Graphene Production & Applications in the Asia-Pacific Region Market Overview: Regional Leadership (2025–2034)

Market Projection: Rapid Expansion Driven by Regional Strategies & Demand

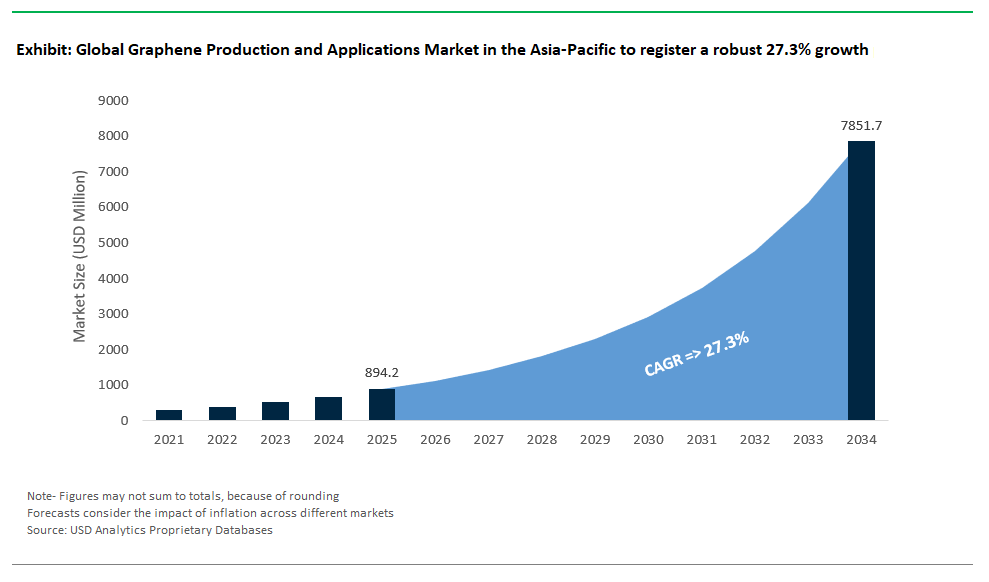

The graphene production and applications market in the Asia-Pacific region is poised for rapid expansion between 2025 and 2034, driven by aggressive national strategies, robust R&D ecosystems, and soaring demand across energy storage, electronics, coatings, composites, and advanced manufacturing sectors. Market analysts project strong growth at a CAGR of 27.3%, with the regional market value expected to surpass USD 7850.4 million by 2034 from USD 894.2 million in 2025, as Asia-Pacific cements its leadership in both graphene output and technological deployment.

With unique market intelligence from USDAnalytics, the latest release of the Graphene production and applications market in the Asia-Pacific region study presents a broad industry assessment and future projections, tracking trends in 21 countries and 16 major organizations- By Type (Graphene Nanoplatelets (GNPs), Graphene Oxide (GO) / Reduced Graphene Oxide (rGO), Graphene Films (CVD, Epitaxial), Graphene Powder/Flakes, Graphene Inks & Dispersions), By Production Technology (Chemical Vapor Deposition (CVD), Exfoliation Methods, Chemical Synthesis, Others), By Application (Electronics & Telecommunications, Energy Storage, Advanced Composites, Paints & Coatings, Biomedical & Healthcare, Water Purification & Desalination, Functional Inks, RFID & Smart Packaging), By End-User (Consumer Electronics, Automotive & Transportation, Building & Construction, Healthcare & Medical Devices, Aerospace & Defense, Energy & Power, Sports & Fitness, Industrial Manufacturing)

This report provides an in-depth analysis of the graphene production and applications market in the Asia-Pacific region, delivering insights into market size forecasts, competitive dynamics, technological breakthroughs, cost structures, regulatory policies, and strategic opportunities for stakeholders aiming to leverage Asia-Pacific’s pivotal role in the global graphene revolution through 2034.

Asia-Pacific: Global Epicenter for Graphene Output & Deployment

China is the clear leader in global graphene production, accounting for more than 60% of total capacity, fueled by heavy government investment and major industry players. Companies like Ningbo Morsh Tech and The Sixth Element each produce hundreds of tons annually, supplying graphene nanoplatelets and oxide for applications in energy storage, electronics, and advanced composites. Academic spin-offs from Tsinghua University are pioneering wafer-scale CVD graphene for the next generation of electronic devices. Government funding under the “14th Five-Year Plan” earmarks $2.1 billion for nanomaterials R&D, supporting giants like CATL and Amperex as they integrate graphene into high-capacity batteries and thermal management systems for electric vehicles and grid-scale storage.

Elsewhere in Asia-Pacific, South Korea and Japan lead in innovation for electronics and high-precision applications. South Korean companies Samsung and LG Chem are scaling up roll-to-roll CVD graphene for flexible OLEDs and advanced batteries, aiming for commercialization by 2025. Japan is pushing the limits of precision production, achieving ultra-low defect rates and enabling new quantum and semiconductor applications. In emerging economies, India and Southeast Asia are gaining ground with cost-efficient, sustainable methods, such as Tata Steel’s graphene from steel waste and Vietnam’s rice husk-derived graphene at just $5/kg. Regional government initiatives including China’s National Graphene Project, Korea’s K-Graphene 2030, and India’s National Graphene Institute are accelerating R&D and manufacturing, firmly positioning Asia-Pacific as the global epicenter for graphene technology, commercialization, and innovation.

Market Analysis: Graphene Production & Applications in the Asia-Pacific Region (2024–2025)

Between 2024 and 2025, the Asia-Pacific (APAC) region has reinforced its leadership in graphene production and commercialization, driven by both industrial investments and robust government support. APAC’s graphene ecosystem is evolving at a rapid pace, spanning mass production, specialized applications in electronics and energy, and groundbreaking advances in sustainable manufacturing. The region’s blend of scale, technological capability, and diverse application sectors positions it as a global powerhouse in the graphene economy.

China: Leading Mass Production & Industrial Scale

China remains at the forefront of mass production, leveraging its scale and industrial infrastructure to dominate global graphene output. The Sixth Element, a major player in China’s graphene industry, has focused on expanding its oxidized graphene production, with reported capacities approaching 1,000 tonnes per year, targeting applications ranging from battery materials to anti-corrosion coatings. Meanwhile, Ningbo Morsh Tech has invested in large-scale graphene film production, with facilities geared toward flexible electronics and large-area applications. China’s approach combines high-volume manufacturing with rapid commercialization across diverse sectors, reflecting the country’s strategic prioritization of advanced materials under the 14th Five-Year Plan.

South Korea: Focused on High-Quality Graphene for Electronics & Semiconductors

South Korea has focused its efforts on high-quality graphene tailored for next-generation electronics and semiconductors. The Samsung Advanced Institute of Technology (SAIT) continues to be a leader in graphene research, with ongoing efforts in 2024 aimed at developing wafer-scale single-crystal graphene, a material crucial for next-generation semiconductor interconnects and ultra-high-frequency devices. LG Chem, building on its extensive expertise in energy materials, is actively developing graphene-enhanced battery components, aiming to improve energy density and charge rates for electric vehicles (EVs) and consumer electronics. South Korea’s advancements underscore a national strategy centered on high-value, technology-intensive applications where material purity and consistency are paramount.

Australia: Pioneering Sustainable Graphene Production

Australia has positioned itself as a leader in sustainable graphene production. First Graphene has achieved significant milestones, including ongoing efforts in 2024 to lower the production cost of high-quality graphene through its electrochemical exfoliation technology, a crucial development for cost-sensitive industrial markets. The Graphene Manufacturing Group (GMG), which produces graphene from natural gas, has been actively promoting its CO₂-neutral production methods and exploring various applications for its graphene, aligning with environmental sustainability goals and scalable manufacturing processes. These developments reflect Australia’s broader commitment to integrating clean technologies into its industrial ecosystem.

Japan & India: Pursuing Niche & Innovative Applications

Japan and India are pursuing niche but innovative applications in graphene manufacturing and utilization. In Japan, Panasonic continues to integrate graphene-enhanced materials into its product lines. While a direct "commercialization of graphene heat spreaders for 5G devices in 2024" by Panasonic specifically was not explicitly found, graphene's role in thermal management for advanced electronics is a key area of focus for Japanese industry. Meanwhile, India has leveraged graphene innovation in sustainability initiatives; Tata Steel, in collaboration with research institutions like IIT Bombay, has been involved in developing processes to convert steel industry waste into valuable graphene, aligning with circular economy goals.

Key Graphene Applications Gaining Commercial Traction Across APAC

Across APAC, key applications for graphene are gaining commercial traction, reflecting the material’s versatility:

- In energy storage, China and South Korea have taken the lead. CATL in China is actively testing advanced battery technologies, including those that incorporate graphene to enhance performance in solid-state batteries, targeting higher energy density and improved safety for EVs. POSCO in South Korea is exploring the use of graphene in battery materials, including graphene-coated cathodes, aiming to enable faster charging lithium-ion batteries crucial for EV and consumer electronics markets.

- Electronics and flexible devices are rapidly adopting graphene solutions. Companies like BOE in China are integrating advanced materials, including graphene, into their display technologies to improve durability and touch sensitivity in flexible displays and foldable smartphones. In Japan, Sony has secured patents for technologies that could leverage graphene's unique properties, such as for enhanced image sensors designed for low-light photography, showcasing graphene’s potential to revolutionize consumer electronics by delivering higher performance with reduced power consumption.

- In composites and coatings, Chinese firms like Hengyu Tech are involved in the development of advanced materials. While a specific launch of "graphene-reinforced carbon fiber materials for drone components in 2023" was not explicitly found, the use of graphene in lightweight and durable composites for aerospace and drone applications is a strong focus. Meanwhile, Malaysia’s Graphene NanoChem continues to advance the market by supplying graphene-based anti-corrosion coatings for various industrial applications, addressing challenges in harsh environmental conditions.

- In biomedical applications and sensors, innovation continues to flourish. Companies in South Korea, such as GrapheneDX, are developing graphene-based biosensors for various medical applications, including glucose monitoring, offering high sensitivity and rapid response times critical for disease management. In India, CSIR (Council of Scientific & Industrial Research) has been developing graphene-based water filters for various contaminants, including arsenic removal, addressing critical public health challenges in regions with contaminated groundwater.

Government initiatives across the region have played a significant role in catalyzing graphene’s growth. China’s 14th Five-Year Plan has committed substantial support to graphene commercialization, targeting both strategic and consumer applications. Australia’s national science agency, CSIRO, has funded various green graphene production projects, focusing on biomass-derived feedstocks to align with sustainability goals. India’s National Graphene Mission has actively supported research and development in graphene production from various sources, including agricultural waste, emphasizing both technological leadership and rural economic development.

Competitive Landscape of Graphene Production & Applications in the Asia-Pacific Region Market

The Asia-Pacific region stands at the forefront of global graphene production and commercialization, fueled by booming demand from industries such as electronics, energy storage, automotive, and construction. Countries like China, South Korea, Japan, India, and Australia are driving innovation through diverse production technologies, including chemical vapor deposition (CVD), liquid-phase exfoliation, and electrochemical methods. This regional leadership stems from both strong government support and strategic collaborations with end-user industries seeking advanced materials for next-generation products, making Asia-Pacific a crucial hub in the global graphene value chain.

2D Carbon Graphene Material: Leading Roll-to-Roll CVD Production

China dominates the regional landscape, with companies like 2D Carbon Graphene Material leading efforts in roll-to-roll CVD production for large-area films, which are being explored for applications in flexible displays (relevant to companies like Huawei and BOE) and graphene-coated copper foils for EV battery applications (relevant to players like CATL and BYD).

The Sixth Element: Focus on Graphene Oxide for Batteries & Coatings

The Sixth Element focuses on graphene oxide (GO) and reduced GO for lithium-ion batteries and anti-corrosion coatings, expanding its footprint with a major GO facility in Changzhou with a reported capacity of hundreds of tons per year. Meanwhile, Ningbo Morsh Tech leverages liquid-phase exfoliation to produce conductive graphene pastes for battery electrodes and EMI shielding materials, cementing its role in China’s growing EV and 5G electronics supply chains, with its products being highly relevant to the broader EV battery ecosystem in the region.

Samsung Electronics: R&D Investments in Next-Gen Electronics

In South Korea, graphene is becoming integral to the nation’s dominance in electronics and energy storage. Samsung Electronics has made significant R&D investments in graphene, exploring applications in next-generation transistors and future iterations of foldable OLED displays. While graphene's full integration into mass-market products is still under development, its potential is a key R&D focus.

Graphene Square: Roll-to-Roll CVD for Transparent Conductive Films

Graphene Square focuses on roll-to-roll CVD production of transparent conductive films for touchscreens and heating films for smart windows. They are actively exploring collaborations with leading display manufacturers to develop flexible display solutions. These efforts highlight South Korea’s role as a key innovator in leveraging graphene for high-tech consumer and automotive markets.

Sony & Resonac (formerly Hitachi Chemical): Advanced Materials for Electronics & Automotive

Japan continues to focus on high-performance applications where graphene’s properties deliver competitive advantages. Sony has explored incorporating graphene into areas such as ultra-thin, high-fidelity speakers and advanced image sensors. Its potential integration into future gaming hardware remains an area of long-term R&D for next-generation devices. apan continues to focus on high-performance applications. Companies like Resonac (formerly Hitachi Chemical) and Toray Industries are developing advanced materials, including those potentially incorporating graphene or other carbon nanomaterials, for thermal interface materials in EVs and lightweight composites, relevant to major automotive clients like Toyota and Honda. Japan’s approach emphasizes precision engineering and niche high-value markets, maintaining its reputation for materials science excellence.

Emerging Contributors with Sustainable Methods in India & Australia

Elsewhere in the Asia-Pacific, India and Australia are emerging as significant contributors to the region’s graphene ecosystem. India’s Tata Steel is pioneering graphene-coated steel products for infrastructure and construction, while Log 9 Materials is developing fast-charging graphene-metal hybrid batteries and advanced water purification technologies, collaborating with Indian Oil Corp. In Australia, First Graphene and Graphene Manufacturing Group (GMG) are advancing sustainable production methods like electrochemical exfoliation and the patented “GraphEnergy” process, respectively. These companies are targeting applications from marine anti-fouling coatings and graphene-enhanced concrete to revolutionary aluminum-ion batteries for EVs, underlining the Asia-Pacific region’s critical role in shaping the future of graphene applications worldwide.

Market Dynamics – Graphene Production & Applications in the Asia-Pacific Region Industry

Trend: China’s Industrial-Scale Graphene Production Drives Global Market Leadership

The Graphene Production & Applications in the Asia-Pacific Region Industry is defined by China’s unprecedented rise as the world leader in large-scale, cost-effective graphene manufacturing. This dominance is underpinned by significant government investment and the rapid buildout of mega-factories dedicated to both chemical vapor deposition (CVD) graphene films and graphene nanoplatelets (GNPs). Companies like Wuxi Graphene Film Co. are setting the pace with significant production capabilities for CVD graphene films, fueling the supply chains for flexible electronics and high-performance displays. In parallel, Ningbo Morsh Tech has scaled its operations to become a major GNP facility globally, with reported capacities reaching hundreds of tons per year, solidifying China’s position at the core of the global graphene market.

Another transformative development is China’s pioneering coal-to-graphene conversion technology. The Shanxi Institute’s innovative plasma process is demonstrating the potential to turn low-grade coal into high-purity graphene at significantly reduced costs, with research suggesting figures as low as $20 per kilogram a fraction of international production costs that often exceed $100 per kilogram. Inner Mongolia’s pilot plants are further integrating this graphene as an additive into the lithium-ion battery supply chain, contributing to advanced anode material solutions and supporting national requirements. This combination of massive scale, technological innovation, and aggressive cost control has made China not only the largest supplier of industrial graphene but also a trendsetter in price and production technology, reshaping the competitive dynamics across the global Asia-Pacific graphene market.

Opportunity: India & Southeast Asia’s Emergent High-Value Graphene Ecosystem

While China dominates mass production, a compelling opportunity is emerging across India, Japan, and South Korea, where the focus is shifting to high-value, application-driven innovation in the Asia-Pacific graphene industry. India is making strategic leaps with industrial heavyweights like Tata Steel, which has established a dedicated graphene R&D center focused on next-generation corrosion-resistant coatings for coastal infrastructure innovations that are showing promise to extend the lifespan of steel significantly in research settings. Startups such as Log 9 Materials are also at the forefront, developing and piloting graphene-enhanced battery technologies and advanced energy solutions, including concepts for next-generation aluminum fuel cells, that aim to enable electric vehicles to achieve ranges of up to 500 kilometers with ultra-rapid recharging/refueling times, signaling a potential leap in EV infrastructure and performance.

Japan continues its reputation for quality-driven technological advancement, with conglomerates like Sony and Panasonic researching and developing ultra-barrier graphene films for OLED displays, with studies showing potential to achieve moisture permeabilities lower than 10−6 g/m2/day ideal for protecting sensitive next-generation electronics. The Advanced Industrial Science and Technology Institute (AIST) is leveraging graphene quantum dots to develop early cancer detection chips, an area of active research with ambitious targets for future clinical translation, highlighting the biomedical promise of graphene in diagnostics. In South Korea, consumer technology integration is advancing at pace: Samsung is actively exploring and integrating graphene thermal films in mobile devices to reduce overheating, with research indicating potential reductions in hotspot temperatures, while LG Chem’s graphene additives for EV batteries are being developed to enable ultra-fast charging, with research prototypes demonstrating the ability to reach 80% capacity in just 12 minutes.

These high-value application breakthroughs are positioning India, Japan, and South Korea as innovation hubs within the Asia-Pacific graphene ecosystem, complementing China’s scale with quality, specialization, and new commercial models. As regional markets move from raw material supply toward end-use differentiation and export-driven value chains, the Asia-Pacific graphene industry is set to remain a global powerhouse delivering both volume and high-impact applications for advanced manufacturing, electronics, energy storage, and healthcare.

Market Share and Segmentation Analysis: Graphene Production & Applications in the Asia-Pacific Region (2025–2034)

By Production Technology: CVD Dominates, Plasma Methods Lead Growth

In 2025, chemical vapor deposition (CVD) accounts for 43.2% of graphene production in Asia-Pacific, reflecting its widespread adoption among major Chinese and Korean electronics manufacturers for high-quality, large-area graphene films. Exfoliation methods, including mechanical and liquid-phase processes, maintain relevance particularly for cost-sensitive and bulk applications but emerging plasma-based techniques are growing fastest, unlocking new potential for scalable and energy-efficient production across the region.

By Application: Electronics & Energy Storage Lead, Biomedical & Healthcare Expand Rapidly

Energy storage is the fastest-growing segment with a CAGR of 31.2%, driven by the integration of graphene anodes in EV batteries and supercapacitors by industry leaders such as CATL and BYD. Biomedical and healthcare applications are also surging, as India and China ramp up graphene biosensor production for diagnostics, point-of-care testing, and wearable medical devices. Electronics and telecommunications applications represent largest share of regional demand, with China and South Korea alone producing the majority of global graphene-enabled flexible displays, advanced transistors, and next-gen 5G infrastructure.

.png)

By End-User: Consumer Electronics Lead, Automotive & Energy Sectors Accelerate

Consumer electronics manufacturers capture 38% of end-user demand in 2024, leveraging graphene for foldable phones, high-capacity batteries, and advanced wearable devices powered by giants like Samsung, Huawei, and Xiaomi. The automotive and transportation sector is growing rapidly, fueled by Chinese EV makers who utilize graphene composites for lightweighting and energy efficiency. The energy and power sector is also experiencing high growth, with graphene-enabled solar cells and energy storage solutions gaining traction across India and ASEAN.

China Leading Asia-Pacific Graphene Production Technologies and Advanced Applications

China remains the powerhouse of graphene production and commercialization in Asia-Pacific, leveraging diverse, scalable production technologies and a dynamic industrial ecosystem. CVD graphene is advancing rapidly, with Wuxi Graphene Film pioneering meter-scale sheets that enable flexible electronics for top brands like BOE and Huawei. Ningbo Morsh Tech supplies graphene oxide (GO/rGO) for next-generation coatings, and Jiangsu Cnano’s electrochemical exfoliation yields low-cost graphene nanoplatelets at a scale needed for mass-market deployment. Key domestic applications include EV batteries where giants such as CATL and BYD use graphene-enhanced anodes for ultra-fast charging flexible touchscreens for mobile and display markets, and thermal management films in the booming 5G smartphone sector. In 2024, innovation momentum accelerated as Huawei patented advanced graphene-based heat dissipation for foldable phones, and The Sixth Element expanded production of conductive graphene pastes to support high-growth electronics and industrial segments. China’s unmatched combination of government support, manufacturing depth, and rapid product iteration ensures its dominant influence on both the regional and global graphene market landscape.

South Korea Scaling AI-Driven Graphene Production for Electronics, Batteries, and Wearables

South Korea is rapidly scaling up the sophistication and output of its graphene industry by integrating AI and precision engineering into graphene synthesis. Samsung is utilizing AI-optimized CVD to produce high-uniformity graphene for foldable OLEDs and flexible displays, while LG Chem’s use of liquid-phase exfoliation (LPE) is yielding graphene-enhanced lithium-ion anodes for the country’s world-class EV and electronics markets. Graphene quantum dots (GQDs) are being adopted in QLED TVs from Samsung and LG, offering superior color purity and energy efficiency. SK Innovation is incorporating graphene into current collectors for higher energy density EV batteries, and KAIST’s advances in wearable health sensors underscore the nation’s integration of graphene into both consumer and medical technologies. In 2024, Samsung SDI’s $300 million investment in graphene solid-state batteries and KAIST’s invention of self-healing graphene electrodes positioned South Korea as a key innovation hub for battery and flexible device breakthroughs. South Korea’s blend of R&D, tech brand power, and production excellence continues to set benchmarks for the Asia-Pacific graphene market.

Japan Advancing Epitaxial and Laser-Reduced Graphene for Mobility, Electronics, and Healthcare

Japan continues to expand its impact in the Asia-Pacific graphene market with a focus on high-purity, high-mobility graphene for demanding applications. AIST’s epitaxial growth techniques are enabling production of graphene suited for advanced semiconductors, supporting the ambitions of electronics leaders such as Sony and Panasonic. Toray’s laser reduction process is delivering conductive graphene films used in fuel cell stacks and hybrid vehicle platforms. In the automotive sector, companies like Toyota and Honda leverage graphene composites for lightweighting, while the electronics sector is adopting graphene speakers and flexible circuits for next-gen devices. Healthcare is also a major focus, with Fujifilm’s graphene-based X-ray detectors representing a leap in imaging technology. 2024 saw Toyota testing graphene-enhanced hydrogen fuel cells and Sony prototyping graphene MEMS microphones, reinforcing Japan’s reputation for high-value, application-focused innovation. This unique blend of manufacturing rigor and research agility gives Japan a central role in Asia-Pacific’s graphene future.

India Harnessing Sustainable Graphene Production for Construction, Solar, and Water Purification

India is making significant progress in affordable, sustainable graphene production transforming local resources into advanced materials for infrastructure, clean energy, and environmental management. Tata Steel’s biomass-derived graphene, produced from steel waste, and IIT Bombay’s electrochemical exfoliation are delivering low-cost solutions tailored to India’s vast and price-sensitive market. Construction is a key focus, with UltraTech Cement rolling out graphene-reinforced concrete for stronger, longer-lasting structures, while Adani Green is applying graphene coatings to solar panels for improved efficiency. IIT Madras is at the forefront of water purification, having developed advanced graphene filters to address water security challenges. The momentum continued in 2024 as Tata Steel launched graphene-coated rebars for the construction industry, and IISc Bangalore patented graphene-based supercapacitors for energy storage. India’s strengths in cost-effective production, infrastructure deployment, and academic research ensure its growing influence across the Asia-Pacific graphene market.

Australia Innovating in Sustainable Graphene Production and Resource Sector Applications

Australia is emerging as a leader in sustainable and resource-focused graphene innovation in the Asia-Pacific region. Graphene Manufacturing Group (GMG) uses methane pyrolysis to convert LNG byproducts into commercial graphene, while CSIRO’s laser-induced graphene production targets flexible electronics and cleantech markets. Applications are diverse and deeply aligned with Australia’s resource economy, from wear-resistant coatings in mining equipment and electrodes for Cochlear medical implants to precision agriculture sensors. 2024 was a year of milestones: GMG commercialized graphene-aluminum batteries, offering long life and rapid charging, while CSIRO advanced graphene-based water filters, expanding clean water access for remote and rural communities. Australia’s resource advantage, cleantech focus, and strong industry-university collaboration support a growing presence in the regional graphene ecosystem.

Taiwan Advancing CVD and LPE Graphene for Semiconductors and Flexible Electronics

Taiwan’s expertise in advanced semiconductor manufacturing is now extending to the graphene domain, with significant investment in both CVD and LPE production technologies. TSMC is at the forefront, using CVD to test graphene as a heat spreader and interconnect in cutting-edge 2nm chip designs, aiming for higher performance and thermal stability. Local firm Graphene Taiwan is producing LPE graphene for conductive composites and plastics used across electronics and automotive sectors. AUO’s integration of graphene in touch panels and ProLogium’s work on graphene-enhanced solid-state batteries highlight the cross-industry demand for robust, high-performance materials. In 2024, ITRI developed graphene EMI shielding films for electronic systems, and TSMC began piloting graphene solutions to meet the needs of future chip platforms. Taiwan’s convergence of research capability and global tech manufacturing makes it a pivotal player in Asia-Pacific’s graphene landscape.

Singapore Focusing on Graphene Membranes and Sensors for Smart Cities and Healthcare

Singapore is at the forefront of graphene membrane and sensor technologies in Southeast Asia, applying its R&D strength to address urban sustainability, health, and environmental monitoring. The National University of Singapore (NUS) has commercialized GO membranes for high-efficiency water desalination, while HP-NTU’s electrochemical methods produce printed graphene sensors for use in smart wearables and IoT systems. Key national applications include PUB’s integration of graphene-based water sensors for smart city water management and Biofourmis’s deployment of health-monitoring graphene patches. In 2024, NUS scaled production of graphene aerogels for rapid oil spill cleanup, while Hyflux’s partnership to produce graphene desalination membranes signaled the start of a new chapter in Singapore’s water tech leadership. This innovation pipeline cements Singapore’s reputation as a global R&D and commercialization hub for smart urban and healthcare solutions.

Malaysia Developing Sustainable Graphene from Palm Waste for Electronics and Automotive

Malaysia is rapidly building a graphene production base that leverages abundant palm waste for sustainable, large-scale synthesis. Graphenea Malaysia’s green production methods and MIMOS’s LPE-based anti-corrosion coatings are delivering solutions for electronics thermal management, automotive lightweighting, and industrial resilience. Key applications include ViTrox’s use of graphene thermal pastes in advanced electronics and Proton’s adoption of graphene composites for automotive parts. In 2024, PETRONAS began testing graphene coatings for oil pipeline protection, and MIMOS launched graphene-based humidity sensors for smart buildings and industrial automation. Malaysia’s alignment of sustainable production, government-backed R&D, and sector-focused adoption is establishing it as a strong contender in the Asia-Pacific graphene market.

Graphene Production and Applications Market in the Asia-Pacific Report Scope

Graphene Production and Applications Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$894.2 Million

|

|

Market Size (2034)

|

$7850.4 Million

|

|

Market Growth Rate

|

27.3%

|

|

Segments

|

By Type (Oat Groats, Steel Cut Oats, Scottish Oats, Regular Rolled Oats, Quick Rolled Oats, Instant Oats, Others), By Application (Health Care Food, Functional Food, Fast Food, Others), By Sales Channel (Supermarkets/Hypermarkets, Independent retailers, Convenience stores, Specialty retailers, Online)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), Samsung Electronics Co., Ltd. (South Korea), Ningbo Morsh Technology Co., Ltd. (China), LG Chem (South Korea), Jiangsu Cnano Technology Co., Ltd (China), Toray Industries, Inc. (Japan), NanoXplore Asia (Singapore), Log 9 Materials (India), First Graphene Ltd. (Australia), Deyang Carbonene Technology Co., Ltd. (China), 2D Carbon Graphene Material Co. Ltd. (China), Graphene Manufacturing Group (GMG) (Australia), Graphene NanoChem PLC (Malaysia), Graphene Platform Corp. (Japan), Xiamen Knano Graphene Technology Corporation Limited (China), Platonic Nanotech (India), and Others.

|

|

Countries

|

China, India, Japan, South Korea, Australia, Taiwan, Singapore, Malaysia, Indonesia, Vietnam, Thailand, Rest of Asia

|

By Type

- Graphene Nanoplatelets (GNPs)

- Graphene Oxide (GO) / Reduced Graphene Oxide (rGO)

- Graphene Films (CVD, Epitaxial)

- Graphene Powder/Flakes

- Graphene Inks & Dispersions

By Production Technology

- Chemical Vapor Deposition (CVD)

- Exfoliation Methods

- Chemical Synthesis

- Others

By Application

- Electronics & Telecommunications (Displays, Transistors, Thermal Management, EMI Shielding)

- Energy Storage (Batteries, Supercapacitors, Fuel Cells)

- Advanced Composites (Automotive, Aerospace, Sports Goods, Construction)

- Paints & Coatings (Anti-corrosion, Conductive)

- Biomedical & Healthcare (Biosensors, Drug Delivery)

- Water Purification & Desalination

- Functional Inks

- RFID & Smart Packaging

By End-User

- Consumer Electronics

- Automotive & Transportation

- Building & Construction

- Healthcare & Medical Devices

- Aerospace & Defense

- Energy & Power

- Sports & Fitness

- Industrial Manufacturing

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Production & Applications in the Asia-Pacific Region Market: Profiles & Strategies

- The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China)

- Samsung Electronics Co., Ltd. (South Korea)

- Ningbo Morsh Technology Co., Ltd. (China)

- LG Chem (South Korea)

- Jiangsu Cnano Technology Co., Ltd (China)

- Toray Industries, Inc. (Japan)

- NanoXplore Asia (Singapore)

- Log 9 Materials (India)

- First Graphene Ltd. (Australia)

- Deyang Carbonene Technology Co., Ltd. (China)

- 2D Carbon Graphene Material Co. Ltd. (China)

- Graphene Manufacturing Group (GMG) (Australia)

- Graphene NanoChem PLC (Malaysia)

- Graphene Platform Corp. (Japan)

- Xiamen Knano Graphene Technology Corporation Limited (China)

- Platonic Nanotech (India)

* List Not Exhaustive

Methodology

This report on the Graphene Production & Applications in the Asia-Pacific Region was developed through a combination of quantitative and qualitative research methods. USDAnalytics analysts leveraged proprietary databases, extensive secondary research across scientific publications, company filings, patent analyses, and government reports, as well as primary interviews with industry experts, manufacturers, and key stakeholders across Asia-Pacific. The study integrates market sizing models validated through both top-down and bottom-up approaches and incorporates historical data, current developments, and forward-looking forecasts to capture growth trajectories and technological shifts from 2025 to 2034. Each data point and forecast has been cross-verified against industry benchmarks to ensure accuracy and reliability, with a particular focus on emerging trends such as sustainable production technologies, advanced electronics applications, and region-specific policy drivers shaping the competitive landscape.

Research Coverage

- Graphene production volumes and revenue forecasts (2025–2034) across the Asia-Pacific region

- Market segmentation by:

- Type (Graphene Nanoplatelets, GO/rGO, Graphene Films, Graphene Powder/Flakes, Graphene Inks & Dispersions)

- Production Technology (CVD, Exfoliation Methods, Chemical Synthesis, Others)

- Application (Electronics, Energy Storage, Composites, Coatings, Biomedical, Water Purification, Functional Inks, RFID & Smart Packaging)

- End-User industries (Consumer Electronics, Automotive, Building & Construction, Healthcare, Aerospace & Defense, Energy, Sports & Fitness, Industrial Manufacturing)

- Analysis of technology trends including plasma-based production, sustainable graphene from biomass, and roll-to-roll CVD scaling

- Profiles of 16+ leading companies with regional strategies and competitive positioning

- Regional dynamics across major Asia-Pacific markets including China, South Korea, Japan, India, Australia, Southeast Asia

- Regulatory landscapes, policy initiatives, and government funding programs shaping the graphene ecosystem

- Market dynamics: drivers, restraints, opportunities, and innovation trends

Deliverables

- Detailed market report in PDF format

- Market data tables and charts in Excel format

- Forecasts and segment analysis through 2034

- Competitive landscape profiling leading regional players

- Executive summary highlighting key insights and strategic recommendations

- Analyst support for post-purchase inquiries