Graphene Sheets Market Overview: Propelling Next-Generation Materials (2025–2034)

Market Projection: Robust Growth Driven by Demand for Ultra-Thin, High-Performance Materials

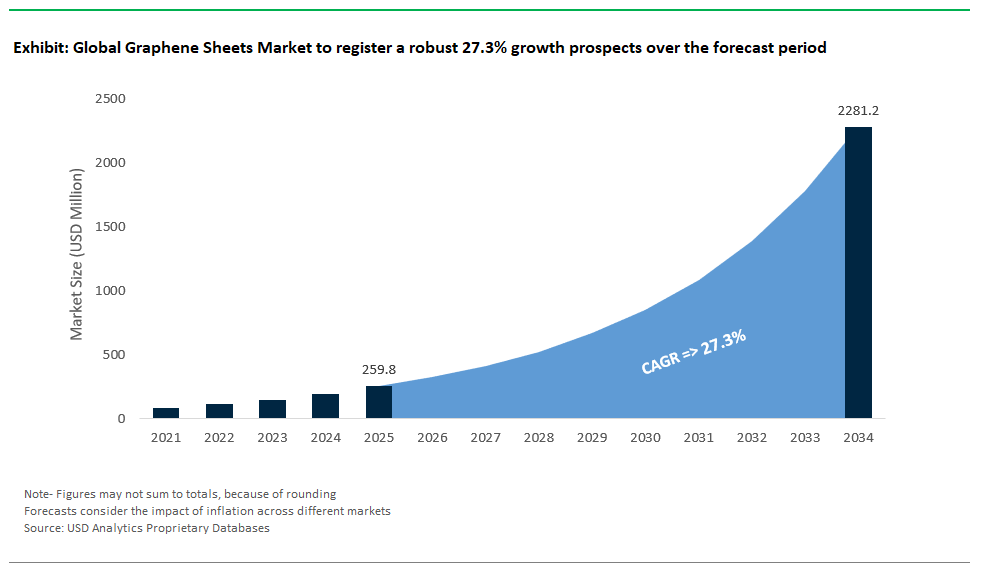

The graphene sheets market is set for significant growth between 2025 and 2034, driven by soaring demand across electronics, aerospace, energy, biomedical, and advanced manufacturing sectors seeking ultra-thin, high-performance materials. Market analysts forecast robust expansion at a CAGR of 27.3%, with total market value expected to exceed USD 2280.8 million by 2034 from USD 259.8 million in 2025, as industries harness graphene sheets’ unique properties to unlock applications far beyond the capabilities of traditional metals, polymers, and conductive films.

Leveraging exclusive data compiled by USDAnalytics, this current edition of the Graphene sheets report provides an in-depth overview and forward-looking assessment of the graphene Sheets market across 21 nations and 17 leading companies- By Type (Monolayer Graphene, Bilayer Graphene, Few-Layer Graphene, Multilayer Graphene Sheets), By Application (Electronics, Energy Storage, Composites, Thermal Management, Sensors & Biomedical), By Production Method (Chemical Vapor Deposition (CVD) Graphene, Liquid-Phase Exfoliation (LPE) Graphene Sheets, Thermal Exfoliation Graphene Sheets, Graphene Oxide (GO) Sheets, Silicon Carbide (SiC) Sublimation), By End-user (Automotive & Transportation, Aerospace & Defense, Electronics, Consumer Goods, Healthcare, Others)

This report delivers a comprehensive analysis of the graphene sheets market, providing insights into market size forecasts, competitive dynamics, technological developments, manufacturing economics, regulatory landscapes, and strategic opportunities for stakeholders seeking to capitalize on graphene’s transformative potential across diverse sectors through 2034.

Exceptional Properties of Graphene Sheets: Strength, Conductivity & Transparency

Graphene sheets are distinguished by their extraordinary properties, including a single-atom thickness of 0.34 nm, an intrinsic tensile strength of 130 GPa stronger than steel and in-plane electrical conductivity up to 10⁸ S/m, which is about six times higher than copper. These sheets also exhibit thermal conductivity levels that can surpass diamond by up to tenfold and boast exceptional optical transparency at 97.7%, exceeding the performance of standard ITO glass. These combined strengths make graphene sheets highly sought after for applications requiring superior strength-to-weight ratios, excellent electrical performance, and advanced heat management. Market segmentation highlights the use of chemical vapor deposition (CVD) for producing high-quality, electronics-grade sheets, while liquid-phase exfoliation (LPE) offers scalable, lower-cost options for structural uses. High-purity epitaxial growth targets semiconductor and quantum applications, but challenges remain in controlling defects and achieving uniformity at scale, which are crucial for commercial viability.

Commercially, graphene sheets are making significant inroads in electronics, aerospace, and biomedicine. Companies like Samsung are exploring their use in flexible displays for improved transparency and conductivity. In aerospace, graphene-polyimide composites are being developed for applications such as lightning strike protection and thermal management in advanced aircraft and space telescopes, though these are not yet in production for flagship projects. Biomedical applications include neural interfaces with ultra-thin graphene layers capable of single-neuron recording and barrier-grade graphene for pharmaceutical packaging with near-zero oxygen permeability. Innovations like graphene-based Hall sensors and quantum devices are setting new performance benchmarks, with scalable manufacturing improvements steadily reducing costs. These advances are positioning graphene sheets as a transformative material for next-generation high-performance industries.

Market Analysis: Graphene Sheets Innovations & Commercialization (2024–2025)

Between 2024 and 2025, the graphene sheets market has emerged as one of the most dynamic and strategically significant segments within the broader graphene industry. Driven by advances in manufacturing scalability, diverse commercial applications, and breakthrough research, graphene sheets are increasingly being integrated into next-generation electronics, energy storage devices, thermal management solutions, and high-performance materials for aerospace and automotive applications. The period has been marked by significant milestones, signaling that large-area, high-quality graphene sheets are transitioning from niche research materials to commercially viable industrial products.

Electronics & Flexible Devices: Enabling High-Performance, Ultra-Thin Technologies

In electronics and flexible devices, graphene sheets are emerging as a critical enabler of high-performance, ultra-thin, and flexible technologies. Leading display manufacturers like Samsung in South Korea are actively researching and advancing technologies for improved thermal management in foldable OLED displays, a key technical hurdle for their widespread adoption and high-power operation. This innovation represents a significant leap for flexible electronics, where thermal management remains one of the key technical hurdles. Meanwhile, Graphenea in Spain continues to be a key provider of wafer-scale graphene sheets, consistently offering high-quality materials for semiconductor research and development. Their foundry services, available prior to and through 2023, cater to the demanding requirements of advanced chip manufacturing processes and high-speed electronic devices.

Energy Storage: Powering Next-Generation Batteries & Supercapacitors

Energy storage has emerged as another significant commercial frontier for graphene sheets. Talga Group, operating across Australia and Sweden, continues to advance its graphene-enhanced anode materials for lithium-ion batteries. Their ongoing development, highlighted in 2024, aims to leverage graphene’s electrical conductivity to reduce internal resistance, thereby enhancing battery energy density and charging performance in anodes. In 2023, Skeleton Technologies in Estonia scaled production of its proprietary 'Curved Graphene' material for use in its SuperBattery product. This innovative technology, which blends characteristics of supercapacitors and batteries, achieves high power densities and fast charge rates, underscoring graphene's pivotal role in enabling next-generation energy storage systems that demand both high power and rapid charge-discharge capabilities.

Thermal Management: Revolutionizing Heat Dissipation

The thermal management segment has seen particularly strong momentum, with graphene sheets finding applications in everything from electric vehicles to telecommunications infrastructure. Companies like Graphmatech in Sweden are actively developing graphene sheet-based thermal interface materials (TIMs) for demanding applications, including electric vehicle (EV) power systems where managing high thermal loads is critical for performance and safety, with advancements ongoing in 2024. In the United States, companies like Vorbeck Materials are developing graphene-enhanced solutions for thermal management. Their expertise in graphene materials and conductive components is highly relevant for applications such as heat spreaders in demanding electronics like 5G base stations, which face significant heat management challenges due to the density and power demands of modern telecom hardware.

Manufacturing Expansions & Production Refinements (2024-2025)

Manufacturing expansions between 2024 and 2025 reflect growing confidence in commercial demand and technological readiness. Companies like First Graphene in Australia are continually refining their production processes, including electrochemical exfoliation, to improve the yield and quality of graphene sheets. These advancements are crucial for enabling consistent production for high-performance industrial applications. Similarly, NanoXplore in Canada announced significant plans in 2023 to expand its graphene production capacity, aiming to reach 20,000 tonnes per year by 2027. This ambitious expansion, with investments commencing in 2023, is positioning the company to supply large-scale orders for various industries, including automotive and aerospace customers eager to integrate graphene’s properties into lightweight structural and functional components.

Research Breakthroughs: Pushing Boundaries in Manufacturing & Performance

Research breakthroughs during this period have pushed the technical boundaries of graphene sheet manufacturing and performance. Leading institutions, including MIT in the United States, are making significant strides in developing scalable methods like roll-to-roll chemical vapor deposition (CVD) for producing high-quality, large-area graphene sheets, with ongoing advancements in 2024 critical for cost-effective integration into commercial electronics. The University of Manchester, a global leader in graphene research, continued to set new benchmarks in 2023 by achieving exceptionally high thermal conductivity values in highly aligned graphene sheets. These advancements, which far surpass traditional materials like copper, are opening new opportunities for extreme heat dissipation applications. Meanwhile, research institutions globally, including the National University of Singapore (NUS), are exploring advanced applications for graphene sheets. Ongoing research in areas like ultra-light graphene materials and their unique properties, with advancements in 2024, signals graphene’s potential entry into specialized markets such as space-grade radiation shielding, where weight and radiation resistance are paramount.

Strategic Partnerships & Collaborations: Driving Real-World Deployment

Partnerships and collaborations have become instrumental in propelling graphene sheets toward real-world deployment. Major automotive players like Tesla are continually seeking advanced thermal management solutions for high-performance electric vehicle battery packs, and leading graphene producers are exploring collaborations to integrate graphene sheet-based technologies to enhance battery cooling systems. In the defense sector, collaborations are ongoing to explore the use of advanced materials like graphene sheets for stealth coatings. Companies such as Lockheed Martin and specialized graphene material providers are investigating how graphene’s unique electrical and mechanical properties can be leveraged to reduce radar signatures while maintaining lightweight characteristics in military platforms.

Competitive Landscape of the Graphene Sheets Market

The graphene sheets market stands at the forefront of advanced materials innovation, driven by rising demand for ultra-thin, high-performance films across sectors including electronics, energy, automotive, and flexible devices. Single-layer and few-layer graphene sheets produced via chemical vapor deposition (CVD), exfoliation, or reduction techniques offer unmatched electrical conductivity, thermal management, and mechanical strength. As industries seek to integrate graphene sheets into transparent conductive films, sensors, quantum devices, and thermal solutions, manufacturers worldwide are competing to achieve scalable, defect-free, and cost-effective production processes.

North American Leaders in CVD & Exfoliated Graphene Sheets

In North America, Grolltex is a prominent player, specializing in single-layer, defect-free CVD graphene sheets for both research and commercial applications. Grolltex provides high-quality graphene sheets and films to organizations exploring applications in flexible electronics, OLED displays, and biomedical sensors, while advancing roll-to-roll (R2R) production techniques to scale sheet manufacturing. Meanwhile, ACS Material offers a diverse portfolio of monolayer and few-layer graphene sheets, along with graphene oxide films for filtration and energy storage. As a major supplier to universities and tech startups, ACS Material bridges research and commercial deployment, exploring applications in water purification membranes and supercapacitors.

European & Transatlantic Innovators

Europe and North America’s Graphenea has carved a niche as a major supplier of CVD graphene films on copper, SiO₂, and PET substrates, catering extensively to research institutions and semiconductor partners working on next-generation electronics. Their expertise extends into flexible circuits, photodetectors, and thermal interface materials, supporting innovations in both electronics and energy storage. IChem is integrating graphenered the production of large-scale graphene sheets in wafer formats up to 8 inches, enabling advancements in applications such as quantum computing, high-performance Hall-effect sensors, and graphene-based medical diagnostics. Paragraf’s engagements with leading tech firms, including projects with companies relevant to future semiconductor and sensing technologies, underscore the integral role graphene sheets are poised to play.

Asia-Pacific & Other Key Commercializers

China plays a significant role in driving industrial-scale adoption. 2D Carbon Graphene Material is a leading producer of large-area graphene sheets, with applications including transparent electrodes for smart windows and heaters. They are also actively involved in supplying materials for battery electrodes, particularly for EV applications. SixCarbon Technology focuses on high-conductivity graphene sheets for thermal management in applications such as 5G devices, EV battery cooling, and wearable heating, positioning itself to support major tech companies in these areas. Meanwhile, US-based Vorbeck Materials specializes in flexible graphene sheets for printed electronics, RFID tags, and wearable sensors, collaborating with industry leaders such as BASF and Henkel. In Canada, NanoXplore integrates graphene powder and masterbatches into composite reinforcement and thermoplastic solutions for aerospace and automotive lightweighting. They are supplying their graphene-enhanced materials to major players and are scaling production to meet rising demand for advanced EV battery components.

Market Dynamics – Graphene Sheets Industry: Key Trends & Opportunities (2025–2034)

Trend: Large-Area, Defect-Free Graphene Sheets Drive Next-Generation Electronics

The Graphene Sheets Industry is on the cusp of a technological revolution as breakthroughs in the production of large-area, defect-free graphene sheets are unlocking transformative opportunities in advanced electronics. Recent advances in roll-to-roll chemical vapor deposition (CVD) are advancing towards the manufacture of meter-scale, single-crystal graphene sheets that combine ultra-low defect density with exceptional electrical and optical performance. For example, transparent conductive electrodes fabricated from CVD graphene are outperforming conventional indium tin oxide (ITO) by delivering sheet resistances below 50 ohms per square at 90% transparency, along with mechanical flexibility that endures over 100,000 bending cycles a sharp contrast to ITO’s limited endurance below 1,000 bends. These superior properties are enabling new generations of flexible displays, with Samsung and other leading display manufacturers actively researching and developing graphene anodes to achieve pixel densities exceeding 1,000 pixels per inch (PPI) in future QD-OLED technologies.

Beyond display technology, the quantum computing sector is exploring the potential of wafer-scale graphene sheets with defect rates below 0.01% as a prerequisite for next-generation topological qubit platforms, an area of active research by entities such as Microsoft's Quantum program. These high-purity sheets are also critical for the fabrication of ultra-low-noise quantum sensors, with research demonstrating spatial resolutions down to 0.1 nanometers in specialized configurations. Collectively, these innovations underscore the pivotal role of defect-free, large-area graphene sheets in shaping the future of flexible, high-performance, and quantum electronics, positioning the Graphene Sheets Market as a central driver of electronics miniaturization and reliability.

Opportunity: Graphene Thermal Interface Materials Revolutionize 3D Chip Packaging

A major opportunity for growth in the Graphene Sheets Market is emerging in the semiconductor sector, where thermal management has become a limiting factor in 3D integrated circuit (IC) designs. As chipmakers transition to stacking chips in three dimensions, traditional thermal pastes and adhesives fall short, leading to overheating and performance throttling. Graphene sheets are redefining the landscape for thermal interface materials (TIMs) by offering record-setting anisotropic thermal conductivity with research demonstrating that vertically aligned sheets achieve through-plane values as high as 1,800 W/mK, a quantum leap over the 5 W/mK typical of industry-standard thermal pastes.

Leading manufacturers such as TSMC are actively researching and piloting graphene TIMs in their CoWoS (Chip-on-Wafer-on-Substrate) packaging, with early results indicating the potential for reductions in hotspot temperatures by as much as 15°C. Meanwhile, research into ultra-thin graphene interlayers for chip stacks suggests their potential to enable designs as thin as 10 microns without introducing thermal bottlenecks, which could support significant boosts in clock speeds under intensive workloads, as explored in studies related to high-performance GPUs like those in Intel's product lines. These advances in graphene-based TIMs are not only solving the pressing challenge of heat dissipation in 3D electronics but are also facilitating higher chip density, improved reliability, and extended device lifetimes. As the drive toward ever-smaller, faster, and more energy-efficient electronics accelerates, the adoption of graphene sheets for both electrical and thermal management cements the Graphene Sheets Industry as a cornerstone of next-generation semiconductor and quantum computing technologies.

Market Share and Segmentation Analysis: Graphene Sheets Market

By Type: Few-Layer Graphene Dominates, Monolayer Graphene Shows Highest Growth

In 2025, Monolayer graphene, is projected to grow fastest with a CAGR of 28.3%, propelled by rising adoption in high-end electronics, photonics, and advanced sensors where atomic-level precision and conductivity are crucial. Few-layer graphene (3–10 layers) holds a significant share of the market, offering the optimal balance between electrical/thermal performance and scalable production costs, making it a preferred choice for for structural composites, energy devices, and mass-market electronics. Multilayer graphene sheets, though more cost-effective, primarily serve structural and industrial composite applications.

By Application: Electronics Lead, Energy Storage Accelerates

The energy storage segment is the fastest-growing with a CAGR of 30.1%, as graphene sheets deliver breakthrough improvements in battery and supercapacitor electrodes, supporting ultra-fast charging and higher energy densities. Sensors, biomedical devices, and thermal management solutions are also emerging as significant growth areas, particularly as demand for wearables, health monitoring, and high-efficiency cooling continues to expand. Electronics applications account for largest market share in 2025, reflecting the pivotal role of graphene sheets in enabling flexible displays, foldable circuits, and 5G antennas for global technology leaders.

.png)

By End-User: Electronics & Automotive Dominate, Healthcare Grows Fastest

Electronics manufacturers are the leading end-users, capturing a 33.5% share in 2025, as companies like Samsung and Huawei integrate graphene sheets into next-generation consumer devices. Healthcare is set for the highest growth, driven by the rapid development of implantable sensors, drug delivery platforms, and advanced diagnostic devices. Automotive, aerospace, and defense sectors also represent significant demand centers, using graphene sheets for lightweighting, de-icing, and structural reinforcement.

China Dominates Global Graphene Sheets Market with Large-Scale Production and Application Innovation

China stands as the world’s undisputed leader in graphene sheet production, accounting for over 60 percent of global market share thanks to a unique combination of state-backed research, rapid industrial scale-up, and aggressive commercialization strategies. Leading institutions like Tsinghua University have achieved a breakthrough with meter-scale single-crystal graphene sheets in 2024, providing a foundation for next-generation applications. Major Chinese brands such as Huawei and BOE are incorporating these advanced materials into flexible displays, while CATL is utilizing graphene sheets to improve energy density and performance in EV battery anodes. The Sixth Element has expanded CVD graphene production to 10,000 square meters per year, meeting surging domestic and international demand. Ningbo Morsh Tech’s release of high-conductivity graphene sheets for 5G devices underscores China’s drive to support digital infrastructure and consumer tech. In recent developments, BYD is integrating graphene sheets into solid-state battery prototypes, further positioning China at the vanguard of battery and materials technology. This integrated supply chain, from research to industrial adoption, ensures China’s continuing dominance in the global graphene sheets market for electronics, energy storage, and advanced manufacturing.

United States Expanding Graphene Sheets Capacity for Aerospace, Electronics, and Next-Gen Chips

The United States is rapidly increasing its capacity and expertise in graphene sheet production, leveraging significant federal support and leading-edge university research. With $50 million in funding for roll-to-roll graphene sheet manufacturing under the CHIPS Act, the U.S. is pushing toward mass production techniques that will enable lower costs and broader adoption. MIT’s achievement of defect-free graphene sheets via AI-controlled CVD is setting new industry benchmarks for quality and consistency. Key American applications span NASA spacecraft shielding, Tesla battery cooling technologies, and stealth coatings for Lockheed Martin, highlighting the material’s role in both defense and mobility. In 2024, Graphenea (a US-Spain venture) commercialized wafer-scale graphene sheets for electronics, and Intel is now testing graphene interconnects as a key step for sub-2nm chip manufacturing. This dynamic ecosystem of government support, technical innovation, and cross-sector partnerships is propelling the United States into a leadership position for aerospace, semiconductors, and high-performance graphene materials.

South Korea Leading Graphene Sheet Integration in Consumer Electronics and Automotive Sectors

South Korea is at the forefront of integrating graphene sheets into mainstream consumer electronics, automotive, and advanced energy systems. Samsung’s $300 million investment in graphene sheet synthesis supports the rapid evolution of foldable OLED displays, which require exceptional flexibility, transparency, and durability. KAIST’s innovation in self-assembled graphene sheets for high-performance supercapacitors is unlocking new possibilities for energy storage and portable electronics. Key applications range from Samsung Galaxy Z Fold screens to Hyundai fuel cell bipolar plates, with LG Chem’s 2024 release of ultra-thin graphene sheets now powering flexible heaters across multiple sectors. South Korean companies like SKC are also collaborating with Tesla on graphene-based battery current collectors, signaling a shift toward advanced battery architectures. This blend of industrial might and academic excellence ensures South Korea’s continued leadership in the production and global supply of high-value graphene sheet materials.

United Kingdom Advancing Aerospace and Industrial Adoption of Functionalized Graphene Sheets

The United Kingdom is establishing itself as a center for advanced graphene sheet research and scalable production, leveraging both university and industrial partnerships. The University of Manchester has pioneered laser-scribed graphene sheets for high-sensitivity sensors, driving breakthroughs in both defense and health applications. Versarien is rapidly scaling up production of graphene sheets for aerospace composites, meeting the needs of BAE Systems for radar-absorbing materials and supporting Dyson’s efforts to improve thermal management in consumer electronics. In 2024, Haydale launched a new line of functionalized graphene sheets optimized for EMI shielding in demanding industrial and military environments. Recent news includes Rolls-Royce’s ongoing testing of graphene sheets in jet engine thermal coatings, confirming the UK’s position at the intersection of research innovation, commercial manufacturing, and critical industry supply chains.

Germany Developing Graphene Sheet Solutions for Automotive, Sensors, and Photonics

Germany’s materials sector is embracing graphene sheets to advance performance in automotive, electronics, and precision sensor markets. The Fraunhofer IWS has made significant progress in optimizing graphene sheet transfer methods for silicon photonics, a critical step for integrating these materials into future data and telecom networks. BASF’s production of graphene sheets for fuel cell stacks supports the automotive industry’s push for cleaner, more efficient vehicles, including BMW’s i7 battery thermal pads and Siemens’ next-gen graphene pressure sensors. In 2024, SGL Carbon launched graphene sheet-reinforced graphite foils for high-end industrial applications, while Bosch is prototyping MEMS microphones that leverage graphene’s superior properties for audio and sensing. Germany’s combination of industrial rigor and cross-sector adoption positions it as a European leader in functional, value-added graphene sheet technologies.

Japan Advancing High-Mobility and Multi-Functional Graphene Sheets for Electronics and Mobility

Japan’s investment in graphene sheets is driving new applications across premium audio, mobility, and advanced medical devices. The National Institute of Advanced Industrial Science and Technology (AIST) has developed graphene sheets with record electron mobility, unlocking possibilities for ultra-fast, efficient electronics. Sony’s investment in graphene diaphragms is expected to set a new global standard for headphone audio, while Toyota is incorporating graphene sheets into hydrogen fuel cell membranes for next-generation green vehicles. Toray’s 2024 launch of graphene sheet-embedded carbon fiber prepregs is fueling innovations in aerospace and automotive structures. Fujifilm’s current testing of graphene sheets for flexible X-ray detectors signals expansion into high-performance medical imaging. This blend of research strength, cross-industry adoption, and global brand leadership is ensuring Japan’s pivotal role in the global graphene sheets market.

Canada Scaling Low-Cost Graphene Sheet Production for Transportation and Clean Tech

Canada is rapidly scaling up its capacity for cost-effective, high-quality graphene sheet production, particularly through NRC’s patented methane pyrolysis process. This approach enables a secure, affordable supply of graphene sheets for domestic and export markets. NanoXplore is now supplying graphene sheets to Magna International for automotive applications, and Bombardier is utilizing these materials in aircraft de-icing and advanced composite systems. In 2024, Grafoid commercialized graphene sheets specifically designed for industrial water filtration, expanding the technology’s environmental impact. Hydro-Québec is conducting advanced tests to integrate graphene sheets into solid-state batteries for grid storage and electric mobility. Canada’s combination of innovative production, industrial collaboration, and focus on sustainability is building a robust market for graphene sheets in transportation, infrastructure, and cleantech.

Australia Innovating with Graphene Sheets for Resource Sector and Medical Devices

Australia is distinguishing itself in the global graphene sheets market by converting local resources and research breakthroughs into high-impact industrial solutions. CSIRO’s world-first creation of graphene sheets from agricultural waste is driving new value streams for the country’s agritech and cleantech sectors. Graphene Manufacturing Group (GMG) is actively producing aluminum-graphene composite sheets, meeting the needs of global mining giants like Rio Tinto for high-strength conveyor belts and supplying advanced electrodes for medical devices such as Cochlear implants. In 2024, Imagine IM introduced corrosion-resistant graphene sheet coatings, extending product life in Australia’s demanding mining and infrastructure markets. ANSTO’s ongoing trials with graphene sheets in nuclear reactor shielding highlight the growing relevance of graphene for extreme environment and energy applications. Australia’s robust research, resource advantage, and focus on industry partnerships ensure its competitive edge in the expanding global graphene sheets industry.

Graphene Sheets Market Report Scope

Graphene Sheets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$259.8 Million

|

|

Market Size (2034)

|

$2280.8 Million

|

|

Market Growth Rate

|

27.3%

|

|

Segments

|

By Type (C6-C8, C10-C12), By Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Others), By Distribution Channel (Online, Offline)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Graphenea S.A. (Spain), General Graphene Corporation (USA), The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), ACS Material LLC (USA), Nanografi Nano Technology (Turkey), 2D Carbon Graphene Material Co. Ltd. (China), Graphene Square Inc. (South Korea), Paragraf (UK), CVD Equipment Corporation (USA), G6 Materials Corp. (USA), NanoXplore (Canada), Global Graphene Group (USA), Grolltex (USA), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Monolayer Graphene

- Bilayer Graphene

- Few-Layer Graphene

- Multilayer Graphene Sheets

By Application

- Electronics (Transparent electrodes, flexible displays)

- Energy Storage (Battery anodes, supercapacitor components)

- Composites (Aerospace, automotive reinforcement)

- Thermal Management (Heat spreaders for electronics)

- Sensors & Biomedical (Biosensors, filtration membranes)

By Production Method

- Chemical Vapor Deposition (CVD) Graphene

- Liquid-Phase Exfoliation (LPE) Graphene Sheets

- Thermal Exfoliation Graphene Sheets

- Graphene Oxide (GO) / Reduced Graphene Oxide (rGO) Sheets

- Silicon Carbide (SiC) Sublimation

By End-user

- Automotive & Transportation

- Aerospace & Defense

- Electronics

- Consumer Goods

- Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Sheets Market: Profiles & Strategies

- Graphenea S.A. (Spain)

- General Graphene Corporation (USA)

- The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China)

- ACS Material LLC (USA)

- Nanografi Nano Technology (Turkey)

- 2D Carbon Graphene Material Co. Ltd. (China)

- Graphene Square Inc. (South Korea)

- Paragraf (UK)

- CVD Equipment Corporation (USA)

- G6 Materials Corp. (USA)

- NanoXplore (Canada)

- Global Graphene Group (USA)

- Grolltex (USA)

* List Not Exhaustive

Methodology

The Graphene Sheets Market Report utilizes USDAnalytics’ proven research methodology combining extensive primary and secondary research. Primary research involved in-depth interviews with industry executives, material scientists, engineers, business leaders, and marketing managers across global graphene manufacturers and key end-user industries such as electronics, automotive, aerospace, and healthcare. Secondary research leveraged proprietary databases, scientific publications, patent analysis, company annual reports, investor presentations, and trade journals to track emerging trends, technological developments, and regulatory impacts.

Data triangulation techniques were applied to validate market sizing, growth rates, and forecasts. Detailed modeling was used to derive market size estimates for each segment, incorporating factors such as technological adoption rates, regional capacity expansions, price trends, and downstream application demand. The final insights presented reflect a synthesis of statistical analysis, expert opinions, and deep industry knowledge, ensuring actionable intelligence for strategic decision-making across stakeholders in the graphene sheets market.

Research Coverage and Deliverables

This report covers the Graphene Sheets Market in depth, including:

- Market size (2025–2034) and CAGR analysis

- Market segmentation by:

- Type: Monolayer, Bilayer, Few-Layer, Multilayer Graphene Sheets

- Application: Electronics, Energy Storage, Composites, Thermal Management, Sensors & Biomedical

- Production Method: CVD, LPE, Thermal Exfoliation, GO/rGO, SiC Sublimation

- End-user: Automotive & Transportation, Aerospace & Defense, Electronics, Consumer Goods, Healthcare, Others

- Competitive landscape profiling 17 key companies

- Country-level analysis for 21 nations

- Key technological innovations and commercialization trends

- Analysis of emerging opportunities and challenges shaping the market’s future

Deliverables

Clients purchasing this report receive:

- A comprehensive PDF report with detailed tables, charts, and insights

- Dataset in Excel format covering all market figures and forecasts

- Company profiles and SWOT analysis for top market participants

- Analyst support for clarifications and follow-up queries

- Customizable segmentation analysis upon request

- Executive summary and key takeaway slides for boardroom presentations