Market Overview: Rising Demand for Certified and Sustainable Food Grade Lubricants

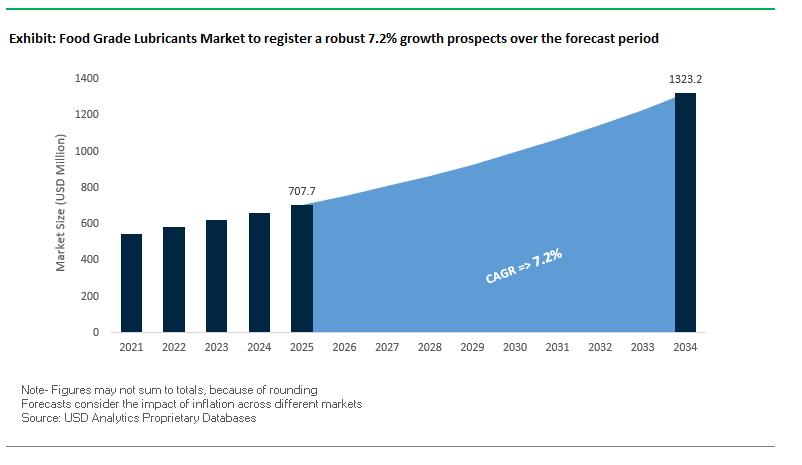

The Global Food Grade Lubricants Market is projected to grow from USD 707.7 million in 2025 to USD 1,323.1 million by 2034, registering a CAGR of 7.2%. This specialized sector provides non-toxic lubricants and greases designed for machinery in food and beverage processing, pharmaceuticals, and cosmetics manufacturing, where contamination prevention and compliance with stringent regulations are critical.

The market is strongly shaped by food safety regulations such as HACCP and NSF certifications (H1, H2, H3), which mandate the use of safe lubricants in food-contact environments. Demand is further fueled by the shift toward bio-based and biodegradable lubricants derived from renewable resources, aligning with sustainability goals.

Advancements in synthetic lubricant formulations are extending equipment life by providing resistance to extreme temperatures, washdowns, and high-load conditions, thereby reducing downtime. Moreover, the rising popularity of user-friendly formats like sprays and aerosols is improving application efficiency in complex production setups.

Key Insights for professionals and Buyers:

- Market expected to exceed USD 1.32 billion by 2034 with a strong CAGR of 7.2%.

- NSF-certified lubricants (H1, H2, H3) are driving compliance in food safety.

- Bio-based and biodegradable lubricants align with circular economy goals.

- Synthetic formulations deliver longer service life and reduced maintenance costs.

- Growing adoption of aerosol and spray formats for precision lubrication.

Market Analysis: Recent Developments in the Food Grade Lubricants Industry

The Food Grade Lubricants industry is witnessing rapid innovation, regulatory compliance measures, and expansion initiatives aimed at sustainability and efficiency.

In August 2025, reports highlighted rising demand for kosher- and halal-certified lubricants, reflecting cultural and dietary compliance needs. That same month, another report emphasized the importance of formulations free from MOSH, MOAH, and PFAS contaminants, aligning with stricter safety regulations.

By July 2025, industry studies connected Food Industry 5.0 concepts with predictive maintenance, reducing acceptable downtime windows and boosting the need for lubricants that provide longer drain intervals. In parallel, another July 2025 report noted surging global demand for bio-based lubricants, particularly in Europe and Asia.

In May 2025, Klüber Lubrication, part of Freudenberg Group, invested USD 16.8 million in its Mysore, India facility, expanding production and strengthening its Asia-Pacific presence. Earlier in February 2025, reports linked petrochemical price fluctuations to a 6% decline in lubricant manufacturing capacity, pressuring suppliers to optimize procurement strategies.

Looking back, in November 2024, a study confirmed that H1 lubricants dominate the market, driven by their suitability for incidental food contact. In December 2024, industry consolidation continued as Hillebrand acquired Braid Logistics, expanding logistics for non-hazardous bulk liquids, indirectly supporting lubricant distribution channels.

Key Trends and Strategic Opportunities Shaping the Food Grade Lubricants Market

Accelerated Adoption of NSF H1 Registered Synthetic Base Stocks

The food grade lubricants market is witnessing a pronounced shift from traditional mineral oil-based H1 lubricants toward high-performance synthetic formulations, particularly those based on polyalphaolefins (PAOs) and synthetic esters. This trend is driven by the need for longer lubricant life, enhanced equipment performance under extreme conditions, and minimized contamination risk during lubricant changes. Publications in specialized industry journals highlight that polyalkylene glycol (PAG) base stocks have enabled gear oils with extended drain intervals and superior anti-wear properties. Leading manufacturers, such as ExxonMobil, offer SpectraSyn™ PAO, which provides robust thermal stability and performance across wide temperature ranges, making it suitable for demanding food and beverage production environments. The adoption of synthetics opens a high-value growth avenue, particularly for high-heat applications like bakery oven chains, where polyolester (POE) fluid technology reduces carbon deposits and extends equipment life. This trend reshapes the value chain, requiring collaboration between synthetic base stock suppliers and lubricant formulators and emphasizing technical education for end-users to realize long-term cost and safety benefits.

Integration of IoT-Enabled Condition Monitoring for Predictive Maintenance

Increasingly, food manufacturers are deploying IoT-enabled sensors to monitor lubricant condition and equipment health in real time. This data-driven approach allows predictive maintenance, optimizing lubricant performance, minimizing unplanned downtime, and providing auditable proof of food safety compliance. The primary driver is operational efficiency, as unplanned downtime can disrupt production schedules and result in lost batches. Companies like Nanoprecise offer wireless sensor solutions for real-time machine health monitoring. Case studies highlight substantial benefits, such as preventing over 16 hours of unplanned downtime by detecting motor imbalances early. This trend establishes a smart lubricant management service, creating a growth avenue where manufacturers can offer real-time monitoring for preventive maintenance, damage reduction, and supply chain optimization. The deployment of IoT also fosters an interconnected value chain among lubricant manufacturers, technology providers, and food processors.

Development of High-Performance, USDA Certified Bio-Based (H1) Lubricants

There is a significant growth opportunity in bio-based lubricants derived from renewable sources like vegetable oils and synthetic esters that meet NSF H1 standards. These lubricants cater to food companies seeking to reduce the environmental footprint of their operations. Drivers include growing demand for sustainable products and programs such as the USDA BioPreferred® and EU Ecolabel, which incentivize the adoption of environmentally acceptable lubricants (EALs). Examples include Bio-Safe EAL Hydraulic Oil made from biodegradable plant-based oils and TotalEnergies’ bio-sourced product range for environmentally sensitive applications. Advances in synthetic ester feedstocks improve oxidative stability and high-temperature performance, making bio-based lubricants competitive with petroleum-based counterparts. The commercialization of these products provides manufacturers a way to appeal to environmentally conscious consumers and meet sustainability mandates, particularly in regions with strict environmental regulations.

Expansion of Comprehensive Lubricant Management and Auditing Services

Beyond product sales, value-added services such as full-site lubricant audits, in-plant training programs, and digital management systems offer a significant opportunity. This holistic approach ensures compliance with ISO 21469, reduces total cost of ownership, and strengthens long-term customer relationships. TotalEnergies’ software-based lubricant management service, for instance, helps customers track machinery needs and maintenance schedules, resulting in measurable cost reductions, such as a reported 4.5% decrease in lubricant costs for a national industrial manufacturer. Offering comprehensive management programs positions manufacturers as trusted partners, shifting the industry from a transactional model to a partnership-based model. This opportunity fosters collaboration throughout the value chain, emphasizing efficiency, compliance, and optimized maintenance practices.

Competitive Landscape: Key Players in the Food Grade Lubricants Market

The Global Food Grade Lubricants Market is shaped by multinational energy companies, independent lubricant specialists, and innovators expanding their product portfolios and global presence to meet rising safety and sustainability standards.

ExxonMobil Corporation strengthens with Mobil SHC Cibus™ series

ExxonMobil leverages its global brand strength and advanced R&D to lead in high-performance lubricants. Its Mobil SHC Cibus™ line is NSF H1-certified, catering to diverse food and beverage applications. A notable innovation, Mobil Gargoyle Arctic SHC 226E, has shown 200% extended oil drain intervals, reducing downtime. ExxonMobil combines product strength with services like oil analysis and consultation, offering complete lubrication solutions.

Fuchs Petrolub SE leads with CASSIDA and carbon-neutral goals

Fuchs, the world’s largest independent lubricant producer, stands out with its CASSIDA synthetic line, lasting three to four times longer than mineral oils. Aligned with its FUCHS2025 strategy, the company targets carbon-neutral lubricants by 2025 while eliminating MOSH, MOAH, and PFAS. Its Lubrication Critical Control Point (LCCP) service helps clients navigate HACCP standards, strengthening its customer-centric positioning.

TotalEnergies SE expands with Nevastane food-grade lubricants

TotalEnergies provides its Nevastane product line, a comprehensive NSF H1 and 3H-approved range for food environments, compliant with FDA 21 CFR 178.3570. Beyond lubricants, TotalEnergies integrates services like LubAnac oil analysis and TIG6 maintenance software, reinforcing its complete solution approach. It is also pioneering bio-sourced lubricants and water-based fluids for wider industrial use.

Shell plc advances with Cassida and carbon-neutral lubricants

Shell offers a wide range of food-grade lubricants under the Shell Cassida brand, including hydraulic fluids, gear oils, and greases designed for demanding environments. Shell is also pushing sustainability with biodegradable and carbon-neutral lubricants, enabling customers to meet regulatory and ESG goals. Its services include oil monitoring and on-site support, optimizing plant efficiency and extending machinery life cycles.

Chevron Corporation innovates with Clarity® Synthetic EA Gear Oils

Chevron utilizes its premium synthetic base oils to deliver high-performance food-grade lubricants. Its Clarity® Synthetic EA Gear Oil stands out as a biodegradable solution compliant with stringent environmental standards. Chevron supports food and beverage manufacturers with products that provide oxidation resistance, wear protection, and long equipment life, while collaborating with additive developers to meet evolving safety and sustainability regulations.

Food Grade Lubricants Market Share Insights

Food and Beverage Processing Leads Market Share by Application in Food Grade Lubricants

Food and beverage processing dominates the food-grade lubricants market with 75% share in 2025, driven by the ubiquity of processing machinery requiring certified, contamination-free lubrication. From mixers, conveyors, and homogenizers to high-speed filling and packaging equipment, every machine in the food supply chain depends on H1-registered lubricants to safeguard consumer safety while meeting global standards such as NSF certification. Pharmaceuticals and healthcare represent a smaller but highly regulated application, where lubricants must meet GMP, FDA, and EMA guidelines, ensuring zero tolerance for contamination in sensitive drug manufacturing environments. Animal feed and cosmetics also adopt food-grade lubricants under similar hygiene-driven principles, though their overall consumption volumes remain smaller. This segmentation highlights how food and beverage processing anchors the market’s scale, while pharmaceuticals establish benchmarks for compliance, and adjacent industries expand adoption under similar purity requirements.

Hydraulic Oils and Greases Lead Market Share by Product Type in Food Grade Lubricants

Within the food-grade lubricants market, hydraulic oils hold the largest share at 35% in 2025, reflecting their critical role in powering the hydraulic systems of modern food processing plants. These oils must combine thermal stability, water resistance, and incidental food contact safety to ensure both operational continuity and regulatory compliance. Greases follow closely with 30% share, owing to their ubiquitous use in bearings, joints, chains, and guides where persistent lubrication is needed under exposure-prone conditions. Their adhesion and durability make them indispensable for maintaining uptime and minimizing wear. Gear oils, compressor oils, and chain oils together represent specialized but essential categories, safeguarding high-load gearboxes, pneumatic compressors, and conveyor chains in wash-down environments. Collectively, this segmentation shows how hydraulic oils and greases dominate through sheer scale and ubiquity, while specialized lubricants enable high-performance reliability in specific machinery functions across food and pharmaceutical plants.

United States Food Grade Lubricants Market Driven by FDA Guidelines and High-Performance Innovations

The U.S. food grade lubricants market operates under a fragmented regulatory environment, with the FDA providing detailed guidelines for H1 lubricants under 21 CFR 178.3570. While the USDA’s food-grade lubricant approval program ended in 1998, the NSF has become a key certification body, and ISO 21469 compliance is increasingly critical for manufacturers. Technological advancements are shaping the market, with ExxonMobil introducing its synthetic NSF H1 registered Mobil SHC Cibus Series, offering high-performance lubrication for extreme conditions such as freezers and cookers.

Corporate investments are further boosting market growth, as companies develop lubricants that are nut-, wheat-, and gluten-free, while also adhering to Kosher and Halal dietary laws. Key applications include food and beverage processing and pharmaceuticals, driven by the rising need for contamination-free operations and automation in manufacturing plants. Sustainability is a growing priority, with the adoption of bio-based oils and phasing out of PFAS chemistries encouraging the development of safer, environmentally-friendly lubricants.

Germany Food Grade Lubricants Market Advances with Circular Economy and Regulatory Compliance

Germany’s food grade lubricants market is governed by a stringent regulatory framework, including the EU’s Packaging and Packaging Waste Regulation (PPWR), emphasizing reusable and recyclable materials. Technological innovation is a strong driver, with manufacturers developing specialized lubricants for high-value food products and advanced barrier films to prevent contamination during transport.

Germany’s leadership in the circular economy supports the adoption of biodegradable and multi-use lubricants, particularly in the food and beverage, and chemical sectors. A robust manufacturing base and significant export activity for specialty foods, such as beer and wine, underpin strong demand for reliable, high-quality lubricants. Innovation and regulatory compliance make Germany a key hub for sustainable food-grade lubrication solutions in Europe.

China Food Grade Lubricants Market Expands with Dual Carbon Initiatives and Strategic Partnerships

China’s food grade lubricants market is influenced by the government’s “dual carbon” objectives, encouraging green manufacturing and sustainable materials. Technological advancements, including automation, AI, and “5G plus industrial internet” integration, are enhancing production efficiency and flexible capacity. Corporate developments, such as Vickers Oils partnering with XIANGXINGCHENG PetroChemical Co., demonstrate foreign investment and an increasing focus on expansion within China.

Key applications include the rapidly growing food and beverage delivery and manufacturing sectors, requiring large volumes of high-quality lubricants. Domestic manufacturing is being prioritized, with local companies expanding production to meet the increasing demand for safe, circular, and high-performance products. These trends position China as a key growth market for both domestic and international food-grade lubricant suppliers.

India Food Grade Lubricants Market Strengthened by Circular Economy Policies and Automation

India’s food grade lubricants market is benefiting from government initiatives promoting a circular economy, including the FSSAI’s Eat Right India program that emphasizes safe, healthy, and sustainable food processes. Technological advancements are accelerating, with increasing adoption of high-performance lubricants optimized for automated food processing machinery.

Corporate investments, such as Klüber Lubrication’s USD 16.8 million expansion in Mysore, support capacity growth to meet rising demand in the food and beverage industry. The Make in India initiative is fostering domestic manufacturing and innovation, while exports of processed food products are driving demand for modern, high-performance lubricants. These trends establish India as a rapidly growing market for food-grade lubrication solutions.

Japan Food Grade Lubricants Market Focused on High-Performance, Specialty Products

Japan’s food grade lubricants industry benefits from advanced manufacturing technologies and a focus on sustainable solutions. Regulatory guidance from the Plastic Resource Circulation Act encourages environmentally-conscious material use, indirectly influencing lubricant development.

High-performance specialty lubricants, including polyalphaolefins and esters, are gaining traction due to their ability to withstand wide temperature ranges, enhancing machinery efficiency and longevity. Japanese manufacturers continue to innovate with value-added properties, positioning the country as a leader in precision and high-performance food-grade lubricants in the Asia-Pacific region.

Brazil Food Grade Lubricants Market Accelerates with Sustainable Innovation and Automation

Brazil’s food grade lubricants market is influenced by government-led sustainable waste management initiatives, including amendments to the National Solid Waste Policy in January 2025 promoting domestic recycling and circular economy practices. Technological advancements such as robotics and AI are improving production efficiency, quality control, and automation in labeling and defect detection.

Key applications are shifting toward premium and specialized digital lubrication solutions, providing extended service life while maintaining product quality and safety. Sustainability initiatives are strong, exemplified by iFood partnering with XPRIZE to develop flexible, biodegradable packaging, reflecting Brazil’s growing commitment to eco-friendly food-grade lubricant solutions.

Food Grade Lubricants Market Report Scope

Food Grade Lubricants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$707.7 Million

|

|

Market Size (2034)

|

$1323.1 Million

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Base Oil Type (Mineral Oil, Synthetic Base Oil, Bio-Based Oil), By Application (Food & Beverage Processing, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Animal Feed), By Product Type (Hydraulic Oils, Gear Oils, Compressor Oils, Greases, Chain Oils)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Fuchs SE, ExxonMobil Corporation, Shell plc, TotalEnergies SE, Chevron Corporation, Castrol (BP plc), Klüber Lubrication München SE & Co. KG, SKF AB, ConocoPhillips, The Dow Chemical Company, Petro-Canada Lubricants Inc., Lubriplate Lubricants Co., Calumet Specialty Products Partners, L.P., JAX Inc., Matrix Specialty Lubricants BV

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Grade Lubricants Market Segmentation

By Base Oil Type

- Mineral Oil

- Synthetic Base Oil

- Bio-Based Oil

By Application

- Food & Beverage Processing

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Animal Feed

By Product Type

- Hydraulic Oils

- Gear Oils

- Compressor Oils

- Greases

- Chain Oils

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Grade Lubricants Market

- Fuchs SE

- ExxonMobil Corporation

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- Castrol (BP plc)

- Klüber Lubrication München SE & Co. KG

- SKF AB

- ConocoPhillips

- The Dow Chemical Company

- Petro-Canada Lubricants Inc.

- Lubriplate Lubricants Co.

- Calumet Specialty Products Partners, L.P.

- JAX Inc.

- Matrix Specialty Lubricants BV

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and multi-layered research methodology to deliver an in-depth analysis of the Global Food Grade Lubricants Market. Our approach combined extensive primary research—including interviews with industry leaders, lubricant manufacturers, machinery operators, and regulatory specialists—with rigorous secondary research using company reports, trade journals, industry publications, and regulatory filings. Market sizing and forecasts were developed across base oil types (mineral, synthetic, bio-based), product types (hydraulic oils, gear oils, greases, compressor oils, chain oils), and applications (food & beverage processing, pharmaceuticals, cosmetics, animal feed). We analyzed emerging trends such as the shift toward synthetic H1-registered lubricants, bio-based formulations, IoT-enabled condition monitoring, and comprehensive lubricant management services. Regional dynamics covering the U.S., Germany, China, India, Japan, and Brazil were evaluated with a focus on regulatory frameworks, sustainability initiatives, and technological adoption. Competitive analysis highlighted leading players like ExxonMobil, Fuchs SE, Shell, TotalEnergies, and Chevron, emphasizing innovations, acquisitions, and global expansion strategies. This methodology ensures that industry professionals, investors, and stakeholders gain actionable, data-driven insights into market growth drivers, emerging opportunities, and evolving compliance and sustainability requirements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.