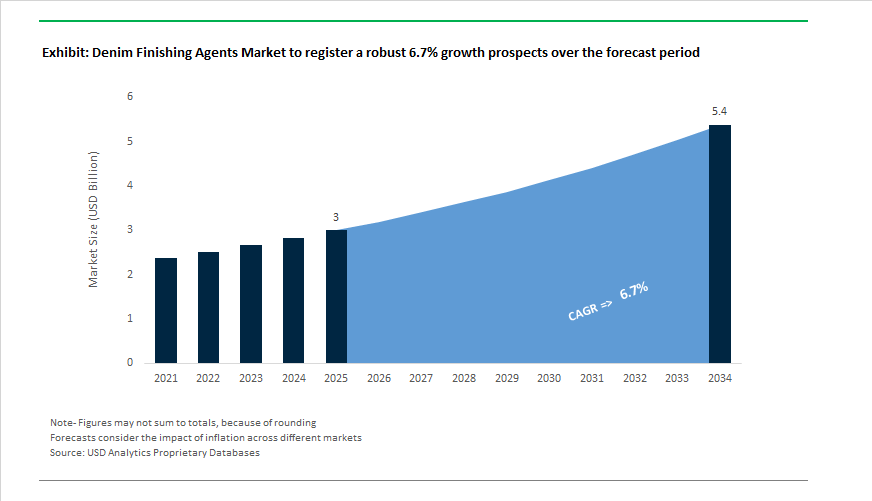

Denim Finishing Agents Market to Reach $5.4 Billion by 2034 at 6.7% CAGR Driven by Laser-Compatible Chemistry and Bio-Based Auxiliaries

The Denim Finishing Agents Market is projected to expand from $3 billion in 2025 to $5.4 billion by 2034, registering a CAGR of 6.7%. Growth is being shaped by the structural transformation of denim wet processing toward laser finishing, enzyme-based abrasion, permanganate-free bleaching, and traceable circular chemistry. Mills across Bangladesh, India, Türkiye, Egypt, and China are under increasing pressure to reduce effluent discharge, eliminate hazardous oxidants, and lower water intensity per garment. This shift is accelerating the adoption of sustainable denim finishing agents, including laser-compatible pretreatments, bio-based auxiliaries, and enzyme-driven abrasion systems that enable high-contrast aesthetics without heavy chemical washing.

Technology-driven sustainability upgrades began gaining visible traction in May 2024, when Archroma introduced the DENIM HALO laser-friendly system at the Bangladesh Denim Expo. The nearly contactless finishing platform enables mills to reduce effluent loads by up to 50% and energy consumption by 40% while maintaining high-contrast used effects. In June 2024, Pulcra Chemicals strengthened its sustainable textile auxiliaries portfolio through the acquisition of Tanatex Chemicals, integrating specialized finishing technologies into Pulcra’s global manufacturing network to target eco-efficient denim processing. During 2024, Novozymes launched the DeniSafe enzyme system, reporting water and energy reductions of up to 90% by minimizing pumice stone usage and lowering total chemical load in abrasion treatments. Operational restructuring also shaped supply dynamics; in February 2025, DyStar consolidated its North American operations into its Reidsville facility following earlier site closures, streamlining denim dye and auxiliary production to improve cost efficiency and supply chain reliability.

Product innovation intensified in May 2025 when Rudolf Group introduced its BIO-LOGIC portfolio of 69 bio-based auxiliaries, including RUCO-SPECIAL LSM, a bio-carbon laser smoother, and RUCOLASE DWS, a waterless bio-abrasive solution designed for sustainable stonewashing. In July 2025, Rudolf signed an exclusive global distribution agreement for Sanitized® technologies, enabling integration of odor-control and antimicrobial finishes into denim auxiliary systems aligned with low-wash consumer trends. Archroma secured Cradle to Cradle Certified® Gold status for over 200 textile chemicals in November 2025, strengthening brand-level adoption of recyclable-safe denim finishing chemistries. Structural ownership changes reshaped the competitive landscape in January 2026, when DyStar transitioned to full ownership under Zhejiang Longsheng Group, stabilizing global dye and finishing auxiliary supply after multi-year restructuring. In parallel, CHT Group announced in January 2026 a breakthrough under its OrganIQ Seek platform enabling permanganate-free spray bleaching with consistent fade performance, directly addressing regulatory and worker safety concerns tied to potassium permanganate. Archroma further expanded laser-compatible chemistry with DIRSOL RD in January 2026, designed to deliver high contrast on black and indigo shades in emerging sourcing hubs such as Egypt. Digital circularity entered the market in early 2026 when SMX introduced embedded fiber tracking technology to verify recycled denim content, reinforcing transparency requirements in global fashion supply chains.

Trends and Opportunities in the Global Denim Finishing Agents Market

Bio-Catalytic Bleaching Replacing Potassium Permanganate in Distressed Denim

- The global phase-out of potassium permanganate in denim bleaching is accelerating under mounting health, safety, and regulatory pressure. A 2024 assessment by the Clean Clothes Campaign revealed that more than five tons of potassium permanganate are used daily in major denim manufacturing clusters such as Turkey, exposing workers to severe respiratory and dermatological risks. In response, tier-one apparel brands including Levi Strauss & Co., H&M, and Inditex have embedded ZDHC MRSL compliance into sourcing requirements, effectively discouraging the continued use of PP-based bleaching.

- This regulatory and brand-driven shift is accelerating adoption of laccase-based enzymatic bleaching systems. These bio-catalytic agents selectively oxidize indigo without damaging cellulose, enabling controlled fading while eliminating hazardous chemical sprays. In October 2025, Archroma received the ITMF Sustainability and Innovation Award for its DENIM HALO system, which enables high-contrast distressed effects while delivering water savings of 40 to 56% and carbon emission reductions of 33 to 34%. The system replaces both stonewashing and permanganate spraying, positioning enzymatic bleaching as the new industry standard rather than an alternative process.

Multifunctional Silicones and Bio-Based Softeners Redefining Performance Denim

- The evolution toward performance denim is driving softening agents to deliver more than tactile comfort. Modern finishing formulations are now expected to provide stretch recovery, abrasion resistance, moisture management, and long-term durability without compromising recyclability or breathability. In December 2025, Archroma confirmed that ten of its finishing product groups achieved Cradle to Cradle Certified Gold status under Version 4.0 standards. These products are based on multi-amino functional silicone chemistries that deliver a premium hand feel while maintaining fiber circularity and material health requirements demanded by luxury and sustainable denim collections.

- At the same time, regulatory pressure on microplastic pollution is accelerating the shift away from petroleum-derived softeners. Under the European Union’s Ecodesign for Sustainable Products Regulation, implementation during 2024 and 2025 has prompted denim mills to adopt bio-based wicking agents and softeners that minimize microfiber shedding during domestic laundering. Innovations such as the LERTISAN range, presented at ITMA Asia 2025, offer fully bio-based alternatives designed to reduce long-term environmental release while maintaining softness and wear performance, addressing a critical compliance gap for European-bound denim exports.

Laser-Sensitizing Finishes Powering Waterless Denim Design

- Laser finishing is rapidly emerging as the digital backbone of sustainable denim production, creating a high-growth niche for chemical pre-treatments that enhance fabric responsiveness to laser energy. Technology collaborations between Jeanologia and Archroma have resulted in integrated concepts such as G2 Dynamic and Denim Halo. These systems use laser-sensitizing agents like Dirsol® RD to engineer dye concentration at the yarn surface, enabling lasers to generate whiskers, fades, and abrasion effects with zero water consumption during the final distressing stage.

- The scalability of laser-compatible finishing chemistry is driving measurable environmental gains. By late 2025, manufacturers reported that 63% of denim assessed using the Environmental Impact Measuring platform achieved low-impact status. This progress is directly linked to the elimination of pumice stones and chemical sprays, which historically accounted for approximately 16% of high-chemical-impact finishing operations. As brands push toward zero-liquid-discharge production models, laser-sensitizing agents are becoming essential enablers rather than optional enhancements.

Compatibilizing Finishes for Recycled and Blended Fiber Denim

- The rapid adoption of recycled cotton, man-made cellulosics, and alternative fibers is creating a new technical challenge for denim finishing. Recycled fibers typically exhibit lower tensile strength, inconsistent dye uptake, and higher fibrillation, requiring specialized finishing agents to normalize performance. In its 2024 and 2025 sustainability disclosures, Levi Strauss & Co. reiterated its commitment to sourcing all cotton from preferred sources, including recycled content. This shift is creating strong demand for compatibilizing enzymes and softeners that can align the mechanical and aesthetic properties of recycled fibers with those of virgin cotton.

- Targeted innovation is addressing this gap. In December 2025, Archroma partnered with Fibre52 to scale a low-temperature, neutral-pH bleaching system engineered specifically for recycled cotton and cotton polyester blends. This technology preserves fiber integrity while achieving uniform brightness, offering a resource-efficient alternative to conventional high-heat bleaching processes that can irreversibly damage recycled substrates. As circular denim moves from pilot collections to mainstream volumes, compatibilizing finishing agents are emerging as a critical growth engine within the denim finishing agents market.

Denim Finishing Agents Market Share and Segmentation Insights

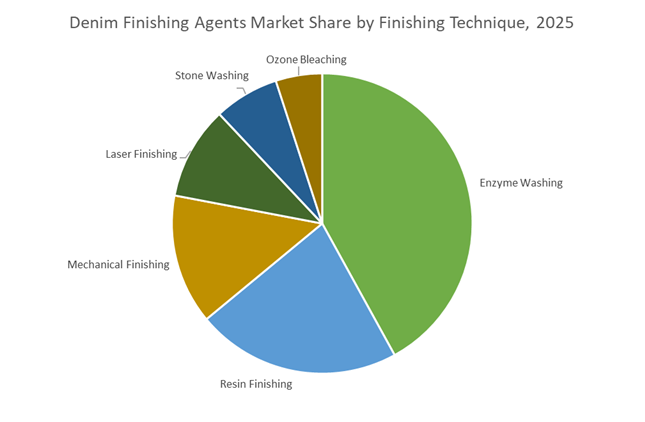

Market Share by Finishing Technique: Enzyme Washing Leads as Laser and Ozone Drive Sustainable Innovation

Enzyme washing commands 42% of the denim finishing agents market in 2025, establishing itself as the dominant technique for achieving soft hand feel, controlled fading, and authentic aged aesthetics. Cellulase-based enzyme washing has largely replaced traditional stone washing due to lower fabric damage, improved productivity, and reduced environmental footprint, aligning with sustainable denim manufacturing trends. Resin finishing maintains a strong position for wrinkle-resistant denim, durable press garments, and 3D effects such as whiskers and permanent creases, with growing adoption of formaldehyde-free resins driven by regulatory compliance. Mechanical finishing continues to support texture development, although sandblasting is declining due to worker safety concerns. Laser finishing is the fastest-growing segment, enabling chemical-free, waterless patterning with high design precision, supporting Industry 4.0 automation. Ozone bleaching is emerging as a low-water alternative for bleaching and fading, while stone washing steadily declines due to waste generation and equipment wear.

Market Share by Application Mode: Exhaust Processing Dominates as Foam Technology Gains Sustainability Focus

Exhaust processing accounts for 58% of application modes, remaining the global standard for garment-based denim finishing using enzymes, resins, and bleaching agents in batch washing systems. Its flexibility for small lots and varied styles makes it indispensable in denim laundries worldwide. Continuous processing represents a significant share in fabric-stage finishing, particularly for resin treatments and bleaching, supporting high-volume production with consistent quality across long fabric runs. Spray application is gaining traction for targeted effects such as whiskers, grinding, and localized fading, allowing designers to achieve realistic wear patterns while reducing chemical consumption. Foam application is an emerging sustainable technology, delivering concentrated finishing agents with dramatically lower water and energy usage compared to immersion methods. As brands prioritize eco-friendly denim production, foam-based and spray techniques are increasingly adopted alongside traditional exhaust systems to meet sustainability targets without compromising fashion aesthetics.

Competitive Landscape of the Denim Finishing Agents Market

The Denim Finishing Agents Market is rapidly evolving toward laser-friendly effects, PFAS-free chemistries, metal-free bleaching systems, and digitally integrated garment processing, as brands prioritize sustainable denim manufacturing, water reduction, and premium aesthetic performance across global supply chains.

Archroma pioneers laser-friendly denim finishing with Halo and DIRSOL RD chemistry

Archroma leads the sustainable denim finishing agents market through its integrated Fiber-to-Garment platform and advanced coloration technologies. In 2026, the company debuted the Denim Halo system powered by DIRSOL® RD chemistry, enabling high-contrast, laser-friendly effects while eliminating manual scraping and toxic oxidants. Its DIRESUL® EVOLUTION BLACK stands out as the industry’s cleanest sulfur black dyestuff, cutting dye synthesis environmental impact by 57%. Archroma strengthened its global sourcing footprint in January 2026 by expanding operations in Egypt, positioning the country as a strategic denim hub for European and North American brands. With over 200 Cradle to Cradle Gold certifications, Archroma continues to set benchmarks in low-impact denim finishing, eco-efficient dyeing, and circular textile chemistry.

CHT Group advances metal-free and KMnO4-free smart denim effects via LAB102

CHT Group targets the premium jeans and garment segment through its LAB102 portfolio, emphasizing clean chemistry and automated finishing. Its LAB102 Product Catalogue 2026 introduced metal-free bleaching agents and formaldehyde-free resins, supporting regulatory-compliant denim processing. A standout innovation is organIQ seek, a high-performance system designed to completely replace potassium permanganate in distressing applications. CHT’s BeSo® Smart Effects range delivers functional performance finishes such as BeSo®FRESH anti-odor and BeSo®DRY water repellency, aligning with rising demand for performance denim. The company’s all-in-one Collection Database digitally links chemical recipes with laser and ozone machines, enabling fully automated garment finishing workflows that reduce water use, labor dependency, and production variability.

DyStar strengthens global denim auxiliaries platform after Zhejiang Longsheng integration

DyStar entered a new growth phase in January 2026 after becoming a wholly owned subsidiary of Zhejiang Longsheng Group, securing long-term financial stability for innovation-led expansion. The company consolidated North American manufacturing into a high-efficiency Reidsville, North Carolina facility in late 2025, streamlining specialty denim auxiliary production. DyStar also reorganized its global sales structure in September 2025 to accelerate regional growth, with strong emphasis on digital color management. Its 2024 to 2025 Integrated Sustainability Report highlighted meaningful reductions in water-to-product ratios across its denim chemical portfolio. With vertically integrated dye and finishing solutions, DyStar continues to scale sustainable indigo processing, low-liquor applications, and data-driven color consistency for global denim producers.

Rudolf drives PFAS-free and bio-based vintage denim aesthetics

Rudolf differentiates through its Better Chemistry philosophy and leadership in enzymatic and bio-based denim finishing. In 2025, the company secured exclusive global distribution rights for Sanitized® textile technologies, embedding hygiene and freshness into next-generation denim finishes. Rudolf’s BIO-LOGIC and CYCLE-LOGIC platforms leverage renewable and recycled raw materials for softeners and water repellents, reinforcing circular textile manufacturing. As of February 2026, Rudolf spearheaded PFAS testing under EN 17681-1:2025, positioning itself at the forefront of PFAS-free compliance. The company dominates the vintage aesthetics segment, supplying enzymatic alternatives to pumice stone washing that replicate authentic worn looks while eliminating solid waste, water-intensive processes, and abrasive garment damage.

Pulcra Chemicals delivers tailor-made high-performance finishes for athleisure denim

Pulcra Chemicals focuses on customized denim finishing agents for premium and functional apparel markets, strengthened by its integration of Devan Chemicals. In January 2026, Pulcra launched STABIFIX® NBF, a next-generation fixing agent that significantly improves color fastness in denim-polyamide blends, supporting the fast-growing athleisure denim category. The company is aligning closely with CSRD requirements, providing detailed life-cycle data for all auxiliaries to help mills meet European sustainability reporting standards. Its PULCRA TEC® NFS platform enables durable water repellent finishes that maintain performance on heavyweight denim. Pulcra is actively expanding Devan functional technologies in North America, highlighted by its major presence at ISPA 2026 in Orlando.

China: Compliance-Driven Reformulation and AI-Led Chemical Efficiency

China’s denim finishing agents market is undergoing a rapid structural transformation as sustainability regulation converges with large-scale industrial digitization. Under the 2025 Action Plan for the Development of the Green Petrochemical Industry, stringent VOC limits on textile auxiliaries have materially accelerated the phase-out of solvent-based resins and conventional finishing polymers. Denim mills supplying export-oriented brands are now prioritizing waterborne, low-VOC, and bio-based softeners to ensure compliance across domestic and international supply chains. This regulatory pressure is reinforced by tightening downstream buyer audits, which increasingly screen denim finishing agents for lifecycle toxicity, worker safety, and wastewater compatibility.

At the manufacturing level, China is pairing regulatory reform with capital-intensive smart factory investments. In late 2024, Anhui Fulltime Specialized Solvents and major denim clusters in Guangdong initiated a $1.2 billion digital upgrade program focused on AI-driven dosage control for finishing agents. These systems dynamically adjust softener, resin, and enzyme concentrations in real time, reducing chemical overuse by an estimated 15–20% while improving batch-to-batch consistency. Parallel to digitalization, the 2025 update to GB/T 18401 textile safety standards has forced a decisive move away from formaldehyde-based crosslinkers. Leading mills report that more than 90% of legacy chemistries have already been replaced with glyoxal-based and citric-acid-based formaldehyde-free alternatives, a shift that directly supports continued access to EU and U.S. denim markets.

India: Policy-Led Sustainability and Enzyme-Based Process Innovation

India’s denim finishing agents market is being reshaped by a rare alignment of regulation, infrastructure investment, and domestic biotechnology innovation. The Sustainable Fashion (Promotion and Regulation) Bill, 2025 represents a watershed moment, mandating large apparel and textile companies to cut water consumption by 20% and disclose supplier-level environmental impact. This policy has sharply increased demand for waterless and low-liquor-ratio finishing agents, particularly ozone-compatible softeners and resins designed for foam and nebulization systems. Denim brands operating in India are now actively reformulating finishing recipes to meet both regulatory and buyer-led ESG expectations.

Infrastructure readiness has amplified this transition. By early 2026, the Tirupur and Erode textile belts in Tamil Nadu achieved near-universal adoption of Zero Liquid Discharge systems. This has fundamentally altered chemical selection criteria, favoring finishing agents with high biodegradability, low salt load, and minimal membrane-fouling risk to protect reverse osmosis assets. On the innovation front, Indian biotech firms reached a commercial breakthrough in 2025 with cold-water cellulase enzymes that operate efficiently at 25°C–30°C. These enzymatic desizing and bio-polishing solutions significantly lower energy consumption during abrasion and finishing, positioning India as a cost-competitive and sustainability-aligned sourcing hub for global denim brands.

Turkey (Türkiye): Nearshoring Momentum and Bio-Certified Differentiation

Turkey’s denim finishing ecosystem is benefiting from its strategic role as the EU’s preferred nearshoring destination. Accounting for 25.4% of EU denim fabric imports in 2025, Turkey is increasingly using sustainability credentials as a competitive differentiator rather than a compliance exercise. Preparations for ITM 2026 have placed digital washing, laser finishing, and bio-certified finishing agents at the center of product development for upcoming seasonal collections. Turkish mills are actively investing in finishing chemistries optimized for digital abrasion and low-water processing, aligning with European brand timelines.

Complementing technology adoption, bilateral green accords signed in late 2025 have accelerated standardization. The Istanbul Textile and Raw Materials Exporters' Association partnered with international certification bodies to formalize Bio-Preferred labeling for denim. This initiative promotes the use of turmeric-derived pigments, recycled dyestuffs, and low-impact finishing agents, enabling Turkish suppliers to command premium positioning in sustainability-focused EU retail channels.

United States: Regulatory Bans and Foam-Based Finishing Scale-Up

The U.S. denim finishing agents market is being driven by state-level chemical bans and federally supported process innovation. PFAS prohibitions enacted in California and New York from January 1, 2025 have forced an immediate pivot away from fluorinated durable water repellent treatments. Major apparel brands have responded by reformulating entire product lines around fluorine-free DWR systems and bio-based stain-resistant finishes, reshaping demand for compliant finishing agents ahead of 2026 collections.

Process innovation is reinforcing this chemistry shift. Supported by the U.S. Department of Energy, foam dyeing and foam finishing pilot programs reached commercial scale in North Carolina during 2025. These systems reduce water usage by up to 95% compared with conventional bath processes and rely on highly specialized foam-stabilizing surfactants and finishing additives. As adoption expands, U.S. mills are increasingly sourcing finishing agents designed for rheological stability, rapid collapse control, and uniform surface deposition under foam-based application.

Bangladesh: Green Finance and Enzyme-Led Process Modernization

Bangladesh’s denim finishing sector is advancing rapidly through targeted financial incentives and operational modernization. The expansion of the Bangladesh Bank’s Green Transformation Fund in 2025 has lowered financing costs for mills adopting laser-compatible finishing agents and ozone bleaching chemistries. These investments are directly linked to improved Higg Index scores, strengthening Bangladesh’s competitiveness among sustainability-conscious global buyers.

Operationally, large Gazipur-based mills reported a complete transition away from pumice stone washing by late 2025. The adoption of bio-synthetic abrasive agents and enzymatic no-stone finishing has eliminated sludge generation, reduced fabric damage, and lowered water consumption. This shift has structurally increased demand for advanced enzymatic finishing agents and micro-emulsion-based abrasion chemistries.

Pakistan: Laser–Chemical Integration for Water Intensity Reduction

Pakistan’s export-oriented denim industry is leveraging chemical innovation to complement rapid adoption of laser and ozone technologies. By early 2026, major exporters in Karachi and Lahore reported water consumption reductions of up to 75% per garment through the integration of E-flow nebulization systems with specialized chemical micro-emulsions. These finishing agents enhance laser fading efficiency and color contrast while minimizing rewash cycles. As a result, Pakistan’s denim finishing agents market is increasingly defined by precision chemistry tailored for digital finishing workflows rather than traditional wet processing.

Comparative Snapshot: Denim Finishing Agents Market by Country

Denim Finishing Agents Market County Level Snapshot

|

Country

|

Primary Policy or Technology Driver

|

Chemistry Shift

|

Strategic Outcome

|

|

China

|

VOC mandates and AI dosage control

|

Waterborne, formaldehyde-free agents

|

Compliance-led efficiency gains

|

|

India

|

Sustainable Fashion Bill and ZLD

|

Enzymatic, ozone-compatible finishes

|

Water and energy intensity reduction

|

|

Turkey

|

EU nearshoring and bio-labeling

|

Bio-certified, digital-wash chemistries

|

Premium sustainability positioning

|

|

United States

|

PFAS bans and foam finishing

|

Fluorine-free, foam-stable additives

|

Regulatory alignment and process innovation

|

|

Bangladesh

|

Green finance and enzyme adoption

|

No-stone, ozone-ready agents

|

ESG score improvement

|

|

Pakistan

|

Laser and E-flow integration

|

Micro-emulsion finishing systems

|

Structural water savings

|

Denim Finishing Agents Market Report Scope

Denim Finishing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2034)

|

$5.4 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Product Type (Enzymes, Softeners, Resins, Bleaching and Oxidizing Agents, Auxiliaries, Functional Agents), By Finishing Technique (Enzyme Washing, Stone Washing, Laser Finishing, Ozone Bleaching, Resin Finishing, Mechanical Finishing), By Denim Type (Raw Denim, Sanforized Denim, Stretch Denim, Selvedge Denim, Sustainable Denim), By Application Mode (Exhaust Processing, Continuous Processing, Spray Application, Foam Application), By End-Use (Fashion and Lifestyle Apparel, Accessories, Home Textiles and Upholstery)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, Huntsman International LLC, BASF SE, Rudolf GmbH, CHT Group, Pulcra Chemicals GmbH, Novonesis Group, DyStar Group, Dow Inc., Kemin Industries, Inc., Garmon Chemicals, Sarex Chemicals, Zydex Industries, NICCA Chemical Co., Ltd., Tanatex Chemicals B.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Denim Finishing Agents Market Segmentation

By Product Type

- Enzymes

- Softeners

- Resins

- Bleaching and Oxidizing Agents

- Auxiliaries

- Functional Agents

By Finishing Technique

- Enzyme Washing

- Stone Washing

- Laser Finishing

- Ozone Bleaching

- Resin Finishing

- Mechanical Finishing

By Denim Type

- Raw Denim

- Sanforized Denim

- Stretch Denim

- Selvedge Denim

- Sustainable Denim

By Application Mode

- Exhaust Processing

- Continuous Processing

- Spray Application

- Foam Application

By End-Use

- Fashion and Lifestyle Apparel

- Accessories

- Home Textiles and Upholstery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Denim Finishing Agents Industry

- Archroma

- Huntsman International LLC

- BASF SE

- Rudolf GmbH

- CHT Group

- Pulcra Chemicals GmbH

- Novonesis Group

- DyStar Group

- Dow Inc.

- Kemin Industries, Inc.

- Garmon Chemicals

- Sarex Chemicals

- Zydex Industries

- NICCA Chemical Co., Ltd.

- Tanatex Chemicals B.V.

*- List not Exhaustive