Graphene Market Overview

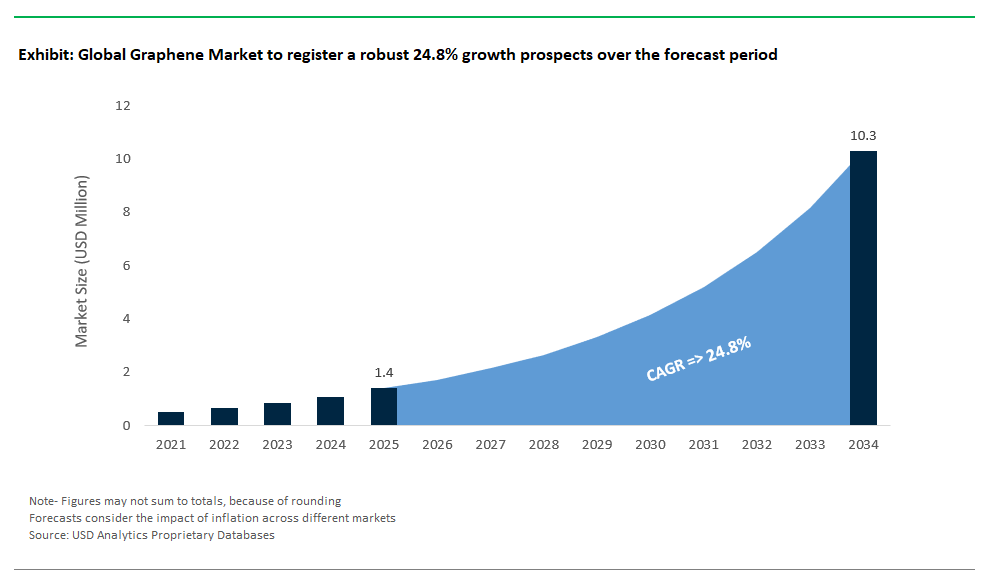

The global graphene market is set for robust growth between 2025 and 2034, fuelled by escalating demand across electronics, energy, and composites applications. Valued at an estimated USD 1.4 billion in 2025, the market is projected to reach approximately USD 10.1 Billion by 2034, expanding at a compelling CAGR of 24.8%. This surge reflects graphene’s transformation from a groundbreaking scientific discovery to a high-impact industrial material attracting substantial investment and commercialization worldwide.

Building on our proprietary datasets, the eighth edition of Graphene market provides a comprehensive analysis and outlook of graphene market across in 21 countries and 17 companies- By Type (Bulk Graphene, Monolayer Graphene), By Application (Composites, Paints, Coatings, Inks, Energy Storage & Harvesting, Electronics, Catalyst, Tires, Others), By End-User (Automotive & Transportation, Aerospace, Electronics, Military & Defense, Others)

Graphene’s unique mechanical strength measured at over 130 GPa, positions it as a game changer for lightweight, high-performance composites in automotive and aerospace. In electronics, its exceptional electrical conductivity and capacity for ballistic electron transport open pathways to ultra-fast transistors, flexible displays, and next-generation integrated circuits. Meanwhile, graphene’s superior thermal conductivity offers critical solutions for heat management in nanoelectronics and high-density energy storage systems, enhancing the efficiency and lifespan of advanced batteries and supercapacitors. Beyond these sectors, graphene’s impermeability to gases and potential biomedical benefits are driving innovations in filtration membranes, water desalination, and targeted drug delivery.

Despite its vast promise, the market faces persistent challenges, including high production costs, defect control in large-scale manufacturing, and technical hurdles like stiction during integration into devices. Yet, these obstacles are increasingly viewed as opportunities for competitive differentiation, with significant R&D investments targeting scalable, cost-efficient manufacturing techniques and new applications.

This report delivers a comprehensive analysis of the global graphene market, offering detailed insights into market size, growth forecasts, competitive strategies, emerging applications, and the evolving landscape of regulations and intellectual property. Stakeholders across the electronics, energy, and composites value chains will gain critical intelligence to effectively navigate this dynamic market and strategically capitalize on the strategic opportunities emerging from graphene’s continued evolution between 2025 and 2034.

Market Analysis: Key Commercial Milestones Driving Graphene Market Growth

The graphene market is advancing decisively from research labs into high-value commercial domains, driven by new product launches, scaled manufacturing capacity, strategic alliances, and robust government support between 2023 and 2024. This period has marked a significant shift, with graphene finding tangible applications in electronics, energy storage, and advanced composites.

Graphene Product Commercialization & Application Innovations

In the sphere of product launches and commercial applications, innovative deployments have underscored graphene’s material advantages. For instance, Recent developments include GMG’s THERMAL-XR® coating achieved key commercialization milestones in November 2024 and secured an industry award in May 2024, signaling confidence in graphene’s potential for enhancing HVAC energy efficiency and reducing operational costs in industrial and commercial buildings. Versarien has made notable progress with its graphene-enhanced concrete admixtures, which saw early trials during 2023 and further advancement into December 2024, demonstrating how graphene can deliver superior strength and durability in construction materials.

In textiles, Directa Plus launched GRAPHITO, an eco-denim product, in June 2023, showcasing graphene’s utility in fashion and medical applications through antibacterial properties and thermal regulation. Meanwhile, the collaboration between the Graphene Flagship and Varta, initially established around 2020, has been making steady progress through 2023 in developing graphene-enhanced batteries aimed at achieving faster charging for consumer electronics, a critical need in today’s fast-paced digital lifestyle.

Momentum in the market is equally visible in expansions and facility openings, as companies invest in scaling up their production capabilities. First Graphene expanded its production operations in Western Australia in 2024 to accommodate rising demand, especially in energy storage and composite applications. NanoXplore’s journey has been especially notable, building on its operational 4,000 tonnes-per-annum facility commissioned in July 2020. The company continues its ambitious vision to scale output to industrial levels, enabling cost efficiencies and broadening supply across sectors like automotive, packaging, and electronics. Across the Atlantic, Paragraf in the UK ramped up manufacturing of graphene-based sensors for industrial and environmental monitoring in 2023, reflecting how graphene’s unique electronic properties are enabling high-performance sensor solutions in multiple sectors.

Graphene Manufacturing Scale-Up and Strategic Partnerships

Strategic partnerships and acquisitions have become critical levers for technological advancement and market penetration, particularly in energy storage and electronics. Lyten’s collaboration with Stellantis in 2023 marks an important milestone in the development of graphene-enhanced lithium-sulfur batteries for electric vehicles. This partnership is focused on delivering batteries that could dramatically increase energy density while reducing weight and costs, an essential step forward for electric mobility. Talga Group, operating across Australia and Sweden, signed deals in 2024 with major European automotive manufacturers to supply graphene-based anode materials for lithium-ion batteries, further strengthening the European EV value chain and demonstrating the growing commercial trust in graphene’s performance benefits. In the electronics domain, Graphenea and Samsung have been collaborating on the integration of graphene into advanced semiconductor devices since 2023, signaling the semiconductor industry’s serious pursuit of graphene’s potential to enable faster, more energy-efficient electronic components.

Graphene R&D Breakthroughs & Government Support Fueling Growth

Progress in research and innovation continues to expand graphene’s potential into new scientific and commercial frontiers. MIT and the University of Manchester have developed ultra-thin graphene membranes for water desalination and purification, offering the promise of high-efficiency solutions to global water challenges, with significant advances achieved in 2023. Rice University has pushed forward the development of laser-induced graphene (LIG), opening pathways for flexible electronics and innovative medical devices, with their work progressing through 2023. Meanwhile, China’s National Graphene Institute announced breakthroughs in graphene-based superconductors in 2024, indicating significant promise for quantum computing and next-generation high-performance electronic systems.

Government initiatives and funding support have played a vital role in maintaining the momentum of commercialization and reducing barriers to market entry. The European Union, through the Graphene Flagship, has channeled an additional €20 million in funding since 2023 to accelerate industrial adoption in energy and composite applications. In North America, the US Department of Energy has continued to support projects focused on graphene applications in advanced batteries and hydrogen storage. Meanwhile, South Korea made a substantial $200 million investment in 2024 to advance graphene research, particularly targeting flexible displays and semiconductor manufacturing, further reflecting Asia’s strong commitment to maintaining leadership in advanced materials.

Competitive Landscape of Graphene Market

The global graphene market is highly dynamic, populated by diverse players pursuing distinct strategies to commercialize this versatile material across applications like batteries, coatings, composites, and flexible electronics. A defining characteristic of the market is the technological specialization of its participants many companies focus on niche applications where graphene’s unique properties, such as high conductivity, mechanical strength, and thermal management, deliver significant performance gains.

In the energy storage segment, several manufacturers are vying for leadership by integrating graphene into next-generation batteries. Australian-based Graphene Manufacturing Group (GMG) has gained attention for developing graphene aluminum-ion batteries that promise rapid charging and high energy density, directly addressing the demands of electric vehicles (EVs) and grid-scale storage. Similarly, NanoXplore in Canada is leveraging its expansive production capacity to supply silicon-graphene anode materials for lithium-ion batteries, collaborating with automotive suppliers to embed graphene into mainstream automotive manufacturing. This signals a strategic push by graphene firms to align with the booming EV and energy transition sectors, which remain key growth drivers for the global market.

Beyond energy, graphene’s role in enhancing mechanical properties and thermal conductivity has fueled its adoption in advanced composites and coatings. UK players like Haydale Graphene Industries and Applied Graphene Materials (Universal Matter Ltd) exemplify this trend, channeling their expertise into functionalized graphene dispersions and additives for protective coatings, aerospace composites, and flexible electronic inks. Their collaborations with major industrial names ranging from BAE Systems and Airbus to coatings giant Sherwin-Williams highlight the increasing penetration of graphene into high-value industrial applications. Meanwhile, First Graphene in Australia has established itself as a major supplier for industrial-scale graphene powders, particularly targeting sustainable construction materials such as graphene-enhanced cement that can reduce CO₂ emissions in building projects, reflecting broader sustainability trends shaping the materials industry.

Another notable area of competition lies in consumer and specialty applications, where companies differentiate by innovating unique end-use products. Italy’s Directa Plus has carved out leadership in textiles and elastomers, supplying graphene nanoplatelets used in sportswear by brands like Colmar and working with Formula One teams on performance materials. Such applications underscore graphene’s potential beyond traditional industrial markets, expanding into lifestyle and environmental solutions, including oil spill remediation products. Similarly, firms like Avanzare Innovación Tecnológica in Spain focus on high-value markets, supplying graphene oxides and conductive inks for flexible electronics and aerospace, often in collaboration with European Space Agency initiatives.

Despite these advances, all players face common market challenges. High production costs, scalability limitations, and the need for consistent material quality continue to constrain widespread commercial adoption. However, growing collaborations between graphene producers and large end-user industries are helping overcome these barriers, driving progress toward cost-effective, scalable solutions. The collective focus on strategic partnerships and proprietary manufacturing technologies positions leading companies to capitalize on the accelerating demand for advanced materials, particularly as industries seek innovations for electric mobility, sustainable infrastructure, and next-generation electronics.

Graphene Market Dynamics: Key Trends and Growth Opportunities

Graphene Accelerates the Future of Flexible and Wearable Electronics

The rapid emergence of graphene as a core material in flexible and wearable electronics is redefining innovation for device manufacturers, investors, and end users worldwide. As the global flexible electronics market is set to surpass $100 billion in value by the end of the decade, graphene’s remarkable set of properties namely its extremely high electrical conductivity, near-total transparency, and mechanical strength that far exceeds steel are fundamentally changing the design and performance standards of next-generation devices. Industry leaders such as Samsung and Huawei are at the forefront, integrating graphene-based OLEDs in foldable smartphones to achieve faster heat dissipation, superior battery efficiency, and robust durability, which are essential for the commercial viability of ultra-thin, flexible form factors. Meanwhile, the booming market for wearable health technologies, projected to reach $74 billion by 2028, is increasingly driven by the adoption of graphene-enabled biosensors. These sensors can deliver up to ten times greater sensitivity for monitoring vital biomarkers such as glucose and heart rate, providing a significant leap in preventive health and personalized medicine.

In parallel, the smart textiles sector is witnessing breakthroughs as companies like Vollebak develop graphene-infused fabrics that offer not just antibacterial and hypoallergenic properties, but also next-level thermal regulation. This directly addresses the growing needs of a smart clothing market valued at $5.4 billion, where comfort, hygiene, and performance are becoming the new benchmarks. Underpinning these advancements is the unprecedented surge in demand for stretchable and conformal electronics, with the segment expected to expand at a CAGR of 30% through 2034. This positions graphene not merely as a material upgrade but as a critical platform technology, opening entirely new revenue streams and applications across the expanding Graphene Market landscape.

Graphene’s Transformative Potential in Next-Gen Energy Storage

Beyond electronics, graphene is now recognized as a disruptive force in advanced energy storage solutions, setting the stage for substantial commercial and technological gains. Graphene’s extraordinarily high surface area (2,630 m²/g) and exceptional electron mobility (200,000 cm²/V·s) make it an ideal candidate for next-generation batteries and supercapacitors. Recent initiatives from industry leaders like Tesla underscore this potential, with research into graphene-anode lithium batteries demonstrating up to fivefold faster charging achievable in under ten minutes and energy densities that are 30% higher than today’s standard lithium-ion cells. The competitive edge of graphene extends further as innovators such as Sila Nanotechnologies and Nanotech Energy engineer battery cells capable of exceeding 500 Wh/kg, laying the groundwork for longer-range EVs and reduced charging infrastructure requirements. In the realm of supercapacitors, companies like Graphene Manufacturing Group (GMG) are reporting power densities up to ten times greater than conventional technologies, potentially allowing electric vehicles to recharge within seconds for specific short-haul applications. This technological leap is equally transformative for the global energy storage sector, which is expected to surpass $50 billion by 2025. Here, graphene’s role in dramatically increasing the cycle life of energy storage systems demonstrating 50,000+ cycles versus just 5,000 cycles for traditional lithium-ion could radically reduce costs and redefine the economics of grid storage and renewable energy integration. The financial implications are profound: even a 5% adoption rate of graphene in the projected $135 billion battery market by 2030 would unlock between $6 billion and $8 billion in annual revenue for graphene suppliers and battery manufacturers. For industry stakeholders, this marks graphene as not just a performance enhancer, but a direct driver of market share, profitability, and technological leadership within the global Graphene Market.

Global Graphene Market Share and Segmentation Analysis

Bulk Graphene Holds the Majority Share, Monolayer Graphene Surges in Advanced Applications

In 2025, bulk graphene including few-layer graphene and graphene oxide accounts for 59.8% of the total market share, establishing itself as the dominant type due to easier mass production and cost efficiency. Bulk graphene’s widespread use in nanocomposites, coatings, and industrial materials has anchored its position in mainstream applications. However, monolayer graphene, despite holding a smaller share (40.2%), is witnessing a higher CAGR of 26.5% through 2034. This accelerated growth is attributed to monolayer graphene’s critical role in high-performance electronics, advanced sensors, and optoelectronic devices, driven by investments in next-generation semiconductors and flexible electronic technologies.

Energy Storage & Harvesting: Largest Application, Electronics Fastest-Growing

The energy storage & harvesting segment covering batteries and supercapacitors leads with 25.6% of the application market in 2025. This leadership is propelled by graphene’s superior conductivity, which is enabling faster-charging, higher-capacity energy storage solutions vital for electric vehicles and renewable energy systems. On the other hand, the electronics segment encompassing flexible displays, wearable tech, and IoT devices registers the highest CAGR at 30.5%, highlighting rapid adoption as manufacturers prioritize performance and miniaturization. These two segments collectively showcase graphene’s dual path: widespread adoption in energy solutions and breakthrough growth in advanced electronics.

Automotive & Transportation: Leading End-User Industry, Electronics Not Far Behind

Automotive and transportation account for 27.8% of total graphene demand in 2025, making it the top end-user industry. The push for lightweight, durable, and energy-efficient vehicles is driving the integration of graphene into batteries, tires, and composite components. Meanwhile, the electronics industry is not far behind, capturing a significant share of 22.1%, and is set to outpace others in growth rate. As both electric mobility and smart consumer devices expand, these industries will continue to shape the trajectory of global graphene consumption.

Country Analysis of Graphene Market

United Kingdom: From University-Led Innovation to Industry Partnerships

The United Kingdom’s graphene sector is underpinned by robust academic research and dynamic public-private partnerships. In 2023, the University of Manchester continued to secure significant investment and awards, such as the Eli and Britt Harari Graphene Enterprise Award, to accelerate graphene commercialization, bolstering the national innovation ecosystem. Versarien’s partnership with Costain to develop graphene-enhanced concrete (2023) points to real-world deployment in infrastructure, targeting longer-lasting, more sustainable building materials. Paragraf’s 2024 launch of graphene biosensors for disease detection illustrates the UK’s push into medical diagnostics and high-tech applications. This confluence of world-class research, infrastructure innovation, and medical technology ensures the UK remains a leading node in the global graphene value chain.

Canada: Scaling Up Production and Commercial Battery Breakthroughs

Canada’s graphene market is characterized by large-scale production and breakthroughs in battery technology. Graphene Manufacturing Group (GMG)’s commercialization of aluminum-ion batteries places Canada at the center of the battery innovation race, appealing to both EV and grid storage markets. Meanwhile, NanoXplore’s expansion makes it one of the largest graphene producers worldwide, enabling cost efficiencies and broadening supply to sectors like automotive, packaging, and electronics. The Canadian approach emphasizes industrial scaling, robust supply chains, and strategic positioning in sustainable technology sectors.

South Korea: Integrating Graphene in Electronics and EV Batteries

South Korea leverages its electronics manufacturing prowess to drive graphene innovation, particularly in displays and battery technology. Samsung's ongoing research and development into integrating graphene into foldable OLED displays points towards more durable, flexible devices, reinforcing South Korea’s global reputation in consumer electronics. LG Chem’s work on graphene battery anodes for electric vehicles (2023) further accelerates the country’s competitiveness in next-gen mobility solutions. South Korea’s graphene market is thus shaped by a tight link between R&D and global product launches, especially in high-volume, high-tech consumer and industrial segments. In particular, Graphene sheets remains a lucrative segment in the country with leading companies such as Standard Graphene focusing on new product launches in IT, military, and bio industries.

Australia: Mining Partnerships and Advanced Battery Materials

Australia’s graphene sector draws strength from its resource-rich landscape and focus on energy materials. First Graphene’s partnership with mining giant Rio Tinto reflects a strategic move to supply graphene-enhanced materials for the mining sector and beyond, leveraging Australia’s mineral expertise. Talga Group’s launch of graphene silicon anodes for batteries in 2024 places Australia at the frontier of advanced battery materials, supporting both domestic innovation and global supply chains. The Australian approach uniquely blends resource integration, mining, and high-value downstream applications.

Spain: Supplying Europe’s Research Ambitions and Safety Solutions

Spain’s graphene market is propelled by specialist companies supporting broader European initiatives and safety-driven applications. Graphenea’s role as a material supplier for the EU’s Graphene Flagship Project highlights Spain’s importance in research-grade graphene production and pan-European collaboration. Meanwhile, GrapheneTech’s development of fire-resistant graphene coatings is expanding the range of industrial safety and construction applications. Spain’s contribution is marked by specialty materials, research synergies, and a focus on protective technologies.

India: Home-Grown R&D and Commercialization for Industrial and Clean Mobility

India is building a dynamic graphene market with a strong emphasis on local R&D and clean energy solutions. The IIT Bombay & Tata Steel partnership to develop graphene-coated steel illustrates the move toward corrosion-resistant, high-strength industrial materials. Log 9 Materials’ launch of graphene-based fuel cells for electric vehicles signals a significant foray into sustainable transportation technologies, positioning India as an innovator in clean energy and advanced materials. With robust public-private collaboration and a focus on industrial applications and green mobility, India’s graphene market is quickly gaining international traction. Further, strong growth prospects in Graphene plastics are encouraging the foray of new investments in the country.

Graphene Market Report Scope

Graphene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$10.1 Billion

|

|

Market Growth Rate

|

24.8%

|

|

Segments

|

By Type (Bulk Graphene, Monolayer Graphene), By Application (Composites, Paints, Coatings, Inks, Energy Storage & Harvesting, Electronics, Catalyst, Tires, Others), By End-User (Automotive & Transportation, Aerospace, Electronics, Military & Defense, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

2D Carbon Graphene Material Co., Ltd., ACS Material, AMO GmbH, Applied Graphene Materials, BGT Materials Limited, CVD Equipment Corporation, Directa Plus S.p.A., Grafoid Inc, Graphene Laboratorie Inc, GRAPHENE SQUARE INC, Graphenea, Graphensic AB, Haydale Graphene Industries Plc, NanoXplore Inc., Talga Group, Thomas Swan & Co. Ltd., Zentek Ltd, and Others

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene Market Segmentation

By Type

- Bulk Graphene

- Monolayer Graphene

By Application

- Composites

- Paints

- Coatings

- Inks

- Energy Storage & Harvesting

- Electronics

- Catalyst

- Tires

- Others

By End-User

- Automotive & Transportation

- Aerospace

- Electronics

- Military & Defense

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Market

- 2D Carbon Graphene Material Co., Ltd.

- ACS Material

- AMO GmbH

- Applied Graphene Materials

- BGT Materials Limited

- CVD Equipment Corporation

- Directa Plus S.p.A.

- Grafoid Inc

- Graphene Laboratorie Inc

- GRAPHENE SQUARE INC

- Graphenea

- Graphensic AB

- Haydale Graphene Industries Plc

- NanoXplore Inc.

- Talga Group

- Thomas Swan & Co. Ltd.

- Zentek Ltd

*- List Not Exhaustive

Research Methodology

This graphene market research report integrates both secondary and primary research to ensure analytical rigor and actionable insights. The secondary research phase involved a comprehensive review of scientific literature, patent filings, industry association reports, company disclosures, and international trade data to map out historical market trends, emerging applications, and innovation patterns across electronics, energy, and composites. This desk research was augmented with analysis of regulatory frameworks, funding initiatives, and competitive developments at both global and country levels.

To validate and enrich the findings, structured interviews and surveys were conducted with industry experts, including executives from graphene manufacturers, battery and electronics OEMs, researchers in advanced materials, and stakeholders from end-user industries. Market size estimation and forecasting leveraged a blend of top-down and bottom-up modeling, cross-verified through data triangulation and scenario analysis. Competitive intelligence and country-level market assessments were further enhanced through real-time industry feedback, enabling the report to deliver robust market sizing, growth projections, and strategic insights tailored for decision-makers navigating the evolving global graphene landscape.

Table Of Contents

1. Executive Summary

1.1. Global Graphene Market Snapshot

1.2. Key Findings & Future Outlook

2. Global Graphene Market Overview (2025-2034)

2.1. Market Definition & Scope

2.2. Market Valuation & Growth Forecast (2025-2034)

2.2.1. Market Size (USD Billion)

2.2.2. Compound Annual Growth Rate (CAGR %)

2.3. Key Properties & Applications of Graphene

2.4. Market Challenges & Opportunities

3. Market Analysis: Key Commercial Milestones Driving Graphene Market Growth

3.1. Graphene Product Commercialization & Application Innovations

3.2. Graphene Manufacturing Scale-Up and Strategic Partnerships

3.3. Graphene R&D Breakthroughs & Government Support Fueling Growth

4. Graphene Market Dynamics and Key Trends

4.1. Trend: Graphene Accelerates the Future of Flexible and Wearable Electronics

4.2. Opportunity: Graphene’s Transformative Potential in Next-Gen Energy Storage

4.3. Restraints

5. Global Graphene Market Share and Segmentation Analysis (2021-2034)

5.1. By Graphene Type

5.1.1. Bulk Graphene (Few-layer, Graphene Oxide, Graphene Nanoplatelets)

5.1.2. Monolayer Graphene

5.2. By Application

5.2.1. Energy Storage & Harvesting (Batteries, Supercapacitors)

5.2.2. Electronics (Flexible Displays, Wearable Tech, IoT Devices)

5.2.3. Composites (Automotive, Aerospace, Construction)

5.2.4. Paints, Coatings & Inks

5.2.5. Others

5.3. By End-User Industry

5.3.1. Automotive & Transportation

5.3.2. Electronics & Telecommunications

5.3.3. Construction

5.3.4. Aerospace & Defense

5.3.5. Healthcare & Biomedical

5.3.6. Others

6. Country Analysis and Outlook of Graphene Market, 2021- 2034

6.1. United States: Pioneering Research and Diverse Industrial Adoption

6.2. Canada: Scaling Up Production and Commercial Battery Breakthroughs

6.3. Mexico: Emerging Demand from Manufacturing and Export Hubs

6.4. Germany: Automotive Innovation and Advanced Materials Research

6.5. United Kingdom: From University-Led Innovation to Industry Partnerships

6.6. France: Aerospace, Defense, and Composite Material Advancements

6.7. Spain: Supplying Europe’s Research Ambitions and Safety Solutions

6.8. Italy: Textiles, Elastomers, and Niche Industrial Applications

6.9. Russia: Fundamental Research and Strategic Industrial Interests

6.10. Rest of Europe: Diverse Specializations and Collaborative Initiatives

6.11. China: Mass Production and Dominance in Industrial Applications

6.12. India: Home-Grown R&D and Commercialization for Industrial and Clean Mobility

6.13. Japan: High-Tech Electronics and Precision Engineering Innovations

6.14. South Korea: Integrating Graphene in Electronics and EV Batteries

6.15. Australia: Mining Partnerships and Advanced Battery Materials

6.16. Southeast Asia: Emerging Manufacturing and Growing Industrial Demand

6.17. Rest of Asia Pacific: Developing Markets and Niche Application Growth

6.18. Brazil: Resource-Rich Landscape and Emerging Industrial Applications

6.19. Argentina: Research Initiatives and Agricultural Sector Potential

6.20. Rest of South America: Nascent Markets and Future Growth Prospects

6.21. Middle East & Africa: Strategic Investments in Diversification and Energy

7. Graphene Market Size Outlook by Region

7.1 North America Graphene Market Size Outlook to 2034

- by Type

- by Application

- by End User Industry

7.2 Europe Graphene Market Size Outlook to 2034

- by Type

- by Application

- by End User Industry

7.3 Asia Pacific Graphene Market Size Outlook to 2034

- by Type

- by Application

- by End User Industry

7.4 South and Central America Graphene Market Size Outlook to 2034

- by Type

- by Application

- by End User Industry

7.5 Middle East and Africa Graphene Market Size Outlook to 2034

- by Type

- by Application

- by End User Industry

8. Competitive Landscape of Graphene Market

8.1. Market Share by Company, 2024

8.2 Key Player Strategies

8.3. Top Graphene Company Profiles (Overview, Key Products/Services, SWOT, Recent Developments)

8.3.1. 2D Carbon Graphene Material Co., Ltd.

8.3.2. ACS Material

8.3.3. AMO GmbH

8.3.4. Applied Graphene Materials

8.3.5. BGT Materials Limited

8.3.6. CVD Equipment Corp

8.3.7. Directa Plus S.p.A.

8.3.8. Grafoid Inc

8.3.9. Graphene Laboratories, Inc.

8.3.10. Graphene Square Inc

8.3.11. Graphenea

8.3.12. Graphensic AB

8.3.13. Haydale Graphene Industries Plc

8.3.14. NanoXplore Inc

8.3.15. Talga Group

8.3.16. Thomas Swan & Co. Ltd.

8.3.17. Zentek Ltd

9. Conclusion & Strategic Recommendations

9.1. Analyst Perspective

9.2. Conclusions and Future Remarks

10. Appendix

10.1. Research Methodology

10.2. Data Sources

10.3. List of Acronyms