borne Systems

- Solvent-Borne Systems

- Radiation-Curing Systems

- High-Solids Systems

By Application Stage

- Grinding Stage Additives

- Let-Down Stage Additives

By End-Use Industry

- Architectural Coatings

- Automotive and Transportation

- Industrial and Protective Coatings

- Printing Inks and Packaging

- Wood Coatings

- Adhesives and Sealants

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Defoaming Coating Additives Industry

- Evonik Industries AG

- BYK-Chemie GmbH

- BASF SE

- Dow Inc.

- Wacker Chemie AG

- Elementis PLC

- Shin-Etsu Chemical Co., Ltd.

- Arkema S.A.

- Nouryon

- San Nopco Limited

- Clariant AG

- Mitsubishi Chemical Group Corporation

- Fineotex Chemical Limited

- Buckman Laboratories International, Inc.

- Hexion Inc.

*- List not Exhaustive