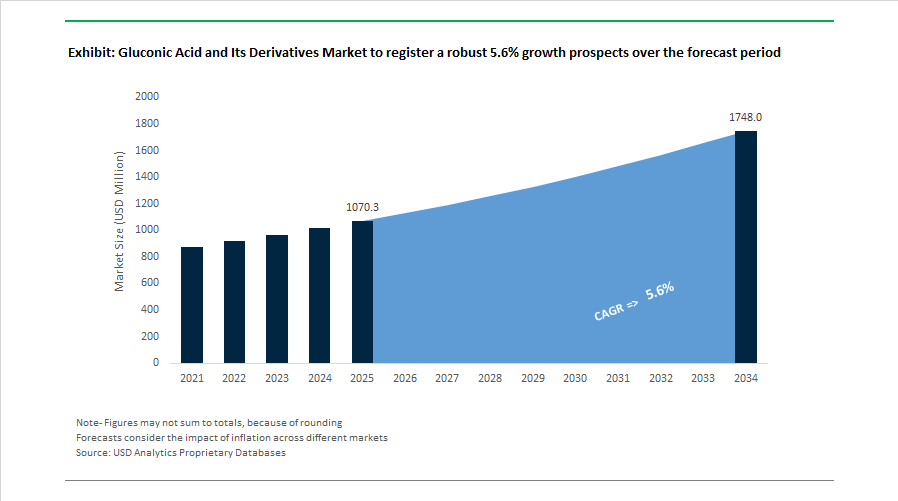

Gluconic Acid and Its Derivatives Market to Reach $1,747.8 Million by 2034 at 5.6% CAGR Driven by Fermentation Scale-Up, Construction Tech, and Pharmaceutical Purity Standards

The Gluconic Acid and Its Derivatives Market is projected to grow from $1,070.3 Million in 2025 to $1,747.8 Million by 2034, registering a CAGR of 5.6%. Market expansion is underpinned by rising demand for sodium gluconate in concrete admixtures, chelating agents in industrial cleaning, glucono-delta-lactone in food processing, and calcium and magnesium gluconates in pharmaceutical formulations. Fermentation-based production, bio-based corrosion inhibitors, and eco-friendly metal chelation technologies are reinforcing the strategic importance of gluconates across construction, healthcare, water treatment, and animal nutrition sectors.

In January 2024, a specialized pharmaceutical-grade producer commissioned a dedicated ultra-high-purity gluconic acid facility targeting injectable calcium and magnesium gluconates for chronic mineral deficiency management. In early 2024, European regulatory authorities expanded the approved use of gluconic acid and glucono-delta-lactone in food and beverage applications, prompting dairy and meat processors to reformulate products with cleaner-label pH regulators and mild acidulants. During 2024, Zhonglan Industry Co., Ltd. completed a significant production expansion to stabilize technical-grade sodium gluconate supply for Asia-Pacific construction and textile industries. In parallel, PMP Fermentation Products optimized its NAGLUSOL liquid sodium gluconate solutions, enhancing alkaline stability for industrial bottle washing and metal degreasing applications. A landmark 2024 healthcare study further validated gluconic acid-based cleaning systems as effective bio-based alternatives for mineral scale and biofilm removal in medical instrument sterilization.

Application innovation accelerated through 2025. In 2025, construction technology firms incorporated specialized sodium gluconate formulations as set-retarders in 3D concrete printing, enabling precise control over mixture open time for complex high-rise structures. Sustainable chemistry startups partnered with Archer Daniels Midland to introduce hybrid glucaric-gluconic acid corrosion inhibitor systems marketed as fully biodegradable solutions for municipal water treatment and industrial cooling towers. Trade policy shifts in the United States during 2025 prompted companies such as Cargill Incorporated to realign sourcing strategies toward domestic sodium gluconate production, mitigating cost volatility linked to imports.

In October 2025, Roquette Frères released collaborative research with European universities demonstrating that gluconic acid supplementation stimulates endogenous butyrate production in piglets, enhancing intestinal health and growth performance in animal nutrition programs. In January 2026, a consortium of European producers launched a blockchain-based traceability pilot for sodium gluconate, allowing verification of glucose feedstock origin and fermentation carbon footprint in compliance with new EU sustainability reporting requirements. In February 2026, Henkel AG & Co. KGaA completed its $2.5 billion acquisition of Stahl Holdings B.V., integrating high-performance coating chemistries that utilize gluconates as eco-friendly chelating agents in metal-free leather processing.

Portfolio expansion also strengthened multifunctional ingredient systems. In late 2024, Jungbunzlauer Suisse AG launched TayaGel® Modus within its texturant portfolio, aligning fermentation-derived acids and gluconates with plant-based dairy and meat alternatives.

The Gluconic Acid and Its Derivatives Market outlook reflects fermentation capacity expansion, pharmaceutical purity upgrades, 3D-printed concrete innovation, biodegradable corrosion inhibitor systems, trade-driven sourcing localization, and blockchain-enabled supply transparency. Competitive differentiation increasingly centers on high-purity grades, alkaline stability performance, sustainable glucose feedstock integration, regulatory-compliant food applications, and multifunctional ingredient system development across construction, healthcare, water treatment, and animal nutrition industries.

Gluconic Acid and Its Derivatives Market Trends and Strategic Growth Opportunities

Green Chelation Is Driving Structural Replacement of Legacy Complexing Agents

The global gluconic acid and sodium gluconate market is undergoing a structural demand shift as regulators and industrial buyers move away from persistent synthetic chelants such as EDTA and NTA. These legacy agents are increasingly scrutinized for poor biodegradability and their ability to remobilize heavy metals in aquatic ecosystems, creating long-term environmental risk. In June 2025, the European Council and Parliament reached a provisional agreement to update the Regulation on Detergents and Surfactants, granting the European Commission authority to enforce stricter biodegradability thresholds for organic substances used above defined concentration levels. This regulatory direction directly favors sodium gluconate, which is already recognized under the EPA Safer Choice Program as a non-toxic and readily biodegradable chelating agent.

From a performance standpoint, sodium gluconate has proven industrial maturity in alkaline cleaning environments. In food and beverage bottle washing and clean-in-place systems operating at high pH, sodium gluconate demonstrates exceptional calcium sequestration capacity. Industrial data from 2024 and 2025 indicate that in one percent sodium hydroxide solutions, sodium gluconate can bind up to 100 milligrams of calcium oxide per gram, effectively preventing scale formation without leaving persistent residues. This combination of regulatory alignment and functional superiority is reinforcing its adoption across industrial cleaning, corrosion control, and water treatment. Pricing trends further confirm market stability, with sodium gluconate prices reaching approximately 960 dollars per metric ton in the United States and 765 dollars per metric ton in India by September 2025, reflecting resilient demand for bio-based chelants despite cautious downstream procurement cycles.

Precision Fermentation and High-Purity Grades Reshape Pharma Positioning

Alongside industrial applications, the gluconic acid market is clearly bifurcating into bulk technical grades and ultra-high-purity, low-pyrogen grades designed for pharmaceutical and medical nutrition use. Precision fermentation is central to this transition. By November 2025, the global precision fermentation sector had scaled into a multi-billion-dollar industry, enabling gluconic acid producers to deploy genetically optimized strains such as Gluconobacter oxydans that deliver higher yields and cleaner downstream purification. This technological shift is critical for producing USP and Ph. Eur. compliant calcium and zinc gluconates with high solubility and neutral taste, properties that make them ideal excipients for effervescent tablets and liquid supplements.

Strategic portfolio repositioning by leading producers underscores this trend. During 2024 and 2025, Roquette intensified its focus on gluconic acid derivatives for human and animal nutrition, highlighting their role in short-chain fatty acid pathways and digestive health. This purity-driven strategy allows suppliers to serve pharmaceutical customers with stringent quality expectations while capturing higher margins. As a result, pharmaceutical and nutrition-grade gluconates are emerging as the fastest-growing application segment through the end of the decade, supported by regulatory acceptance and strong clinical utility.

Sustainable Concrete Admixtures Supporting Low-Carbon Construction

The global push toward net-zero construction and low-carbon cement formulations is creating a significant opportunity for sodium gluconate as a performance-critical concrete admixture. In modern infrastructure projects, especially those using self-consolidating concrete and supplementary cementitious materials, precise control over setting time and workability is essential. Research updated in early 2025 confirms that adding just 0.1% gluconic acid by weight of cement can extend concrete workability by up to 150 minutes, a critical advantage for mass pours and high-temperature construction environments.

Sodium gluconate also exhibits strong synergy with polycarboxylate ether superplasticizers. Technical disclosures in May 2025 from producers such as Arshine Lifescience demonstrated that gluconate-enhanced systems improve cement particle dispersion, enabling up to a 50% reduction in the water-to-cement ratio when combined with PCEs. This directly supports the adoption of low-carbon binders and reduced clinker content. Unlike chloride-based accelerators, gluconate-based retarders are non-corrosive, reducing porosity and extending the service life of steel-reinforced structures. These attributes position sodium gluconate as a dual-benefit additive that improves durability while aligning with sustainability mandates.

Mineral Fortification and Bioavailability Across Food, Feed, and Pharma

Gluconic acid’s ability to form stable, highly soluble mineral chelates underpins a broad opportunity across nutrition and healthcare markets. In August 2025, the World Health Organization highlighted that more than 30% of women of reproductive age globally suffer from anemia, accelerating government-led iron fortification initiatives. Ferrous gluconate is increasingly preferred in these programs due to its superior taste profile and gastrointestinal tolerance compared with sulfate or metallic iron salts.

Demand for zinc and calcium gluconates is also expanding rapidly. Zinc gluconate is seeing strong uptake in immunity-focused supplements, while calcium gluconate is becoming a standard fortification ingredient in dairy products, infant formula, and clinical nutrition due to its high solubility and neutral sensory impact. Beyond human health, precision livestock nutrition represents a high-growth niche. Calcium gluconate is widely used in transition diets for dairy cows to prevent milk fever, a metabolic disorder that significantly impacts productivity in high-yield herds. These applications collectively position gluconic acid and its derivatives as essential, multifunctional ingredients at the intersection of public health, sustainable agriculture, and regulated nutrition markets.

Gluconic Acid and Its Derivatives Market Share and Segmentation Insights

Sodium Gluconate Leads the Gluconic Acid and Its Derivatives Market Due to Multi-Industry Chelating Applications

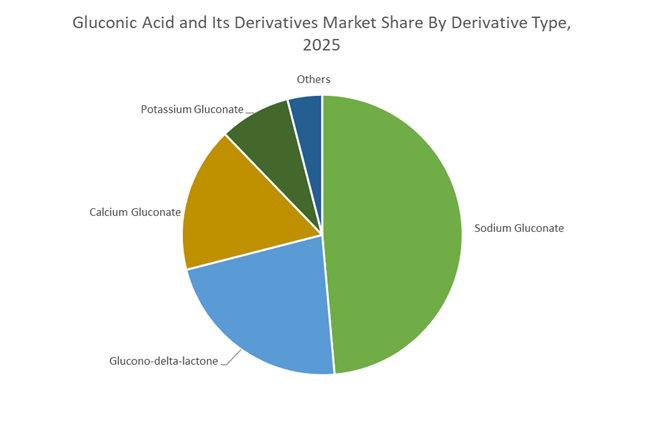

Sodium Gluconate accounted for 48.60% of the Gluconic Acid and Its Derivatives Market share in 2025, making it the most widely used derivative within the gluconate chemical family. Sodium gluconate is highly valued for its excellent chelating ability, biodegradability, and cost-effective production, enabling its use across diverse industrial sectors including industrial cleaning, construction chemicals, food processing, and water treatment. In detergent and cleaning formulations, it functions as a sequestrant that binds metal ions such as calcium and iron, preventing interference with surfactant performance. In construction applications, sodium gluconate acts as an effective concrete retarder and plasticizer, helping regulate cement hydration and improve workability in complex concrete placements. In 2025, the sodium gluconate segment is experiencing strong demand growth driven by the global transition toward phosphate-free chelating systems. Environmental regulations restricting phosphate use in cleaning formulations have accelerated adoption of biodegradable gluconate-based chelants, positioning sodium gluconate as a preferred alternative to traditional phosphates and phosphonates in environmentally compliant formulations.

Construction Industry Drives the Largest Demand for Gluconic Acid Derivatives in Concrete Admixtures

Construction represented 34.80% of the Gluconic Acid and Its Derivatives Market share in 2025, making it the largest application segment for gluconate-based chemical additives. Sodium gluconate plays a critical role in cement and concrete admixture formulations, where it functions as a set retarder that slows cement hydration and improves concrete workability during placement. These properties are particularly valuable in large infrastructure projects, high-temperature construction environments, and complex concrete pours, where extended working time is required to ensure proper placement and finishing. Global construction activity and large-scale infrastructure development continue to drive consistent demand for concrete admixtures containing gluconate derivatives. In 2025, the sector is increasingly focused on the development of high-performance concrete formulations designed to deliver improved durability, strength, and long service life. Gluconate-based admixtures are being incorporated into multi-component admixture systems that precisely control hydration kinetics, supporting advanced construction techniques such as self-consolidating concrete, high-rise pumpable concrete mixes, and large-scale structural pours in extreme weather conditions.

Competitive Landscape in Gluconic Acid and Its Derivatives Market

Roquette Frères Leads High-Purity Gluconic Acid for Pharma and Biostimulants

Roquette Frères maintains a dominant position in plant-based gluconic acid production, particularly within pharmaceutical-grade and life sciences applications. In October 2025, the company introduced a new liquid gluconic acid application in piglet nutrition, demonstrating improved intestinal villous height and endogenous butyrate stimulation as a natural growth promoter. Its GLUCONIC ACID TECHNICAL 50/50 portfolio is widely used as a non-volatile, fully water-soluble complexing agent in biostimulants, fertilizers, and industrial cleaning formulations. In February 2026, Roquette joined the Ferments du Futur consortium to accelerate development of fermented bio-based chelating agents that replace petroleum-derived chemicals. The company is advancing ISO 14001 certification across all sites, reinforcing circular starch-to-acid refinery integration and environmental compliance.

Jungbunzlauer Expands Specialty Mineral Gluconates with Low-Carbon Production

Jungbunzlauer Suisse AG is one of the largest global producers of fermentation-derived gluconates, supported by extensive vertical integration and carbon-neutral manufacturing ambitions. Its Phase 1 expansion in Port Colborne, Canada, operational by Spring 2026, strengthens corn-wet milling infrastructure that supports specialty salts and gluconate production. The company focuses on high-bioavailability mineral gluconates including zinc, magnesium, and calcium salts for global nutraceutical fortification markets. Sustainability upgrades incorporating electrical evaporation and heat pump systems have reduced natural gas dependency in acidification processes. In 2026, Jungbunzlauer is leveraging digital sales optimization to serve fragmented personal care and detergent markets with precision inventory and demand forecasting tools.

Fuso Chemical Strengthens Glucono-Delta-Lactone and Electronics Applications

Fuso Chemical Co., Ltd. remains a top global supplier of glucono-delta-lactone, widely used as a non-GMO acidulant and protein coagulant in tofu and dairy processing. The company is recognized among the top five global players in the gluconolactone segment due to its established distribution networks in North America and Southeast Asia. In 2026, Fuso expanded into electronic materials applications, utilizing the high chelating precision of gluconic acid derivatives for semiconductor cleaning and rust-proofing formulations. Late 2025 enzymatic conversion optimizations increased yields of malic and gluconic acid derivatives at its Osaka production facility while reducing environmental impact. Its integration of high-purity fermentation technology supports advanced food and life science markets across Asia-Pacific.

ADM Leverages Vertical Integration for Industrial and Functional Gluconates

Archer Daniels Midland Company utilizes its global agricultural origination network to provide cost-competitive sodium gluconate and specialty gluconic acid derivatives. Sodium gluconate remains a key product for concrete retarders and industrial cleaning formulations, particularly in infrastructure and construction sectors. In February 2026, ADM’s Global Culinary Trends Report identified Authentic Wellbeing as a growth driver, positioning gluconates as functional snack ingredients supporting longevity and mental resilience. The company is also investigating gluconic acid-containing oligosaccharides as precision prebiotics targeting beneficial gut bacteria such as Faecalibacterium prausnitzii. Full traceability of soybean and corn derivatives introduced to the European market aligns with EUDR requirements effective December 2025 and 2026.

Corbion Integrates Gluconates into Clinical Nutrition and Biomedical Systems

Corbion N.V. focuses on high-end mineral gluconates and co-formulated bio-acid systems under its GLUCONAL® brand. These calcium, magnesium, and ferrous gluconates are engineered for superior solubility and neutral taste in fortified beverages and clinical nutrition products. In 2026, Corbion emphasized synergy between PURAC® lactic acid and GLUCONAL® gluconates to enhance mineral absorption while preserving shelf stability in clean-label yogurt and dairy alternatives. The company is extending gluconic acid derivatives into controlled-release drug delivery systems, leveraging decades of polymer science expertise. Operating under its Preserve What is Good framework, Corbion utilizes renewable energy across a significant portion of its European manufacturing footprint, strengthening sustainability credentials in the bio-based acids sector.

United States: Domestic Bio-Manufacturing Scale-Up and Regulatory-Driven Substitution

The United States gluconic acid and derivatives industry is undergoing a structural shift toward domestic capacity expansion, bio-manufacturing innovation, and regulatory-aligned product substitution. In December 2025, PMP Fermentation Products, a subsidiary of Fuso Chemical, committed USD 7.1 million to expand its Illinois facility through the installation of a new crystallizer and auxiliary processing equipment. Scheduled for completion by 2027, this project will lift sodium gluconate and derivative output by approximately 30%, directly addressing rising demand from construction admixtures and fertilizer formulations where gluconates function as chelating and dispersion agents. Parallel to capacity expansion, tariff-driven cost pressures introduced in early 2025 have raised landed costs for imported gluconates by an estimated 6 to 10%, accelerating onshoring decisions across the U.S. specialty chemical value chain.

Innovation-led decarbonization is reinforcing this shift. Solugen, in partnership with ADM, is scaling its USD 90 million bio-manufacturing hub in Marshall, Minnesota, utilizing corn dextrose feedstock in a proprietary chemo-enzymatic pathway to produce gluconic acid at materially lower energy intensity than conventional fermentation. Regulatory dynamics are equally influential. EPA-led green chemistry initiatives are driving the replacement of persistent chelators such as EDTA with biodegradable gluconic acid derivatives in water treatment and household cleaning products, while the FDA’s March 2025 GRAS purity reform has imposed tighter heavy-metal testing protocols for high-purity gluconates used in infant formula and medical nutrition, favoring vertically integrated and quality-controlled domestic suppliers.

India: Pharmaceutical API Localization and Agro-Chemical Export Orientation

India’s gluconic acid market is being reshaped by policy-backed pharmaceutical localization, fermentation efficiency gains, and expanding agro-chemical exports. Under the Production Linked Incentive scheme effective from 2026, the government has earmarked USD 574.5 million to scale domestic API manufacturing, explicitly including calcium gluconate and ferrous gluconate as India positions itself to capture post-patent generic demand. This policy tailwind is complemented by process innovation. In late 2025, the CSIR achieved glucose conversion efficiencies above 95% using a continuous fermentation platform, materially improving the cost competitiveness of gluconic acid for regional agro-chemical and industrial applications.

Downstream demand diversification is further supporting capacity investments. The Ministry of Textiles incentivized sodium gluconate adoption in large dyeing clusters during 2025 as a leveling agent that ensures color uniformity while complying with Zero Discharge of Hazardous Chemicals standards. In parallel, private capital inflows into Gujarat’s chemical belt enabled the commissioning of three spray-drying units dedicated to zinc and magnesium gluconates for micronutrient fertilizer exports. Collectively, these developments are positioning India as a low-cost, high-volume supplier of both pharmaceutical-grade and agro-industrial gluconates with increasing export relevance.

China: Energy-Efficient Fermentation and Infrastructure-Linked Demand Growth

China remains a pivotal global supplier of gluconic acid, with competitiveness increasingly defined by energy efficiency, infrastructure-linked demand, and emerging battery applications. Under the MIIT 2025–2026 green processing mandate, gluconic acid producers are required to adopt Mechanical Vapor Recompression technology in crystallization units, targeting a 15% reduction in steam consumption. This regulatory push is accelerating capital upgrades across major fermentation hubs and reinforcing China’s scale advantage under tightening environmental constraints.

Capacity expansion is aligned with downstream construction demand. Zhonglan Industry completed a major facility expansion spanning late 2024 and early 2025, specifically designed to supply sodium gluconate for concrete admixtures used in Southeast Asia’s urban infrastructure projects. Beyond traditional uses, strategic R&D in Shandong has piloted gluconic acid derivatives as organic binders for sodium-ion battery cathodes, with commercial sampling initiated in January 2026. At the same time, exports of pharmaceutical-grade glucono-delta-lactone are rising, targeting European clean-label food manufacturers seeking non-GMO, corn-derived acidulants with transparent supply chains.

European Union: Clean-Label Food Fortification and Circular Recovery Models

Across the European Union, regulatory clarity and sustainability frameworks are reshaping gluconic acid demand in food, pharmaceuticals, and textiles. In November 2025, the EFSA updated its food additive guidance, approving wider concentration ranges of gluconates in vegan dairy alternatives. This decision has directly increased the use of calcium gluconate for mineral fortification in plant-based milk products across France and Germany, where clean-label positioning and mineral bioavailability are key differentiation factors.

Industrial players are reinforcing sustainability narratives through circularity. Roquette highlighted plant-derived gluconic acid as a substitute for synthetic chelants in pharmaceutical controlled-release systems at AAPS 2025, while Lenzing Group implemented a circular recovery pilot to extract organic acids and sodium sulfate from viscose byproduct streams and refine them into industrial-grade gluconate salts. These initiatives are strengthening the EU’s position as a demand center for traceable, low-impact gluconic acid derivatives rather than bulk commodity volumes.

Comparative Snapshot: Gluconic Acid and Derivatives by Region

Gluconic Acid and Its Derivatives Market County Level Snapshot

|

Region

|

Primary Demand Drivers

|

Strategic Industry Direction

|

|

United States

|

Construction admixtures, fertilizers, green cleaners

|

Onshoring, bio-manufacturing, regulatory substitution

|

|

India

|

APIs, textiles, micronutrient fertilizers

|

PLI-driven localization and export-oriented scale

|

|

China

|

Infrastructure concrete, food acidulants, batteries

|

Energy-efficient fermentation and capacity expansion

|

|

European Union

|

Plant-based foods, pharma, textiles

|

Clean-label approvals and circular recovery

|

Gluconic Acid and Its Derivatives Market Report Scope

Gluconic Acid and Its Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1070.3 Million

|

|

Market Size (2034)

|

$1747.8 Million

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Derivative Type (Sodium Gluconate, Glucono-delta-lactone, Calcium Gluconate, Potassium Gluconate, Other Gluconate Salts), By Grade (Pharmaceutical Grade, Food Grade, Industrial Grade), By Production Source (Microbial Fermentation, Chemo-Enzymatic Synthesis, Chemical Oxidation), By Application (Construction, Food and Beverages, Pharmaceuticals and Personal Care, Industrial Cleaning, Agriculture), By Physical Form (Crystalline Powder, Liquid Solution)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Roquette Frères, Jungbunzlauer Suisse AG, Archer Daniels Midland Company, PMP Fermentation Products, Corbion N.V., Zhonglan Industry Co., Ltd., Shandong Kaison Biochemical Co., Ltd., Xiwang Sugar Co., Ltd., Anhui Pulis Biological Technology Co., Ltd., Nagase & Co., Ltd., Prathista Industries Limited, Global Calcium Pvt. Ltd., Solugen, Inc., Givaudan, Akzo Nobel N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gluconic Acid and Its Derivatives Market Segmentation

By Derivative Type

- Sodium Gluconate

- Glucono-delta-lactone

- Calcium Gluconate

- Potassium Gluconate

- Other Gluconate Salts

By Grade

- Pharmaceutical Grade

- Food Grade

- Industrial Grade

By Production Source

- Microbial Fermentation

- Chemo-Enzymatic Synthesis

- Chemical Oxidation

By Application

- Construction

- Food and Beverages

- Pharmaceuticals and Personal Care

- Industrial Cleaning

- Agriculture

By Physical Form

- Crystalline Powder

- Liquid Solution

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Gluconic Acid and Its Derivatives Industry

- Roquette Frères

- Jungbunzlauer Suisse AG

- Archer Daniels Midland Company

- PMP Fermentation Products

- Corbion N.V.

- Zhonglan Industry Co., Ltd.

- Shandong Kaison Biochemical Co., Ltd.

- Xiwang Sugar Co., Ltd.

- Anhui Pulis Biological Technology Co., Ltd.

- Nagase & Co., Ltd.

- Prathista Industries Limited

- Global Calcium Pvt. Ltd.

- Solugen, Inc.

- Givaudan

- Akzo Nobel N.V.

*- List not Exhaustive