Xanthates Market Overview 2025–2034: $951.1 Million to $1,566.4 Million at 5.7% CAGR Anchored in Copper Flotation Demand, Green SIBX Formulations, and Low-Carbon Mining Chemicals

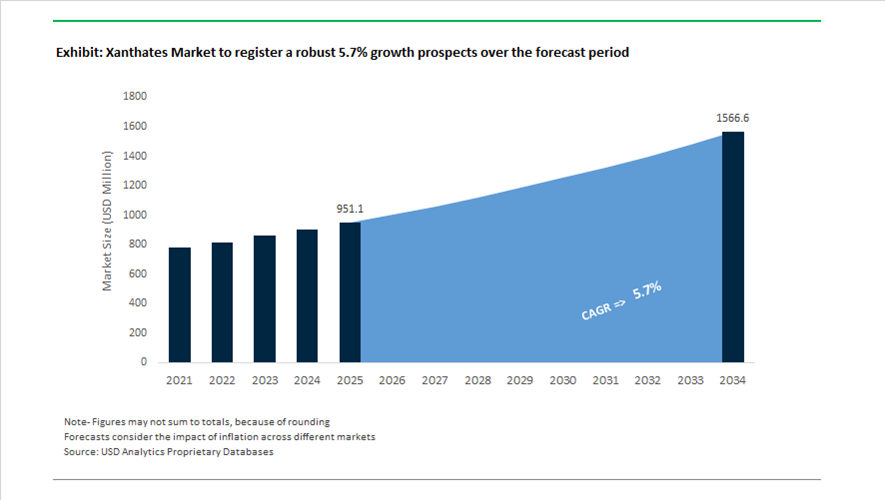

The Xanthates market is valued at $951.1 million in 2025 and is projected to reach $1,566.4 million by 2034, expanding at a CAGR of 5.7%. Xanthates, including Sodium Isobutyl Xanthate (SIBX), Sodium Isopropyl Xanthate (SIPX), and Potassium Amyl Xanthate (PAX), remain essential flotation collectors in copper, zinc, gold, and polymetallic ore beneficiation. Demand growth is directly linked to rising copper output for electrification, battery metals extraction, and deeper, more complex orebodies requiring selective flotation chemistry. Secondary applications include rubber vulcanization accelerators and agrochemical intermediates, reinforcing diversified end-use exposure.

Capacity expansion and portfolio integration defined the competitive landscape in 2024. In January 2024, CTC Mining expanded its xanthate production capacity in Chile to meet accelerating demand from high-throughput copper operations transitioning to lower-grade ores. In May 2024, Orica finalized its acquisition of Cyanco, strengthening its mining chemicals platform and enabling integrated solutions combining blasting agents, flotation collectors such as xanthates, and cyanide leaching systems. In November 2024, Tate & Lyle completed the acquisition of CP Kelco, expanding the availability of fermentation-derived biopolymers that are increasingly being evaluated as modifiers within flotation systems to reduce reagent intensity and environmental impact.

Environmental compliance and selective chemistry innovation accelerated in 2025. In February 2025, research demonstrated the successful photocatalytic degradation of SIPX using TiO2-clinoptilolite systems, providing mining operators with a scalable tailings treatment solution to meet stricter wastewater discharge regulations. In August 2025, manufacturers introduced starch-supported “eco-friendly” SIBX variants designed to maintain high collecting efficiency while reducing carbon disulfide emissions during production and application, aligning with new EU and Australian water quality directives. Orica launched advanced In-Place Recovery (IPR) techniques in 2025, promoting lower-volume, higher-selectivity collector formulations tailored for complex sulfide ores. In parallel, Wärtsilä’s CCS-ready emission control technologies, introduced between 2024 and 2025, are being adapted for heavy chemical facilities including xanthate manufacturing plants to address volatile organic emissions.

Decarbonization investments are reshaping feedstock economics and production footprints. In August 2025, Orica secured conditional funding of $432 million for its Hunter Valley Hydrogen Hub, supporting low-carbon chemical manufacturing pathways for mining reagents. In its 2025 sustainability update, Orica confirmed elimination of one million tonnes of CO2 equivalent at its Kooragang Island site, a key mining chemicals hub. In March 2025, Sudarshan Chemical completed its acquisition of the Heubach Group, expanding its specialty chemicals and mineral processing capabilities. In January 2026, Savita Oil Technologies reported full operational capacity of its expanded Indian facilities, including intermediates serving rubber and agrochemical sectors where xanthates function as vulcanization agents.

The xanthates market is advancing toward low-emission SIBX formulations, selective flotation chemistries for complex ores, integrated blasting-leaching-flotation platforms, photocatalytic tailings treatment, and hydrogen-supported low-carbon production routes. Copper electrification demand, mining sustainability mandates, and diversification into rubber and agrochemical intermediates will continue supporting mid-single-digit growth through 2034.

Trends and Opportunities in the Xanthates Market

Trend 1: Strategic Sourcing and Inventory Buffering Amid Carbon Disulfide Volatility

Xanthate production economics are highly sensitive to fluctuations in Carbon Disulfide (CS₂) and alcohol feedstocks, prompting a fundamental change in procurement and inventory strategies across the mining chemicals value chain.

In 2025, CS₂ spot pricing exhibited sharp swings, with U.S. indices declining by 10.7% in Q2 due to inventory overhangs, followed by renewed upward pressure in Q3, stabilizing near USD 780 per metric ton. This volatility has undermined traditional just-in-time procurement models. As a result, Tier-1 mining operators and reagent suppliers are shifting toward long-term supply contracts and buffer inventory strategies to stabilize the delivered cost of high-volume collectors such as Sodium Isopropyl Xanthate (SIPX) and Potassium Amyl Xanthate (PAX).

To structurally reduce logistics risk, Clariant Mining Solutions committed USD 100 million to a new xanthate production facility in Indonesia, fully operational by 2025. This localization strategy directly addresses the port congestion, inland rail bottlenecks, and emergency freight premiums that materially inflated reagent costs in early 2025, particularly for Southeast Asian copper and gold operations. Local manufacturing is now being viewed as a competitive differentiator rather than a cost optimization alone.

Trend 2: Compliance-Driven Transition to Closed-Loop Tailings and Process Water Management

Environmental scrutiny around xanthate degradation products, notably carbon disulfide and hydrogen sulfide, is accelerating the adoption of closed-loop water systems and real-time monitoring technologies in flotation circuits.

Under the 2025 Global Industry Standard on Tailings Management (GISTM), mining operators are required to reduce freshwater intake by up to 40% compared to 2020 baselines, particularly in high-risk or water-stressed regions. This has driven the integration of wet scrubbers, inline sensors, and automated neutralization systems to capture and degrade residual xanthates before process water is recycled.

The International Council on Mining and Metals reported in 2025 that 67% of member sites had achieved full conformance with the 77 essential GISTM safety requirements. A critical enabler of this compliance has been the deployment of Advanced Oxidation Processes (AOP), including peroxide and ozone-based systems, to chemically degrade residual xanthates in tailings storage facilities. These systems reduce the risk of toxic seepage, improve long-term tailings stability, and are increasingly mandated as part of operating license renewals.

Opportunity 1: Unlocking Value from Critical Mineral Tailings and Low-Grade Sulfide Ores

The global push for supply chain sovereignty in critical minerals is opening a substantial opportunity for xanthates in secondary resource recovery and the reprocessing of historically uneconomic ores.

According to research published in the Journal of Sustainable Metallurgy (June 2025), advanced flotation flowsheets using Potassium Amyl Xanthate (PAX) are now commercially viable for recovering cobalt, nickel, and rare earth elements from legacy tailings. With global mining waste generation exceeding 7 billion tons annually, xanthates play a central role in selectively collecting sulfide phases from complex, oxidized matrices where conventional collectors underperform.

Declining primary ore grades further reinforce this opportunity. Average global copper grades have fallen below 0.6%, forcing operators to rely on optimized xanthate blends to sustain recovery rates. Operational case studies from 2025 demonstrate that precision dosing of xanthate collectors can improve metal recovery by up to 5% in low-grade circuits, materially improving project economics. In parallel, improved control over sulfide recovery enhances the mechanical properties of tailings-based construction materials, supporting circular mine closure strategies.

Opportunity 2: High-Yield Spodumene Flotation for the EV Battery Supply Chain

The rapid expansion of lithium demand for electric vehicle batteries is creating a high-growth application for xanthates in hard-rock spodumene flotation, where reagent efficiency directly determines downstream lithium conversion costs.

In 2025, U.S. and Australian lithium producers highlighted flotation optimization as a critical bottleneck in scaling battery-grade lithium supply. Mixed collector systems incorporating xanthates have demonstrated the ability to produce spodumene concentrates exceeding 5.5% Li₂O, a threshold required for efficient lithium carbonate and hydroxide production.

New spodumene projects in Western Australia and North Carolina are increasingly designed around reagent-driven flotation rather than acid-intensive processing routes. Technical evaluations published in April 2025 indicate that replacing energy-heavy acid steps with optimized xanthate-based flotation can reduce overall energy consumption in lithium extraction by up to 30%. This aligns directly with the decarbonization targets of EV manufacturers and strengthens the strategic position of xanthates within the battery materials value chain.

Xanthates Market Share and Segmentation Insights

Product Type Market Share: Sodium Isobutyl Xanthate Leads with High Selectivity in Sulfide Flotation

Sodium isobutyl xanthate holds a 32.80% share in the xanthates market in 2025, driven by its superior balance of selectivity and collecting power in sulfide mineral flotation. It is widely used for copper, lead, zinc, and nickel ore processing, enabling efficient recovery and high-grade concentrate production. Sodium isopropyl xanthate, sodium ethyl xanthate, and potassium variants serve complementary roles depending on ore characteristics. A key market trend is collector optimization for complex ores, where blended xanthate systems and tailored reagent schemes improve recovery rates and separation efficiency as ore grades decline and mineralogy becomes more challenging.

End-Use Industry Market Share: Mining and Metallurgy Dominates with Flotation Reagent Demand

Mining and metallurgy account for 84.60% of the xanthates market in 2025, reflecting the critical role of flotation reagents in base metal and precious metal extraction processes. The scale of global mining operations and the reliance on flotation technology drive sustained consumption of xanthates. Rubber processing, pulp and paper, and water treatment represent minor application segments. A key growth driver is the increased processing of lower-grade ores, where higher reagent dosages and advanced flotation strategies are required, supporting consistent demand for xanthates as mining companies maximize resource recovery and extend mine life.

Xanthates Market Competitive Landscape

The Xanthates market in 2026 is defined by reagent precision, with emphasis on adsorption kinetics, liquid xanthate stabilization, and automated dosing systems, as mining operators optimize flotation efficiency, reduce hazardous dust exposure, and enhance recovery rates across copper, gold, and polymetallic sulfide operations.

Senmin Strengthens Vertical Integration with Smart Reagent Systems and African Supply Chain Control

Senmin, part of AECI Mining, leads the xanthates market through full vertical integration across the carbon disulfide (CS2) value chain, ensuring consistent quality and supply security. The company produces key collectors such as Sodium Isobutyl Xanthate (SIBX) and Potassium Amyl Xanthate (PAX) with tight process control. Its 2026 Smart Reagents initiative focuses on liquid xanthate storage and automated dosing systems, eliminating manual handling risks and reducing dust exposure. Expansion into Latin American copper markets includes bundled reagent supply with flotation optimization audits using simulation tools. Proximity of production hubs to mining sites minimizes hydrolysis degradation during transport. This logistics resilience ensures high active content delivery for flotation circuits.

Orica Integrates Digital Mining Platforms with High-Selectivity Xanthate Formulations

Orica is advancing xanthate technology through digital-chemical convergence, integrating reagent performance with mining analytics platforms. Its Specialty Mining Chemicals segment reported strong earnings growth in 2026 driven by new contracts and manufacturing efficiency. The company is piloting high-selectivity xanthate blends that improve copper and gold recovery while reducing pyrite co-flotation, lowering downstream processing costs. Decarbonization efforts at Kooragang Island reduced over one million tonnes of CO2-e, supporting low-carbon reagent production. Integration with WebGen™ and OREPro™ platforms enables real-time optimization of reagent dosing based on ore fragmentation data. This data-driven approach enhances flotation efficiency and reagent utilization.

Coogee Chemicals Leads Liquid Xanthate Innovation with Enhanced Stability and Safe Transport Systems

Coogee Chemicals dominates the liquid xanthate segment, offering stabilized PAX and SIPX formulations tailored for Asia-Pacific mining operations. Its products are engineered for high hydrolytic stability, allowing extended storage without loss of collector performance. The company has developed low-odor xanthates using proprietary additives to suppress sulfur emissions, improving environmental compliance. Investment in Smart ISO-Tank systems with real-time monitoring ensures safe transport to remote mining sites. Coogee’s focus on green chemistry and process safety aligns with strict environmental regulations in Tier-1 jurisdictions. This regulatory trust positions the company as a preferred supplier in sensitive mining environments.

Yantai Humon Expands Customized Xanthate Blends for Complex Polymetallic Ore Recovery

Yantai Humon is scaling customized flotation reagent solutions designed for polymetallic sulfide ores across Asia and Central Asia. Its tailored xanthate blends enable selective recovery of lead, zinc, and silver from complex ore bodies. High-purity Sodium Ethyl Xanthate (SEX) and Sodium Isopropyl Xanthate (SIPX) products exceed 90% active content, supporting efficient flotation kinetics. The company introduced refined-grade xanthates for specialty chemical and rubber applications, diversifying its portfolio. Expansion into CIS markets through regional partnerships secures long-term supply contracts for gold and copper operations. Automation of pelletization processes improves dissolution rates and consistency in industrial-scale flotation systems.

China Xanthate International Drives Bulk Supply Efficiency with Dust-Free Pellet Innovation

China Xanthate International (CXI) and Nanjing Henghong lead global bulk xanthate supply through economies of scale and cost competitiveness. The company introduced Green-Label xanthates with enhanced traceability and impurity control to meet Western regulatory standards. Its transition toward dust-free pellet production addresses safety concerns associated with traditional powder forms, reducing explosion and inhalation risks. Alignment with China’s 2025–2026 chemical industry growth policies supports ongoing investment in digital manufacturing and safety systems. CXI’s ability to produce large volumes of Potassium Amyl Xanthate (PAX) ensures supply stability for major mining regions. This scale-driven model positions CXI as a backbone supplier for global flotation reagent demand.

Australia Xanthates Market Shaped by Mining Digitization and Critical Minerals Security

Australia’s xanthates market is structurally anchored in large-scale mining operations and is increasingly influenced by digitization, environmental permitting, and critical minerals policy. Coogee Chemicals continues to dominate liquid xanthate supply across Asia-Pacific, with a differentiated focus on safe-handling packaging and automated on-site blending systems. These capabilities are particularly critical for remote operations in the Pilbara and Goldfields regions, where logistics reliability and reagent stability directly impact flotation efficiency and plant uptime. The preference for liquid xanthates over solid grades reflects Australia’s emphasis on operational safety, rapid dosing, and reduced handling risk in high-throughput mineral processing plants.

Technology integration is further reshaping reagent consumption patterns. In early 2025, Orica expanded AI-based reagent optimization across 60 mine sites, enabling real-time dose control and reducing chemical wastage by an estimated 12%. Policy alignment is reinforcing domestic production. The 2025 Critical Minerals Strategy incentivizes local flotation reagent manufacturing to secure nickel and cobalt supply chains for EV batteries. Concurrently, Western Australia’s stricter zero-discharge mandates for flotation tailings are accelerating the transition toward biodegradable xanthate derivatives and starch-supported variants by 2026. Looking ahead, Orica’s AUD 432 million investment in the Hunter Valley Hydrogen Hub is expected to decarbonize Carbon Disulfide production over time, structurally improving the sustainability profile of xanthate synthesis in Australia.

China Xanthates Market Driven by Green Compliance and Metallurgical Innovation

China remains the largest global producer and exporter of xanthates, with its market trajectory increasingly shaped by environmental compliance and metallurgical performance gains. In 2025, exporters such as China Xanthate International introduced green-label xanthates featuring improved traceability and reduced odor profiles to align with tightening EU import requirements. This shift reflects China’s broader strategy to protect export access while moving away from low-spec commodity grades. Cost competitiveness is also improving through upstream integration. BASF’s Zhanjiang Verbund site, scaling through 2025–2026, is expected to optimize the availability of alcohol and acrylic feedstocks, lowering production costs for technical-grade Sodium Ethyl Xanthate in southern China.

Provincial consolidation policies are accelerating modernization. Shandong’s 2025 mandate to relocate small chemical plants into advanced industrial parks has forced xanthate producers to install closed-loop Carbon Disulfide recovery systems, reducing emissions while improving yield economics. On the demand side, innovation is driving uptake. BGRIMM Technology Group introduced nanotech-enhanced flotation reagents in 2024–2025, with early trials in Hunan mines demonstrating a 9% increase in gold-copper recovery. The rapid expansion of lithium and rare earth processing in 2025 has further lifted domestic consumption of specialized frother-xanthate blends, reinforcing China’s position as both the largest producer and a fast-growing end user.

United States Xanthates Market Defined by Compliance, Supply Stability, and Niche Applications

The U.S. xanthates market is characterized by regulatory-driven reformulation and a focus on supply reliability for strategic mining and industrial uses. Following updated EPA effluent guidelines in 2025, SNF FloMin accelerated the rollout of PFAS-free collectors, targeting full compliance for copper mines in Arizona and Utah by 2026. This transition is shifting procurement preferences toward suppliers with documented environmental performance and consistent quality control, particularly for operations subject to federal land oversight.

Supply chain resilience remains a priority. In late 2024, Orica completed safety and production upgrades at its Winnemucca, Nevada facility, stabilizing the domestic supply of cyanide and xanthates for the North American precious metals sector. Beyond mining, adjacent industries are contributing incremental demand. In 2025, xanthate-based compounds saw increased use as vulcanization accelerators in rubber formulations, driven by domestic production of heavy-duty tires for fracking and mining equipment. Additionally, rising semiconductor investments through 2025–2026 have created a niche market for high-purity xanthates used in precision cleaning of metal-etched silicon wafers, broadening the application base beyond traditional flotation.

India Xanthates Market Supported by Policy Liberalization and Quality Formalization

India’s xanthates market is transitioning from fragmented procurement toward formalized, transparent trading structures. The Mines and Minerals Development and Regulation Amendment Act of August 2025 established a dedicated Mineral Exchange, enabling transparent trading of xanthates and other processing chemicals for the first time. This reform is improving price discovery and supply assurance for both public and private sector miners. Simultaneously, the removal of sale limits for captive mines in 2025 has encouraged steel and aluminum producers to invest in in-house reagent plant engineering, prioritizing supply security over spot-market dependence.

Regulatory classification changes are also reshaping demand. The October 2025 reclassification of limestone as a major mineral has introduced mandatory environmental filings for chemical usage, favoring high-purity, well-documented xanthate formulations. On the innovation front, Indian producers are exploring hybrid solutions. In 2025, Meron Group announced facility upgrades to produce microbial gum and xanthate blends for construction and grouting applications, signaling early diversification beyond mining. Collectively, these developments position India’s xanthates market for higher compliance standards, improved traceability, and gradual expansion into adjacent industrial uses.

Xanthates Market Country Snapshot

Xanthates Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Key End Uses

|

Strategic Direction

|

|

Australia

|

Mining digitization and critical minerals policy

|

Nickel, cobalt, gold flotation

|

High-safety, low-waste formulations

|

|

China

|

Green compliance and metallurgical efficiency

|

Gold, copper, lithium, REE

|

Export-ready, innovation-led

|

|

United States

|

EPA compliance and supply stability

|

Copper mining, rubber, semiconductors

|

PFAS-free, high-purity niches

|

|

India

|

Policy liberalization and quality formalization

|

Iron ore, limestone, construction

|

Transparent trading and diversification

|

Xanthates Market Report Scope

Xanthates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$951.1 Million

|

|

Market Size (2034)

|

$1566.4 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Sodium Ethyl Xanthate, Sodium Isopropyl Xanthate, Sodium Isobutyl Xanthate, Potassium Amyl Xanthate, Potassium Ethyl Xanthate), By Form (Solid, Liquid), By Grade (Technical Grade, Commercial Grade), By Application (Flotation Process, Extraction Process, Vulcanization Accelerator, Agrochemical Intermediate), By End-Use Industry (Mining and Metallurgy, Rubber Processing, Pulp and Paper, Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Orica Limited, SNF Group, AECI Limited, Coogee Chemicals Pty Ltd, BASF SE, Sinopec Corporation, Yantai Humon Chemical Auxiliary Co. Ltd., Qingdao Sunrui Marine Environmental Engineering, Tieling Flotation Reagent Co. Ltd., Clariant AG, Vanderbilt Chemicals LLC, American Elements Corporation, Qixia Tongda Flotation Reagent Co. Ltd., Y and X Beijing Technology Co. Ltd., Meron Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Xanthates Market Segmentation

By Product Type

- Sodium Ethyl Xanthate

- Sodium Isopropyl Xanthate

- Sodium Isobutyl Xanthate

- Potassium Amyl Xanthate

- Potassium Ethyl Xanthate

By Form

By Grade

- Technical Grade

- Commercial Grade

By Application

- Flotation Process

- Extraction Process

- Vulcanization Accelerator

- Agrochemical Intermediate

By End-Use Industry

- Mining and Metallurgy

- Rubber Processing

- Pulp and Paper

- Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Xanthates Market

- Orica Limited

- SNF Group

- AECI Limited

- Coogee Chemicals Pty Ltd

- BASF SE

- Sinopec Corporation

- Yantai Humon Chemical Auxiliary Co. Ltd.

- Qingdao Sunrui Marine Environmental Engineering

- Tieling Flotation Reagent Co. Ltd.

- Clariant AG

- Vanderbilt Chemicals LLC

- American Elements Corporation

- Qixia Tongda Flotation Reagent Co. Ltd.

- Y and X Beijing Technology Co. Ltd.

- Meron Group

*- List not Exhaustive