Market Overview: Food Storage Container Industry Growth Fueled by Plastic Dominance and E-commerce Expansion

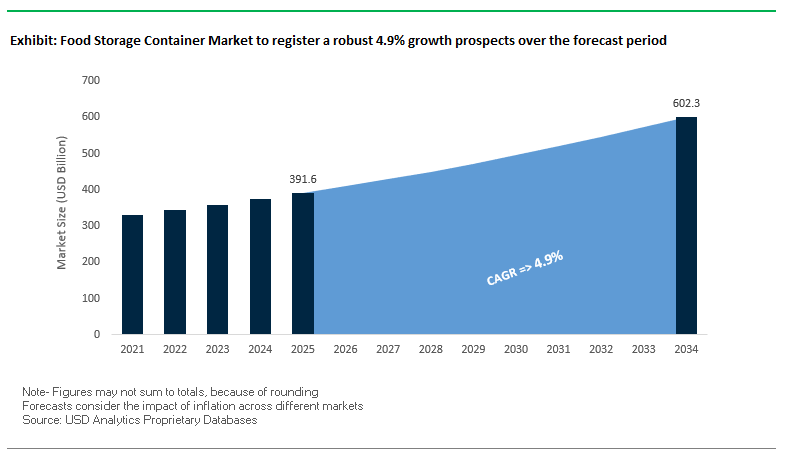

The Food Storage Container Market is valued at $391.6 billion in 2025 and is projected to reach $602.3 billion by 2034, growing at a steady CAGR of 4.9%. This expansion is driven by the rising demand for convenient, airtight, and eco-friendly storage solutions across households and foodservice sectors. Plastic continues to dominate as the most widely used material, due to its lightweight, durable, and affordable nature, making it essential for meal preparation, takeaway services, and bulk storage applications.

Glass containers are increasingly carving out a premium position, favored by eco-conscious consumers for being non-toxic, odor- and stain-resistant, and reusable. This segment is particularly strong among urban professionals and health-focused households seeking safe and sustainable alternatives. The market is also driven by rising consumer expectations for airtight, leak-proof functionality, which has become a key purchasing criterion in both plastic and glass categories.

The rapid growth of e-commerce platforms is transforming market dynamics, enabling direct-to-consumer food storage brands to thrive. Online retail channels provide consumers access to innovative and aesthetically designed storage solutions, while companies leverage digital platforms for personalized marketing, global reach, and recurring subscription-based sales models.

Key Insights for Industry Professionals

- Plastic remains dominant: Cost-effective and durable, widely used across residential and commercial segments.

- Glass rising in premium: Non-toxic, reusable, and eco-friendly, glass is gaining traction in high-value markets.

- Airtight features drive demand: Leak-proof seals and freshness-retaining designs are major consumer priorities.

- E-commerce accelerates growth: Online platforms enable new brand entrants and reshape consumer buying behavior.

Market Analysis: Recent Developments Reshaping the Food Storage Container Industry

The food storage container market has witnessed significant strategic shifts, product launches, and partnerships that reflect consumer demand for innovation, convenience, and sustainability.

In August 2025, Newell Brands announced its participation at the Barclays Global Consumer Staples Conference to update stakeholders on its strategic priorities, including innovations from its Rubbermaid line. Around the same time, Lock & Lock launched a new marketing campaign in Southeast Asia to promote freezer-safe containers, highlighting their effectiveness in preserving food freshness in frozen environments. In July 2025, Rubbermaid introduced modular, stackable food storage containers designed for smaller kitchens, reflecting the growing demand for space optimization solutions.

In September 2025, a global food services company partnered with a plastic container manufacturer to develop reusable, returnable food storage containers, marking a push toward closed-loop systems in commercial kitchens. Earlier in June 2025, the merger between IPL and Schoeller Allibert created a major force in reusable packaging, reinforcing the role of reusables in foodservice and industrial supply chains.

Product diversification is also evident in brand repositioning. In August 2024, YETI, a brand recognized for outdoor coolers, entered the household segment with a new line of durable storage containers. Meanwhile, Tupperware Brands, in March 2024, shifted its distribution model from direct-selling to multi-channel retail and e-commerce, expanding consumer access.

Emerging Trends and Opportunities Driving the Food Storage Container Market

Food Storage Container Market Embraces Smart Innovation and Sustainable Material Transition

The food storage container market is rapidly evolving as consumers, brands, and regulators push for healthier, safer, and more sustainable solutions. Two powerful trends material transitions away from plastics and the adoption of smart, connected storage systems are reshaping the industry. At the same time, new opportunities are arising from the use of ocean-bound recycled plastics and modular, space-efficient designs tailored to modern urban lifestyles. These shifts highlight how innovation in materials, technology, and design is setting the stage for long-term growth and competitive differentiation in the global food storage container market.

Material Transition from Plastics to Engineered Glass and Stainless Steel

One of the most profound shifts in the food storage container market is the move away from conventional plastics even BPA-free options toward premium materials such as engineered glass and stainless steel. Consumers increasingly perceive these materials as healthier, more durable, and more sustainable. A survey across the U.S., Canada, and Europe revealed that more than 40% of consumers have abandoned a purchase due to unsustainable packaging, underscoring the urgency for brands to diversify their portfolios. Engineered glass, particularly soda-lime and borosilicate glass, is prized for its thermal shock resistance and non-porous properties, preventing odor retention and ensuring long-term durability. Similarly, 304-grade stainless steel is emerging as a premium option due to its corrosion resistance and compatibility with both hot and cold storage. Leading corporations such as Unilever are investing in plastic-free portfolios, committing to collect and process more plastic than they sell. These strategic initiatives are accelerating the adoption of glass and stainless steel solutions, ensuring that the food storage container market aligns with consumer demand for healthier and eco-friendly products.

Integration of Smart Technology for Food Freshness and Inventory Management

Food storage containers are moving beyond passive preservation to active monitoring and inventory management systems, enabled by smart technologies. IoT-enabled sensors embedded within containers can monitor temperature, humidity, and even gases such as methane that signal spoilage. These technologies provide real-time alerts, enabling households and commercial kitchens to reduce food waste and maintain product freshness. Startups are rolling out connected solutions that integrate with mobile apps, giving users insights into shelf life, storage conditions, and inventory tracking. In large-scale foodservice operations, blockchain and AI-powered systems are being piloted to ensure full-chain traceability and rapid response to contamination risks. For example, IoT-based monitoring platforms in freezers and storage units have reduced spoilage incidents by more than 20% in early trials. By transforming containers into active data carriers, the industry is addressing the dual challenge of food waste reduction and supply chain optimization, a capability that will increasingly define competitive differentiation in the food storage container market.

Development of High-Performance, Ocean-Bound Plastic PCR Containers

The incorporation of ocean-bound plastic (OBP) into food storage containers represents a critical opportunity to marry sustainability with performance. OBP initiatives intercept plastic waste in coastal areas before it enters the ocean, transforming it into high-value, food-grade resins. Companies have already achieved FDA No Objection Letters (NOLs) confirming the safety of 100% OBP in direct food-contact applications, setting the stage for premium offerings in the market. This creates a pathway for brands to launch certified sustainable product lines while addressing consumer demand for eco-conscious solutions. Collaborations between chemical companies, resin producers, and consumer brands such as SABIC’s partnership with film manufacturers and seafood companies are demonstrating how OBP can be reintegrated into the circular economy. Beyond its environmental impact, OBP-based containers represent a storytelling opportunity for brands to showcase measurable sustainability impact, thereby strengthening consumer trust and loyalty.

Proliferation of Modular and Space-Optimized Container Systems for Urban Living

The rise of compact urban living and smaller households is driving demand for modular, stackable, and space-optimized container systems that maximize pantry and refrigerator efficiency. Unlike traditional round or rectangular designs, new container systems are engineered to interlock, nest, and adapt seamlessly to varied kitchen spaces. Reports highlight that modular systems not only improve space utilization but also enhance meal preparation and organization, making them particularly appealing for time-constrained urban consumers. Aesthetic considerations are equally important consumers increasingly demand minimalist designs, clear lids or windows for easy content visibility, and multi-functional features such as oven-to-fridge versatility. Modular systems are also gaining traction in premium product lines, where innovation in form and function aligns with modern kitchen design trends. By addressing both practical and lifestyle-driven needs, modular and stackable containers represent a fast-growing segment of the food storage container market that caters directly to evolving consumer demographics.

Competitive Landscape: Leading Companies in the Global Food Storage Container Market

The food storage container market is led by consumer goods giants and specialized brands leveraging innovation, sustainability, and strong retail networks. Companies are focusing on eco-friendly materials, airtight technologies, and premium design to meet evolving consumer needs.

Newell Brands: Expanding with Sustainable Rubbermaid and Sistema Solutions

Newell Brands, owner of Rubbermaid and Sistema, is a global leader in food storage solutions. Rubbermaid’s Brilliance line is known for airtight, leak-proof seals and stain-resistant designs, making it a top choice among consumers. In July 2025, it launched modular stackable containers for space-conscious households, while Sistema introduced containers made with 35% ocean-bound plastic, aligning with sustainability goals. Newell’s Design for Sustainability framework underpins its long-term strategy to reduce PVC and EPS use.

Tupperware Brands: Transitioning to Multi-Channel Distribution

Tupperware remains an iconic name in food storage, built on its airtight plastic containers. In March 2024, it shifted from a pure direct-selling model to multi-channel distribution, forging partnerships with major retailers and strengthening its e-commerce presence. Its innovations include Vent N Serve steaming containers, Modular Mates for organization, and ECO+ products made from mixed plastic waste. This strategic shift broadens Tupperware’s reach and enhances its positioning in premium and eco-conscious markets.

Lock & Lock Co.: Leveraging Patented Airtight Locking Systems

Lock & Lock is renowned for its four-sided locking system, providing secure, airtight, and leak-proof seals. In August 2025, the company launched a new campaign in Southeast Asia for freezer-safe containers, tapping into regional demand. Its Top Class glass containers with detachable silicone clips improve hygiene and ease of cleaning. Lock & Lock’s diversified range serves meal prep, pantry storage, and niche needs such as fermented food and baby food storage.

Sterilite Corporation: Providing Affordable Everyday Food Storage Solutions

Sterilite offers a wide range of polypropylene and polyethylene containers that are BPA- and phthalate-free. Its Ultra•Seal line with gasketed lids caters to consumers demanding airtight and leak-proof storage. Known for affordability and wide availability through major retailers, Sterilite’s focus is on functional, mass-market products. Its core strength lies in producing durable and cost-effective food storage containers that cater to the daily needs of mainstream households.

The Conair Group: Leveraging Cuisinart Brand for Kitchen Ecosystem Integration

Conair, best known for personal care, has built a strong food storage presence through its Cuisinart brand. Its storage containers are positioned as part of an integrated kitchenware ecosystem, often sold with other appliances. Conair’s focus is on lifestyle innovation, offering on-the-go and at-home solutions that align with its strategy of blending functionality with design appeal. Its wide retail distribution and brand equity make it a notable competitor in premium and mid-range markets.

Food Storage Container Market Share Insights

Boxes & Containers Lead Market Share by Product Type in Food Storage Containers

Boxes and containers secure the largest share of the food storage container market, accounting for 45% of global demand, largely because they combine reusability, durability, and material versatility. Polypropylene remains dominant due to cost-effectiveness, but the segment is undergoing a material revolution as consumers increasingly adopt glass and stainless steel containers for their non-toxic, stain-resistant, and oven-safe properties. This shift is fueled by heightened awareness of food safety and the rising importance of sustainability in consumer purchase decisions. The segment is also a hub of design innovation, with stackable modular formats, airtight silicone seals, and smart freshness indicators transforming containers into multifunctional kitchen assets. Their ability to bridge both in-home storage and on-the-go convenience solidifies their leadership within the broader food preservation landscape.

Household Applications Dominate Market Share by End-Use Industry in Food Storage Containers

The household segment represents 75% of the food storage container market, reflecting the category’s penetration into everyday consumer lifestyles. Demand is driven not only by food preservation and storage needs but also by the growing influence of home organization trends amplified by social media platforms. Households are increasingly prioritizing BPA-free, non-toxic, and reusable options, with significant traction for premium glass sets, modular container systems, and sustainable materials. The dominance of households is further reinforced by the replacement cycle, as consumers regularly update containers for aesthetics, safety, or convenience. While the commercial sector values durability and efficiency, the household market sets the pace for innovation, brand competition, and sustainability integration, making it the primary revenue engine for global food storage container manufacturers.

United States: Smart and Sustainable Food Storage Containers Drive Market Growth

The U.S. food storage container market is experiencing strong growth, fueled by increasing consumer demand for sustainability and eco-friendly solutions. Consumers and corporations are prioritizing durable, reusable, and stackable containers made from materials like glass, stainless steel, and BPA-free plastics. Technological advancements, including freshness-indicator lids and QR codes that provide information on inventory and expiration dates, are transforming conventional containers into smart storage solutions, enhancing food management for households.

Sustainability is a key market driver. YETI, for instance, launched a new line of food storage containers in October 2024 made from 50% recycled plastic, highlighting the shift toward eco-conscious consumer preferences. The rapid growth of e-commerce, which contributed over 45% of retail market value by 2029, has increased demand for modular and aesthetically designed storage solutions. Regulatory oversight, including FDA approvals under the FDCA and Food Contact Notification (FCN) system, ensures food safety and chemical compliance, making the U.S. market a highly regulated yet rapidly innovating landscape for smart and sustainable food storage containers.

Germany: Circular Economy and Innovation Propel Eco-Friendly Container Demand

Germany’s food storage container industry is strongly influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates fully recyclable packaging by 2030 and sets reuse and refill targets. Consumer preference is increasingly shifting toward reusable glass and stainless steel containers, aligning with Germany’s leadership in the circular economy and sustainable lifestyle practices.

Technological innovation is driving product differentiation. Companies like LocknLock have introduced eco-containers made from recycled materials, reflecting the market’s focus on green consumption. Rising demand for multi-functional containers that support meal prepping and on-the-go consumption is further fueling market expansion. Overall, Germany is positioning itself as a pioneer in sustainable, innovative, and convenient food storage solutions, combining regulatory compliance with eco-conscious consumer trends.

China: Government Initiatives and E-Commerce Expansion Boost Premium Food Storage Containers

China’s food storage container market is being transformed by governmental sustainability initiatives, including the dual carbon goal to achieve carbon peak and carbon neutrality. Policies promoting eco-friendly and reusable materials are driving innovation in container design and production, with a notable focus on premium airtight glass storage kits.

Technological advancements, such as the integration of 5G and industrial internet technologies combined with AI, are optimizing production efficiency and enabling flexible manufacturing processes. The rapid expansion of domestic e-commerce platforms is a significant growth driver, with online sales of bundled kitchenware products spurring innovation in container designs and promoting localized product development. China’s market reflects a combination of government-led sustainability initiatives, technological modernization, and e-commerce-driven consumer demand, creating a highly dynamic food storage container industry.

India: Home-Based Solutions and Regulatory Support Drive Sustainable Container Adoption

India’s food storage container market is expanding due to growing home-based cooking trends, meal prepping, and efficient kitchen organization needs. Government initiatives, including the Ministry of Food Processing Industries’ schemes like the Integrated Cold Chain and Value Addition Infrastructure, are promoting the adoption of efficient storage solutions. Investments in food processing infrastructure are also creating demand for high-quality storage systems.

Sustainability is a critical market driver. The Plastic Waste Management (Amendment) Rules are encouraging the adoption of eco-friendly and reusable containers, meeting consumer demand for sustainable kitchen solutions. The Indian market is thus characterized by regulatory support, infrastructure investments, and rising consumer focus on home-based and sustainable storage solutions, positioning it as a fast-growing hub for innovative and eco-conscious food storage containers.

Food Storage Container Market Report Scope

Food Storage Container Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$391.6 Billion

|

|

Market Size (2034)

|

$602.3 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Glass, Plastic, Metal, Silicone, Other Materials), By Product Type (Boxes, Jars & Bottles, Bags & Pouches, Others), By End-Use Industry (Household, Commercial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Newell Brands Inc., Tupperware Brands Corporation, LocknLock Co., Amcor plc, Berry Global Inc., Zojirushi Corporation, OXO, Rubbermaid Commercial Products LLC, Yeti Holdings, Inc., Silgan Holdings Inc., The ONE Group, VWR International, O-I Glass, Inc., Anchor Hocking, Fuling Global Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Storage Container Market Segmentation

By Material Type

- Glass

- Plastic

- Metal

- Silicone

- Other Materials

By Product Type

- Boxes

- Jars & Bottles

- Bags & Pouches

- Others

By End-Use Industry

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Storage Container Market

- Newell Brands Inc.

- Tupperware Brands Corporation

- LocknLock Co.

- Amcor plc

- Berry Global Inc.

- Zojirushi Corporation

- OXO

- Rubbermaid Commercial Products LLC

- Yeti Holdings, Inc.

- Silgan Holdings Inc.

- The ONE Group

- VWR International

- O-I Glass, Inc.

- Anchor Hocking

- Fuling Global Inc.

* List Not Exhaustive

Methodology

USDAnalytics utilized a multi-layered research methodology combining primary and secondary sources to deliver a precise and actionable analysis of the global Food Storage Container Market. Primary research included interviews with leading industry stakeholders such as manufacturers, distributors, retail experts, and sustainability consultants to capture insights on material preferences, design innovation, and consumer behavior. Secondary research involved detailed examination of company reports, press releases, regulatory guidelines, industry publications, and e-commerce data to validate market trends, mergers, strategic initiatives, and sustainability-driven transformations. Market sizing and forecasting were derived from historical sales data, production volumes, adoption rates across plastic, glass, stainless steel, and silicone containers, and regional consumption trends. Segmentation was conducted by material type, product format, and end-use industry, while qualitative analysis emphasized innovations such as airtight and modular designs, smart storage technologies, ocean-bound recycled plastics, and urban lifestyle adaptations. This methodology provides industry professionals with a robust, data-driven understanding of market dynamics, competitive landscapes, growth opportunities, and sustainability initiatives shaping the Food Storage Container Market through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.