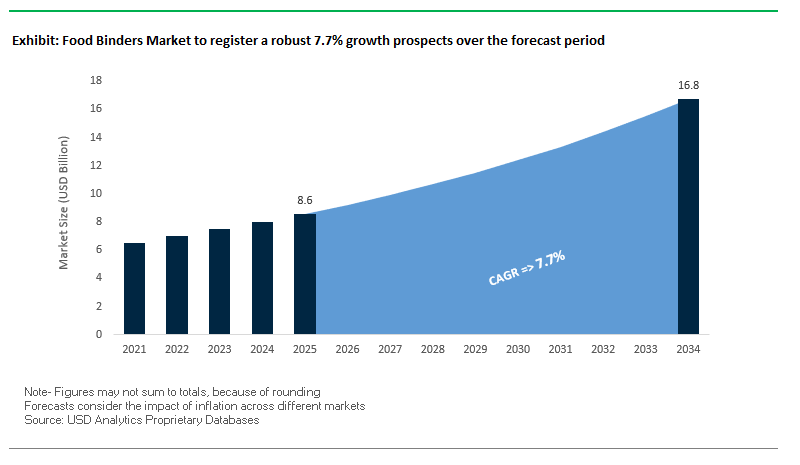

Market Overview: Food Binders Market to Reach $16.8 Billion by 2034 at 7.7% CAGR

The global food binders market is projected to grow from $8.6 billion in 2025 to $16.8 billion by 2034, expanding at a robust CAGR of 7.7%. This rapid growth is driven by rising consumer demand for clean-label, plant-based, and sustainable ingredients, along with increasing applications of binders in reformulated, low-calorie, and fortified food products. For industry professionals and buyers, the central questions are: How are natural binders replacing synthetic options? Which plant-based alternatives are gaining traction? And how will sustainability in sourcing reshape procurement strategies?

Key Insights for stakeholders:

- Natural & Clean-Label Reformulation: Growing replacement of artificial binders with natural starches, gums, and proteins to meet clean-label demand.

- Plant-Based Binders on the Rise: Strong adoption of binders from pulses, citrus fibers, and plant proteins to replicate meat and dairy textures.

- Solving Formulation Challenges: Key role in sugar and fat reduction while maintaining texture, stability, and sensory quality in foods and beverages.

- Sustainable Sourcing: Expansion of regenerative agriculture programs and responsible sourcing initiatives to reduce environmental impact.

Market Analysis: Recent Developments in the Global Food Binders Industry

The food binders market is undergoing significant transformation, marked by strategic partnerships, acquisitions, and innovation-driven product launches.

In August 2025, Ingredion announced a quarterly dividend increase to $0.82 per share, underscoring its financial strength and shareholder confidence. A month earlier, in July 2025, Ingredion and AGRANA’s joint venture received regulatory clearance, a move expected to strengthen their collaborative position in starches and sweeteners. In the same month, Ingredion expanded its partnership with Univar Solutions to the Benelux region, targeting healthier and sustainable product demand.

Meanwhile, Tate & Lyle has been actively innovating. In May 2025, the company showcased new prototypes and opened its Mouthfeel Lab at IFT FIRST 2025, expanding its capabilities post-CP Kelco acquisition. This followed its November 2024 launch of EUOLIGO® FOS and TASTEVA® M sweetener solutions in the Middle East, designed to enhance sugar reduction while preserving texture.

ADM continues to expand its starch and sweeteners portfolio. In March 2025, ADM acquired a 50% equity stake in Aston Foods’ corn wet milling business in Russia, enhancing its corn processing capacity and global reach.

Ingredion has also been driving clean-label innovation. In August 2024, it launched FIBERTEX® CF 500 and CF 100 citrus fiber ingredients, expanding its natural binder offerings in texture and viscosity. At the same time, Ingredion terminated its RealSweet JV with Amyris in May 2025, securing exclusive rights to fermented Reb M technology, a critical sugar-reduction ingredient.

Trends and Opportunities Reshaping the Food Binders Market

Clean-Label Reformulation Replacing Synthetic and Allergenic Binders

The food binders market is undergoing a fundamental shift toward clean-label reformulation, as consumer distrust of synthetic and allergenic additives drives manufacturers to embrace natural alternatives. An International Food Information Council (IFIC) survey revealed that 63% of consumers avoid products with unfamiliar technical terms on the ingredient list, underscoring the importance of transparency. This has compelled leading food brands to reformulate their portfolios with recognizable, plant-derived binders such as pectin, starches, and natural gums.

Corporate action is aligning with this trend. A major yogurt producer replaced artificial thickeners with fruit-derived pectin, achieving a clean label without compromising taste or texture. Similarly, a bakery brand successfully switched to natural fruit- and vegetable-based colorants, demonstrating that natural binders can meet both performance and consumer expectations. The definition of clean label has expanded beyond ingredient lists to encompass ethical sourcing, environmental responsibility, and supply chain transparency. As a result, manufacturers must now consider not only the composition of binders but also their sustainability profile, creating a holistic evolution of the clean-label movement.

Technological Innovation in Plant and Fruit-Based Binders for Meat Analogues

The rise of plant-based meat and dairy alternatives has catalyzed intense innovation in plant- and fruit-derived binders. Traditional binders like methylcellulose, though effective, are not considered clean-label, creating a gap for next-generation natural binders that can deliver the structure, texture, and juiciness of animal-based products. A recent patent filing describes a binder system combining cellulose microfibrils with thermally gelling proteins, designed to improve mouthfeel and replicate meat-like chewiness.

Scientific research highlights that combining hydrocolloids like kappa carrageenan and konjac mannan can significantly enhance water-holding capacity and cooking yields, overcoming limitations of conventional starches. Additionally, dietary fibers sourced from legumes and fruits are being studied for their natural viscosity and gelation abilities, enabling the creation of binders that deliver authentic textures in extruded plant-based products. This wave of innovation is critical for scaling the plant-based protein sector, as consumers increasingly demand both clean-label ingredients and sensory parity with animal proteins.

Upcycled Ingredient Sourcing for Sustainable Binding Solutions

A major growth avenue lies in upcycled ingredients as sustainable, high-performance food binders. The food industry generates significant by-product streams such as fruit pomace, vegetable pulp, and okara (soy pulp) that are rich in dietary fiber and proteins. These materials can be repurposed into binders that not only improve product structure but also add nutritional value. For example, a company producing okara-based flour has demonstrated its potential as a gluten-free, low-carb binding agent, expanding its application in bakery and functional foods.

Consumer behavior research indicates a clear willingness to pay for sustainability. A study revealed that when consumers are informed about the nutritional and environmental benefits of products containing upcycled binders, their willingness to pay a premium increases significantly. This creates a strong marketing advantage for brands leveraging upcycled binding solutions. Beyond sustainability, these ingredients often exhibit unique functional properties, making them attractive not just for waste reduction but also for performance enhancement in new product development.

Precision Fermentation for Next-Generation Functional Proteins

Another transformative opportunity lies in precision fermentation, which enables the production of tailor-made functional proteins with superior binding capabilities. Scientists are already replicating casein the key dairy protein responsible for emulsification, foaming, and thickening without cows, opening pathways for authentic plant-based dairy and cheese products. Engineered proteins such as alpha-S1 casein analogues offer functionalities like cold-set gelation and superior emulsification, creating possibilities for entirely new product categories in dairy alternatives and protein-based foods.

Beyond performance, precision fermentation addresses allergen and dietary concerns by creating allergen-free and potentially non-GMO proteins. This makes it a compelling solution for manufacturers catering to sensitive consumer segments. Companies can design binders with specific properties such as enhanced gel strength, heat stability, or dispersibility that go beyond what is available in nature. With rising investment in alternative proteins and fermentation platforms, this field represents a game-changing growth opportunity, bridging the gap between sustainability, performance, and consumer acceptance in the global food binders market.

Competitive Landscape: Global Leaders Driving Food Binder Innovation

The food binders industry is highly consolidated, with multinational companies competing on R&D strength, sustainability strategies, and portfolio breadth.

Tate & Lyle PLC Expanding Capabilities with CP Kelco Acquisition

Tate & Lyle is a global provider of starches, sweeteners, and texturants, with a strong position in food binders from corn, tapioca, and plant sources. In 2025, it completed the acquisition of CP Kelco, significantly strengthening its expertise in pectin and gums. Its “Transforming Lives Through the Science of Food” strategy emphasizes healthier eating while preserving taste and texture. With over 5,000 employees across 75 locations, it leverages its global R&D and production footprint to deliver scalable binder solutions.

Ingredion Incorporated Strengthening Partnerships and Clean-Label Innovations

Ingredion is a leading global provider of starches, hydrocolloids, and plant-based proteins. The company reported a 13% increase in Q2 2025 operating income, reflecting strong market performance. Its JV with AGRANA and expanded partnership with Univar Solutions highlight its collaborative growth model. Ingredion also launched new citrus fiber binders (FIBERTEX® CF 500 and CF 100) in 2024 to serve the clean-label trend. Its strategy centers on sustainability and innovation, aligning with rising consumer demand for natural solutions.

Cargill, Incorporated Leveraging Global Scale and Integrated Supply Chain

Cargill offers an extensive portfolio of food binders, including modified starches, lecithins, and carrageenan. Its strategy emphasizes high-quality, functional ingredients and integrated solutions across the supply chain. With 13 manufacturing sites and a corn wet milling facility in India, Cargill demonstrates its regional expansion strategy. Its ability to manage sourcing, R&D, and application testing allows it to provide end-to-end customized binder solutions for global food manufacturers.

Archer Daniels Midland (ADM) Expanding Starches and Sweeteners through Acquisitions

ADM is a global leader in starches, gums, and hydrocolloids, key binders for bakery, dairy, and meat alternatives. In March 2025, it acquired a 50% stake in Aston Foods’ sweeteners and starches business, expanding its global footprint. ADM leverages its expertise in fermentation and plant proteins, with innovation centers on six continents accelerating product development. With 500 procurement sites and 270 ingredient facilities, ADM’s integrated value chain strengthens its competitive position in the food binders market.

DuPont de Nemours, Inc. Innovating with Hydrocolloids and Plant-Based Solutions

DuPont (now part of IFF Nutrition & Biosciences) offers a range of hydrocolloids, enzymes, and plant-based binders. Its scientific expertise in material science and sustainability underpins its strategy for food and beverage innovation. DuPont has launched specialty hydrocolloids and pectin designed for superior gelling and thickening in dairy, fruit, and confectionery applications. Its binder portfolio also supports meat and dairy alternatives, enabling manufacturers to replicate authentic textures in plant-based foods.

Food Binders Market Share Insights

Hydrocolloids Dominate Market Share by Type in Food Binders

In 2025, hydrocolloids account for 45% of the food binders market, positioning themselves as the functional backbone of processed food stability and performance. Their dominance stems from unparalleled versatility whether delivering viscosity in sauces, gelation in confectionery, or water-binding in plant-based meat analogs, they ensure consistency across diverse food systems. Their ability to perform at extremely low usage levels provides cost efficiency, while their compatibility with clean-label positioning (e.g., agar, guar gum, xanthan) ensures relevance in both traditional and emerging applications. Proteins, with a 30% share, are the fastest-growing cohort, driven by consumer demand for natural and recognizable ingredients and their irreplaceable role in plant-based meats that require fibrous textures mimicking animal protein. Fats & oils remain indispensable for delivering richness, tenderness, and sensory appeal in bakery and meat applications, while starches and fibers, though smaller in share, provide functional support, nutritional enhancement, and cost optimization. Overall, type segmentation highlights how hydrocolloids secure dominance through multifunctionality, proteins fuel clean-label and plant-based innovation, and fats/oils anchor indulgence-driven formulations.

Meat Products and Meat Analogs Lead Market Share by Application in Food Binders

By application, meat products and meat analogs represent 30% of the food binders market in 2025, making them the epicenter of innovation and R&D investment. In traditional meat processing, proteins and starches improve water retention, yield, and texture in sausages and patties, while in plant-based analogs, complex blends of hydrocolloids and pea/soy proteins replicate the fibrous bite of real meat driving exponential demand in this fast-growing category. Bakery and confectionery at 25% provide a stable, high-volume base where gluten, fats, and hydrocolloids are fundamental to structure, moisture retention, and chewiness, ensuring reliable demand from both artisanal and industrial producers. Sauces, dressings, and soups continue to anchor hydrocolloid usage by ensuring suspension and shelf stability, while dairy and frozen desserts rely on binders to prevent whey separation, control ice crystallization, and deliver smooth textures. Convenience foods and beverages remain smaller but strategically important niches, where binders safeguard structural integrity under freezing, reheating, and suspension challenges. Collectively, the application landscape shows that binders sustain dominance through meat innovation, bakery tradition, and stability in liquid and frozen systems.

United States: Clean-Label and Plant-Based Food Binders Driving Market Innovation

The U.S. food binders market is undergoing a transformation driven by consumer demand for clean-label and natural ingredients. Manufacturers are increasingly incorporating plant-based binders such as flaxseeds, chia seeds, and starches to meet the rising consumer preference for transparent, healthier food products. This shift is particularly evident in the development of organic and plant-based products, where innovative binders play a crucial role in creating desirable texture, stability, and mouthfeel for meat analogs, vegan baked goods, and other emerging food segments.

Technological advancements are also shaping the market. Collaborations between leading food companies are leveraging binders in plant-based yogurt bases and other novel formulations, ensuring consistent texture, consistency, and product performance. The focus on functional, natural, and sustainable ingredients is driving innovation and opening new applications in both traditional and emerging food categories.

Germany: Regulatory Compliance and Circular Economy Focus Strengthening Food Binder Adoption

Germany’s food binders market is characterized by stringent quality and safety standards, positioning the country as a leader in producing high-quality binders for diverse applications, from meat products to baked goods. The market’s adherence to rigorous regulations ensures compliance with food safety standards, a critical factor for domestic and export-oriented manufacturers.

As part of Europe’s circular economy initiatives, German companies are optimizing the use of binders to extend product shelf life and utilize upcycled ingredients. In addition, the Act on Corporate Due Diligence Obligations in Supply Chains drives transparency and ethical sourcing, encouraging manufacturers to procure sustainably produced raw materials. This focus on environmentally responsible practices enhances the credibility and sustainability of the German food binders industry.

China: Regulatory Standards and Rising Demand for Novel Food Binders

China’s food binders market is shaped by comprehensive government regulations on food additives, including standards such as GB 9685-2016 for additives in food contact materials. These regulations ensure product safety, quality, and compliance, while fostering innovation in binder formulations.

The market is also benefiting from rapid growth in novel foods and processed food sectors, with the National Health Commission actively reviewing innovative applications. New binders derived from fermented mycelium, krill oil, and algae protein are being developed to meet the evolving needs of plant-based, fortified, and functional foods. Rising urbanization and the increasing demand for convenient, ready-to-eat products are further accelerating market adoption and innovation in China.

India: Make in India and Functional Foods Boosting Food Binder Growth

India’s food binders industry is experiencing accelerated growth driven by the Make in India initiative and favorable foreign direct investment policies in the food processing sector. This has led to a boom in local manufacturing, enabling the development of innovative binder solutions to meet domestic demand.

The market is witnessing strong demand for fortified and functional foods, where binders enhance the nutritional profile by adding fiber, protein, or vitamins, while improving texture and product stability. Expansion of India’s food processing infrastructure, including Mega Food Parks and Agro-Processing Clusters, is providing a robust platform for industry growth, fostering innovation and commercialization of novel binder applications.

Brazil: Sustainability and Food Waste Reduction Driving Binder Applications

Brazil’s food binders market is benefiting from the country’s leadership in bio-based and sustainable solutions, with companies producing green polyethylene from sugarcane ethanol for eco-friendly packaging. These developments reduce reliance on fossil fuels and enhance the sustainability of the food supply chain.

The government’s focus on food waste reduction and composting is influencing binder use to extend shelf life and create products from upcycled ingredients, addressing both environmental and economic objectives. Additionally, initiatives to track global supply chain sustainability metrics are encouraging manufacturers to source environmentally and socially responsible raw materials, driving innovation in sustainable binder solutions for the food industry.

Japan: Functional Food Regulation and Innovative Binder Technologies

Japan’s food binders market is uniquely shaped by the Foods with Function Claims (FFC) system, which allows the promotion of functional foods with specific health benefits. This regulatory framework encourages the development of binders that not only enhance texture and stability but also contribute nutritional and functional value to products.

The market emphasizes high-quality and safe ingredients, with Japanese companies pioneering innovative binder materials, such as dietary fibers, to improve mouthfeel, texture, and consistency across a variety of food applications. Regulatory support, combined with a strong culture of food quality and safety, positions Japan as a leader in advanced functional and sustainable binder technologies.

Food Binders Market Report Scope

Food Binders Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2034)

|

$16.8 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Type (Hydrocolloids, Proteins, Fats & Oils, Others), By Source (Natural, Synthetic), By Application (Bakery & Confectionery, Meat Products & Meat Analogs, Dairy & Frozen Desserts, Sauces, Dressings & Soups, Beverages, Convenience Foods, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cargill, Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, DuPont de Nemours Inc., Kerry Group plc, Tate & Lyle PLC, CP Kelco US, Inc., Roquette Frères, DSM-Firmenich AG, ICL Food Specialties, Bunge Limited, Ashland Global Holdings Inc., Corbion N.V., Nexira, Gelita AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Binders Market Segmentation

By Type

- Hydrocolloids

- Proteins

- Fats & Oils

- Others

By Source

By Application

- Bakery & Confectionery

- Meat Products & Meat Analogs

- Dairy & Frozen Desserts

- Sauces

- Dressings & Soups

- Beverages

- Convenience Foods

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Binders Market

- Cargill, Incorporated

- Ingredion Incorporated

- Archer Daniels Midland Company

- DuPont de Nemours Inc.

- Kerry Group plc

- Tate & Lyle PLC

- CP Kelco US, Inc.

- Roquette Frères

- DSM-Firmenich AG

- ICL Food Specialties

- Bunge Limited

- Ashland Global Holdings Inc.

- Corbion N.V.

- Nexira

- Gelita AG

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Food Binders Market, offering comprehensive insights into market dynamics, breakthroughs in natural and plant-based binders, and innovations in sustainable sourcing strategies. The analysis reviews recent mergers, partnerships, and R&D initiatives that are shaping product formulations for meat analogs, bakery items, and functional foods. The report highlights market trends such as the surge in clean-label and upcycled ingredient solutions, precision fermentation for functional proteins, and plant-derived binder adoption to meet consumer demand for transparency, sustainability, and sensory quality. In addition, this report is an essential resource for food manufacturers, ingredient suppliers, product developers, and investors seeking actionable intelligence on global market expansion, competitive positioning, and technology-driven innovations. By integrating historic market performance from 2021 to 2024 with forecast data from 2025 to 2034, USDAnalytics provides a forward-looking view on opportunities, regulatory impacts, and strategic imperatives to enhance market competitiveness and guide decision-making.

Scope Highlights

- Segmentation: By Type (Hydrocolloids, Proteins, Fats & Oils, Others), By Source (Natural, Synthetic), By Application (Bakery & Confectionery, Meat Products & Meat Analogs, Dairy & Frozen Desserts, Sauces, Dressings & Soups, Beverages, Convenience Foods, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ leading companies, including Cargill, Ingredion, ADM, DuPont, Tate & Lyle, CP Kelco, Roquette, DSM-Firmenich, and others.

Methodology

This report is based on a rigorous multi-step research methodology that combines both primary and secondary sources. USDAnalytics conducted extensive primary interviews with industry experts, ingredient manufacturers, food formulators, and distributors to obtain qualitative insights on emerging trends, technological breakthroughs, and regulatory impacts. Secondary research included a thorough review of company reports, patent filings, investor presentations, scientific publications, and trade databases. Market sizing and forecasts were developed using a combination of bottom-up and top-down approaches, integrating historical data, consumption trends, and application-specific adoption rates. All findings were cross-verified with industry stakeholders, and data triangulation was applied to ensure accuracy. The methodology further incorporates competitive benchmarking and scenario-based forecasting to provide a realistic outlook on the Food Binders Market for the period 2025–2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.