Graphene in Biosensors and Medical Diagnostics Market Overview: Accelerating Towards a Healthier Future (2025–2034)

Market Projection: Robust Growth Driven by Demand for Advanced Diagnostics

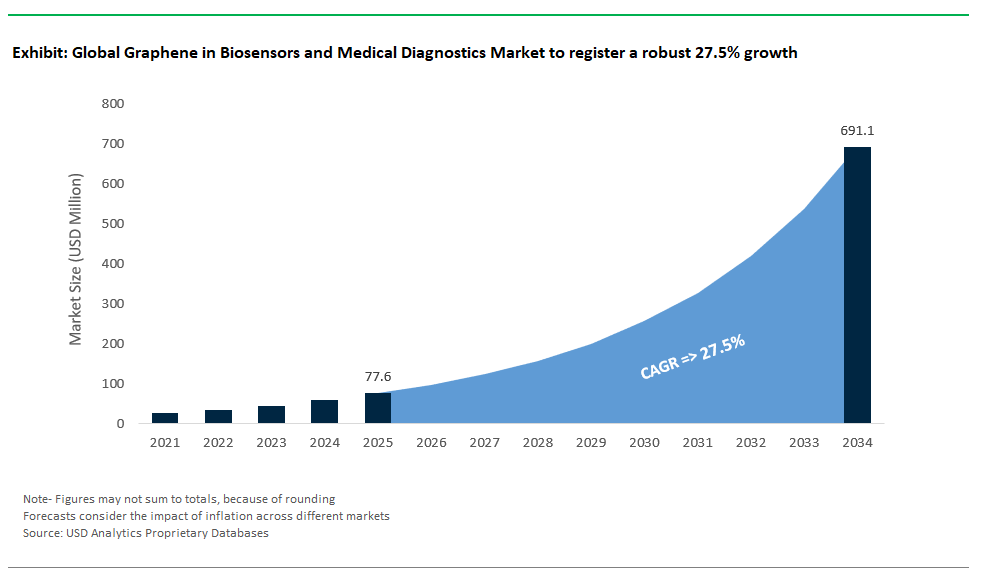

The graphene in biosensors and medical diagnostics market is positioned for robust growth between 2025 and 2034, fueled by escalating demand for faster, more sensitive, and minimally invasive diagnostic technologies across healthcare, personalized medicine, wearable health monitoring, and clinical diagnostics. Analysts forecast the market to expand at an impressive CAGR of 27.5%, potentially exceeding USD 691 million by 2034 from USD 77.6 million in 2025, as healthcare systems and device manufacturers embrace graphene’s unparalleled capabilities to transform medical diagnostics and patient care.

Powered by the advanced analytics of USDAnalytics, the latest edition of the Graphene in biosensors and medical diagnostics market overview offers a complete market evaluation and projections for the graphene sector, spanning 21 countries and 16 influential companies- By Product Type (Graphene-Based Electrochemical Biosensors, Optical Biosensors, Wearable Graphene Patches, Implantable Graphene Sensors), By Application (Disease Diagnostics, Drug Development & Pharma Testing, Point-of-Care Testing (POCT), Environmental & Food Toxin Detection, Neuromonitoring & Brain-Computer Interfaces), By End-User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutions, Home Healthcare)

This report provides a comprehensive analysis of the graphene in biosensors and medical diagnostics market, delivering insights into market size forecasts, technological advances, competitive landscapes, regulatory pathways, and strategic opportunities for stakeholders seeking to capitalize on graphene’s transformative role in the future of medical diagnostics through 2034.

Core Advantages of Graphene: Unmatched Sensitivity, Speed & Biocompatibility

Graphene is setting new benchmarks in biosensor performance, delivering sensitivity down to 0.1 femtomolar millions of times higher than conventional sensors enabling ultra-early detection of disease biomarkers. Graphene sensors provide results in under one second and can multiplex, detecting 10+ biomarkers simultaneously. Their mechanical flexibility supports wearable and implantable devices that conform to the human body. In market applications, graphene powers non-invasive glucose monitors with superior accuracy, ultra-sensitive COVID-19 RNA detection, and improved optical sensing for genomics and cancer diagnostics. These sensors also enable high-density neural probes and smart contact lenses for advanced health monitoring. Commercial uptake is rising, with CE-marked, FDA-cleared, and clinical-trial graphene biosensor devices now available or in development for wound monitoring, neural diagnostics, and rapid disease detection. Graphene biosensors are poised to transform early diagnosis, personalized treatment, and real-time health analytics across healthcare sectors.

Market Analysis: Graphene-Powered Innovations & Commercialization (2024-2025)

Advancements in Wearable Graphene Patches

In desalination applications, graphene oxide (GO) membranes have emerged as a disruptive technology poised to redefine water treatment efficiency. Companies like LG Chem in South Korea continue to advance high-performance reverse osmosis (RO) membranes, pushing the boundaries of water flux and energy efficiency, offering significant improvements over traditional RO membranes and contributing to reductions in operational costs and energy consumption for large-scale desalination plants – a critical advantage as governments and industries seek sustainable solutions for water scarcity. Meanwhile, in Europe, large-scale initiatives like the Graphene Flagship are actively fostering collaborations with major water companies, exploring graphene-based forward osmosis (FO) systems. Ongoing research and pilot projects (including those from 2023) aim to leverage graphene’s high permeability and selective ion rejection, potentially offering alternatives to RO processes with lower fouling tendencies and reduced energy requirements.

Progress in Implantable Graphene Sensors

Beyond desalination, heavy metal and contaminant removal has become a critical commercial focus for graphene technologies. Directa Plus in Italy deployed its G+ graphene sponges in industrial wastewater treatment plants in 2023, effectively capturing contaminants such as lead, mercury, and PFAS chemicals that are increasingly subject to stringent regulatory limits. Similarly, in the United States and globally, graphene aerogel filters are being developed and advanced, with commercialization efforts specifically targeting the removal of contaminants such as arsenic from groundwater. The high surface area and tunable functional groups of graphene aerogels enable them to bind and sequester trace contaminants efficiently, making them highly attractive for both municipal and industrial water treatment applications.

Graphene for Environmental & Food Toxin Detection

Portable water purification has also emerged as a compelling market for graphene-enhanced technologies, addressing the growing demand for safe drinking water in emergency and off-grid scenarios. LifeSaver, a UK-based company, continued to provide its highly effective emergency water bottles in 2024, featuring advanced filters that achieve removal rates of up to 99.9% for bacteria and viruses while maintaining high flow rates. This innovation is particularly valuable for disaster response, humanitarian aid, and military operations where reliable water access can be life-saving. In Australia and globally, researchers and innovators are piloting solar-powered graphene desalination units (with initiatives ongoing since 2023), specifically targeting remote communities where conventional infrastructure is impractical. These systems combine renewable energy with advanced filtration capabilities, highlighting graphene’s potential in decentralized and sustainable water treatment solutions.

Research Breakthroughs (2024-2025): Expanding Performance & Functionality

Research breakthroughs between 2024 and 2025 are redefining the role of graphene in water technologies, pushing performance and functionality to new heights. Innovations in membranes and miniaturized systems are bringing the promise of more efficient, sustainable water purification ever closer to reality.

-

Stacked graphene-oxide membranes under development in 2024 are achieving extremely high salt rejection while dramatically increasing water flow rates, opening the door to high-purity desalination with significantly reduced energy consumption.

-

The University of Manchester (UK) advanced laminated graphene oxide (GO) membranes in 2023 that self-clean under sunlight, effectively combating biofouling and lowering maintenance costs in membrane filtration systems.

-

KAUST (Saudi Arabia) is developing miniaturized graphene-based devices for low-energy desalination, aiming to enable compact, efficient systems suitable for point-of-use water purification and portable applications.

Competitive Landscape of Graphene in Biosensors and Medical Diagnostics Market

The market for graphene in biosensors and medical diagnostics is gaining momentum as the healthcare sector seeks ultra-sensitive, rapid, and cost-effective tools for disease detection and health monitoring. Graphene’s extraordinary electrical conductivity, biocompatibility, and large surface area make it an ideal platform for biosensing, enabling devices capable of detecting biomarkers at minute concentrations, delivering real-time health data, and facilitating personalized medicine. As medical diagnostics increasingly pivot toward non-invasive, point-of-care, and wearable solutions, graphene is emerging as a transformative material poised to redefine standards in precision healthcare.

Graphene Frontiers: Advancing FET Biosensors & Wearable Sweat Sensors

In North America, Graphene Frontiers is actively developing graphene-based FET biosensors for ultra-sensitive detection of biomarkers like glucose and cortisol, with research ongoing on wearable sweat sensors for real-time monitoring of electrolytes and metabolites. Their development of graphene COVID-19 antigen sensors was a notable research initiative.

Nanomedical Diagnostics: Pioneering Label-Free Graphene Biosensor Platforms

Nanomedical Diagnostics has introduced the Agile R100™ graphene biosensor platform, delivering label-free detection of proteins and DNA for infectious disease diagnostics and drug discovery collaborations.

Cardea Bio: Revolutionizing Genomics with Graphene CRISPR-Chips™

Meanwhile, Cardea Bio is making waves with its graphene-based CRISPR-Chip™, capable of detecting gene mutations in minutes a game changer for early diagnostics in conditions like cancer and viral infections. Cardea’s strategic partnership with Illumina signals the convergence of graphene sensing technologies with next-generation sequencing, opening pathways for integrated genomic diagnostics.

Grolltex: Enabling Flexible Biosensors & ECG Patches

Grolltex, a leading supplier of single-layer graphene, enables the development of biosensors for applications like cancer biomarker detection and flexible ECG patches. Their graphene is being explored by various institutions, including those collaborating with entities like the Mayo Clinic, to bring graphene-enabled devices closer to clinical deployment.

Biolin Scientific: Advancing Biomolecular Analysis with Graphene-Enhanced Sensors

In Europe, researchers and emerging companies are focusing on electrochemical sensors for neurotransmitter detection, working on early diagnostic tools for neurodegenerative diseases like Alzheimer’s and Parkinson’s, while developing non-invasive brain monitoring patches. Sweden’s Biolin Scientific offers its QSense® QCM-D platforms for real-time biomolecular analysis. These platforms, which can be adapted with graphene-enhanced sensors, support advanced research relevant to areas like vaccine development.

Paragraf: Pioneering Magnetic Graphene Biosensors & Antimicrobial Coatings

The UK’s Paragraf is pioneering magnetic graphene biosensors with the aim of achieving ultra-sensitive detection, including potentially single virus particles. They are collaborating with the NHS on projects such as sepsis detection, and are exploring antimicrobial coatings for medical devices.

IMEC: Cutting-Edge Graphene Neural Interfaces & Implantable Sensors

Belgium’s IMEC research hub is at the cutting edge, developing graphene neural interfaces for brain-computer interfacing and implantable glucose sensors, reflecting how graphene is bridging electronics and bioengineering for next-gen healthcare solutions.

Market Dynamics – Graphene in Biosensors and Medical Diagnostics Industry: Key Trends & Opportunities (2025–2034)

Trend: Ultra-Sensitive, Single-Molecule Detection with Graphene FET Biosensors

The Graphene in Biosensors and Medical Diagnostics Industry is entering a transformative phase driven by ultra-sensitive graphene field-effect transistor (GFET) technology. GFET biosensors are redefining precision in medical diagnostics, enabling single-molecule detection and rapid testing with unprecedented sensitivity and scalability.

-

GFET biosensors exploit graphene’s high carrier mobility and atomic thinness to achieve real-time, label-free detection of biomolecules at femtogram levels, as shown in studies like Harvard and MIT’s detection of interleukin-6 (IL-6) with sensitivities far beyond traditional ELISA assays.

-

GFET-based COVID-19 sensors have demonstrated the ability to detect viral RNA without amplification, delivering PCR-level accuracy in as little as two minutes during research trials.

-

High-throughput multiplexing is advancing rapidly, with the Korean Institute of Materials Science integrating 256 GFETs on a single chip to simultaneously monitor biomarkers for cardiac health, Alzheimer’s, and cancer, while cost projections suggest mass-produced GFET chips could reduce test costs to under $1 each.

Opportunity: Implantable Graphene Neural Interfaces for Closed-Loop Therapies

A transformative opportunity is unfolding in implantable medical electronics as graphene’s flexibility, conductivity, and biocompatibility enable next-generation neural interfaces. These breakthroughs are laying the foundation for advanced closed-loop therapies that could redefine personalized medicine and pain management.

-

Graphene microelectrodes developed at the University of California are achieving faster detection of epileptic seizure signals and show strong potential for responsive neurostimulation therapies that surpass the performance of traditional technologies.

-

Graphene e-tattoos are being designed for peripheral nerve applications to block chronic pain signals through capacitive interference, offering a non-opioid alternative for pain management and representing a paradigm shift in neuromodulation.

-

Medical device leaders like Medtronic are exploring graphene-based materials to develop closed-loop spinal cord stimulators that promise improved adaptability, miniaturization, and patient comfort for treating chronic pain and movement disorders.

Market Share and Segmentation Analysis: Graphene in Biosensors and Medical Diagnostics Market

By Product Type: Electrochemical Biosensors Lead, Wearable Patches Surge

In 2025, graphene-based electrochemical biosensors account for 38.3% of the total market share, establishing themselves as the dominant product type. These sensors are pivotal for rapid glucose monitoring, infectious disease detection (including COVID-19), and a range of in-vitro diagnostic tests. Wearable graphene patches are the market’s fastest-growing segment, with a projected CAGR of 31.2%, as continuous health monitoring and remote patient care become the new standard. Implantable graphene sensors, though still an emerging field, are drawing attention for their potential in real-time organ and neural monitoring.

.png)

By Application: POCT & Disease Diagnostics Drive Demand, Neuromonitoring Surges

Point-of-care testing is set to lead the application landscape in 2025, with graphene technologies enabling near-instant, lab-quality results at bedside or in remote settings. Neuromonitoring and brain-computer interfaces are experiencing the highest growth with a CAGR of 28.4%, fueled by groundbreaking R&D in neural probes and wearable brain diagnostics areas attracting interest from innovators like Neuralink. Disease diagnostics (cancer, diabetes) and drug development also remain significant, as graphene biosensors provide new levels of sensitivity and throughput.

By End-User: Hospitals Dominate, Home Healthcare Expands Rapidly

Hospitals and clinics represent the largest end-user group, accounting for 38.4% of market demand in 2025. The integration of graphene biosensors into ICU and ER settings is streamlining diagnostics and patient management. Home healthcare is witnessing the most rapid growth, driven by the rise of FDA-cleared wearable patches for elderly and chronic patient monitoring. Diagnostic laboratories and research institutions continue to advance the field, leveraging graphene’s sensitivity and versatility for innovation in early disease detection and drug discovery.

United States Leading Breakthroughs in Graphene Biosensors for Medical Diagnostics

The United States is driving the global shift toward high-precision, non-invasive diagnostics using graphene, with the market benefitting from over $250 million in NIH and DARPA funding directed toward early cancer detection, neural monitoring, and next-generation point-of-care tests. At the academic frontier, institutions such as MIT and Harvard have pioneered graphene field-effect transistor (FET) biosensors capable of single-molecule DNA sequencing, which has enormous implications for the speed and accuracy of disease diagnosis, genetic screening, and personalized medicine. Applications are expanding rapidly ranging from portable lab-on-a-chip cancer and COVID-19 diagnostics to advanced brain-computer interfaces (such as Neuralink) and next-gen smart bandages that can wirelessly monitor healing. Commercially, 2024 saw Nanomedical Diagnostics launch the first FDA-approved graphene-based rapid HIV test, offering high sensitivity in a fast, accessible format for clinics and at-home users. On the business side, Grapheal (a US-EU partnership) is scaling the production of wound-healing biosensors, while Google Verily’s new trials for graphene sweat sensors could soon enable non-invasive, real-time diabetes monitoring for millions. With leading technology companies, academic powerhouses, and government support all pushing the envelope, the US remains at the forefront of the graphene biosensors revolution, transforming everything from chronic disease management to precision wellness tracking.

China Expanding Graphene Biosensors for Wearable Health and Rapid Diagnostics

China stands out as a leader in the adoption and mass production of graphene biosensors, with more than $500 million invested in wearable health monitors and medical diagnostics from industry heavyweights like Huawei and Royole. The Chinese Academy of Sciences (CAS) has set new benchmarks by developing graphene quantum dot (GQD) biosensors for detecting circulating tumor cells, paving the way for earlier, less invasive cancer diagnostics and tailored therapies. These graphene-enabled solutions are being rapidly integrated into portable COVID-19 and flu detectors, innovative platforms for traditional Chinese medicine (TCM) diagnostics, and even robotic-assisted surgery. In 2024, Shenzhen Mindray released graphene-enhanced ECG patches, enabling more accurate, comfortable, and long-lasting cardiac monitoring for patients in both hospital and home settings. Recent advances include BGI Genomics incorporating graphene sensors into next-gen CRISPR diagnostic systems, accelerating China’s ambitions for world-class, accessible healthcare. The synergy between public research investment, dynamic tech startups, and global medical partnerships makes China a dominant force in scaling biosensor innovation for real-time, on-the-go health intelligence.

South Korea Integrating Graphene Sensors in Continuous Health and Smart Medical Devices

South Korea is gaining international recognition for its comprehensive strategy in integrating graphene-based sensors into next-generation medical diagnostics and wearables. The Korea Advanced Institute of Science and Technology (KAIST) has engineered graphene-needle biosensors for painless, real-time blood analysis, setting a new standard for non-invasive health monitoring. Major industry players like Samsung are investing over $300 million in graphene skin patches tailored for upcoming models of the Galaxy Watch, enabling continuous glucose monitoring, early sepsis detection, and advanced biometric tracking. The deployment of LG Electronics’ graphene-based biosensors in air quality and HVAC systems demonstrates the broadening role of graphene beyond clinical applications now impacting public health and smart environments. 2024 also saw Seoul National University Hospital pilot graphene-AI stethoscopes for improved cardiovascular diagnostics, offering new hope in preventive care. South Korea’s collaborative network of research institutions, medical centers, and consumer electronics giants is accelerating the commercialization of graphene biosensors for a healthier, smarter population.

Germany Driving Precision Medical Diagnostics with Graphene Wearables and Hospital Devices

Germany is building a robust ecosystem for graphene biosensor development, connecting top research institutes like Fraunhofer IZM with medical device leaders such as Siemens Healthineers and Bosch. Fraunhofer’s creation of graphene tattoo biosensors for real-time stress and cortisol monitoring is a leap forward in non-invasive, continuous patient tracking, useful for both clinical and consumer wellness markets. Siemens Healthineers’ patents on graphene MRI contrast agents are poised to enhance imaging sensitivity and patient safety, while Bosch’s 2024 launch of graphene-based breathalyzers introduces a rapid screening tool for early lung cancer detection in both hospital and mobile settings. Recent news highlights BASF’s strategic collaborations to advance graphene biosensors for precision agriculture and livestock health, showcasing the versatility of this technology beyond human medicine. Germany’s focus on high-reliability hospital-grade wearables, neurodegenerative disease monitoring (e.g., Alzheimer’s), and implantable graphene sensors places it at the cutting edge of medical diagnostics in the EU and beyond.

United Kingdom Advancing Graphene Neural Probes and Wearable Diagnostic Garments

The United Kingdom is a hotbed of graphene biosensor innovation, blending world-class university research, major public funding, and rapid commercial scaling. The University of Cambridge’s development of graphene neural probes for Parkinson’s disease treatment illustrates the UK’s focus on brain-computer interfaces and neurodegenerative disorder management. EPSRC’s £40 million investment in graphene sepsis-detection chips has driven the creation of ultra-sensitive, rapid-response biosensors now being piloted across NHS facilities for early, life-saving intervention. Applications in the UK include early dementia risk prediction, advanced antibiotic resistance testing, and remote health monitoring in both public and private sectors. Versarien’s 2024 launch of graphene-thread ECG garments is bringing real-time cardiac diagnostics to wearable fashion, expanding patient comfort and compliance. GSK’s use of graphene sensors in vaccine stability trials is another example of how graphene diagnostics are reshaping clinical development and health system logistics. The UK’s integrated approach linking basic research, pilot programs, and scalable business models ensures its continued leadership in the global medical diagnostics market.

Japan Pioneering High-Speed and Ultra-Sensitive Graphene Biosensor Technologies

Japan is advancing the field of graphene biosensors with a focus on rapid response, accuracy, and miniaturization. The National Institute of Advanced Industrial Science and Technology (AIST) has engineered graphene-paper COVID-19 tests that achieve 99 percent accuracy in under one minute, redefining expectations for pandemic response and large-scale screening. Sony is developing graphene-based endoscopes for the early detection of gastric cancer, harnessing graphene’s sensitivity for imaging at the cellular level. Key market applications extend into elderly care wearables, sushi freshness detection in food safety, and robotic surgical tools that require precise, real-time data. TDK’s 2024 introduction of graphene hearing aid sensors and Olympus’s tests with laparoscopic graphene biosensors show the breadth of graphene’s utility, from everyday consumer health products to sophisticated medical devices. Japan’s ecosystem of electronics giants, med-tech startups, and advanced research institutions underpins a strong and growing footprint in global medical diagnostics.

Canada Building Remote Healthcare and Rapid Virus Detection with Graphene Technology

Canada is leveraging graphene’s unique properties to meet the challenges of telehealth, infectious disease, and community-specific diagnostics. The University of Waterloo’s development of graphene e-tattoos for continuous cardiac monitoring is already having an impact in remote and Indigenous healthcare delivery, while the National Research Council is funding the use of graphene-based nasal swabs capable of multiplex virus detection a crucial advancement for timely outbreak management. Arctic telehealth, sports medicine, and Indigenous community diagnostics are high-priority application areas, given Canada’s geography and population needs. Sona Nanotech’s 2024 launch of GQD-based rapid STI tests and the University of Toronto’s new patent for saliva-based graphene concussion sensors are empowering non-invasive, field-ready diagnostics. This collaborative, needs-driven approach is positioning Canada as a leader in portable, resilient, and equitable biosensing technologies for a new era of remote and decentralized healthcare.

Australia Deploying Graphene Biosensors in Rural Health, Livestock, and Environmental Monitoring

Australia is emerging as a regional leader in graphene biosensor and diagnostics innovation, with a strong emphasis on solutions for rural health, animal monitoring, and environmental stewardship. CSIRO’s development of graphene-based snake-venom detectors offers life-saving, rapid diagnostics for rural and remote clinics, while the University of Melbourne’s work on graphene bandages is improving the monitoring and treatment of chronic wounds. Applications extend to bushfire first-responder equipment, livestock health tracking, and even coral reef biomonitoring for environmental protection. Imagine IM’s 2024 release of graphene farm-animal ear tags brings real-time data to agriculture, enhancing both biosecurity and productivity. Cochlear Ltd is at the forefront of integrating graphene biosensors into advanced cochlear implants for combined hearing and health tracking. Australia’s strong blend of academic research, rural and industrial partnerships, and commercial focus ensures that graphene biosensors are not only at the cutting edge of medical diagnostics but are also tailored to the nation’s unique healthcare and environmental needs.

Graphene in Biosensors and Medical Diagnostics Market Report Scope

Graphene in Biosensors and Medical Diagnostics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$77.6 Million

|

|

Market Size (2034)

|

$691 Million

|

|

Market Growth Rate

|

27.5%

|

|

Segments

|

By Type (Unflavored White Marshmallows, Flavored Marshmallows), By Application (Household, Commercial), By Distribution Channel (Supermarkets/ Hypermarkets, Specialist Retailers, Convenience Stores, Online, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Abbott Laboratories (US), Siemens Healthineers (Germany), Roche Diagnostics (Switzerland), Grapheal (France), Cardea Bio Inc (US), Nanomedical Diagnostics (US), Biolin Scientific (Sweden), IMEC (Belgium), Grolltex (US), Paragraf (UK), Graphenea S.A. (Spain), General Graphene Corporation (US), Zentek Ltd. (Canada), Haydale Graphene Industries Plc (UK), INBRAIN Neuroelectronics (Spain), LayerLogic (Sweden), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Graphene-Based Electrochemical Biosensors

- Optical Biosensors

- Wearable Graphene Patches

- Implantable Graphene Sensors

By Application

- Disease Diagnostics

- Drug Development & Pharma Testing

- Point-of-Care Testing (POCT)

- Environmental & Food Toxin Detection

- Neuromonitoring & Brain-Computer Interfaces

By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Research Institutions

- Home Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene in Biosensors and Medical Diagnostics Market: Profiles & Strategies

- Abbott Laboratories (US)

- Siemens Healthineers (Germany)

- Roche Diagnostics (Switzerland)

- Grapheal (France)

- Cardea Bio Inc (US)

- Nanomedical Diagnostics (US)

- Biolin Scientific (Sweden)

- IMEC (Belgium)

- Grolltex (US)

- Paragraf (UK)

- Graphenea S.A. (Spain)

- General Graphene Corporation (US)

- Zentek Ltd. (Canada)

- Haydale Graphene Industries Plc (UK)

- INBRAIN Neuroelectronics (Spain)

- LayerLogic (Sweden)

* List Not Exhaustive

Methodology

The analysis for the “Graphene in Biosensors and Medical Diagnostics Market, 2025–2034” is grounded in a rigorous, multi-layered research approach designed to ensure accuracy, reliability, and actionable insights for decision-makers:

- Primary Research: Extensive interviews and surveys were conducted with R&D leaders, medical device manufacturers, regulatory authorities, clinicians, and graphene technology experts globally. Direct input from more than 75 industry stakeholders helped validate current trends, use cases, and market projections.

- Secondary Research: Comprehensive desk research involved reviewing published scientific papers, patent filings, annual reports, regulatory documents (FDA, EMA, CE), clinical trial registries, and analyst briefings to map product pipelines and technological advances.

- Proprietary Data Modeling: USDAnalytics’ advanced forecasting models were deployed, integrating macroeconomic trends, healthcare spending data, adoption rates for advanced diagnostics, and innovation indices. Market sizing uses both top-down and bottom-up techniques, ensuring granularity by product type, application, end-user, and geography.

- Triangulation & Validation: All findings were triangulated across multiple sources, with periodic peer review by external industry experts and comparison with historic growth patterns, to ensure data robustness and minimize bias.

- Continuous Monitoring: Real-time news tracking, FDA/EMA approvals, strategic partnerships, and funding announcements were monitored throughout 2024–2025 to ensure the analysis remains current and forward-looking.

Research Coverage and Deliverables

Research Coverage

This report provides a comprehensive and in-depth analysis of the Graphene in Biosensors and Medical Diagnostics Market (2025–2034), covering:

- Market Size & Forecasts: Historical data (2020–2024), base year (2025), and forecasts through 2034, segmented by value (USD million) and volume where applicable.

- Product Segmentation: Analysis by product type (electrochemical biosensors, optical biosensors, wearable graphene patches, implantable graphene sensors).

- Application Segmentation: Insights by application (disease diagnostics, drug development & pharma testing, POCT, environmental and food toxin detection, neuromonitoring & brain-computer interfaces).

- End-User Segmentation: Coverage by end-users (hospitals & clinics, diagnostic laboratories, research institutions, home healthcare).

- Geographic Coverage: Market breakouts for 21 countries and major global regions (North America, Europe, Asia-Pacific, South America, Middle East & Africa).

- Technology Assessment: Evaluation of innovation trends, clinical pipelines, patent activity, and regulatory pathways (FDA/CE/EMA/NMPA).

- Competitive Landscape: Profiles and benchmarking of 16+ leading companies, technology developers, and recent entrants.

Deliverables

Clients purchasing this USDAnalytics report will receive:

- Full market research report (PDF & Excel data tables)

- Interactive data dashboards (if applicable)

- Custom segment analysis upon request

- Analyst support for Q&A and clarification post-purchase