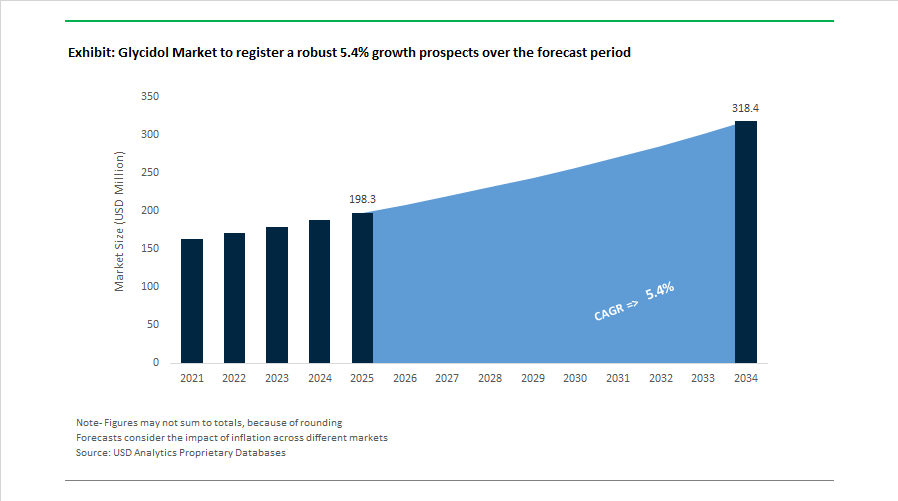

Glycidol Market to Reach $318.3 Million by 2034 at 5.4% CAGR Driven by API Expansion, Polymer Stabilization, and Regulatory Controls on Glycidyl Esters

The Glycidol Market is projected to grow from $198.3 Million in 2025 to $318.3 Million by 2034, registering a CAGR of 5.4%. Market expansion is supported by rising utilization of glycidol and glycidyl intermediates in active pharmaceutical ingredient synthesis, specialty resins, vinyl polymer stabilization, agrochemical formulations, and non-ionic surfactants for personal care. Increasing regulatory scrutiny on glycidyl ester contaminants in edible oils, coupled with demand for high-purity chiral intermediates such as (R)-glycidol, is reshaping production standards and supply chain traceability across pharmaceutical and food-grade segments.

In January 2024, AbbVie Inc. announced a $223 million expansion of its Singapore biologics and small-molecule manufacturing site, indirectly strengthening upstream demand for high-purity glycidol used in API synthesis. In May 2024, Asian Paints Polymers Pvt Ltd unveiled a greenfield vinyl polymers project in Gujarat valued at approximately INR 2,100 crore, reinforcing demand for glycidol-based stabilizers in VAM and VAE polymerization systems. In September 2024, India Glycols Limited reported progress on new specialty chemical projects enhancing glycol derivative capacity for pharmaceutical and detergent markets. In October 2024, BASF SE registered Liberty ULTRA herbicide, where glycidyl intermediates play a role in improving solubility and formulation stability of advanced agrochemical actives.

Regulatory developments intensified market realignment in 2025. As of January 1, 2025, the Eurasian Economic Union implemented mandatory standards limiting fatty acid glycidyl esters in edible fats and oils, compelling refiners to adopt advanced mitigation and purification technologies. During early 2025, manufacturers reported a surge in (R)-glycidol production to support enantiomerically pure cardiovascular and antiviral APIs requiring strict stereochemical control. In June 2025, Nagase & Co., Ltd. completed the acquisition of SACHEM’s semiconductor chemicals business in Asia, integrating high-purity intermediates relevant to electronics-grade glycidol derivatives used in specialty laminates and resin systems. Throughout 2025, construction technology pilots validated glycidol-modified surfactants as precision set-retarders in 3D-printed concrete, enabling controlled layer solidification for complex infrastructure applications.

Capacity expansion and digital integration progressed into 2026. Between 2024 and 2026, Evonik Industries AG expanded hydroxyl-terminated polybutadiene production at its Marl and Shanghai sites and advanced plans for a new Asian facility, supporting resin and adhesive systems that incorporate glycidol as a functionalizing agent. In 2025, leading beauty houses including L'Oréal S.A. and The Estée Lauder Companies Inc. partners increased adoption of glycidol-based non-ionic surfactants in clean beauty formulations due to improved mildness and biodegradability profiles. In January 2026, BASF established a global Digital Hub in Hyderabad to deploy AI-driven optimization for Care Chemicals supply chains, including quality tracking and distribution of pharmaceutical and cosmetic-grade glycidol.

The Glycidol Market outlook reflects regulatory tightening on glycidyl ester contaminants, pharmaceutical demand for chiral intermediates, polymer stabilization growth in Asia, electronics-grade specialty resin integration, agrochemical formulation innovation, and digitalized supply chain management. Competitive positioning increasingly depends on stereochemical purity, contaminant control compliance, high-purity production infrastructure, and application-specific derivative development across pharmaceuticals, food processing, construction materials, electronics, and personal care sectors.

Glycidol Market Trends and Strategic Growth Opportunities

Regulatory-Driven Portfolio Realignment and Capacity Consolidation

The global glycidol market is entering a phase of structural consolidation as regulatory scrutiny around glycidyl-related contaminants intensifies across food, pharmaceutical, and consumer product value chains. Stricter limits on glycidyl fatty acid esters are compelling producers to redesign manufacturing processes, invest in advanced purification, and rationalize legacy capacity. A major inflection point came with the enforcement of Commission Regulation (EU) 2024/1003 from January 2025, under which the European Commission sharply reduced permissible glycidyl ester levels in infant formula and medical nutrition. Powdered formulations are now capped at 80 micrograms per kilogram, forcing upstream glycidol suppliers to eliminate trace contaminants at the source rather than relying on downstream blending or dilution.

This regulatory tightening is accelerating capital reallocation toward compliant, value-added production. In early 2024, India Glycols Limited announced progress on capacity enhancement at its Kashipur complex, including new facilities dedicated to high-value chemical intermediates with an estimated output of 5,000 metric tons per year by the second quarter of fiscal year 2025. At the same time, portfolio streamlining is becoming common among multinational producers. BASF has divested non-core optical brightener assets and refocused its mid-2024 strategy on ISCC+ certified glycol ethers and acetates, underscoring a broader industry shift toward sustainable, tightly regulated chemical supply chains. Collectively, these moves are reducing commoditized output while strengthening pricing power for high-purity glycidol grades.

Rising Demand for Ultra-High-Purity Glycidol in Oncology and Biologics

The pharmaceutical sector is rapidly emerging as a key growth engine for the glycidol market, driven by the expansion of antibody-drug conjugates and other targeted oncology platforms. These therapies require ultra-high-purity glycidol, typically above 97%, to serve as a critical intermediate in linker synthesis and high-potency active pharmaceutical ingredient manufacturing. Glycidol derivatives are increasingly used to fine-tune drug-to-antibody ratios in chemically labile linkers, ensuring controlled release of cytotoxic payloads while preserving the structural integrity of complex biologic molecules.

Capital investment trends in biologics manufacturing are reinforcing this demand trajectory. In 2024, AbbVie announced a 223 million dollar expansion of its Singapore biologics facility, while Arrowhead Pharmaceuticals completed a 200 million dollar investment in a new Wisconsin manufacturing site designed for advanced drug delivery technologies. Parallel academic and preclinical research published during 2024 and 2025 has shown that polyglycidol-based carriers offer superior hemocompatibility and reduced protein adsorption compared with conventional polyethers. This evidence is positioning high-purity glycidol as a preferred building block not only for oncology drugs but also for next-generation biosensors and diagnostic platforms.

Low-VOC Industrial Coatings and High-Performance Crosslinkers

Environmental regulations targeting volatile organic compound emissions are creating a substantial opportunity for glycidol-derived monomers, particularly glycidyl methacrylate, in industrial coatings. Automotive, aerospace, and infrastructure sectors are increasingly adopting high-solid, low-VOC formulations that require reactive crosslinkers capable of maintaining performance at reduced solvent levels. Glycidol derivatives enable lower-viscosity systems without sacrificing adhesion or corrosion resistance, making them attractive substitutes for solvent-heavy chemistries.

Demand is especially pronounced in Asia-Pacific and the Middle East, where infrastructure expansion and harsh operating environments drive the need for durable protective coatings. Mitsubishi Gas Chemical has signaled increased output of functional chemicals at its Niigata facility to meet rising regional demand. In electronics and advanced materials, glycidol-based epoxide additives are being incorporated into thermal interface materials and conformal coatings. Strategic collaborations announced by Dow during 2024 and 2025 highlight the role of epoxide chemistry in protecting sensitive components under thermal and mechanical stress, further expanding the coatings and adhesives addressable market for glycidol derivatives.

Lithium-Ion Battery Binders and Electrolyte Stabilization

Electrification of transport represents a frontier growth opportunity for the glycidol market, as battery manufacturers seek sustainable alternatives to fluorinated binders and unstable electrolyte systems. Glycidol-based polymers are being actively researched as next-generation binders for lithium-ion battery electrodes, offering improved ionic conductivity and mechanical resilience. Materials science studies published in August 2025 demonstrated that cross-linked glycidol-derived binder networks achieved nearly 95% capacity retention after 400 charge-discharge cycles at one C, materially outperforming conventional polyvinylidene fluoride benchmarks.

Beyond binders, glycidol’s reactive epoxide functionality is being leveraged to design electrolyte additives that scavenge free radicals and suppress degradation pathways. These additives have shown the ability to stabilize high-energy-density cells over more than 500 cycles, directly addressing durability concerns in electric vehicle batteries. As the global lithium-ion battery binder segment scales toward an estimated value approaching 14 billion dollars by the mid-2030s, demand for aqueous, low-toxicity, and high-performance materials is accelerating. In this context, glycidol-derived polymers are well positioned as a sustainable solution aligned with both performance requirements and decarbonization goals of the electric mobility ecosystem.

Glycidol Market Share and Segmentation Insights

Industrial Grade Glycidol Leads Production of Chemical Intermediates in the Glycidol Market

Industrial Grade accounted for 48.60% of the Glycidol Market share in 2025, making it the most widely used grade across global glycidol manufacturing and downstream chemical synthesis. Industrial grade glycidol is primarily utilized in large-scale chemical processing applications, where it serves as a reactive epoxide intermediate for producing glycerol derivatives, glycidyl ethers, esters, and other specialty organic compounds. These intermediates are essential for manufacturing surfactants, resins, coatings, polymer additives, and industrial specialty chemicals used across multiple industrial sectors. The grade’s dominance is supported by its cost efficiency and suitability for high-volume production processes, where ultra-high purity is not required. In 2025, a major structural advantage in this segment is the high level of captive consumption within integrated chemical manufacturing facilities. Large producers frequently manufacture glycidol internally and use it directly in downstream derivative production, reducing reliance on merchant market supply. This integrated production model stabilizes demand and allows manufacturers to optimize feedstock utilization, production efficiency, and derivative product economics across the glycidol value chain.

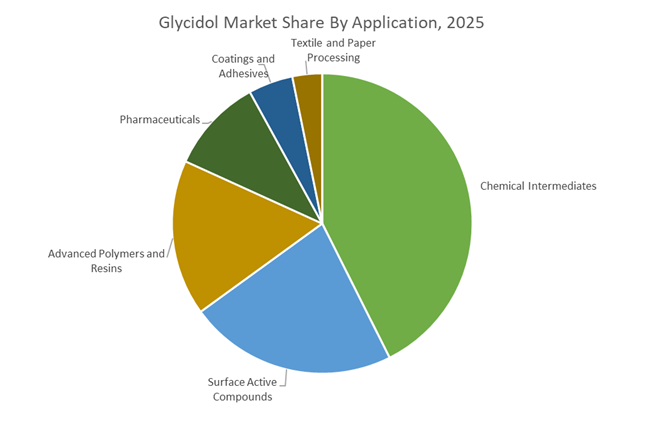

Chemical Intermediate Applications Drive the Largest Demand for Glycidol Derivatives

Chemical Intermediates represented 42.60% of the Glycidol Market share in 2025, making it the largest application segment for glycidol-based chemical production. Glycidol is valued for its reactive epoxide functionality and hydroxyl group, enabling it to serve as a versatile building block in the synthesis of glycerol, glycidyl ethers, esters, amines, and other functional chemical intermediates. These compounds are further processed into surfactants, epoxy resins, polymer additives, coatings ingredients, and specialty industrial chemicals used across sectors including construction materials, consumer products, and industrial manufacturing. In 2025, growing interest in bio-based chemical production is creating new opportunities for glycidol derivatives. Glycidol can be produced from renewable glycerol generated as a byproduct of biodiesel production, enabling the development of bio-based chemical intermediates that meet sustainability targets in downstream industries. These renewable derivatives are gaining traction in cosmetics, personal care formulations, and specialty polymers, where manufacturers increasingly seek bio-based content and reduced carbon footprints, supporting premium positioning in environmentally conscious product markets.

Competitive Landscape in Glycidol Market

Evonik Industries AG Drives Specialty Epoxide Innovation

Evonik Industries AG positions glycidol within its Smart Materials segment, emphasizing high-margin specialty epoxides and low-VOC resin systems. Under its Next Markets program, the company is pivoting toward bio-based intermediates that enhance durability in coatings and performance additives. In early 2026, Evonik confirmed adjusted EBITDA of €1.874 billion for 2025 and is streamlining its Marl and Wesseling Verbund sites to optimize specialty epoxide production. Its glycidol derivatives serve as reactive diluents and stabilizers for vinyl resins, targeting industrial coatings with reduced volatile organic compound emissions. A significant portion of its glycidol-related production now operates on 100% renewable electricity, reinforcing sustainability credentials in regulated European markets.

Mitsubishi Chemical Group Expands Chiral and Electronics-Grade Glycidol

Mitsubishi Chemical Group Corporation is scaling glycidol-based specialty materials under its Grow UP 2026 plan, prioritizing high-value semiconductor and advanced film applications. Its Specialty Materials segment reported a ¥11.8 billion year-over-year core operating income increase in late 2025, supported by semiconductor demand. The company is concentrating resources on glycidol-modified polymers and optically active R-glycidol and S-glycidol, critical for chiral pharmaceutical synthesis and liquid crystal materials. In February 2026, Mitsubishi announced the transfer of its synthetic resin emulsion business to focus capital on higher-margin chemical intermediates. This repositioning strengthens its role in high-purity glycidol supply for electronics and life sciences sectors across Asia-Pacific.

FUJIFILM Wako Sets Benchmark for Ultra-Pure Research-Grade Glycidol

FUJIFILM Wako Pure Chemical Corporation operates as a premium supplier of laboratory and clinical-grade glycidol, serving semiconductor, pharmaceutical, and analytical markets. Its 2026 strategy emphasizes trace metal management at single-digit parts-per-billion levels to meet stringent fabrication and GMP standards. The company supplies 97%or higher purity glycidol along with glycidol fatty acid ester analytical standards for global food safety and lipid research laboratories. In early 2026, Wako expanded into glycidol-derived azo polymerization initiators for high-performance paints and hygiene products. As part of Fujifilm’s Healthcare and Highly Functional Materials division, it benefits from sustained R&D investment growth across biotech and advanced materials sectors.

Nagase & Co. Accelerates Semiconductor-Focused Epoxide Manufacturing

Nagase & Co., Ltd. is expanding its specialty epoxide footprint through integration of SACHEM Asia under the Nagase Circrea brand. This 2026 initiative strengthens its position in semiconductor-grade glycidol derivatives and high-purity cross-linking agents. Under its ACE 2.0 plan, Nagase is shifting its revenue composition toward higher-margin manufacturing activities, reducing reliance on legacy trading operations. Targeting consolidated net sales above ¥1 trillion in 2026, the company is investing in new semiconductor materials production lines. Its glycidol-based resin modifiers enhance thermal stability and mechanical reliability in automotive electronics and advanced composite applications.

Merck KGaA Supports Precision Medicine and GMP-Compliant Supply Chains

Merck KGaA, through its Life Science division, supplies glycidol and glycidyl ether intermediates to pharmaceutical manufacturers and clinical research laboratories worldwide. In 2026, the company is integrating digital Certificate of Analysis platforms into its glycidol supply chain to ensure full GMP compliance and real-time traceability. Its catalog includes glycidyl butyrate and specialized glycidyl ethers used in drug delivery systems and precision medicine synthesis. Merck’s Life Science 2030 roadmap emphasizes green chemistry approaches to reduce environmental impact associated with epoxide production. With a strong global distribution network, Merck remains a key supplier of pharmaceutical-grade glycidol derivatives across North America, Europe, and Asia-Pacific.

China: Integrated Epoxy Value Chains Anchoring Scale and Export Reach

China’s glycidol industry is consolidating its global leadership through deep integration across the epoxy and specialty resin value chain. In 2025, major producers in the Shandong and Jiangsu clusters commissioned fully integrated benzene-to-glycidol complexes, embedding digital twin systems to optimize allyl alcohol epoxidation. These smart manufacturing platforms have reduced byproduct generation by approximately 14% while stabilizing output of high-purity glycidol exceeding 97% assay. This efficiency gain is particularly relevant for downstream epoxy resins, surfactants, and reactive diluents that require consistent molecular performance in industrial coatings and polymer applications.

Policy alignment is reinforcing this trajectory. Under the green chemical mandate issued by the Ministry of Industry and Information Technology, glycidol producers are required to deploy automated catalytic monitoring and energy-optimization systems through 2026. On the demand side, domestic infrastructure expansion has accelerated the use of glycidol as a stabilizing agent in heat-resistant PVC for telecommunications and utility ducting. Export momentum is also strengthening. The commissioning of a dedicated 10,000 metric ton per year chemical pier at the Ningbo-Zhoushan port complex has enabled a sharp rise in technical-grade glycidol shipments to Southeast Asian automotive and component manufacturing hubs, positioning China as the primary supply anchor for the region.

India: Trade Protection and Downstream Polymer Investments Reshaping Demand

India’s glycidol market is entering a structurally different phase, driven by trade policy intervention and aggressive downstream capacity creation. In Q2 2025, India Glycols Limited commissioned the second phase of its Kashipur expansion, adding dedicated capacity for value-added chemical intermediates that utilize glycidol in specialty synthesis. This investment signals a shift away from commodity dependence toward higher-margin derivatives serving coatings, pharmaceuticals, and advanced materials.

The inflection point came with the Ministry of Finance’s Notification No. 33/2025-Customs, which imposed a five-year anti-dumping duty on liquid epoxy resins imported from China, Korea, and Thailand. This measure is forcing domestic resin manufacturers such as Atul Ltd to accelerate local epoxy and derivative production, directly increasing domestic glycidol consumption. Parallel greenfield investments, including a ₹2,100 crore polymer project by Asian Paints in Gujarat, are reinforcing glycidol’s role as a stabilizer in VAE and RDP systems. Additionally, government-backed biomedical research grants in 2025 have prioritized high-purity glycidol for cardiac and anti-arrhythmic drug synthesis, positioning India as an emerging exporter of pharma-grade glycidol intermediates.

United States: Regulatory Precision and EV Materials Innovation

In the United States, glycidol demand is being shaped less by volume expansion and more by regulatory precision and high-value innovation. Updated API guidance issued in 2025 by the Food and Drug Administration has tightened purity expectations for glycidol-derived beta-blockers, prompting pharmaceutical manufacturers to standardize on 97 to 98% assay grades to ensure tissue compatibility and safety. This shift is raising entry barriers while favoring suppliers capable of advanced purification and analytical validation.

Environmental oversight is also intensifying. The Environmental Protection Agency revised Toxic Substances Control Act reporting requirements for epoxide-based intermediates ahead of 2026, mandating granular lot traceability and lifecycle disclosures for industrial glycidol. Beyond regulation, innovation is emerging in e-mobility. U.S.-based chemical majors, including DuPont, are accelerating R&D into glycidol-derived resins for electric vehicle battery thermal management. These materials are engineered to deliver superior dielectric insulation and chemical resistance under high-voltage, high-temperature operating conditions, linking glycidol demand directly to next-generation EV architectures.

Japan: Circular Chemistry and Semiconductor-Grade Differentiation

Japan’s glycidol industry is evolving along two distinct axes: circular material recovery and ultra-high-purity electronics applications. In late 2025, Mitsubishi Chemical Group launched a commercial-scale pilot focused on chemical recycling of composite waste. This initiative enables the recovery of glycidyl-based intermediates from end-of-life materials, aligning glycidol production with Japan’s 2030 circular economy roadmap while reducing dependence on virgin petrochemical feedstocks.

At the same time, Japanese specialty chemical producers are pushing glycidol derivatives into the semiconductor value chain. The scaling of electronic-grade glycidyl methacrylate is supporting advanced photoresist formulations required for domestic 2-nanometer chip manufacturing pilots scheduled for early 2026. This application demands exceptional impurity control and molecular consistency, reinforcing Japan’s position in high-end, low-volume glycidol derivatives rather than commodity supply.

European Union: Food Safety Constraints and Low-VOC Coating Transition

Across the European Union, glycidol dynamics are being reshaped by food safety regulation and sustainability-driven solvent substitution. In January 2025, the European Food Safety Authority implemented lower maximum thresholds for glycidol fatty acid esters in infant nutrition. This regulatory tightening has compelled food processors and edible oil refiners to invest in advanced deodorization and purification technologies to suppress glycidol formation, indirectly influencing upstream refining and analytical demand.

From an industrial perspective, regulators are steering glycidol toward greener applications. Under the forthcoming REACH “Safe by Design” audit scheduled for 2026, European authorities are encouraging the use of glycidol as a low-VOC reactive diluent in epoxy systems for aerospace, marine, and wind energy coatings. This policy-driven substitution is positioning glycidol as a compliance-enabling molecule within the European Green Deal framework, particularly for manufacturers seeking to balance performance with emissions reduction.

Comparative Snapshot: Country-Level Glycidol Industry Drivers

Glycidol Market County Level Snapshot

|

Region

|

Core Strategic Driver

|

Structural Impact on Glycidol Demand

|

|

China

|

Integrated epoxy chains and export logistics

|

Large-scale, cost-efficient technical and high-purity supply

|

|

India

|

Anti-dumping duties and polymer localization

|

Rapid domestic demand growth for specialty derivatives

|

|

United States

|

API purity rules and EV materials R&D

|

High-value, regulation-led consumption

|

|

Japan

|

Circular economy pilots and semiconductor focus

|

Ultra-high-purity, niche derivative expansion

|

|

European Union

|

Food safety limits and low-VOC mandates

|

Compliance-driven adoption in coatings and refining

|

Glycidol Market Report Scope

Glycidol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$198.3 Million

|

|

Market Size (2034)

|

$318.3 Million

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Grade (Technical Grade, Industrial Grade, Specialty Grade, Pharmaceutical Grade), By Type (Racemic Glycidol, Chiral Glycidol), By Application (Chemical Intermediates, Pharmaceuticals, Surface Active Compounds, Advanced Polymers and Resins, Coatings and Adhesives, Textile and Paper Processing), By End-Use Industry (Healthcare and Pharmaceuticals, Automotive and Aerospace, Construction and Infrastructure, Cosmetics and Personal Care, Electronics and Electrical Laminates)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Mitsubishi Chemical Group Corporation, Dow Inc., Hunan Er-Kang Pharmaceutical Co., Ltd., India Glycols Limited, SACHEM, Inc., Evonik Industries AG, Sumitomo Chemical Co., Ltd., Solvay S.A., Lier Chemical Co., Ltd., DuPont de Nemours, Inc., Atul Ltd., Nippon Shokubai Co., Ltd., Merck KGaA, Hubei Jinghong Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glycidol Market Segmentation

By Grade

- Technical Grade

- Industrial Grade

- Specialty Grade

- Pharmaceutical Grade

By Type

- Racemic Glycidol

- Chiral Glycidol

By Application

- Chemical Intermediates

- Pharmaceuticals

- Surface Active Compounds

- Advanced Polymers and Resins

- Coatings and Adhesives

- Textile and Paper Processing

By End-Use Industry

- Healthcare and Pharmaceuticals

- Automotive and Aerospace

- Construction and Infrastructure

- Cosmetics and Personal Care

- Electronics and Electrical Laminates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glycidol Industry

- BASF SE

- Mitsubishi Chemical Group Corporation

- Dow Inc.

- Hunan Er-Kang Pharmaceutical Co., Ltd.

- India Glycols Limited

- SACHEM, Inc.

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- Solvay S.A.

- Lier Chemical Co., Ltd.

- DuPont de Nemours, Inc.

- Atul Ltd.

- Nippon Shokubai Co., Ltd.

- Merck KGaA

- Hubei Jinghong Chemical Co., Ltd.

*- List not Exhaustive