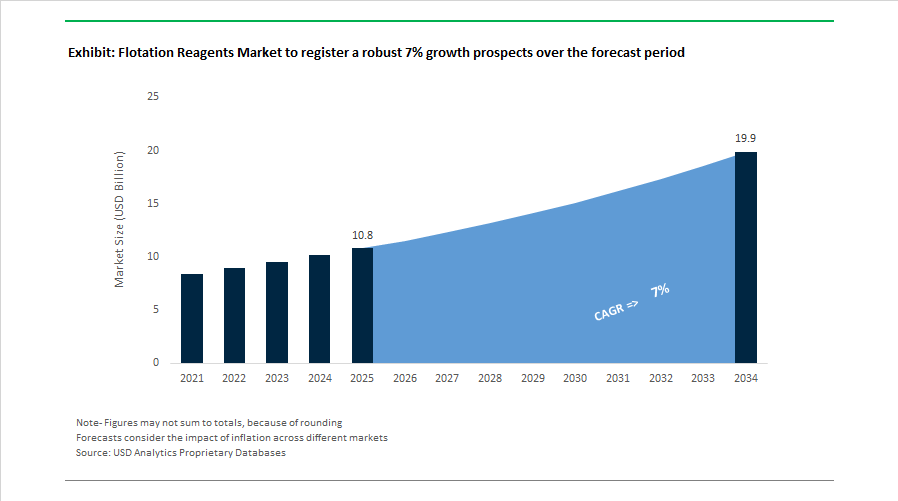

Flotation Reagents Market Size 2025–2034: $10.8 Billion to $19.9 Billion at 7% CAGR Driven by Lithium, AI Dosing and Xanthate Replacement

The Flotation Reagents Market is projected to expand from $10.8 billion in 2025 to $19.9 billion by 2034, registering a robust CAGR of 7%. Growth is underpinned by rising global demand for copper, nickel, lithium, phosphate, and gold, alongside increased processing of lower-grade ores that require higher reagent intensity and optimized froth chemistry. Collectors, frothers, dispersants, depressants, and flotation modifiers remain core product categories, with increasing emphasis on environmental, health, and safety compliance, reagent efficiency, and digitalized dosing control. The shift toward battery minerals and sustainable mining practices is accelerating innovation in selective collectors and bio-based surface modifiers.

In early 2026, the European Chemicals Agency implemented stricter reporting and usage guidelines for certain sulfhydryl collectors, including selected xanthate derivatives, due to environmental persistence concerns. This regulatory tightening has intensified “xanthate replacement” programs across European base metal and precious metal concentrators, driving adoption of alternative collectors and low-toxicity frothers. In October 2025, Syensqo launched SmartFloat, an artificial intelligence platform designed to optimize flotation reagent dosing in real time by analyzing ore variability, froth stability, and recovery metrics. In 2025, Syensqo also introduced Transfoamer™, an adaptive frother technology engineered to modulate performance based on slurry pH, improving coarse particle recovery while reducing reagent overuse.

At the Flotation 2025 conference in Cape Town, Clariant Mining Solutions unveiled novel spodumene collectors tailored for lithium extraction from hard-rock deposits, addressing escalating demand from electric vehicle battery supply chains. During 2025, SNF Group expanded its polyacrylamide production hub in Oman to support Middle Eastern and African phosphate and gold operations, where water scarcity and high-efficiency solid-liquid separation demand advanced polymer systems integrated with flotation circuits. In November 2024, Solenis completed the acquisition of BASF’s mining flocculants business, incorporating brands such as Magnafloc®, Rheomax®, and Alclar®, strengthening its presence in mineral processing chemistry and tailings management.

Earlier in 2024, Clariant inaugurated its $100 million mining chemicals facility in Indonesia, localizing production of xanthates and specialty collectors to serve nickel and copper expansion projects across Asia-Pacific. In early 2024, BASF introduced the Luprofroth® and Luproset® reagent families, engineered to provide improved environmental and safety profiles compared to conventional MIBC-based frothers. Integration of flotation chemistry with digital mine water management also advanced following Nalco Water’s acquisition of Flottec, completed in late 2023 and fully integrated through 2024, expanding specialized frother and collector offerings within whole-of-mine service platforms. The January 2024 formation of Novonesis introduced enzymatic and bio-based flotation modifiers into pilot programs, reflecting early-stage adoption of biotechnology-driven surface chemistry aimed at reducing synthetic surfactant dependence in mineral beneficiation.

Trends and Opportunities in the Flotation Reagents Market

Selective Chemistry for Complex Polymetallic and Fine-Particle Recovery

As easily beneficiated ores are depleted, mining companies are increasingly processing complex polymetallic deposits and finely disseminated mineral systems that demand ore-specific reagent design. The focus has shifted from generic xanthate-based systems to high-selectivity collectors and modifiers capable of operating under narrow pH and redox windows.

A February 2025 optimization program on a silver-bearing copper–molybdenum ore in Xizang demonstrated the commercial value of this approach. By deploying a strong selective collector (BK-345) under low-alkalinity conditions, operators achieved a 16.4 percentage point increase in molybdenum recovery versus conventional mixed flotation routes. This result highlights how modern collectors can unlock secondary metal value that is typically suppressed in traditional high-pH circuits.

Fine-particle recovery has become another defining trend. By late 2025, plants combining microbubble generation with engineered surfactants designed for particles below 5 microns were reporting copper recoveries approaching 90% in ores previously classified as uneconomic. This is materially improving project economics in porphyry and low-grade disseminated deposits.

Digitalization is reinforcing this precision shift. In October 2025, Solvay introduced its SmartFloat platform, an AI-enabled system that dynamically adjusts reagent dosing based on real-time ore mineralogy and throughput data. Early deployments indicate reagent savings of 10–15% while maintaining stable concentrate grades, a critical advantage in high-capacity milling operations where variability directly impacts downstream smelting penalties.

Sustainability-Driven Phase-Out of Xanthates and Cyanides

Environmental compliance is accelerating the transition away from xanthates, cyanides, and sodium hydrosulfide toward reagents with lower aquatic toxicity, improved biodegradability, and safer handling profiles. By mid-2025, low-impact flotation chemistries accounted for roughly 32% of new reagent installations, reflecting both regulatory pressure and long-term liability management strategies.

In North America and Canada, legacy sites face heightened scrutiny under frameworks such as CERCLA, pushing operators to adopt reagents that minimize acid mine drainage risks. Fatty-acid-based collectors and bio-derived frothers are increasingly specified, particularly in operations with long closure horizons.

Replacement of sodium hydrosulfide is gaining momentum in copper–molybdenum separation. In December 2025, Clariant expanded its FLOTICOR DP range, enabling full NaSH substitution. These alternatives improve operator safety, offer longer shelf life, and reduce environmental exposure without sacrificing metallurgical performance.

Water scarcity is amplifying this trend. Studies published in 2025 show that biodegradable frothers can cut reagent consumption by up to 50% in closed-loop water circuits. This is particularly relevant in arid mining regions such as Chile and Western Australia, where water reuse is now a permitting prerequisite rather than an operational choice.

Economic Recovery of Critical Minerals from Mine Tailings

Reprocessing historical tailings is emerging as a strategic growth opportunity as governments seek domestic sources of cobalt, nickel, and rare earth elements without the environmental footprint of new greenfield mines. According to International Energy Agency, investment interest in secondary recovery intensified in 2025, particularly for lithium and copper, even as exploration spending plateaued elsewhere.

Modern reprocessing relies on highly selective thionocarbamates and dithiophosphinates to recover oxidized residual metals from aged tailings. These surfaces behave differently from fresh sulfides, creating a clear innovation gap for reagent suppliers capable of tailoring adsorption behavior to weathered mineralogy.

Environmental performance is a parallel driver. At Eldorado Gold’s Skouries project in Greece, where Phase 2 construction reached 73% completion by Q3 2025, filtered tailings technology is being used to maximize water recycling. This has created demand for advanced dewatering aids and flotation reagents that reduce tailings footprint by up to 40% while maintaining metal recovery.

In the Democratic Republic of Congo, cobalt recovery from copper–cobalt ores is emerging as a high-margin niche. By late 2025, the strongest growth was concentrated in ultra-selective reagent regimes that can differentiate cobalt-bearing phases from conventional sulfides, positioning this segment as a key innovation frontier.

Reagent Integration in Direct Lithium Extraction

Direct Lithium Extraction is rapidly reshaping chemical demand in brine-based lithium projects. By October 2025, around 35% of new lithium developments were expected to adopt DLE technologies, replacing slow evaporation ponds with modular, year-round processing.

These systems rely heavily on chemical pre-treatment. Aluminum-based sorbents used in adsorption DLE and manganese or titanium resins used in ion-exchange DLE require precise pH control, impurity removal, and surface conditioning. This creates sustained demand for specialty coagulants, modifiers, and surfactants that remove boron, magnesium, and calcium before lithium capture.

In May 2025, Evonik demonstrated electrochemical lithium extraction from DLE eluates, underscoring the role of advanced surfactants and membranes in next-generation lithium flowsheets. Unlike evaporation ponds that typically yield 40–60% recovery over 12–18 months, DLE systems supported by optimized reagent packages can exceed 90% recovery in a matter of days.

This speed and efficiency are strategically critical for battery supply chains in Europe and North America. As gigafactories seek secure, low-carbon lithium supply, reagent suppliers that embed themselves early into DLE process design are well positioned to secure long-term, high-value contracts.

Flotation Reagents Market Share and Segmentation Insights

Collector Reagents Lead Mineral Processing Chemistry with Selectivity-Focused Innovations

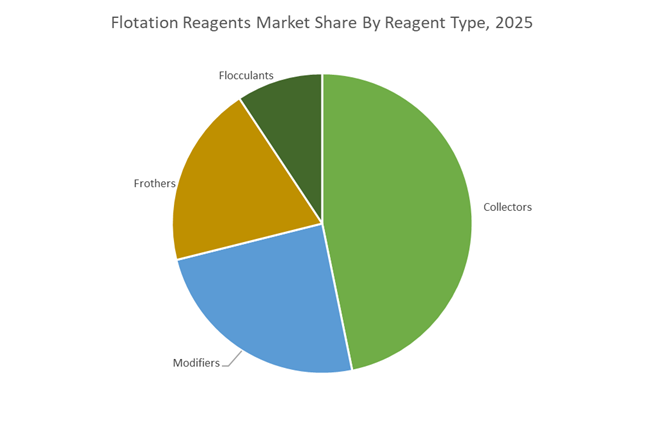

Collectors accounted for 46.80% of the Flotation Reagents Market share in 2025, making them the most critical reagent category used in modern mineral flotation circuits. Collectors are specialized chemical compounds that modify the surface properties of target minerals, rendering them hydrophobic so they can attach to air bubbles and rise to the froth layer during flotation. This process forms the core mechanism of froth flotation technology, which is widely used to concentrate sulfide ores and separate valuable minerals from surrounding gangue material. Common collector chemistries include xanthates, dithiophosphates, thiocarbamates, and specialty sulfur-based reagents, which are tailored to interact with specific mineral surfaces. In 2025, collector development is increasingly focused on enhancing mineral selectivity, driven by declining ore grades and growing mineralogical complexity in global mining operations. Advanced collector formulations are designed to selectively target valuable minerals such as copper sulfides, zinc sulfides, rare earth minerals, and lithium-bearing spodumene, while minimizing unwanted gangue flotation. These innovations enable mining companies to improve recovery rates, reduce reagent consumption, and optimize flotation circuit efficiency, reinforcing collectors as the most strategically important product category in the global flotation reagents market.

Base Metal Mining Drives the Largest Consumption of Flotation Reagents in Global Mineral Processing

Base Metal Mining represented 52.80% of the Flotation Reagents Market share in 2025, making it the dominant application segment across the global mineral processing industry. Base metals such as copper, zinc, lead, and nickel are produced at massive industrial scale, and froth flotation remains the primary beneficiation method used to concentrate these sulfide ores. Mining operations rely heavily on specialized flotation reagent suites—including collectors, frothers, modifiers, and flocculants—to maximize mineral recovery and maintain efficient processing of increasingly complex ore bodies. In 2025, demand for flotation reagents is being strongly influenced by the global energy transition and the growing importance of battery and technology metals. Copper continues to dominate base metal mining due to its central role in electric vehicles, renewable energy infrastructure, and electrical grid expansion, but the market is also seeing increased mining activity for nickel and cobalt, which are essential for lithium-ion battery production. As ore bodies become more complex and polymetallic, flotation circuits are being redesigned with customized reagent programs tailored to specific mineral assemblages and processing conditions. This trend is driving higher consumption of advanced flotation reagents, reinforcing base metal mining as the largest demand center in the global flotation reagents market.

Competitive Landscape in Flotation Reagents Market

Solvay Strengthens Leadership in High-Selectivity Sulfide Collectors

Solvay remains the global leader in mineral processing chemicals through its legacy Cytec mining portfolio, particularly in high-selectivity sulfide flotation reagents. Its AERO® and AEROPHINE® collector brands are widely recognized as industry standards for copper, zinc, and complex polymetallic ore beneficiation. In February 2026, Solvay reported underlying full-year 2025 sales of €4.3 billion while maintaining a solid EBITDA margin of 20.7% despite uneven global mining demand. Following the Syensqo demerger, the company is executing a Pure-Play Essential Chemistry strategy focused on operational efficiency and optimized allocation of CO2 emission rights ahead of 2030 targets. Solvay has also expanded its footprint in Chile and Peru to support rising production of green copper required for renewable energy infrastructure and electric vehicles. Its technical expertise in phosphine-based collectors and established relationships in the Latin American copper belt reinforce its dominant position in high-performance flotation reagents.

Clariant Advances Critical Minerals Flotation and Coarse Particle Technologies

Clariant is positioning itself as a purpose-driven innovator in flotation reagents for critical minerals such as lithium, cobalt, and phosphate. Its HOSTAFLOAT® and FLOTIGAM® product lines include tailored collectors for spodumene flotation and specialty phosphate beneficiation. At the Flotation 2025 conference, Clariant introduced advanced Coarse Particle Flotation technologies, enabling reduced grinding intensity and potential greenhouse gas reductions of up to 20% at mine sites. The company reported 2025 sales of CHF 3.9 billion, with its Decarbonization Minerals Program accounting for a growing share of mining-related revenue, particularly through xanthate-replacement collector systems. Clariant has streamlined lower-margin commodity reagent lines while maintaining focus on high-value specialty flotation chemicals. This strategic shift enhances its exposure to battery metals and energy transition minerals, reinforcing its competitive standing in sustainable mineral processing chemistry.

BASF Expands Sustainable Frother and Modifier Technologies

BASF leverages its integrated chemical production network to deliver cost-effective flotation frothers, modifiers, and activators under the Luprofroth™, Luproset™, and Lupromin® brands. The recent launch of Gold Activator Luproset A 1127 improves gold recovery efficiency at lower dosage rates compared to conventional activators, addressing cost pressures in gold mining operations. Backward integration into raw material feedstocks provides stability against supply disruptions that affected the market during 2024 and 2025. Under its Green Transformation roadmap for 2026, BASF prioritizes sustainable mining reagents with enhanced environmental, health, and safety profiles and reduced ecotoxicity. By aligning flotation chemistry with stricter global environmental standards, BASF strengthens its appeal among large mining operators seeking performance optimization alongside regulatory compliance.

Chevron Phillips Chemical Dominates Sulfur-Based Collectors in North America

Chevron Phillips Chemical holds a strong position in hydrocarbon-based and sulfur-based collectors, particularly for molybdenum and copper flotation circuits. Its Orfom® and Molyflo® brands are widely used in sulfide mineral processing, while Orfom® D8 provides an alternative to sodium hydrosulfide in copper-moly separation, reducing operator exposure to hazardous chemicals. North America accounts for approximately 35% of global flotation reagents revenue, where CPChem maintains steady market share. The company has expanded its Philflo® flotation oils portfolio to enhance recovery of coarse potash and phosphate particles at lower dosage levels compared to diesel or kerosene. Integration with its petrochemical infrastructure ensures secure supply of high-purity mercaptans and sulfur-based intermediates critical for high-selectivity collectors. This structural integration reinforces CPChem’s leadership in sulfur chemistry for mineral beneficiation.

Kemira Integrates Flotation Chemistry with Water Scarcity Solutions

Kemira differentiates itself in the flotation reagents market by combining solid-liquid separation polymers with advanced water treatment chemistry. Its high-performance flocculants and coagulants address tailings thickening and water recycling bottlenecks in mining operations. In July 2025, Kemira invested in new production lines to support increased demand for coagulants in Zero Liquid Discharge systems, particularly in water-stressed regions such as Australia and Chile. Under its Water Scarcity Solutions strategy, the company bundles flotation reagents with water reuse chemistries to improve overall process efficiency. Kemira’s A- rating in the 2025 CDP Water Security rankings highlights its leadership in sustainable mining water management. By integrating flotation performance with water conservation technologies, Kemira secures a differentiated position in environmentally constrained mining markets.

SNF Expands Volume Leadership in Flocculant and Collector Overlap

SNF Group leverages its dominance in water-soluble polymers to capture significant share in the overlap between flotation reagents and tailings management chemistry. Its FLOPAM™ polyacrylamide range is widely applied in mineral thickening and dewatering, supporting efficient solid-liquid separation in large-scale mining operations. The company also produces specialized xanthates for sulfide flotation, benefiting from vertical integration across the acrylamide production chain. In 2025, SNF expanded Local-for-Local manufacturing capacity in China and India to address the projected 5 to 6% CAGR in Asia-Pacific mining activity through 2030. In 2026, SNF introduced bio-based flocculants manufactured via enzymatic processes, reducing carbon footprint by more than 30% compared to conventional synthesis. This combination of scale, integration, and sustainability innovation reinforces SNF’s competitiveness in high-volume flotation reagent supply.

Australia: Rare Earth Processing, Autonomous Mining, and Ethical Reagent Innovation

Australia’s flotation reagents market is undergoing a structural upgrade driven by downstream rare earth processing and digitalized mining operations. In early 2025, the Lynas Rare Earths processing facility in Kalgoorlie reached steady-state operations, marking the country’s first major step into domestic rare earth refining. This milestone has directly increased demand for highly selective thionocarbamate and hydroxamate collectors tailored for monazite and xenotime ores, where impurity rejection and recovery efficiency are commercially critical. Unlike bulk sulfide flotation, these rare earth circuits require reagent systems engineered for narrow mineral windows, accelerating collaboration between miners and specialty chemical suppliers.

Parallel to processing upgrades, Australia is emerging as a global benchmark for autonomous and AI-assisted flotation control. By mid-2025, mining majors such as Rio Tinto and BHP reported that autonomous systems accounted for more than 50% of haulage and processing movements across Pilbara operations. These platforms increasingly integrate real-time reagent optimization tools from Nalco Water and Arsenale Bioyards, enabling dynamic dosing adjustments that reduce reagent overconsumption and stabilize metallurgical performance. In parallel, the Victorian government’s 2025 Critical Minerals Roadmap, focused on antimony and zircon, is encouraging the adoption of biodegradable frothers to support ethical sourcing certifications. The upcoming graphite demonstration plant by Renascor Resources further reinforces demand for fatty-acid based collectors capable of achieving battery-grade purity for EV supply chains.

Chile: Copper Megaprojects and High-Salinity Flotation Breakthroughs

Chile remains the epicenter of global copper flotation reagent demand, supported by an unprecedented project pipeline. The government’s 2025 Mining Investment Guide confirms 51 active projects with a cumulative investment of USD 83 billion through 2033. This expansion is occurring against a backdrop of declining ore grades and more complex sulfide mineralogy, driving a shift away from traditional xanthates toward next-generation collectors designed for selectivity and lower environmental impact. These xanthate-replacement chemistries are increasingly favored to manage arsenic-bearing and polymetallic ores without compromising concentrate quality.

Environmental regulation is acting as a catalyst rather than a constraint. The Environmental Evaluation 2.0 Project, implemented in 2025, reduced permitting timelines by up to 70% for projects that adopt green mining practices. One key outcome is the rapid uptake of saline-water tolerant frothers that enable flotation in seawater, preserving scarce freshwater resources in arid regions. At the Chuquicamata operation, bespoke reagent systems trialed in late 2025 delivered a reported 15% improvement in platinum recovery under high-salinity conditions, while simultaneously lowering energy intensity per ton of concentrate. These results are reshaping reagent selection criteria across Chilean base and precious metal operations.

China: Resource Security, Battery Mineral Focus, and Export-Oriented Innovation

China’s flotation reagents market in 2025 is being reshaped by strategic resource security priorities. New export restrictions on rare earths and permanent magnets introduced in April 2025 have intensified domestic pressure to maximize recovery from low-grade ores and tailings. As a result, Chinese reagent producers are accelerating R&D into high-selectivity depressants and dispersants that enable cleaner separation in complex mineral systems. This internal optimization push is structurally increasing demand for performance-driven reagent packages rather than volume-based commodity chemicals.

The rapid rise of Lithium Iron Phosphate batteries is further redefining reagent demand. By 2025, LFP technology accounted for roughly 60% of passenger EVs in China, redirecting flotation chemistry needs toward phosphate-specific regulators and modifiers used in large open-pit operations. At the policy level, the Ministry of Agriculture and Rural Affairs streamlined export-only registrations in 2025, allowing domestic chemical majors to manufacture and export advanced Pyrazole-class flotation reagents before completing domestic approvals. This regulatory flexibility is strengthening China’s position as a global supplier of next-generation flotation chemistries while simultaneously serving domestic strategic minerals.

United States: Rare Earth Resurgence and Green Reagent Mandates

The United States flotation reagents market is being revitalized by renewed investment in critical minerals. Following the discovery of significant rare earth deposits by Ramaco Resources, pilot-scale flotation circuits commenced operations in Wyoming during 2025. These projects are explicitly designed around green reagent systems that minimize environmental liabilities associated with heavy mineral separation, aligning with state-level permitting expectations.

Federal funding is reinforcing this trend. The U.S. Department of Energy allocated targeted funding in 2025 for cobalt and nickel recovery projects, including new processing infrastructure by Doe Run that utilizes chelating collectors to extract battery metals from historic mine waste. At the same time, escalating tariffs on petrochemical intermediates during Spring 2025 have prompted U.S. reagent producers to restructure supply chains. Procurement alliances and production shifts toward tariff-neutral regions such as Saudi Arabia are becoming common, particularly for basic collectors like xanthates, while domestic players concentrate on higher-margin specialty formulations.

India: Integrated Value Chains and Bio-Based Frother Transition

India’s flotation reagents landscape is evolving beyond conventional mining applications into integrated agri-mineral value chains. In December 2025, BASF through its Nunhems division acquired Noble Seeds Pvt. Ltd., signaling a broader strategy where chemical majors offer end-to-end solutions spanning seeds, processing aids, and downstream extraction. This approach is boosting demand for specialized anti-caking agents and flotation reagents used in industrial seed oil extraction and mineral beneficiation.

Sustainability-driven innovation is accelerating under the BioE3 Policy. Government-backed biomanufacturing hubs established in 2025 are supporting precision fermentation platforms that produce bio-inspired surfactants. These are increasingly positioned as alternatives to hydrocarbon-based frothers in coal and iron ore beneficiation plants, particularly where environmental compliance and worker safety are becoming decisive procurement criteria. This shift positions India as a future growth center for biologically derived flotation reagents in Asia.

Comparative Snapshot: Flotation Reagents Market by Country (2025–2026)

Flotation Reagents Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Strategic Shift

|

Implication for Reagents

|

|

Australia

|

Rare earth processing and autonomy

|

AI-controlled dosing and ethical sourcing

|

High-selectivity collectors and biodegradable frothers

|

|

Chile

|

Copper megaprojects

|

Seawater-compatible flotation

|

Xanthate replacements and saline-tolerant frothers

|

|

China

|

Resource security and EV minerals

|

Export-oriented advanced chemistries

|

Depressants and phosphate-specific regulators

|

|

United States

|

Critical mineral resurgence

|

Green flotation and tariff realignment

|

Specialty collectors and chelating agents

|

|

India

|

Integrated value chains

|

Precision fermentation surfactants

|

Bio-based frothers and niche collectors

|

Flotation Reagents Market Report Scope

Flotation Reagents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.8 Billion

|

|

Market Size (2034)

|

$19.9 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Reagent Type (Collectors, Frothers, Modifiers, Flocculants), By Ore Type (Sulfide Ores, Non-Sulfide Ores), By Application (Base Metal Mining, Precious Metal Mining, Industrial Minerals, Coal Beneficiation, Water and Wastewater Treatment), By Form (Liquid, Powder, Solid)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Syensqo, BASF SE, Clariant AG, Solenis, SNF Group, Nouryon Holding B.V., Orica Limited, Arkema S.A., Chevron Phillips Chemical Company, Kemira Oyj, Kao Corporation, Dow Inc., Huntsman Corporation, Evonik Industries AG, Indorama Ventures

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flotation Reagents Market Segmentation

By Reagent Type

- Collectors

- Frothers

- Modifiers

- Flocculants

By Ore Type

- Sulfide Ores

- Non-Sulfide Ores

By Application

- Base Metal Mining

- Precious Metal Mining

- Industrial Minerals

- Coal Beneficiation

- Water and Wastewater Treatment

By Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Flotation Reagents Industry

- Syensqo

- BASF SE

- Clariant AG

- Solenis

- SNF Group

- Nouryon Holding B.V.

- Orica Limited

- Arkema S.A.

- Chevron Phillips Chemical Company

- Kemira Oyj

- Kao Corporation

- Dow Inc.

- Huntsman Corporation

- Evonik Industries AG

- Indorama Ventures

*- List not Exhaustive