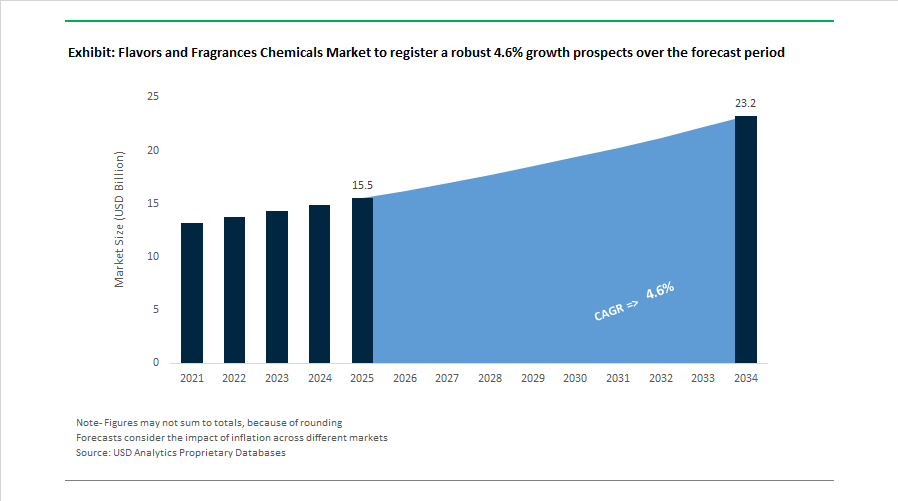

Flavors and Fragrances Chemicals Market Size 2025–2034: $15.5 Billion to $23.2 Billion at 4.6% CAGR Fueled by Fermentation, Portfolio Realignment, and Regional Expansion

The Flavors and Fragrances Chemicals Market is projected to grow from $15.5 billion in 2025 to $23.2 billion by 2034, registering a CAGR of 4.6%. Market growth is being driven by biotechnology-enabled aroma molecules, clean-label flavor compounds, plant-based formulation demand, and premium fragrance development across cosmetics, personal care, beverages, and functional foods. Synthetic aroma chemicals, fermentation-derived terpenes, high-intensity flavor modulators, and natural-identical fragrance ingredients remain core revenue streams, while regulatory compliance and sustainability metrics increasingly shape R&D pipelines.

In February 2026, dsm-firmenich finalized a definitive agreement to divest its Animal Nutrition & Health business to CVC Capital Partners, sharpening its positioning as a consumer-centric Taste, Texture, and Health specialist. In January 2026, Symrise AG announced the divestment of its terpenes business, reallocating capital toward high-growth cosmetic ingredients and pet palatability solutions while initiating a €400 million share buy-back program. During late 2025 and early 2026, International Flavors & Fragrances formally launched the sale of its Food Ingredients segment, confirming by February 2026 a strategic portfolio restructuring focused on higher-margin Scent and Health & Biosciences divisions. In December 2025, dsm-firmenich introduced “Frosted Star Anise” as its 2026 Flavor of the Year, leveraging cooling sensory technology and sweet-spicy licorice notes aligned with evolving consumer wellness positioning.

Expansion activity intensified in 2025 across Asia-Pacific and the Americas. In October 2025, dsm-firmenich opened a global food innovation center in Delft dedicated to flavor and texture development for plant-based dairy and meat alternatives. In September 2025, Givaudan broke ground on a CHF 40 million Fragrance & Beauty facility in Guangzhou, incorporating automated production lines and creative labs to serve China’s fast-growing cosmetics sector. That same month, Givaudan completed acquisition of a majority stake in Brazil-based Vollmens Fragrances, strengthening regional customization capabilities in Latin America. In October 2025, Givaudan announced plans to acquire US fragrance house Belle Aire Creations, targeting expansion in the North American mid-market segment with incremental annual sales contribution.

Biotechnology integration has accelerated since early 2024. The January 2024 merger of Novozymes and Chr. Hansen to form Novonesis created a large-scale fermentation platform supporting natural flavor enhancers and enzyme-driven taste modulation systems. In March 2024, BASF expanded its Isobionics® biotechnology portfolio with Natural beta-Caryophyllene 80, a fermentation-derived flavor and fragrance molecule offering high purity and sustainable sourcing advantages over traditional extraction methods. Across 2024 and 2025, T. Hasegawa USA completed acquisition of Abelei Flavors to enhance North American formulation capabilities, later identifying “Dark Sweet Cherry” as a primary flavor trend driver in beverage and confectionery innovation. In 2025, MANE Group strengthened its R&D platform by acquiring ChemoSensoryx Biosciences, integrating advanced neuroscientific tools to study olfactory-limbic system interactions and emotional scent mapping in premium fragrance development.

Trends and Opportunities in the Flavors and Fragrances Chemicals Market

Precision Biotechnology for Scaling Rare and Sustainable Aroma Molecules

The industry is rapidly shifting toward precision fermentation to stabilize access to rare, climate-sensitive, and geopolitically exposed natural ingredients. Traditional agricultural extraction methods for aroma chemicals face volatility from climate events, land constraints, and biodiversity regulations, making biomanufacturing a strategic necessity rather than an experimental option.

In January 2025, the European Investment Bank committed €35 million to Formo to support the industrial-scale fermentation of high-value proteins and bio-identical flavor precursors. This investment underscores institutional confidence in fermentation as a long-term solution for specialty ingredients supply chains, particularly for dairy-associated and protein-linked flavor compounds.

Regulatory validation is accelerating commercialization. In early 2025, the U.S. FDA issued a No Questions letter granting GRAS status to Onego Bio’s precision-fermented Bioalbumen. This milestone confirmed that fermentation-derived ingredients can directly replace animal-based or resource-intensive botanical inputs in global flavor formulations without regulatory friction, opening the door for wider adoption by multinational food and beverage manufacturers.

Corporate R&D investment is also scaling. In May 2025, Layn Natural Ingredients inaugurated an expanded biotechnology facility focused on advanced biocatalysis. The site is dedicated to producing beta-glucans and rare botanical replicas with significantly lower environmental footprints than conventional extraction, aligning flavor ingredient portfolios with sustainability and traceability expectations from global brand owners.

AI-Driven Formulation and Predictive Sensory Modeling as Core Infrastructure

Artificial intelligence has moved from experimental pilots to a foundational capability within leading flavor and fragrance houses. AI platforms are now shortening formulation timelines, improving regulatory compliance, and enabling predictive consumer acceptance across regions.

In late 2024, Osmo launched Generation, the world’s first AI-powered fragrance house. Using proprietary Olfactory Intelligence, the platform translates molecular structures into scent outcomes, allowing the creation of allergen-conscious and regulation-ready fragrances that comply with evolving EU REACH standards introduced in 2025.

Established leaders are embedding AI deeply into their creative workflows. By 2025, Givaudan and DSM-Firmenich were using AI systems to analyze databases exceeding 100,000 historical formulas. These tools generate cost-optimized and naturality-focused formulation frameworks before human perfumers refine them, enabling faster response to customer briefs while maintaining margin discipline.

Market-facing validation has also improved. Symrise, through its Philyra platform developed with IBM, demonstrated in 2025 that AI models can forecast consumer acceptance in emerging markets such as Brazil and China with accuracy exceeding 90%. This capability is reshaping go-to-market strategies by reducing the risk of failed regional launches.

Functional Flavors for Off-Note Masking in Alternative Proteins

The rapid expansion of plant-based and precision-fermented proteins is creating sustained demand for advanced masking and modulation chemistries. Pea, chickpea, duckweed, and fungi-derived proteins often exhibit bitter, grassy, or metallic off-notes that limit repeat consumption if not effectively addressed.

Industry technical briefs from 2025 indicate a 25 to 30% increase in demand for bitterness blockers and modulators designed to interact selectively with taste receptors. Solutions such as stevia-derived sweetness modulators are being engineered to suppress bitterness signals while maintaining clean-label positioning, allowing manufacturers to reduce sugar and sodium without compromising palatability.

Savory flavor innovation is a parallel growth engine. In November 2025, DSM-Firmenich announced advances in grilled meat tonalities for plant-based products. These systems combine precision-fermented heme analogs with yeast extracts to replicate Maillard reaction-driven umami and fatty mouthfeel, addressing one of the most persistent sensory gaps in meat alternatives.

Functional ingredient synergies are also expanding. Botanical aromatics such as lavender, cardamom, and rosemary are increasingly used not only for flavor and fragrance but as functional masking agents in stress-support beverages. In 2025, these botanicals played a key role in neutralizing the earthy notes of adaptogenic mushrooms and mineral fortifications, enabling premium positioning in the wellness beverage segment.

Scent-as-a-Service and Olfactory Branding for the Experience Economy

The rise of the experience economy is transforming fragrance from a product input into a service-driven revenue stream. Scent marketing and olfactory branding are gaining traction in hospitality, automotive, retail, and premium real estate, creating new demand for technical fragrance delivery systems.

By 2025, the global scent marketing segment was on a trajectory toward a projected valuation of $6.4 billion by 2033. Hospitality leaders such as Marriott and Hilton have deployed signature scents through HVAC-integrated systems to strengthen brand recall, with internal studies showing improvements in customer return rates of up to 20%.

This opportunity is highly technical. Growth is concentrated in microencapsulated, non-staining fragrance systems designed for smart diffusers and high-pressure aerosolization. These formulations must retain olfactory integrity while complying with indoor air quality standards, driving demand for advanced encapsulation chemistries and low-volatility aroma molecules.

Neuroscience-backed scent design is further elevating value creation. Research cited by major fragrance houses in 2025 confirms that specific scent profiles can induce emotional states such as calm, focus, or confidence in commercial spaces. This has led to the emergence of olfactory branding as a multidisciplinary service, where fragrance chemists collaborate with architects and interior designers to embed scent-as-a-service into premium residential, retail, and workplace environments.

Flavors and Fragrances Chemicals Market Share and Segmentation Insights

Aroma Chemicals Dominate Flavor and Fragrance Formulations Through Consistency and Scalable Production

Aroma Chemicals accounted for 48.60% of the Flavors and Fragrances Chemicals Market share in 2025, making them the leading chemical category in modern sensory formulation. These compounds include synthetic and nature-identical molecules such as vanillin, menthol, linalool, citronellol, and benzyl acetate, which serve as the foundational ingredients used by flavorists and perfumers to create precise taste and scent profiles across food, beverage, personal care, and household products. Aroma chemicals dominate because they provide consistent purity, stable pricing structures, and predictable sensory performance, all of which are critical for large-scale manufacturing where natural ingredient variability can compromise formulation stability. In 2025, the sector is experiencing a major shift driven by biotechnology-based aroma production technologies. Fermentation and biocatalytic synthesis are increasingly used to produce high-demand molecules such as vanillin, nootkatone, and rose ketones, offering an alternative to traditional petrochemical synthesis or plant extraction. These bio-based aroma chemicals enable manufacturers to label ingredients as “nature-identical” or naturally derived, improving sustainability credentials while ensuring supply chain stability for high-volume flavor and fragrance ingredients. This biotechnology-driven production model is rapidly transforming the global aroma chemicals value chain.

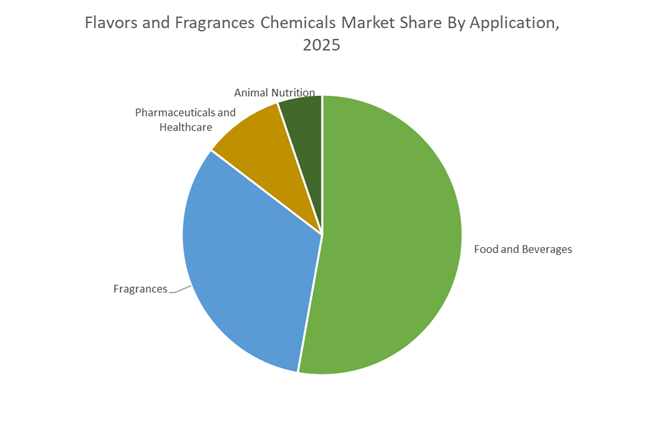

Food and Beverage Industry Drives the Largest Demand for Flavor Chemistry Innovation

Food and Beverages represented 52.80% of the Flavors and Fragrances Chemicals Market share in 2025, making it the most significant application segment within the global flavor chemistry ecosystem. Flavor chemicals play an essential role in nearly every processed food and beverage category, including soft drinks, dairy products, bakery items, confectionery, savory snacks, sauces, and ready-to-eat meals. These ingredients are used to deliver consistent taste profiles, product differentiation, and consumer sensory satisfaction, which are critical factors in competitive food markets. The industry’s reliance on flavor chemistry continues to grow as consumer demand for new taste experiences, ethnic flavor profiles, and premium sensory formulations accelerates product innovation cycles. A key market development in 2025 is the rapid expansion of health and wellness-driven flavor reformulation technologies. As global food manufacturers reduce sugar, sodium, and fat levels to comply with health regulations and consumer nutrition trends, flavor chemists are developing advanced taste modulation systems to preserve product palatability. These include bitterness blockers for plant proteins, salt enhancers for low-sodium foods, and sweetness potentiators that amplify perceived sweetness in reduced-sugar beverages. Such technologies allow manufacturers to maintain desirable sensory experiences while meeting evolving nutrition and clean-label standards, reinforcing the central role of flavor chemistry in the global food innovation landscape.

Competitive Landscape in Flavors and Fragrances Chemicals Market

Givaudan Strengthens Digital-First Leadership in Fine Fragrance and Taste Innovation

Givaudan remains the global market leader in flavors and fragrance chemicals, closing its 2025 Strategy ahead of targets with full-year 2025 sales of CHF 7.5 billion and a 5.1% like-for-like growth rate. The company maintained a robust EBITDA margin of 23.4%, reflecting operational efficiency and premium portfolio positioning. Fine Fragrance delivered 18.3% growth in 2025, reinforcing Givaudan’s dominance in high-end perfumery and luxury scent compounds. Its AI-assisted formulation tool, Carto, enables advanced olfactive palette optimization and accelerates digital scent design workflows. In March 2026, leadership transitioned from Gilles Andrier to Christian J. J. Mauer, marking the launch of a 2030 Strategy centered on digital-first creation and disciplined capital allocation. Under its Predictable Compounder model, Givaudan targets 4 to 6% organic growth and a 12% free cash flow margin through 2030, consolidating its premium positioning in the global fragrance ingredients and flavor solutions market.

dsm-firmenich Completes Transformation into Consumer-Focused Fragrance and Taste Leader

dsm-firmenich, formed through the DSM and Firmenich merger, accelerated portfolio optimization throughout 2025 to become a focused leader in nutrition, health, and beauty ingredients. In February 2026, the company finalized the €2.2 billion divestment of its Animal Nutrition and Health business, sharpening its concentration on Perfumery and Beauty, Taste, Texture and Health, and Health, Nutrition and Care. By the end of 2025, total realized synergies reached €350 million, driving adjusted EBITDA margins toward the 22 to 23% mid-term target. The company expanded aggressively in the Middle East, launching a new fragrance range in Riyadh in early 2026 to capture regional demand growth. dsm-firmenich remains a pioneer in biotech-derived aroma molecules such as Clearwood®, reflecting its leadership in sustainable fragrance chemistry. Through disciplined restructuring and biotechnology integration, the company strengthens its competitive edge in high-value scent and flavor creation.

IFF Executes Portfolio Reset to Reinforce Core Scent and Taste Technologies

International Flavors and Fragrances reported full-year 2025 net sales of $10.89 billion, with comparable currency-neutral growth of 2% despite a 5% decline in reported sales due to divestitures. The company initiated a formal sale process for its Food Ingredients segment in early 2026, following the $2.85 billion divestment of its Pharma Solutions business in 2025. This restructuring supports its Tighter Focus, Stronger Margins strategy aimed at deleveraging the balance sheet, with net debt to EBITDA reduced to 2.6x. Fine Fragrance sales rose 20% in 2025, underscoring renewed emphasis on premium scent technologies. IFF also introduced the Tastepoint 2026 Trend Forecast, leveraging AI and social listening analytics to anticipate emerging flavor profiles such as neuro-gastro concepts tied to mental wellness. Through asset rationalization and reinvestment in core fragrance ingredients and taste modulation systems, IFF is repositioning for margin expansion and innovation-led growth.

Symrise AG Leverages Diversified Portfolio and Circular Economy Integration

Symrise AG reported 2025 sales exceeding €4.7 billion and sustained an EBITDA margin of approximately 21.5% despite macroeconomic volatility. The company’s diversified structure integrates Scent and Care with Taste, Nutrition and Health, enabling cross-functional innovation in cosmetic actives, sunscreen filters, and micro-protection technologies. Symrise maintains a dominant presence in pet food palatability while expanding its natural taste molecules portfolio. The ONE SYM Transformation program launched in late 2025 aims to deliver €40 million in annual cost savings by the end of 2026, strengthening operational efficiency. A defining competitive advantage is its Full Side-Stream Valorization model, converting food production by-products into high-value natural aroma compounds and flavor enhancers. This circular sourcing strategy enhances sustainability credentials and secures raw material resilience within the global flavors and fragrance chemicals industry.

Mane SA Expands Natural Extraction and Encapsulation Capabilities in Asia

Mane SA remains the largest family-owned entity in the flavors and fragrances chemicals market, distinguished by long-term investment cycles and expertise in botanical extraction. In October 2025, the company initiated Phase II of its Pinghu production facility in China, a $70 million expansion projected to increase annual capacity by 17,000 tons by 2027. Mane is recognized for advanced encapsulation technologies such as E-Pure and Sense Capture, enabling controlled and prolonged scent release in laundry detergents and household care applications. Its strategic emphasis on independence and vertical integration ensures direct control over botanical and spice raw materials, reinforcing quality assurance in natural flavor and fragrance formulations. Mane holds a strong position in the Savory and Snacks segment across EMEA and continues expanding its Fine Fragrance Creation Center in China to support regional luxury brand growth. Through sustained capital investment and natural ingredient leadership, Mane strengthens its competitive stance in the global flavor and fragrance ingredients market.

India: Natural Labeling, AI-Driven Fragrance Design, and Biomanufacturing Scale-Up

India’s flavors and fragrances chemicals ecosystem is undergoing a structural upgrade driven by regulation, localization of innovation, and biotechnology-led manufacturing. The late-2024 amendment by the Food Safety and Standards Authority of India (FSSAI) to the Food Product Standards and Additives Regulations, implemented through 2025, has tightened the definition and labeling of “natural flavors.” This shift is compelling food and beverage manufacturers to accelerate the substitution of synthetic aroma chemicals with plant-derived and fermentation-based alternatives, particularly in beverages, dairy analogues, and packaged foods. As a result, demand is rising for traceable terpenes, essential oil fractions, and bio-identical flavor molecules that meet the revised compliance framework while maintaining sensory consistency.

On the innovation front, Symrise inaugurated its Bangalore Innovation Center in May 2025, positioning India as a regional R&D nucleus for culturally resonant taste and scent profiles. The facility integrates Ayurvedic knowledge systems with modern analytical chemistry to develop localized fragrance accords and flavor actives. Parallelly, the BioE3 Policy has enabled the launch of biomanufacturing hubs that support precision fermentation for fragrance intermediates such as bio-based musks and lactones. A notable strategic shift is Unilever’s in-house fragrance hub, backed by a €100 million investment, which uses AI-enabled scent design to internalize fragrance IP creation for global FMCG brands. Together, these moves are transforming India from a cost-efficient production base into a formulation and innovation center for global flavor and fragrance supply chains.

European Union (France and Germany): Allergen Transparency and Fluorine-Free Reformulation

The European Union remains the global regulatory benchmark for the flavors and fragrances chemicals market, with France and Germany setting the pace on compliance-driven innovation. Regulation (EU) 2023/1545 marks a fundamental inflection point, with the transition period for labeling 56 additional fragrance allergens ending on July 31, 2026. From this deadline, manufacturers must disclose these allergens when concentrations exceed 0.001% in leave-on and 0.01% in rinse-off products. This requirement is forcing aroma chemical suppliers to reformulate complex accords, invest in allergen-reduced alternatives, and upgrade analytical testing for ultra-low detection thresholds.

France’s January 2026 ban on PFAS in cosmetic formulations is further accelerating the shift toward silicon-free and fluorine-free fragrance delivery systems. In response, European suppliers are prioritizing encapsulation technologies based on biodegradable polymers and carbohydrate matrices. Innovation capacity is being reinforced by DSM-Firmenich, which opened its global food innovation center in Delft in October 2025 to advance taste-modulating chemicals for plant-based proteins. Additionally, the mandatory adoption of the updated INCI Glossary by July 30, 2026 introduces 348 new ingredient entities, tightening nomenclature control and raising entry barriers for non-compliant suppliers. Collectively, these measures are consolidating the EU market around high-purity, well-documented, and regulation-ready fragrance and flavor chemicals.

United States: Compliance Digitization and Clean-Label Scent Positioning

In the United States, the enforcement phase of the Modernization of Cosmetics Regulation Act (MoCRA) throughout 2025 has reshaped operational priorities for flavor and fragrance chemical manufacturers. Enhanced requirements for fragrance allergen disclosure, mandatory facility registration, and adverse event reporting are pushing suppliers to implement end-to-end digital traceability systems. This regulatory environment favors large, compliance-ready players with integrated quality systems, while smaller suppliers face rising barriers to market participation.

Innovation is simultaneously shifting toward fermentation-derived and natural positioning. The FDA’s 2025 “No Questions” letter granting GRAS status to Bioalbumen has opened new formulation pathways, enabling fermented proteins to be used as flavor carriers and mouthfeel enhancers. In the fine fragrance segment, Young Living launched Wyld Notes in February 2025, signaling growing consumer demand for clean-label and naturally positioned scents. Supply-side resilience is being strengthened by Kao Corporation, which completed its tertiary amine facility in Pasadena, Texas, in August 2025 to secure domestic production of intermediates used in fragrance stabilizers. The U.S. market is thus evolving toward transparency-led compliance combined with premium natural and biotech-enabled differentiation.

China: Export-Oriented Flexibility and AI-Enabled Sensory Design

China’s flavors and fragrances chemicals market is leveraging regulatory flexibility and digital innovation to strengthen its global export position. In late 2025, the Ministry of Agriculture and Rural Affairs streamlined “export-only” chemical registration, allowing manufacturers to produce novel aroma chemicals and flavor precursors for overseas markets ahead of domestic approval. This policy is particularly advantageous for suppliers targeting Southeast Asia, Latin America, and the Middle East, where demand for cost-competitive yet compliant aroma chemicals is rising.

Manufacturing and blending sophistication is also increasing. Adisseo’s 37KT Specialty Blending Facility in Nanjing, ramped up in 2025, is increasingly utilized for advanced flavor-enhancing palatants in livestock and pet food applications. On the consumer side, Givaudan’s “Guardians of Memories” digital initiative showcased at VivaTech 2025 demonstrates how AI is being used to translate Chinese consumer scent preferences into market-ready formulations. These developments position China as a hybrid hub, combining scale manufacturing with data-driven sensory customization for global clients.

United Arab Emirates: Premium Perfumery and Circular Bioeconomy Alignment

The UAE is emerging as a strategic hub for premium fragrances and sustainable aroma chemical production. In 2025, Mane established its regional headquarters in Dubai, underscoring the region’s importance in Arabic perfumery built around oud, amber, and vanilla accords. This hub enables rapid customization for Middle Eastern preferences while serving as a gateway to African and South Asian markets.

At the policy level, the UAE’s Operation 300bn strategy is channeling public funding into circular bioeconomy projects. Grants announced in 2025 support industrial-scale fermentation units for producing bio-solvents used in perfume extraction and aroma isolation. This alignment of luxury perfumery demand with bio-based processing positions the UAE as a high-margin, innovation-driven node in the global flavors and fragrances chemicals value chain.

Strategic Summary: Flavors and Fragrances Chemicals Market by Country (2025–2026)

Flavors and Fragrances Chemicals Market County Level Snapshot

|

Region

|

Primary Policy or Strategic Driver

|

Technology Focus

|

Market Implication

|

|

India

|

Natural flavor labeling and BioE3

|

Precision fermentation and AI scent design

|

Rapid shift to plant-based and bio-identical molecules

|

|

European Union

|

Allergen disclosure and PFAS bans

|

Allergen-reduced, fluorine-free systems

|

High compliance costs, premium reformulations

|

|

United States

|

MoCRA enforcement

|

Digital traceability and clean-label scents

|

Consolidation around compliance-ready suppliers

|

|

China

|

Export-only registration and AI

|

Data-driven sensory formulation

|

Competitive export-oriented growth

|

|

UAE

|

Operation 300bn and luxury perfumery

|

Bio-solvents and premium aroma chemicals

|

High-margin niche leadership

|

Flavors and Fragrances Chemicals Market Report Scope

Flavors and Fragrances Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.5 Billion

|

|

Market Size (2034)

|

$23.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Chemical Type (Aroma Chemicals, Essential Oils, Extracts and Oleoresins), By Source (Natural, Synthetic), By Form (Liquid, Powder, Encapsulated), By Application (Food and Beverages, Fragrances, Pharmaceuticals and Healthcare, Animal Nutrition)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Givaudan, DSM-Firmenich, International Flavors & Fragrances Inc., Symrise AG, Takasago International Corporation, Mane SA, Sensient Technologies Corporation, T. Hasegawa Co., Ltd., Robertet Group, Kerry Group plc, BASF SE, Huabao International Holdings, Treatt plc, Solvay S.A., Kao Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flavors and Fragrances Chemicals Market Segmentation

By Chemical Type

- Aroma Chemicals

- Essential Oils

- Extracts and Oleoresins

By Source

By Form

- Liquid

- Powder

- Encapsulated

By Application

- Food and Beverages

- Fragrances

- Pharmaceuticals and Healthcare

- Animal Nutrition

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Flavors and Fragrances Chemicals Industry

- Givaudan

- DSM-Firmenich

- International Flavors & Fragrances Inc.

- Symrise AG

- Takasago International Corporation

- Mane SA

- Sensient Technologies Corporation

- T. Hasegawa Co., Ltd.

- Robertet Group

- Kerry Group plc

- BASF SE

- Huabao International Holdings

- Treatt plc

- Solvay S.A.

- Kao Corporation

*- List not Exhaustive