Fracking Water Treatment Market Overview

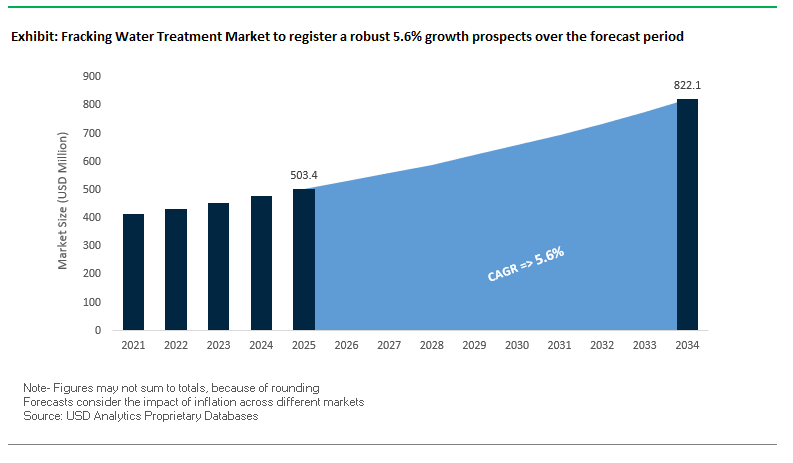

The global fracking water treatment market is projected to grow from $503.4 billion in 2025 to $822 billion by 2034, at a CAGR of 5.6%. This market growth is largely driven by the oil and gas industry’s increasing emphasis on sustainable water management, particularly in arid regions where freshwater scarcity is a pressing concern. Fracking operators are increasingly treating and reusing flowback and produced water to reduce freshwater dependence and meet strict environmental regulations.

The adoption of modular and mobile water treatment systems allows on-site treatment, reducing transportation costs and environmental impact while enhancing operational efficiency. Furthermore, innovative technologies are enabling resource recovery, where treated water can be repurposed for agricultural or industrial use. These developments are critical for companies seeking to optimize operations, comply with regulatory mandates, and improve sustainability in hydraulic fracturing processes.

Key Insights for Industry Stakeholders:

- Sustainable Water Management: Reuse of flowback and produced water reduces freshwater dependency.

- Regulatory Compliance: Advanced on-site treatment solutions help meet EPA and regional wastewater regulations.

- Mobile and Modular Systems: Quick deployment at well sites cuts costs and environmental footprint.

- Resource Recovery: Treated water can be reused for irrigation or industrial purposes.

- Operational Efficiency: Integrated water treatment solutions optimize logistics and reduce operational risks.

Market Analysis: Recent Developments in Fracking Water Treatment

The fracking water treatment market has experienced significant developments from 2024 to 2025, driven by technological innovation and strategic expansions. In August 2025, RSE opened a new office in Milwaukee, Wisconsin, to provide modular biological and nature-based treatment technologies, targeting North American fracking operations. During the same month, Grundfos completed the acquisition of Newterra, enhancing its portfolio of modular, scalable water treatment solutions for oil and gas, including fracking applications.

In March 2025, Siemens and KETOS announced a partnership to integrate real-time water intelligence with AI-driven analytics, improving the efficiency of industrial and municipal water management systems a technology adaptable to fracking water treatment. Veolia Environnement’s February 2025 collaboration with Mistral AI introduced generative AI for resource optimization, emphasizing AI-enabled water treatment solutions. In January 2025, a Canadian research initiative advanced electrocoagulation and ultrasound technology for fracking wastewater, achieving up to 90% removal of suspended solids and oil, with potential for mobile deployment.

Strategic acquisitions have further strengthened market capabilities. Xylem Inc. acquired Idrica in December 2024, enhancing digital and analytics capabilities for water management, while Diehl Metering acquired PREVENTIO GmbH in November 2024, boosting real-time monitoring and predictive maintenance expertise. Additionally, ExxonMobil’s acquisition of Pioneer Natural Resources in October 2024 accelerated the net-zero Permian ambition to 2035, signaling substantial investment in advanced fracking water treatment and recycling infrastructure.

Key Trends Driving Fracking Water Treatment Adoption

Regulatory Compliance and Real-Time Monitoring

The fracking water treatment market is increasingly shaped by regulatory pressures and the need for continuous effluent monitoring. The U.S. Environmental Protection Agency (EPA) emphasizes real-time oversight of fracking wastewater to mitigate localized environmental impacts. Academic studies, such as the 2024 MDPI review, confirm that IoT-enabled monitoring systems provide real-time data on pH, temperature, and chemical concentrations, ensuring compliance with strict discharge standards. This trend drives investment in sensor networks and cloud-based monitoring platforms, allowing operators to proactively manage water quality and reduce regulatory risk.

AI and Machine Learning for Predictive Operations

Integration of AI and machine learning with IoT sensors is revolutionizing fracking water management. According to a 2025 ResearchGate study, AI models analyze large datasets to optimize chemical dosing, predict equipment failures, and reduce operational costs. Companies leveraging these technologies achieve up to 20% chemical savings and significant energy reductions while maintaining treatment efficiency. Predictive maintenance, enabled by early detection of wear in pumps and treatment equipment, minimizes downtime, extends equipment lifespan, and enhances operational resilience in capital-intensive fracking operations.

Water Reuse and Circular Economy Strategies

The drive toward water reuse and circular economy solutions is transforming the fracking water treatment market. Fracking operations generate high volumes of produced and flowback water, often contaminated with salts, hydrocarbons, and heavy metals. Real-time monitoring and smart chemical dosing systems facilitate recycling of treated water for subsequent fracking operations, reducing dependence on freshwater sources. This approach also mitigates environmental impacts and lowers logistics costs, offering both economic and sustainability benefits. Companies adopting on-site water treatment and reuse systems are capitalizing on this growing trend.

Emerging Opportunities in Fracking Water Treatment Market

The market presents opportunities in advanced membrane filtration, electrocoagulation, and thermal evaporators, as well as in integrated AI and IoT-based treatment solutions. As operators face rising freshwater costs and stricter regulations, solutions enabling on-site treatment, reuse, and predictive operations are in high demand. Service providers offering turnkey treatment solutions and OPEX-based service models can capture growing market share, especially in shale-focused regions dominated by horizontal wells. Sustainability-focused technologies and equipment that enhance water recovery rates offer long-term growth potential.

Market Share Insights of Fracking Water Treatment Market

Market Share by Service & Equipment: Equipment Dominates, Services Grow

The treatment equipment segment (58.5%) dominates the market due to its role as the primary capital expenditure in fracking water management, encompassing membrane filtration, electrocoagulation, DAF, and thermal evaporators. The services segment (44.1%) is growing steadily, driven by the outsourcing of design, operation, maintenance, and waste disposal to specialized providers. Innovation in compact, energy-efficient, and high-recovery equipment is enhancing market value, while the services segment supports operational efficiency and reduces OPEX for operators.

Market Share by Source Water Type: Produced Water Leads Volumes

Produced water (54.2%) represents the largest segment by volume, as it is continuously generated throughout the well lifecycle. Flowback water (32.8%) receives immediate attention due to high contaminant concentrations, necessitating rapid treatment for recycling. Freshwater/makeup water (11.8%) is minimized as operators increasingly rely on recycled water, reducing environmental impact and freshwater acquisition costs. Efficient source water management underpins the economics and sustainability of fracking operations.

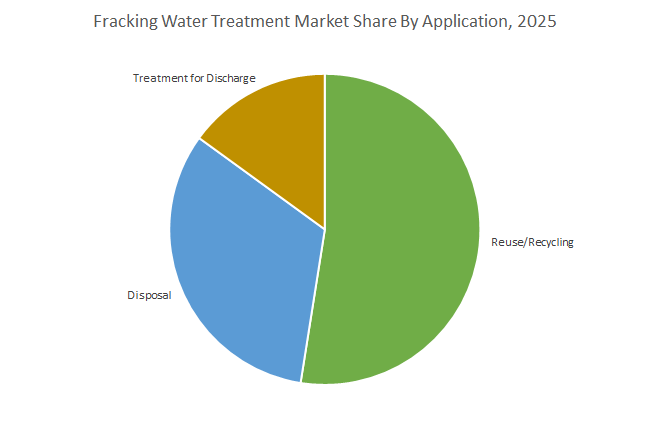

Market Share by Application: Reuse and Recycling Set the Pace

Reuse/recycling (54.2%) is the fastest-growing application, driven by the need to reduce freshwater consumption, lower logistics costs, and support circular water strategies. Disposal (32.8%), primarily via deep-well injection, remains necessary in areas lacking recycling infrastructure but faces rising costs and regulatory scrutiny. Treatment for discharge (11.8%) represents a small but technologically advanced segment, offering the potential for full closed-loop water management. This shift highlights the market’s focus on sustainable, high-value water treatment solutions.

Market Share by Well Type: Horizontal Wells Define Market Demand

The horizontal wells segment (90–95%) overwhelmingly drives the fracking water treatment market due to their high water requirements in shale oil and gas operations. The massive water volumes per well create strong demand for advanced treatment and recycling systems. In contrast, vertical wells have negligible market impact, with treatment often handled by low-cost, direct disposal methods. The dominance of horizontal drilling underscores the market’s reliance on high-capacity, efficient water management solutions.

United States: Federal Funding and Technological Innovation Driving Fracking Water Treatment Market Growth

The United States fracking water treatment market is the most advanced globally, driven by strict wastewater disposal and reuse regulations enforced by the EPA and state-level agencies. The Bipartisan Infrastructure Law (BIL) is a game-changer, channeling billions into water infrastructure upgrades, part of which supports fracking wastewater treatment and reuse systems.

On the infrastructure side, New Mexico’s $500 million water reuse plan (2024) highlights the shift toward large-scale investment in desalination and on-site treatment facilities. With shale plays such as the Permian Basin, Marcellus Shale, and Bakken Formation intensifying drilling, operators are prioritizing advanced, cost-effective water treatment technologies to offset rising freshwater sourcing and disposal costs. Emerging solutions include chemical-free treatments, mobile treatment units, and advanced membrane filtration systems, tailored for harsh shale conditions. These developments cement the U.S. as a hub for technological innovation in hydraulic fracturing wastewater management.

China: Shale Gas Expansion and Stricter Environmental Policies Boosting Wastewater Treatment Solutions

The China fracking water treatment market is growing rapidly due to the country’s massive shale gas reserves (over 15% of the global total) and the government’s aggressive push for energy security. Stricter environmental protection laws now require advanced treatment for high-salinity and chemically contaminated wastewater streams, creating strong demand for innovative, sustainable water management technologies.

China’s regulatory frameworks are evolving to balance energy expansion and ecological safeguards, opening opportunities for technology providers in high-salinity wastewater treatment, desalination, and brine recycling systems. The country is also investing in domestically developed fracking water treatment technologies with a focus on circular economy principles, including water reuse and resource recovery. With Asia Pacific forecasted to be the fastest-growing region for fracking wastewater treatment, China remains at the epicenter of HPHT (high-pressure, high-temperature) applications and unconventional oil and gas development.

Canada: Regulatory Frameworks and R&D Driving Advanced Wastewater Treatment Adoption

The Canada fracking water treatment market is supported by strong government and academic collaboration. For example, Natural Resources Canada is funding a project with the University of Alberta to address knowledge gaps around non-recovered fracturing water and salt production during shale operations. This research is key to minimizing environmental impact and optimizing treatment practices.

Canadian provinces such as Alberta and British Columbia enforce well-defined regulations for oil and gas wastewater management, requiring operators to adopt efficient produced water treatment systems. With the country’s growing reliance on shale gas and tight oil production, operators face increasing pressure to manage high volumes of saline water using membrane technologies, evaporation systems, and other advanced methods. The market is primarily driven by the need for environmentally compliant treatment solutions that support Canada’s long-term hydrocarbon production strategy.

Australia: Water Scarcity and Environmental Regulations Accelerating Wastewater Recycling in Fracking

The Australia fracking water treatment market is strongly influenced by Western Australia’s water sustainability policies, designed to manage water resources for both present and future generations. The Department of Water and Environmental Regulation (DWER) rigorously evaluates water allocation for petroleum projects, considering ecological sustainability and cumulative impacts.

Australia enforces strict restrictions on hydraulic fracturing activities, including a 2,000-meter exclusion zone from Public Drinking Water Source Areas and mandatory Environmental Protection Authority (EPA) assessments for new fracking projects. Given Australia’s arid climate and water-scarce environments, treatment companies are focusing on recycling, reuse, and advanced membrane technologies. The key driver in this market is the growing demand for innovative water purification systems capable of handling wastewater from shale gas and tight oil exploration while ensuring regulatory compliance and ecological protection.

United Kingdom: Regulatory Mandates and Corporate Innovation Supporting Fracking Wastewater Treatment

The United Kingdom fracking water treatment market is shaped by strict offshore oil and gas regulations, particularly in the North Sea region. The UK’s Asset Management Period (AMP) 8 program mandates the installation of new wastewater management infrastructure to mitigate environmental risks, reinforcing demand for advanced, high-purity water treatment systems in fracking operations.

Corporate innovation is also playing a major role. In 2024, Siemens launched its Water Quality Analytics as a Service (WQAaaS) for UK water utilities, offering real-time water quality data and predictive insights. These solutions enhance monitoring and treatment efficiency for both onshore fracking projects and mature offshore fields. With mature field developments increasingly relying on enhanced oil recovery (EOR) techniques, advanced fracking wastewater treatment technologies are essential to maintain reservoir pressure and improve hydrocarbon yields.

Russia: Produced Water Treatment Driving Demand for Advanced Fracking Wastewater Solutions

The Russia fracking water treatment market benefits from the country’s position as a leading global oil and gas producer, with continuous investments in exploration and production activities. However, large-scale extraction generates massive volumes of produced water, contaminated with high salinity, hydrocarbons, and heavy metals. This makes advanced produced water treatment systems a necessity.

Russian oilfield operators are increasingly deploying new treatment technologies designed for high-contaminant wastewater streams, including biological treatments, advanced oxidation processes, and desalination solutions. The key application driver remains the need for efficient water management solutions that can sustain production in unconventional oil and gas reserves while minimizing ecological risks. As Russia scales up production, the demand for cost-effective, high-performance fracking water treatment systems is expected to grow steadily.

Competitive Landscape of Fracking Water Treatment Market

The fracking water treatment market is highly competitive, with leading companies leveraging technology, mobility, and integrated solutions to address freshwater scarcity and regulatory compliance challenges. Market players differentiate themselves through modular systems, AI-driven analytics, and advanced treatment technologies that optimize water reuse and operational efficiency.

Schlumberger Limited (SLB) leads integrated water management solutions

SLB provides a comprehensive suite of water management services, including sourcing, transfer, treatment, and recycling of fracking water. Through its M-I SWACO division, SLB leverages digital tools for predictive maintenance and real-time monitoring, reducing non-productive time (NPT) and improving efficiency. In April 2024, SLB’s acquisition of ChampionX enhanced its chemical and monitoring service capabilities, solidifying its position in integrated fracking water solutions.

Halliburton Company delivers customized water treatment solutions

Halliburton offers mobile and modular water treatment technologies, including advanced filtration, chemical treatment, and desalination, tailored to complex produced water compositions. In 2024, the company focused on solutions for the Permian Basin, helping operators reduce disposal costs and improve water reuse. Halliburton’s strategic emphasis on sustainability supports reduced freshwater consumption and efficient water recycling.

Veolia Water Technologies pioneers AI-enabled mobile water fleets

Veolia provides mobile, on-demand water treatment solutions using technologies like reverse osmosis and media filtration. Its Drop® technology, launched in June 2025, addresses emerging contaminants such as PFAS, demonstrating Veolia’s capability to develop specialized treatment solutions for fracking water. The Hubgrade platform further enhances operational efficiency through AI-driven performance optimization.

Xylem Inc. integrates digital analytics in fracking water solutions

Xylem delivers a broad range of fracking water solutions, including mobile pumping and dewatering systems and advanced treatment technologies. Its Xylem Vue platform provides real-time analytics for monitoring and optimizing water operations. The December 2024 acquisition of Idrica strengthened Xylem’s digital capabilities, enabling end-to-end management of fracking water from transfer to final treatment and reuse.

DuPont de Nemours, Inc. specializes in membrane-based water purification

DuPont offers reverse osmosis (RO) and nanofiltration (NF) membranes designed to handle high-salinity and chemically complex fracking wastewater. The company’s 2024 innovations include durable, fouling-resistant membranes that enhance water reuse and meet stringent environmental regulations. DuPont focuses on high-efficiency solutions to reduce environmental impact and improve water treatment performance.

Fracking Water Treatment Market Report Scope

Fracking Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$503.4 Million

|

|

Market Size (2034)

|

$822 Million

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Service & Equipment (Treatment Equipment, Services), By Source Water Type (Flowback Water, Produced Water, Freshwater / Makeup Water), By Application (Reuse/Recycling, Disposal, Treatment for Discharge), By Well Type (Horizontal Wells, Vertical Wells), By Location (Onshore, Offshore)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Schlumberger Limited, Halliburton, Baker Hughes Company, Veolia, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Aquatech International, Ovivo Inc., SUEZ, Ecolab Inc., Newpark Resources, Inc., Siemens, Kurita Water Industries Ltd., VA Tech Wabag Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fracking Water Treatment Market Segmentation

By Service & Equipment

- Treatment Equipment

- Services

- Media Filtration

- Reverse Osmosis

- Others

By Source Water Type

- Flowback Water

- Produced Water

- Freshwater / Makeup Water

By Application

- Reuse/Recycling

- Disposal

- Treatment for Discharge

By Well Type

- Horizontal Wells

- Vertical Wells

By Location

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Fracking Water Treatment Industry include-

- Schlumberger Limited

- Halliburton

- Baker Hughes Company

- Veolia

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Aquatech International

- Ovivo Inc.

- SUEZ

- Ecolab Inc.

- Newpark Resources, Inc.

- Siemens

- Kurita Water Industries Ltd.

- VA Tech Wabag Ltd.

*- List not Exhaustive

Research Coverage

The Fracking Water Treatment Market Report by USDAnalytics this report investigates how modular, mobile, and AI-enabled treatment trains are reshaping flowback/produced-water reuse, it highlights breakthroughs in electrocoagulation–DAF hybrids, high-recovery membranes, and automated brine management; delivers analysis reviews on real-time compliance, PFAS-readiness, and OpEx service models; and maps region-specific playbooks for shale basins and arid geographies. By linking treatment choices to costs, logistics, and emissions outcomes, this report is an essential resource for E&P leaders, water midstream operators, and ESG teams seeking to reduce freshwater draw, curb disposal volumes, and scale closed-loop recycling across horizontal drilling programs. Scope Includes-

- Segmentation: By service & equipment (equipment; services; media filtration; RO; others), source water type (flowback; produced; freshwater/makeup), application (reuse/recycling; disposal; discharge), well type (horizontal; vertical), and location (onshore; offshore).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Schlumberger Limited; Halliburton; Baker Hughes Company; Veolia; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Aquatech International; Ovivo Inc.; SUEZ; Ecolab Inc.; Newpark Resources, Inc.; Siemens; Kurita Water Industries Ltd.; VA Tech Wabag Ltd.

Methodology

USDAnalytics integrates primary interviews with E&P water managers, midstream water operators, and technology vendors across major shale plays with secondary validation from permits, UIC/disposal filings, procurement tenders, academic trials, and vendor performance sheets. We build bottom-up water balance models (per-well flowback curves, produced-water yields, TDS/TOC ranges) and align them with top-down rig counts, lateral lengths, and completion intensity. Forecasts (2025–2034) incorporate basin-specific reuse targets, trucking vs. pipeline mix, disposal pricing, power/chemicals indices, and regulatory timelines. Competitive benchmarking scores solutions on recovery %, specific energy (kWh/m³), chemical intensity, mobility footprint, and SLA structures to deliver decision-grade sizing and share.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Fracking Water Treatment Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Fracking Water Treatment Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $503.4 Billion

2.2.2. Forecasted Market Size (2034): $822 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 5.6%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Freshwater Scarcity and Regulatory Mandates

2.3.2. Challenges: High Capital Costs and Operational Complexity

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Regulatory Compliance and Real-Time Monitoring

3.2. AI and Machine Learning for Predictive Operations

3.3. Water Reuse and Circular Economy Strategies

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Acquisitions and Partnerships

3.4.2. Technology Innovations and Research Initiatives

4. Fracking Water Treatment Market – Segmentation Insights

4.1. By Service & Equipment

4.1.1. Treatment Equipment (58.5% Market Share)

4.1.2. Services (44.1% Market Share)

4.1.3. Specific Technologies (Media Filtration, Reverse Osmosis, etc.)

4.2. By Source Water Type

4.2.1. Produced Water (54.2% Market Share)

4.2.2. Flowback Water (32.8% Market Share)

4.2.3. Freshwater / Makeup Water (11.8% Market Share)

4.3. By Application

4.3.1. Reuse/Recycling (54.2% Market Share)

4.3.2. Disposal (32.8% Market Share)

4.3.3. Treatment for Discharge (11.8% Market Share)

4.4. By Well Type

4.4.1. Horizontal Wells (90-95% Market Share)

4.4.2. Vertical Wells

4.5. By Location

4.5.1. Onshore

4.5.2. Offshore

5. Country Analysis and Outlook: Fracking Water Treatment Market

5.1. United States: Federal Funding and Technological Innovation

5.2. China: Shale Gas Expansion and Environmental Policies

5.3. Canada: Regulatory Frameworks and R&D

5.4. Australia: Water Scarcity and Environmental Regulations

5.5. United Kingdom: Regulatory Mandates and Corporate Innovation

5.6. Russia: Produced Water Treatment Driving Demand

6. Fracking Water Treatment Market Size Outlook by Region (2025–2034)

6.1. North America Fracking Water Treatment Market Size Outlook to 2034

6.1.1. By Service & Equipment

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Fracking Water Treatment Market Size Outlook to 2034

6.2.1. By Service & Equipment

6.2.2. By Application

6.2.3. By Country (UK, Germany, Russia, Rest of Europe)

6.3. Asia Pacific Fracking Water Treatment Market Size Outlook to 2034

6.3.1. By Service & Equipment

6.3.2. By Application

6.3.3. By Country (China, India, Australia, Rest of Asia)

6.4. South America Fracking Water Treatment Market Size Outlook to 2034

6.4.1. By Service & Equipment

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Fracking Water Treatment Market Size Outlook to 2034

6.5.1. By Service & Equipment

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Schlumberger Limited (SLB)

7.1.1. Company Overview

7.1.2. Integrated Water Management Solutions

7.2. Halliburton Company

7.2.1. Company Overview

7.2.2. Customized Water Treatment Solutions

7.3. Veolia Water Technologies

7.4. Xylem Inc.

7.5. DuPont de Nemours, Inc.

7.6. Other Prominent Companies

7.6.1. Baker Hughes Company

7.6.2. Evoqua Water Technologies

7.6.3. Aquatech International

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures