Food & Beverage Wastewater Treatment Equipment Market Overview

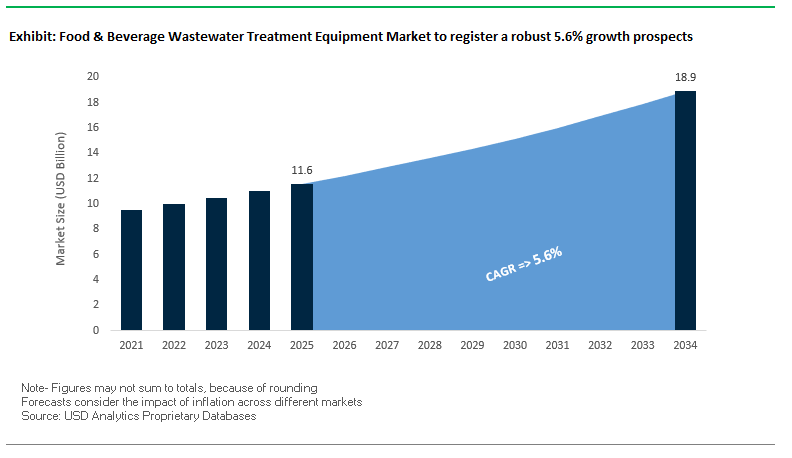

The global food & beverage wastewater treatment equipment market is projected to grow from $11.6 billion in 2025 to $18.9 billion by 2034, reflecting a steady CAGR of 5.6%. With food and beverage production ranking among the most water-intensive industrial sectors, the demand for advanced treatment solutions is being propelled by stricter environmental regulations, rising operational costs, and the need for sustainable practices.

Key Insights for Industry Stakeholders

- Dairy and beverage plants are the most water-intensive users in this market, requiring specialized equipment for cleaning, processing, and waste stream management.

- The Asia-Pacific region remains a growth hub due to rapid food processing expansion in China and India, coupled with stricter wastewater discharge rules.

- Globally, nearly 80% of wastewater flows untreated back into ecosystems, emphasizing the massive opportunity for advanced treatment adoption.

- Biological treatment solutions, such as anaerobic digestion, are becoming central in food & beverage facilities, turning organic waste into renewable biogas while reducing pollution.

Market Analysis: Recent News and Developments in Food & Beverage Wastewater Treatment

The food & beverage wastewater treatment equipment market continues to evolve with innovations in ZLD, biological treatment, and digital water management. Industry leaders are actively scaling projects, pursuing acquisitions, and piloting breakthrough technologies to address water reuse and energy recovery challenges in food and beverage manufacturing.

In August 2025, DuPont Water Solutions was honored as part of the BIG Sustainability Awards for its advancements in wastewater reuse and MLD systems, underscoring its role in circular water practices for food and beverage plants. Similarly, in July 2025, Veolia Water Technologies was selected to equip France’s largest wastewater reuse project in Argelès-sur-Mer, where treated effluent will support agriculture, a sign of growing cross-sector collaboration. Earlier, in May 2025, Veolia also acquired full ownership of its Water Technologies and Solutions subsidiary, a strategic move that streamlined its industrial offerings, including customized solutions for food & beverage clients.

Digitalization and renewable energy integration are also shaping this market. In March 2025, Ecolab advanced AI-driven water conservation tools designed to optimize consumption and minimize the environmental footprint of food plants. Xylem, in January 2025, partnered with the University Area Joint Authority (Pennsylvania) to introduce a biological hydrolysis system that accelerates renewable energy production from biosolids. Similarly, Kurita Water Industries made progress in December 2024 with microbial fuel cell technology, enabling electricity generation directly from wastewater. Scientific research also plays a role: an August 2024 publication highlighted the use of engineered nanoparticles for cost-effective treatment. Additionally, SUEZ reinforced its municipal and industrial presence in October 2024 by laying the foundation for Haliotis 2 wastewater treatment plant in Nice, France, underscoring its global leadership in ecological transition projects.

Key Trends and Emerging Opportunities in Food & Beverage Wastewater Treatment Equipment Industry

Stricter Regulations and the Push for Zero Liquid Discharge (ZLD)

Government policies are catalyzing investment in advanced treatment equipment. In India, the 2024 Liquid Waste Management Rules mandate that F&B establishments reuse an additional 20% of their wastewater by 2027-28, with penalties for non-compliance. This regulatory push encourages the adoption of ZLD systems and advanced treatment trains. Globally, proactive manufacturers such as Refres Now S.A. in Argentina have invested in dedicated wastewater treatment plants capable of handling 80 cubic meters per hour to comply with discharge limits and protect nearby water bodies. These examples demonstrate a clear trend of regulatory compliance translating into substantial equipment demand.

Integration of Resource Recovery and Circular Economy Principles

Sustainability is a major driver for investment in F&B wastewater equipment. Corporate initiatives, such as PepsiCo’s “pep+” agenda, aim to achieve a net water-positive impact by 2030. Pilot programs in India work with farmers to enhance water efficiency while leveraging advanced treatment equipment in plants to reduce freshwater consumption. Studies by the U.S. EPA show that membrane bioreactors (MBRs) can recover high-quality water suitable for cleaning processes, illustrating the direct link between resource recovery and advanced equipment adoption.

Technological Advancements in Smart and Automated Systems

Innovation in smart and automated treatment systems is reshaping operations. Evoqua Water Technologies’ upgraded Vantage PTI system is optimized for high-organic-load beverage effluents, demonstrating industry focus on specialized, efficient equipment. EPA data indicates that 60% of new U.S. beverage plants employ advanced filtering and real-time monitoring systems, reducing manual labor by up to 30% while boosting water reuse rates.

Food & Beverage Wastewater Treatment Equipment Market Share Insights

Market Share by Technology: Secondary Treatment Leads

Secondary (Biological) Treatment Equipment (45%) dominates due to the high organic strength of F&B wastewater. Technologies include anaerobic digesters (UASB, IC), aerobic activated sludge processes, MBBR, MBR, and sequencing batch reactors (SBR), which efficiently degrade BOD/COD and can generate biogas. Primary/Pre-treatment Equipment (30%) removes suspended solids, FOG, and equalizes flow using screens, grit chambers, DAF, and sedimentation tanks critical for protecting downstream systems. Tertiary/Polishing Treatment (25%) addresses nutrient removal, disinfection, and advanced polishing for reuse through membrane filtration (UF, NF, RO), UV disinfection, and sand/media filters. The high share of secondary treatment underscores the organic-intensive nature of F&B effluent, while tertiary systems are increasingly deployed to enable water reuse and regulatory compliance.

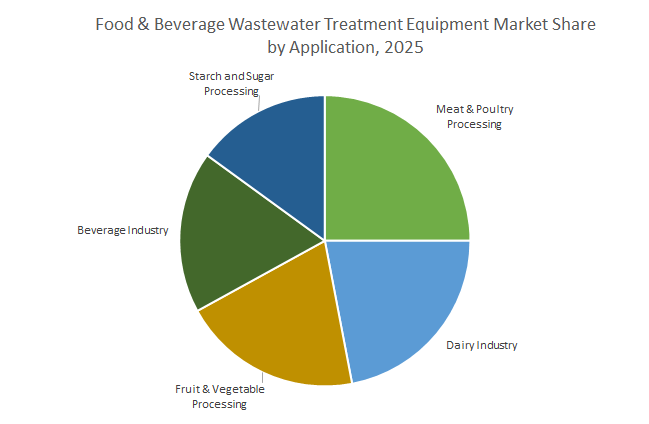

Market Share by Application: High-Strength Wastewater Dominates

Meat & Poultry Processing (25%) and Dairy (22%) lead due to extremely high organic and FOG content, requiring robust treatment solutions often integrated with anaerobic digestion for energy recovery. Fruit & Vegetable Processing (20%) generates high solids loads and seasonal wastewater, emphasizing flexible pre-treatment solutions to recover valuable biomass. Beverage Industry produces high sugar and BOD-laden effluents, necessitating advanced secondary and tertiary treatment. Starch and Sugar Processing produces some of the strongest wastewater streams, driving the adoption of energy-efficient anaerobic digestion as a primary step. The application-based distribution highlights that the most water- and organics-intensive segments are key growth drivers.

Market Share by System Integration: Customization is Critical

Custom-Engineered Systems (65%) dominate for large-scale processing facilities due to complex waste streams, site-specific constraints, and high flow volumes. They allow optimal integration of pre-treatment, biological, and tertiary systems, often including energy and resource recovery. Packaged/Containerized Systems (35%) are gaining traction for SMEs, greenfield expansions, and modular add-ons for specific treatment steps. These systems provide rapid deployment, cost efficiency, and pre-tested reliability for less complex waste streams, making them ideal for craft breweries, small dairies, and standalone food processing units.

United States: PFAS Regulations and Advanced Membrane Technologies Drive Market Adoption

The U.S. food and beverage wastewater treatment equipment market is experiencing growth due to stringent environmental policies and technological innovation. The U.S. Environmental Protection Agency (EPA) finalized new PFAS Maximum Contaminant Levels, triggering immediate investment in retrofitting existing water treatment facilities with membrane technologies. The 2024 Water Reuse Action Plan (WRAP) highlighted activated carbon adsorption pilots in food and beverage plants, achieving high organic contaminant removal rates. Technological advancements include Evoqua Water Technologies’ upgraded Vantage PTI system, optimizing high-organic-load effluent treatment for beverage production. Additionally, sensor integration and automated controls enhance real-time monitoring and operational efficiency. Corporate initiatives, such as water recovery projects by major beverage manufacturers aiming for net-zero emissions, and Koch Separation Solutions’ Eco-Tec Ion Exchange system, support nutrient recovery and water reuse. Key applications include bioenergy generation and resource recovery in food and beverage production facilities, reflecting strong market adoption.

China: Strategic Investments and Localized Membrane Production Strengthen Market Growth

China’s food and beverage wastewater treatment equipment market is driven by regulatory compliance, government investment, and technological innovation. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge regulations, compelling food and beverage companies to adopt advanced treatment solutions. Government initiatives include a $50 billion investment by 2025 in wastewater infrastructure, targeting food processing, brewing, and other heavy-polluting sectors. China has achieved approximately 85% self-sufficiency in membrane module production, leading to competitive pricing and increasing adoption in replacement projects. Technological advancements include SUEZ’s "embedded WWTP" for Hengli Group, leveraging 12 patented technologies to reduce energy and material use, cut emissions, and prevent secondary pollution. These developments enhance operational efficiency and sustainability across the Chinese food and beverage sector.

India: Infrastructure Development and Advanced Membrane Systems Accelerate Market Penetration

India’s market for food and beverage wastewater treatment equipment is expanding through government initiatives, technological innovations, and corporate partnerships. The "Jal Jeevan Mission" promotes water and wastewater treatment adoption in urban and rural areas, while the "Namami Gange Mission" and "Smart Cities Mission" accelerate plant deployment and modernization. In January 2024, Emerald Technology Ventures invested in INDRA, boosting water treatment technology adoption in India and Southeast Asia, with clients including Unilever. Technological advancements include IIT Madras’ pilot-scale systems for textile wastewater, achieving 96% color removal and 60% COD reduction, which are increasingly applied in food processing. Corporations like Veolia supply ZeeWeed membranes and T-MBR systems for breweries, supporting effluent recycling and meeting environmental compliance. Key applications include water reuse, resource recovery, and sustainable effluent management across the food and beverage industry.

Germany: Regulatory Compliance and Digitalized Wastewater Solutions Propel Market Growth

Germany’s food and beverage wastewater treatment equipment market is driven by regulatory mandates, technological innovation, and digitalization. The revised EU Urban Wastewater Treatment Directive (January 2025) requires a "4th purification stage" to eliminate micropollutants, fostering the adoption of advanced oxidation and decentralized treatment systems. Technological innovations include EnviroChemie’s two-stage flotation process for poultry wastewater, reducing chemical usage by up to 60% and enabling oil and fat recovery for biofuel production. Digitalization efforts, such as the WaterExpert app, provide real-time monitoring and operational efficiency for treatment plants. Key applications span the chemical and food and beverage sectors, where complex wastewater streams necessitate advanced treatment equipment for regulatory compliance and sustainability.

Brazil: Legal Reforms and Large-Scale Infrastructure Investments Support Market Expansion

Brazil’s food and beverage wastewater treatment equipment market is gaining traction through legal reforms, private sector participation, and large infrastructure projects. The new water framework sets ambitious targets for 2033: 99% water coverage and 90% treated sewage coverage, providing regulatory certainty and encouraging investment. Projects totaling approximately BRL 105 billion across 43 privatization initiatives will serve industrial customers, including food and beverage manufacturers. Key applications focus on treating wastewater from major production hubs in São Paulo and Santa Catarina, ensuring environmental compliance, efficient resource management, and sustainable industrial water reuse.

Japan: Corporate Sustainability and Membrane Innovation Drive Advanced Wastewater Management

Japan’s food and beverage wastewater treatment equipment market is influenced by corporate sustainability initiatives, regulatory frameworks, and advanced R&D. Suntory Beverage & Food has reduced water intensity by 22% compared to 2015, targeting a 20% reduction by 2050. While no new wastewater discharge regulations have been introduced, changes to the Food Sanitation Law (June 2025) indirectly impact wastewater from packaging operations. Academic and corporate research, led by Toray Industries Inc., focuses on advanced membrane technologies essential for high-efficiency effluent treatment. Applications include nutrient recovery, water reuse for irrigation, and wastewater management in seafood and beverage processing, reflecting Japan’s leadership in sustainable wastewater solutions.

Competitive Landscape: Leading Companies in Food & Beverage Wastewater Treatment

The competitive landscape of the food & beverage wastewater treatment equipment market is defined by multinational water leaders, advanced membrane developers, and innovative technology providers. Companies differentiate through sustainability-driven strategies, resource recovery systems, and the integration of digital water intelligence.

DuPont Water Solutions – Membrane Innovations Driving Food & Beverage Reuse

DuPont is a global leader in advanced membrane technologies with its FilmTec™ line, widely adopted in food & beverage wastewater reuse. In 2025, it received an R&D 100 Award for the FilmTec™ Fortilife™ XC160 Membrane, which enables efficient concentration of high-strength wastewater streams. DuPont’s broad portfolio including RO, NF, UF membranes, and ion exchange resins offers integrated solutions for MLD and ZLD. Its sustainability strategy focuses on enabling water circularity and cost efficiency, with its technologies purifying 50 million gallons of water per minute worldwide.

Veolia Water Technologies – Large-Scale Circular Economy Solutions

Veolia specializes in integrated water resource management, offering solutions that span from dissolved air flotation (DAF) to anaerobic digestion and membrane bioreactors (MBRs). In May 2025, the company consolidated ownership of its water technology arm, strengthening its market agility. Veolia’s strength lies in delivering circular economy models, converting wastewater into resources like biogas and biosolids, directly aligning with the sustainability goals of food & beverage companies.

Xylem Inc. – End-to-End Digital and Biological Solutions

Xylem delivers comprehensive solutions, including pumps, biological treatment, advanced oxidation, and analytics, for high-strength wastewater. The company’s 2023 acquisition of Evoqua created a powerful platform for industrial wastewater, including food and beverage applications. In January 2025, Xylem advanced renewable energy recovery projects in partnership with UAJA. By combining digital water solutions, IoT monitoring, and predictive maintenance, Xylem helps processors cut costs and maximize compliance.

SUEZ – Customized High-Performance Systems for Food Wastewater

SUEZ has a strong global presence in biological and membrane systems tailored for industrial applications. Its solutions include MBR systems and advanced nutrient removal technologies, both critical for food plants with high organic loads. The company is also integrating digital performance platforms to reduce fouling and chemical consumption. In October 2024, SUEZ reinforced its leadership by launching the Haliotis 2 project in France, reflecting its role in driving the ecological transition across both municipal and industrial markets.

Evoqua Water Technologies LLC – Strong North American Footprint in Industrial Wastewater

Now part of Xylem, Evoqua has long been recognized as a trusted provider of industrial wastewater solutions across 38,000 customers and 200,000 installations. With a focus on filtration, disinfection, and reuse systems, Evoqua brings mission-critical solutions to the food & beverage sector. Its Sustainability and Innovation Hub in Pittsburgh is pushing advancements in areas such as PFAS removal and climate resilience, positioning it at the forefront of emerging wastewater treatment challenges.

Kurita Water Industries Ltd. – Chemical-Equipment Hybrid Expertise

Kurita combines equipment solutions with chemical treatment expertise, offering tailored technologies for complex organic loads in food & beverage wastewater. Its expansion into India through Kurita AquaChemie India (June 2024) underlines its commitment to textile, food, and industrial wastewater growth markets. Kurita’s innovative microbial fuel cell technology highlights its focus on energy-positive treatment. Its sustainability agenda centers on reducing wastewater discharges to minimal levels while enabling efficient reuse for food processors.

Food & Beverage Wastewater Treatment Equipment Market Report Scope

Food & Beverage Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2034)

|

$18.9 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Technology (Primary / Pre-treatment, Secondary (Biological) Treatment Equipment, Tertiary/Polishing Treatment Equipment), By Application (Dairy Industry, Meat & Poultry Processing, Fruit & Vegetable Processing, Beverage Industry, Starch and Sugar Processing), By System Integration (Custom-Engineered Systems, Packaged/Containerized Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Pentair plc, Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Nalco Water (An Ecolab Company), Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food & Beverage Wastewater Treatment Equipment Market Segmentation

By Technology

- Primary / Pre-treatment

- Secondary (Biological) Treatment Equipment

- Tertiary/Polishing Treatment Equipment

By Application

- Dairy Industry

- Meat & Poultry Processing

- Fruit & Vegetable Processing

- Beverage Industry

- Starch and Sugar Processing

By System Integration

- Custom-Engineered Systems

- Packaged/Containerized Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Food & Beverage Wastewater Treatment Equipment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Pentair plc

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Nalco Water (An Ecolab Company)

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Food & Beverage Wastewater Treatment Equipment Market with analysis reviews of demand drivers, regulatory catalysts, and plant-level economics, and highlights technology breakthroughs in biological digestion, membrane polishing, ZLD/MLD trains, and digital controls shaping CAPEX/OPEX decisions. Compiled by USDAnalytics, the study sizes growth across dairies, beverages, meat processing, and starch/sugar streams, benchmarks recovery rates and energy intensity, and maps replacement and retrofit cycles alongside packaged vs. engineered deployments. It assesses vendor positioning, procurement patterns, and circularity gains from biogas and water reuse. This report is an essential resource for utilities managers, engineering leaders, OEMs/EPCs, and investors seeking compliant, cost-efficient, and resilient treatment strategies through 2034. Scope Includes-

- Segmentation

- By Technology: Primary / Pre-treatment; Secondary (Biological) Treatment Equipment; Tertiary/Polishing Treatment Equipment

- By Application: Dairy Industry; Meat & Poultry Processing; Fruit & Vegetable Processing; Beverage Industry; Starch and Sugar Processing

- By System Integration: Custom-Engineered Systems; Packaged/Containerized Systems

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; Forecasts 2025–2034.

- Companies (15+ profiles/analysis): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Pentair plc; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Nalco Water (An Ecolab Company); Thermax Limited.

Methodology

USDAnalytics applies a triangulated approach combining bottom-up audits of installed equipment and shipments with top-down spend curves by sub-sector and region. Primary interviews with plant utilities heads, OEMs/EPCs, and regulators validate removal efficiencies (BOD/COD/FOG, nutrients), recovery rates, kWh·m⁻³, chemical dose, membrane cleaning intervals, and sludge/biogas yields. Secondary research spans permits, tenders, ESG disclosures, and peer-reviewed trials on MBR/UASB/IC, DAF, UF/NF/RO, AOP/UV, and ZLD/MLD. We convert plant data into regional LCC models, run sensitivity on tariffs, PFAS and discharge limits, energy prices, and water-scarcity indices, and produce defensible 2025–2034 forecasts and vendor share estimates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Food & Beverage Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Water-Intensive Sectors, Regional Dominance, and Resource Recovery

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $11.6 Billion

1.3.2. Projected Market Valuation (2034): $18.9 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 5.6%

2. Market Outlook (2025–2034)

2.1. Introduction: Market Drivers and Growth Forecast

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends and Emerging Opportunities

2.3.1. Stricter Regulations and the Push for Zero Liquid Discharge (ZLD)

2.3.2. Integration of Resource Recovery and Circular Economy Principles

2.3.3. Technological Advancements in Smart and Automated Systems

3. Innovations and Strategic Developments

3.1. Market Analysis: Recent News and Developments

3.1.1. DuPont Water Solutions Recognized with Sustainability Award (August 2025)

3.1.2. Veolia and SUEZ Secure Major Water Reuse and Ecological Transition Projects (July 2025)

3.1.3. Corporate Consolidation and Partnerships Reshaping the Market

3.1.4. Digitalization and Renewable Energy Integration in Wastewater Treatment

3.1.5. Breakthroughs in Scientific Research and Nanoparticle Technology

4. Competitive Landscape: Leading Companies

4.1. Competitive Overview: Global Leaders and Innovators

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Membrane Innovations Driving F&B Reuse

4.2.2. Veolia Water Technologies: Large-Scale Circular Economy Solutions

4.2.3. Xylem Inc.: End-to-End Digital and Biological Solutions

4.2.4. SUEZ: Customized High-Performance Systems for Food Wastewater

4.2.5. Evoqua Water Technologies LLC: Strong North American Footprint

4.2.6. Kurita Water Industries Ltd.: Hybrid Chemical-Equipment Expertise

5. Market Segmentation Insights

5.1. By Technology

5.1.1. Secondary (Biological) Treatment Equipment (45% Market Share)

5.1.2. Primary / Pre-treatment Equipment (30% Market Share)

5.1.3. Tertiary/Polishing Treatment Equipment (25% Market Share)

5.2. By Application

5.2.1. Meat & Poultry Processing (25% Market Share)

5.2.2. Dairy Industry (22% Market Share)

5.2.3. Fruit & Vegetable Processing (20% Market Share)

5.2.4. Beverage Industry

5.2.5. Starch and Sugar Processing

5.3. By System Integration

5.3.1. Custom-Engineered Systems (65% Market Share)

5.3.2. Packaged/Containerized Systems (35% Market Share)

6. Country Analysis and Outlook

6.1. United States: PFAS Regulations and Advanced Membrane Technologies

6.2. China: Strategic Investments and Localized Membrane Production

6.3. India: Infrastructure Development and Advanced Membrane Systems

6.4. Germany: Regulatory Compliance and Digitalized Solutions

6.5. Brazil: Legal Reforms and Large-Scale Infrastructure Investments

6.6. Japan: Corporate Sustainability and Membrane Innovation

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By Technology

7.1.2. By Application

7.1.3. By System Integration

7.2. Europe Market Outlook

7.2.1. By Technology

7.2.2. By Application

7.2.3. By System Integration

7.3. Asia Pacific Market Outlook

7.3.1. By Technology

7.3.2. By Application

7.3.3. By System Integration

7.4. South America Market Outlook

7.4.1. By Technology

7.4.2. By Application

7.4.3. By System Integration

7.5. Middle East & Africa Market Outlook

7.5.1. By Technology

7.5.2. By Application

7.5.3. By System Integration

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. DuPont de Nemours, Inc.

8.6. Pentair plc

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures