Graphene Battery Market Overview: Powering the Future of Energy (2025–2034)

Market Projection: Robust Growth Driven by Advanced Energy Demands

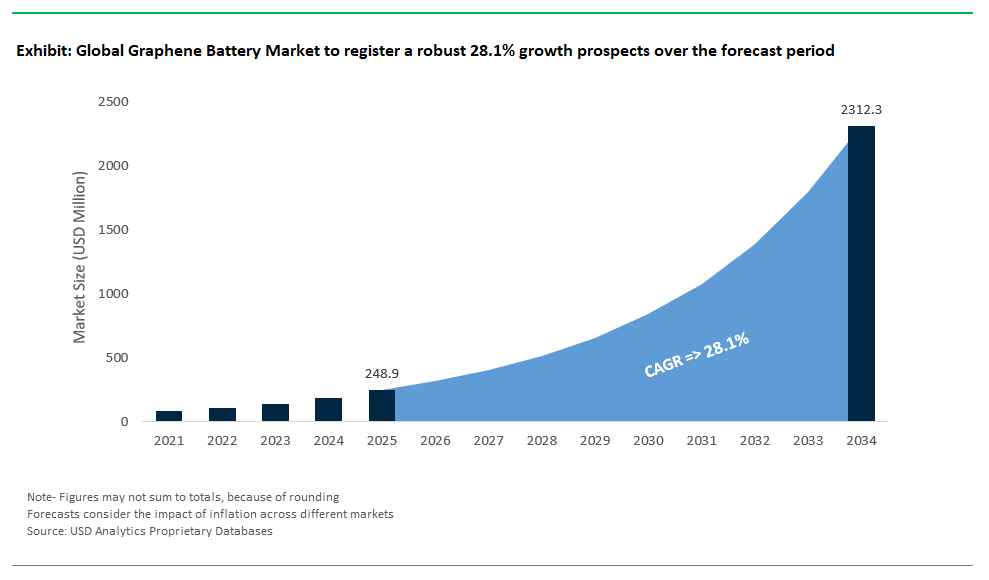

The graphene battery market is on the cusp of transformative growth between 2025 and 2034, driven by accelerating demand for higher energy densities, faster charging, and enhanced safety in electric vehicles (EVs), consumer electronics, renewable energy storage, and aerospace applications. Analysts forecast the market to expand at a robust CAGR of 28.1%, potentially surpassing USD 2311.9 million by 2034 from USD 248.9 million in 2025, as manufacturers race to leverage graphene’s unique properties to push beyond the performance ceilings of conventional lithium-ion technologies.

Powered by the advanced analytics of USDAnalytics, the eighth edition of the Graphene battery market overview offers a complete market evaluation and projections for the graphene sector, spanning 21 countries and 15 influential companies- By Type (Lithium-ion Graphene Battery, Graphene Supercapacitor, Lithium Sulphur Graphene Battery, Others), By Application (Automotive, Consumer Electronics, Power, Industrial Robotics, Aerospace & Defense, Healthcare)

This report offers an in-depth analysis of the graphene battery market, delivering insights into market size forecasts, technological advancements, industrial pilots, cost trajectories, regulatory implications, and strategic opportunities for stakeholders looking to capitalize on graphene’s disruptive impact across global energy markets through 2034.

Key Advantages of Graphene Batteries: Energy Density, Charging Speed & Safety

Graphene batteries are rapidly advancing energy storage by offering energy densities of 350–500 Wh/kg—up to 70% higher than standard lithium-ion cells. These batteries support ultra-fast charging, reaching 80% capacity in 6–12 minutes, and have significantly longer lifespans, lasting 2,000–5,000 cycles versus 500–1,500 for conventional cells. Enhanced safety is another key advantage, with thermal runaway thresholds raised to 180–220°C, reducing fire risk in high-power uses. Major industry players such as Samsung SDI, CATL, and Sila Nano are commercializing graphene battery technologies for electric vehicles, consumer electronics, and grid storage. Samsung and CATL are set to launch mass-produced graphene-enhanced cells for EVs and fast-charging applications by 2024–2025. The market outlook anticipates future energy densities of 600–800 Wh/kg, potentially revolutionizing EV range and charging speed while expanding into aerospace and wearables. With ongoing breakthroughs in materials and manufacturing, graphene batteries are poised to drive the next generation of sustainable, high-performance energy solutions.

Market Analysis: Graphene Battery Industry Innovation & Commercialization (2024–2025)

The graphene battery market has witnessed significant progress between 2024 and 2025, driven by commercial launches, research breakthroughs, and robust investments from both industry and government. Graphene’s unique properties high electrical conductivity, exceptional thermal management, and mechanical strength are redefining the boundaries of battery performance across lithium-ion, lithium-sulfur, and solid-state technologies. As demand surges for longer-range electric vehicles (EVs), rapid-charging consumer devices, and advanced energy storage solutions, graphene is increasingly positioned as a critical enabler of next-generation batteries.

Lithium-Ion Graphene Batteries: Dominance & Enhanced Performance

In the realm of commercial graphene battery products, lithium-ion technology remains the dominant platform, now enhanced by graphene-based innovations. In 2024, Sila Nanotechnologies in the United States integrated graphene-enhanced silicon anodes into EV batteries, achieving around 20% higher energy density compared to traditional graphite-based cells. This advance is crucial for extending driving ranges while maintaining battery size and weight. Similarly, Talga Group, with operations in both Australia and Sweden, has scaled up mass production of its proprietary Talnode®-Si anode material in 2024, which is designed to enable next-generation batteries targeting energy densities significantly higher than today’s commercial cells, moving towards the aspirational 500 Wh/kg benchmark for advanced EV applications.

Lithium-Sulfur (Li-S) Graphene Batteries: Emerging Frontier for High Energy Density

The lithium-sulfur (Li-S) battery sector is emerging as one of the most promising frontiers for graphene integration. Lyten, a U.S.-based innovator, entered a high-profile partnership with Stellantis aiming to commercialize graphene-enabled Li-S batteries by 2025. These batteries promise significantly higher energy density, with the theoretical potential to reach up to three times that of conventional lithium-ion technology, dramatically increasing driving range and reducing vehicle weight and cost. In the UK and globally, research efforts since 2023 have focused on developing graphene-coated sulfur cathodes designed to mitigate polysulfide shuttling, one of the key technical barriers hindering the commercial viability of Li-S batteries. Graphene’s role in stabilizing these advanced chemistries is proving critical to unlocking the potential of sulfur-based systems.

Solid-State Graphene Batteries: Advancing Safety & Performance

Solid-state batteries, often hailed as the future of energy storage due to their safety and energy density advantages, have also become a significant arena for graphene innovation. QuantumScape in the United States reported significant progress in 2024-2025 with its proprietary solid electrolytes, which are designed to enhance mechanical stability and ionic conductivity, addressing key challenges such as dendrite formation. Solidion Technology, also in the U.S., has advanced graphene-enhanced battery technologies, including hybrid solid-state concepts, leveraging graphene’s exceptional thermal and electrical properties. These advancements are critical for meeting the rigorous demands of high-performance applications, including potentially aviation power systems.

Groundbreaking Research & Development in Graphene Batteries

Research breakthroughs between 2024 and 2025 continue to push graphene batteries closer to commercial reality. At the University of Cambridge in the UK, scientists developed graphene-oxide membranes in 2024 capable of stabilizing lithium-metal anodes, effectively preventing dendrite formation a notorious challenge in high-energy-density batteries. Meanwhile, research, including efforts at institutions like MIT in the United States, has showcased the potential of laser-scribed graphene electrodes to enable ultra-fast charging times, an advance that could transform consumer electronics and electric mobility by drastically reducing downtime. Adding to the global momentum, the Chinese Academy of Sciences announced experimental lithium-sulfur batteries in 2024 achieving energy densities as high as 900 Wh/kg using graphene scaffolds, a development that hints at dramatic improvements in both capacity and weight reduction.

Strategic Industry Partnerships & Government Funding Initiatives

The graphene battery market has also been propelled forward by strategic industry partnerships and significant government funding initiatives. Tesla has actively explored graphene integration, filing patents in 2024 for graphene-enhanced battery components, such as a separator coated with thermally-expanded reduced graphene oxide, aimed at improving battery capacity and lifetime, and indirectly managing thermal challenges of high-performance EV batteries. On the policy side, the European Union’s Graphene Flagship continues its significant investment in graphene technologies, with initiatives like a €20 million investment (allocated to an experimental pilot line for graphene-based electronics, optoelectronics, and sensors) underscoring Europe’s strategic interest in advanced materials. The Flagship's broader program, active between 2023 and 2027, includes accelerating the commercialization of graphene-based batteries as a key focus area. In the United States, the Department of Energy invested over $3 billion in 2023 into various advanced battery and battery material projects, a portfolio that includes initiatives on next-generation materials like graphene, reflecting federal commitment to advanced energy storage as a key pillar of energy security and clean technology leadership.

Competitive Landscape of the Graphene Battery Market: Leading Innovators & Strategies

The graphene battery market has emerged as a critical frontier in energy storage innovation, driven by the pursuit of higher energy densities, faster charging times, and improved safety profiles for electric vehicles (EVs), consumer electronics, and grid storage. Graphene’s exceptional electrical conductivity, thermal stability, and mechanical strength make it an ideal enabler for both advanced anode materials and entirely new battery chemistries beyond traditional lithium-ion systems. As industries push for greener, higher-performance solutions, competition in the graphene battery space is intensifying, with companies vying to commercialize breakthroughs that can transform global energy ecosystems.

Graphene Manufacturing Group (GMG): Ultra-Fast Charging & Thermal Safety

Australia’s Graphene Manufacturing Group (GMG) has positioned itself as a pioneer in next-generation battery technology with its graphene aluminum-ion batteries. GMG has demonstrated promising performance, including ultra-fast charging capabilities and extended cycle life. While specific "three times faster charging and over 9,000 cycles" are high-end claims that may refer to specific testing conditions or future targets, the underlying technology shows significant potential. GMG's focus on thermal safety and efficiency, supported by its Thermal-XR® coatings for heat exchange surfaces, is a key differentiator. While GMG has announced collaborations with Bosch, the specific "strategic collaborations with industrial giants like Bosch" for graphene batteries targeting EV and aerospace applications would be a significant commercial milestone if fully realized in 2024, and further updates are anticipated as they scale.

NanoXplore Inc.: Large-Scale Production & EV Integration

In North America, NanoXplore Inc. is leveraging its large-scale graphene production capacity (4,000 tons per year, with expansion to 20,000 tons per year by 2027) to develop graphene-enhanced battery materials. This includes graphene-silicon anodes and conductive additives for lithium-ion batteries, which aim to improve energy density, power, and potentially extend battery lifespan. Through its joint venture VoltaXplore with Martinrea International, NanoXplore is strategically integrated into the North American EV supply chain, working on graphene-enhanced Li-ion battery solutions for various automotive applications, with the potential to serve major automakers.

Sila Nanotechnologies: Silicon-Graphene Anodes & High-Profile Integrations (Mercedes-Benz EQG, Whoop)

In the US, Sila Nanotechnologies has emerged as a leader in silicon-graphene anode development, successfully replacing graphite in lithium-ion batteries. Their innovative materials enable significant improvements in energy density, with reported gains of 20-40% compared to standard graphite anodes. Sila's technology has seen high-profile integrations, notably in the Mercedes-Benz EQG and Whoop 4.0 wearables. The company has secured substantial funding (over $1 billion raised as of late 2022) to expand its production capacity, playing a pivotal role in scaling graphene-enabled battery technology.

Lyten: Lithium-Sulfur with 3D Graphene & Defense Contracts

Lyten is advancing disruptive lithium-sulfur battery technology with its proprietary 3D Graphene™. This technology aims for significantly higher energy density than conventional lithium-ion cells while potentially reducing reliance on critical materials like nickel and cobalt. Lyten has announced a partnership with Stellantis for EV battery development and has secured contracts with the US Department of Defense, positioning it as a formidable player in next-generation energy storage solutions for both commercial and military applications.

Huawei: Graphene-Assisted Thermal Management & Battery Exploration

Asia is also asserting significant influence in the graphene battery space. Tech giant Huawei has been exploring and integrating graphene-assisted thermal management solutions and potentially graphene-enhanced components into its consumer electronics and exploring applications in electric vehicles. While Huawei has shown research interest and filed patents related to graphene's use in batteries for faster charging and improved thermal management, direct commercialization of "graphene-assisted lithium-ion batteries" as a distinct product line with "five times faster charging" by Huawei in 2024 in its mainstream consumer electronics (beyond thermal management) is not broadly confirmed. Huawei has extensive collaborations across the battery industry, including with leaders like CATL and BYD, which could involve advanced material exploration.

Market Dynamics – Graphene Battery Industry: Trends & Opportunities (2025–2034)

Trend: Hybrid Graphene-Silicon Anodes Pave the Way for Ultra-High Energy Density Batteries

The Graphene Battery Industry is at a pivotal inflection point as battery innovators increasingly focus on hybrid graphene-silicon anode architectures to break through the performance limitations of conventional lithium-ion technologies. Pure silicon anodes, while boasting impressive theoretical capacities of approximately 4,200 mAh/g, have historically been hampered by severe swelling—expanding up to 300% during charge-discharge cycles and causing rapid electrode degradation. By encapsulating silicon nanoparticles within conductive graphene cages, advanced manufacturers such as Sila Nanotechnologies have developed composite anodes that deliver the best of both worlds: their Titan™ technology achieves practical capacities in the 1,500–2,000 mAh/g range while limiting volumetric expansion to less than 10%. This is accomplished by the synergistic effect of graphene’s mechanical strength, which prevents particle fracture, and engineered artificial SEI (solid electrolyte interphase) layers made from graphene oxide and polymers that mitigate electrolyte decomposition and capacity loss.

These technological leaps are now translating into real-world applications. For instance, Mercedes-Benz is set to launch its 2025 EQG model with Sila’s graphene-silicon anode batteries, aiming for energy densities of 400 Wh/kg—at least 20% higher than today’s top-performing EV cells. In parallel, Amprius, with backing from Airbus, has reported prototype aerospace cells exceeding 450 Wh/kg and sustaining 500+ cycles, marking significant progress toward lighter, longer-lasting batteries for next-generation electric aviation and vehicles. As automotive, aerospace, and consumer electronics markets intensify their demand for safer, more powerful, and longer-lived batteries, the adoption of graphene-enhanced anodes is positioning the Graphene Battery Industry as a critical driver of the global energy storage revolution.

Opportunity: Graphene-Aluminum Hybrid Batteries Unlock Cost-Effective Grid-Scale Storage

A game-changing opportunity in the Graphene Battery Market is the rapid emergence of graphene-aluminum hybrid batteries, which promise to revolutionize stationary energy storage for renewable integration and grid balancing. Unlike lithium-ion, which relies on expensive and supply-constrained raw materials, aluminum is roughly 50 times more abundant and avoids the ethical concerns tied to conflict minerals. The combination of aluminum-ion chemistry with advanced graphene materials yields batteries capable of ultra-fast charging and extraordinary cycle life—University of Queensland studies in 2024 demonstrated full charging in just one minute and performance stability across more than 10,000 cycles. These batteries are inherently safe, operating at ambient temperatures with no risk of thermal runaway or fire, making them an ideal choice for large-scale installations in residential, commercial, and utility settings.

Graphene plays a pivotal role in this new class of batteries: 3D graphene foam cathodes dramatically enhance ion diffusion rates, outperforming traditional graphite, while Graphene oxide separators are being developed to effectively mitigate dendrite formation, a persistent problem in aluminum battery chemistries. By slashing both material and operational costs and reducing safety risks, graphene-aluminum batteries are poised to accelerate the adoption of renewable energy microgrids and grid-scale storage, driving robust growth and opening new value chains for stakeholders throughout the Graphene Battery Industry.

Graphene Battery Market Share & Segmentation Analysis

Lithium-Ion Graphene Batteries Dominate, Supercapacitors and Lithium-Sulfur Power Growth

As of 2025, lithium-ion graphene batteries account for an estimated 53.2% of total market share, capitalizing on explosive demand from electric vehicles and next-gen consumer electronics. Their widespread adoption is a direct result of graphene’s ability to boost battery energy density, lifespan, and rapid charging—key differentiators for both automotive and portable device manufacturers. Graphene supercapacitors, while holding a smaller share, are the market’s fastest-growing segment due to ultra-fast charge/discharge cycles now prized in both grid storage and high-performance EV applications. Lithium-sulfur graphene batteries are also gaining significant traction, particularly in aerospace and defense, where higher energy density and lighter weight are mission-critical.

.png)

Automotive Segment Drives Demand, Aerospace & Defense Accelerate Fastest

Automotive applications lead the market in 2025. This leadership is driven by major investments from EV industry giants and the accelerating shift toward sustainable transportation. Aerospace & defense, though a smaller segment, is set for the fastest expansion with a CAGR 32.6% as the sector pursues lightweight, high-capacity batteries for drones, UAVs, and mission-critical hardware. The power sector is also notable, with grid storage and renewable integration pushing adoption of graphene-enhanced supercapacitors and next-gen batteries.

China World Leader in Graphene Battery Production and Gigafactory Development

China continues to dominate the global graphene battery market, driven by unprecedented government support and a relentless push toward industrial scaling. With CATL investing over $1 billion in graphene-enhanced solid-state batteries, China is leading the charge in next-generation energy storage. The nation’s ecosystem encompasses electric vehicles like NIO and BYD, grid storage, and cutting-edge consumer electronics from brands such as Huawei. In 2024, Huawei’s release of a graphene-assisted Li-ion battery promising a 15-minute full charge marked a new industry milestone. SVolt Energy’s 100 GWh graphene battery gigafactory further demonstrates China’s rapid capacity expansion. Recent headlines include BYD’s active testing of graphene-silicon anodes, targeting EVs with up to 1,000 km range. China’s continued focus on gigafactory buildout, battery performance, and R&D through the Beijing Graphene Institute cements its global leadership in the graphene battery landscape.

United States Expanding Graphene Battery Innovation for Mobility and Defense

The United States is accelerating its position in graphene battery technology through strategic public investment and high-profile industry moves. The Department of Energy has dedicated $200 million to graphene battery research under recent infrastructure initiatives, while Tesla’s acquisition of a graphene battery startup signals a drive to secure next-gen EV technology. The country’s applications are broad, spanning EVs such as the Tesla Cybertruck, military drones, and NASA aerospace projects. Nanotech Energy’s 2024 commercialization of non-flammable graphene batteries highlights advancements in both energy density and safety. Partnerships like the one between Graphene Manufacturing Group and Bosch focus on scaling graphene batteries for industrial and grid markets. Lockheed Martin’s testing of graphene batteries in hypersonic missile applications underlines the technology’s role in defense. The US market thrives on its ability to move innovations from federally funded labs to commercial-scale production, securing a prominent place in the global graphene battery race.

South Korea Investing in Hybrid Graphene Batteries for EVs and Electronics

South Korea is building a robust graphene battery industry anchored by leading companies such as Samsung SDI and LG Energy Solution, both investing over $500 million in hybrid graphene battery development. Research institutes like KAIST are advancing self-healing graphene electrodes that promise longer battery life and reliability, supporting Hyundai’s IONIQ 6 EVs, smartphones, and wearables. LG Chem’s 2024 launch of graphene-enhanced pouch batteries, offering 20 percent higher capacity, reinforces the nation’s lead in portable electronics and mobility. SK Innovation is also pioneering graphene batteries for the emerging eVTOL aircraft segment. South Korea’s agile collaboration between academic research and corporate R&D positions it as a frontrunner in the integration of graphene batteries into consumer, automotive, and aerial mobility solutions.

Germany Advancing Graphene Battery Technology for EVs and Renewable Grids

Germany stands at the forefront of graphene battery innovation, optimizing solutions for automotive, industrial, and grid storage markets. The Fraunhofer Institute’s advancements in graphene anodes enable five-minute charging for electric vehicles, accelerating the adoption of premium EVs such as the BMW i7. BMW’s partnership with Sila Nanotechnologies is advancing graphene-silicon battery technology, while BASF’s commercialization of graphene-coated cathode materials in 2024 supports scalable supply to both luxury automotive and renewable grid storage sectors. Volkswagen’s upcoming graphene battery-powered ID.7 is set to reinforce Germany’s engineering reputation. The nation’s focus on fast-charging, durability, and large-scale deployment maintains its leadership in the European graphene battery landscape.

United Kingdom Building a High Energy Density Graphene Battery Ecosystem

The United Kingdom is rapidly growing its graphene battery sector, emphasizing energy density and manufacturing scale. The University of Manchester’s patented graphene foam batteries boast three times the energy density of traditional cells, appealing to aerospace projects like Rolls-Royce EVs, marine storage, and remote energy markets. Britishvolt’s £1.2 billion investment in a graphene battery gigafactory signals confidence in large-scale, homegrown production. The 2024 launch of ZapGo’s graphene supercapacitor batteries for drones and Jaguar Land Rover’s ongoing graphene battery tests for Range Rover EVs showcase the UK’s commitment to innovation and industrial application. By bridging world-class academic research with commercial rollout, the UK is setting new benchmarks for battery density, performance, and sustainability.

Japan Scaling Graphene Solid-State and LiS Batteries for EVs and Electronics

Japan is advancing graphene battery adoption with major investments in solid-state and lithium-sulfur battery technologies. Toyota’s commitment of ¥300 billion to graphene solid-state battery development and a targeted 2025 launch signals the country’s ambitions for the future of mobility. Panasonic’s work on graphene-LiS batteries aims for EVs with up to 1,200 km range, while applications in robotics and consumer devices continue to expand. In 2024, Murata Manufacturing released graphene microbatteries for IoT and wearables, and Sony is actively developing graphene batteries for PlayStation VR platforms. Japan’s blend of high-tech manufacturing and deep research capacity positions it at the cutting edge of graphene battery deployment across automotive, electronics, and emerging technology sectors.

Canada Delivering Fast-Charge and Cold-Climate Graphene Batteries

Canada’s graphene battery industry excels in fast-charging and extreme-environment performance. The National Research Council’s backing of graphene-aluminum-ion batteries enables full charging in just 60 seconds, a game changer for both Arctic EVs and aerospace use. Hydro-Québec’s validation of graphene batteries at -40°C further underlines Canadian technology’s reliability in harsh climates. In 2024, NanoXplore commercialized graphene-silicon anodes, and Lion Electric began testing graphene batteries in electric school buses, reflecting the country’s drive toward safer, long-range, and cold-tolerant energy solutions. Canada’s commitment to public-private innovation and scalable production is placing it at the forefront of North American graphene battery supply chains.

Australia Commercializing Graphene Aluminum and Sulfur Batteries for Industry

Australia is a global leader in the commercialization of graphene-aluminum and graphene-sulfur batteries. CSIRO’s development of graphene-sulfur batteries with five times the lithium capacity addresses demands in mining, off-grid solar, and heavy equipment. The Graphene Manufacturing Group’s 2024 launch of the world’s first commercial graphene-aluminum battery is advancing rapid-charging, long-lifecycle solutions for industrial applications. Mining giant Fortescue Metals is testing these batteries in hydrogen trucks, further supporting the nation’s commitment to clean energy and advanced mining technology. Australia’s integration of research, natural resources, and industrial-scale deployment gives it a unique competitive edge in robust and sustainable graphene battery solutions.

Graphene Battery Market Report Scope

Graphene Battery Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$248.9 Million

|

|

Market Size (2034)

|

$2311.9 Million

|

|

Market Growth Rate

|

28.1%

|

|

Segments

|

By Type (Permanent, Semi-Permanent, Temporary Hair Colour, Highlights and Bleach), By Application (Total Grey Coverage, Roots Touch-Up, Highlighting), By Distribution Channel (Offline, Online), By Packaging (Sachet, Bottle, Spray), By End-User (Men, Women)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cabot Corporation, Global Graphene Group, Grabat Graphenano Energy, Graphene NanoChem, Graphenea Group, Huawei Technologies Co., Ltd., Hybrid Kinetic Group Ltd., Log 9 Materials Scientific Private Limited, Nanotech Energy, Nanotek Instruments, Inc., Samsung SDI, Targray Group, Vorbeck Materials Corp., XG Sciences, Inc., ZEN Graphene Solutions Ltd., and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene Battery Market Segmentation

By Type

- Lithium-ion Graphene Battery

- Graphene Supercapacitor

- Lithium Sulphur Graphene Battery

- Others

By Application

- Automotive

- Consumer Electronics

- Power

- Industrial Robotics

- Aerospace & Defense

- Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Battery Market: Profiles & Strategies

- Cabot Corporation

- Global Graphene Group

- Grabat Graphenano Energy

- Graphene NanoChem

- Graphenea Group

- Huawei Technologies Co., Ltd.

- Hybrid Kinetic Group Ltd.

- Log 9 Materials Scientific Private Limited

- Nanotech Energy

- Nanotek Instruments, Inc.

- Samsung SDI

- Targray Group

- Vorbeck Materials Corp.

- XG Sciences, Inc.

- ZEN Graphene Solutions Ltd.

* List Not Exhaustive

Methodology

The Graphene Battery Market Report (2025–2034) utilizes a robust, multi-layered research methodology designed to deliver the most accurate and actionable market intelligence for industry stakeholders. The approach combines primary research (in-depth interviews with battery manufacturers, materials scientists, R&D leaders, and key executives) with secondary research (review of published reports, technical papers, regulatory filings, patent analysis, trade publications, and company presentations). Proprietary data modeling leverages historical market performance, real-time production and sales statistics, and scenario-based forecasting. Competitive analysis includes benchmarking of key players, new product launches, and recent investments, ensuring a holistic view of the global graphene battery landscape. Data triangulation and validation steps are rigorously applied to ensure findings are comprehensive, up-to-date, and trustworthy for strategic business decisions.

Research Coverage and Deliverables

Research Coverage:

- Global and regional market sizing, value, and volume forecasts (2025–2034)

- Segmentation by battery type (Lithium-ion Graphene Battery, Graphene Supercapacitor, Lithium Sulphur Graphene Battery, Others)

- Application analysis by sector (Automotive, Consumer Electronics, Power, Industrial Robotics, Aerospace & Defense, Healthcare)

- Country-level insights for 21 markets across North America, Europe, Asia Pacific, South America, and Middle East & Africa

- Competitive landscape: Profiles of 15+ leading companies, market share analysis, recent developments, and innovation strategies

- Analysis of production trends, raw material sourcing, supply chain dynamics, and cost trajectories

- Review of regulatory frameworks, IP landscape, and sustainability trends impacting the graphene battery sector

- Future outlook: Technology roadmaps, pilot projects, and disruptive innovation opportunities through 2034

Deliverables:

- Comprehensive PDF report (including charts, graphs, and tables)

- Executive summary and strategic recommendations

- Interactive Excel data workbook (market size, share, segmentation, company profiles)

- Access to proprietary USDAnalytics databases for further data queries

- Customization support: Tailored queries or segmentation upon request

- Analyst consultation for key findings and action points