Graphene Production Technologies Market Overview: Meeting Soaring Demand (2025–2034)

Market Projection: Robust Growth Driven by Scalable, Cost-Effective Production

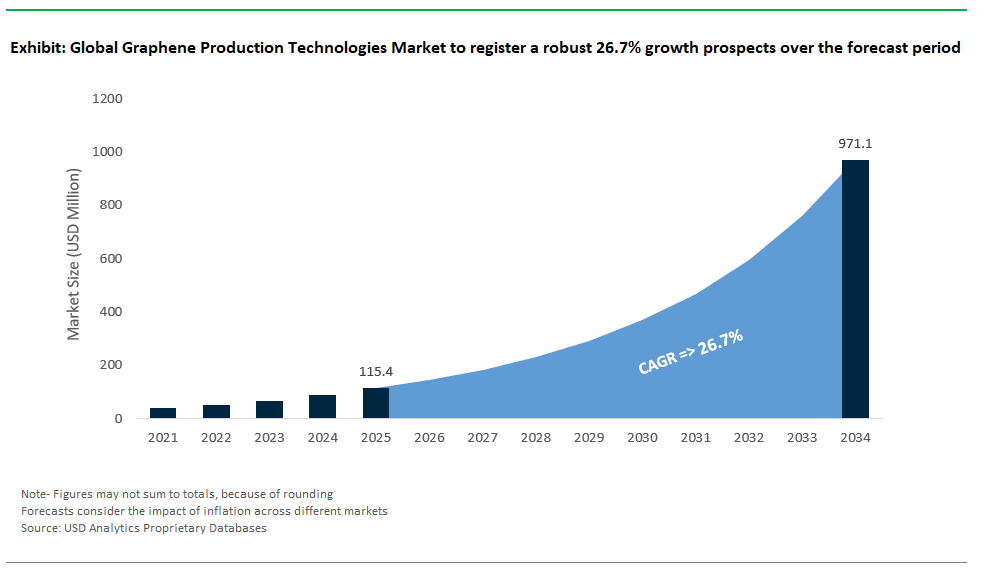

The graphene production technologies market is poised for significant expansion between 2025 and 2034, driven by surging global demand for high-performance graphene across electronics, composites, energy storage, flexible devices, and advanced manufacturing sectors. Analysts forecast robust growth at a CAGR of 26.7%, with the market’s total value projected to exceed USD 970.9 million by 2034 from USD 115.4 million in 2025, as industries increasingly adopt scalable, cost-effective methods to meet the stringent quality and volume requirements of emerging applications.

Building on USDAnalytics’ proprietary datasets, the latest edition of the Graphene production technologies market delivers a comprehensive analysis and outlook of the graphene industry, spanning 21 countries and 18 companies- By Technology (Chemical Vapor Deposition (CVD), Mechanical Exfoliation, Liquid-Phase Exfoliation (LPE), Electrochemical Exfoliation, Reduction of Graphene Oxide (rGO), Plasma Methods, Others), By End Product Form (Graphene Sheets/Films, Graphene Nanoplatelets (GNPs), Graphene Oxide (GO), Graphene Powder/Flakes, Graphene Quantum Dots (GQD), By Application (Electronics & Photonics, Energy Storage, Composites, Coatings, Others), By Scale of Production (Research & Lab Scale, Pilot Scale, Industrial/Commercial Scale), By End-Product Quality (High-Purity / Research Grade Graphene, Industrial Grade Graphene, Functionalized Graphene)

This report offers a comprehensive analysis of the graphene production technologies market, delivering insights into market size forecasts, competitive strategies, technological advances, production economics, regulatory standards, and strategic opportunities for stakeholders aiming to capitalize on graphene’s transformative role across industries through 2034.

Evolving Graphene Production Methods: Top-Down vs. Bottom-Up

Graphene production is advancing rapidly, with both top-down and bottom-up methods evolving to meet industrial demand. Top-down techniques like mechanical exfoliation yield nearly defect-free graphene but are mainly used for research due to low scalability. Liquid-phase exfoliation (LPE) dominates bulk production, offering up to 50% yield and low costs, making it ideal for composites and conductive materials, though it can result in varied layer quality. Bottom-up methods, especially chemical vapor deposition (CVD), produce high-purity, electronics-grade graphene, now scaled up by companies like Samsung for large-area films used in flexible electronics. Epitaxial growth on silicon carbide is gaining momentum for quantum and high-frequency devices, despite limited scalability. Next-generation approaches plasma-enhanced CVD, laser-induced graphene, and flash joule heating are driving down costs and energy usage while enabling new applications. Quality control is essential, with international standards ensuring high purity and electrical performance, as large-scale, consistent quality remains the primary industrial challenge and a key competitive factor.

Market Analysis: Graphene Production Technologies Innovations & Commercialization (2024–2025)

Between 2024 and 2025, the field of graphene production technologies has experienced a significant leap forward, evolving from laboratory-scale processes into diverse, industrial-scale manufacturing methods. A convergence of technological innovation, cost reduction, and environmental sustainability is transforming how graphene is produced, making it increasingly viable for widespread commercial adoption across electronics, energy storage, composites, and flexible devices. Global companies and research institutions are investing heavily in new production techniques, each offering unique pathways to meet the market’s growing demand for high-quality graphene at affordable prices.

Industrial-Scale Production Methods: Expanding Capacity

Industrial-scale production methods have expanded rapidly, led by breakthroughs in chemical vapor deposition (CVD), liquid-phase exfoliation (LPE), and advanced plasma or laser synthesis techniques. In CVD, leading electronics manufacturers, such as Samsung in South Korea, are actively pursuing advancements in roll-to-roll production of monolayer graphene sheets for flexible displays and large-area electronics, with progress continuing into 2024. Meanwhile, Graphenea in Spain continues to provide wafer-scale graphene for semiconductor research and development, supporting the industry's exploration of graphene for next-generation chip technologies, including potential applications in interconnects.

Liquid-Phase Exfoliation (LPE): Commercial Success for Nanoplatelets

Liquid-phase exfoliation remains one of the most commercially successful methods for producing graphene nanoplatelets (GNPs). In Australia, First Graphene is a key player, utilizing a proprietary single-step electrochemical exfoliation process to produce high-quality graphene. Their efficient production methods contribute to competitive pricing, with ongoing efforts in 2024 to further reduce costs and scale for mass-market applications. NanoXplore in Canada, a major player in the LPE space, has a stated goal to significantly scale its graphene production capacity to 20,000 tonnes per year by 2027, with investments commencing in 2023, positioning itself as one of the world’s largest graphene manufacturers. Such capacity ensures sufficient supply for large-volume applications, including polymers composites, and energy storage systems.

Plasma & Laser Synthesis: High-Purity & Reduced Environmental Footprint

In plasma and laser synthesis, advanced techniques are enabling high-purity graphene production while reducing environmental footprints. Research institutions like MIT in the United States are pioneering plasma-based synthesis approaches, including methods utilizing methane as a feedstock, aiming to significantly cut energy consumption compared to traditional methods, with ongoing developments in 2024. Meanwhile, companies like Graphene Leaders Canada (GLC) are active in producing various graphene forms, and the broader industry is seeing advancements in laser-induced graphene (LIG) production (with applications emerging in 2023) for flexible electronics applications, offering a direct, scalable route to patterned graphene films that can be integrated into wearable devices and sensors.

Emerging & Green Production Methods: Driving Sustainability

Emerging and green production methods are gaining traction as sustainability becomes a critical driver for the materials industry. The University of Queensland in Australia has developed innovative processes for converting biomass waste, such as coconut shells, into graphene, demonstrating pathways for valorizing agricultural by-products into advanced materials. Rice University in the United States continued its pioneering work in 2024, scaling up plastic waste-to-graphene conversion using its proprietary flash graphene technique, highlighting how circular economy principles can be integrated into advanced materials manufacturing. Additionally, Graphene Manufacturing Group (GMG) in Australia, which produces graphene from natural gas, is exploring sustainable production pathways, with ongoing efforts in 2024 to enhance environmental efficiency. In Germany, the Fraunhofer Institute is actively researching sustainable graphene production methods, including electrolytic techniques that aim to minimize chemical waste, underscoring the push toward cleaner manufacturing technologies.

Industry Expansions & Strategic Partnerships: Commercial Momentum

Industry expansions and strategic partnerships have defined the commercial momentum of this market segment. NanoXplore’s strategic scale-up in Canada, initiated in 2023, aims for a multi-fold increase in capacity, positioning the company as a key supplier for automotive and aerospace markets seeking reliable graphene supply chains. First Graphene’s continuous efforts to reduce production costs, achieving competitive pricing in 2024, mark a significant threshold for economic viability in mass-market applications. Graphenea’s ongoing provision of wafer-scale graphene is strategically positioning graphene in semiconductor research and development. Lyten in the United States, utilizing advanced plasma synthesis methods, continues to produce graphene tailored specifically for EV battery applications, demonstrating significant progress in 2024 toward sustainable manufacturing by running its 3DG Graphene manufacturing and Lithium-Sulfur pilot battery line entirely on renewable power.

Research Breakthroughs (2024-2025): Redefining Production Possibilities

Research breakthroughs between 2024 and 2025 are revolutionizing graphene production methods, opening new possibilities for scalable, high-quality, and sustainable manufacturing. Innovations in continuous growth techniques, AI-driven processes, and greener production routes are setting the stage for broader commercial adoption.

-

The University of Manchester (UK) is making significant strides in continuous CVD production of graphene sheets with low defect rates, crucial for achieving consistent high-performance materials for electronics and composites.

-

KAIST (South Korea) advanced AI-optimized material growth processes in 2023, enabling faster, more efficient production of high-quality graphene materials.

-

Tsinghua University (China) and other research groups are developing eco-friendly production methods like supercritical CO₂ exfoliation, which avoids harsh solvents and lowers the environmental impact of graphene manufacturing.

Competitive Landscape of the Graphene Production Technologies Market

The graphene production technologies market represents the backbone of the global graphene industry, defining the scalability, purity, and cost-efficiency of graphene materials across diverse applications. From chemical vapor deposition (CVD) for large-area films to liquid-phase and electrochemical exfoliation for nanoplatelets and dispersions, producers are innovating to deliver consistent, high-quality graphene for advanced composites, batteries, electronics, and industrial applications. As industries increasingly adopt graphene for lightweighting, thermal management, and energy storage, competition among manufacturers revolves around technological differentiation, production capacity, and strategic partnerships.

NanoXplore Inc.: Proprietary LPE for Nanoplatelets

In North America, NanoXplore Inc. leverages its proprietary liquid-phase exfoliation (LPE) process to produce GrapheneBlack® nanoplatelets, serving the plastics, battery, and coatings markets. With strategic shareholder Martinrea International, and ongoing collaborations with major industrial and automotive players like Siemens and Volkswagen for developing graphene-enhanced components, NanoXplore is scaling production to meet rising demand.

Haydale Graphene Industries Plc (UK): Plasma Functionalization & Printed Electronics

The UK’s Haydale Graphene Industries specializes in plasma functionalization technology, creating highly dispersible graphene inks and HDPlas® materials for aerospace composites and printed electronics. Haydale’s engagement with the aerospace supply chain, including past developmental work with companies like Boeing, and the launch of graphene-enhanced 3D printing filaments signal how functionalized graphene is unlocking new manufacturing possibilities.

Graphenea S.A.: Global Leader in CVD Graphene Films & GO

Europe’s Graphenea remains a global leader in producing CVD graphene films and graphene oxide (GO), supplying industries ranging from flexible electronics to biomedicine. With a new U.S. facility opened in 2023, Graphenea is expanding its footprint to provide high-quality graphene materials for advanced research and development to key players in the semiconductor industry, including those exploring applications in quantum computing and advanced photonics.

Directa Plus S.p.A: Eco-Friendly Plasma Exfoliation (G+® graphene)

In Italy, Directa Plus employs plasma exfoliation to produce its eco-friendly G+® graphene, widely used in tires, textiles, and composites, collaborating with partners like Versalis (Eni Group) and Pirelli to integrate graphene into sustainable industrial materials.

2D Carbon Graphene Material (China): Pioneering Roll-to-Roll CVD

Asia-Pacific players are rapidly scaling production for high-volume industrial markets. China’s 2D Carbon Graphene Material is pioneering roll-to-roll CVD technology for large-area graphene films, targeting applications ranging from EV batteries to 5G thermal management. They are actively positioning themselves to supply leading manufacturers in sectors like EV and consumer electronics.

SixCarbon Technology (China): Electrochemical Exfoliation for Heating Films & Supercapacitors

SixCarbon Technology, also in China, focuses on electrochemical exfoliation to produce graphene heating films and supercapacitor materials, expanding mass production capacity in Shenzhen.

First Graphene Ltd.: Electrochemical Exfoliation for PureGRAPH

In Australia, First Graphene uses electrochemical exfoliation for scalable PureGRAPH® production, targeting composites and anti-corrosion coatings, while Graphene Manufacturing Group (GMG) employs its patented electrochemical GraphEnergy process to produce graphene for aluminum-ion batteries and thermal pastes, partnering with Rio Tinto for sustainable graphite sourcing.

Paragraf (UK): Unique Wafer-Scale CVD Technology

Meanwhile, the UK’s Paragraf stands out with its unique wafer-scale CVD technology, producing 8-inch graphene wafers for precision sensors and quantum devices. They are engaged in strategic development efforts with leading technology companies like ARM and Siemens to advance next-generation electronics.

Market Dynamics – Graphene Production Technologies Industry: Key Trends & Opportunities (2025–2034)

Trend: Plasma-Enabled Scalable Synthesis Drives High-Quality, Industrial-Scale Graphene Production

The Graphene Production Technologies Industry is undergoing a major transformation as plasma-enabled synthesis methods gain traction for their scalability, speed, and product quality effectively overcoming many limitations of traditional graphene manufacturing processes. A prime example is plasma jet deposition, a cutting-edge approach that allows for single-step synthesis of high-purity, monolayer graphene at atmospheric pressure, without the need for metal catalysts. This breakthrough eliminates complex and costly transfer steps, while achieving more than 95% monolayer purity at rates up to ten times faster than conventional chemical vapor deposition (CVD). Industry pioneers like Graphene Manufacturing Group (GMG) have already commercialized this technology, operating a modular graphene production plant that has exceeded initial expectations, and are advancing towards a second-generation plant with an initial production capacity of one tonne of graphene per year expected by mid-2026 an achievement that is paving the way for mass-market applications across electronics, composites, and energy storage.

The push for sustainability is equally strong, as microwave plasma exfoliation emerges as a revolutionary method for upcycling waste plastics and biomass directly into graphene. This process not only slashes processing times achieving conversion in as little as 30 seconds compared to hours for legacy Hummers’ methods but also consumes 80% less energy than thermal reduction techniques. Versarien, with its Nanene® product line, is leveraging microwave plasma exfoliation to bring industrial-grade graphene flakes to market, with the aim of achieving production costs below $50 per kilogram, thereby dramatically lowering the barrier for widespread industry adoption. Together, these plasma-based and waste-to-graphene technologies are positioning the Graphene Production Technologies Market for accelerated growth and expanded accessibility, enabling high-quality graphene to move rapidly from pilot plants to large-scale commercial supply chains.

Opportunity: AI-Optimized Graphene Synthesis Unlocks Tailored Properties and Next-Gen Applications

The next frontier for the Graphene Production Technologies Industry lies in harnessing artificial intelligence (AI) and machine learning to achieve property-specific, on-demand graphene synthesis. AI-driven closed-loop process control is now being integrated into manufacturing lines, where real-time feedback from advanced Raman spectroscopy allows for precise tuning of plasma parameters to target specific graphene characteristics such as defect density (achieving ID/IG ratios below 0.1) and customizable layer counts ranging from single-layer to ten-layer graphene. Graphenea, for instance, is at the forefront of exploring AI-powered reactor technologies aimed at consistently delivering batches with high precision, striving for minimal variation in targeted properties, ensuring both reliability and quality at scale.

Materials acceleration platforms, such as those pioneered by Citrine Informatics, are further revolutionizing the landscape by rapidly discovering and optimizing new graphene derivatives with tunable properties. These platforms have identified a dozen novel forms of graphene with adjustable bandgaps and a wide range of hydrophilicity, tailored for specific industry needs. The commercial impact is immediate: leading technology companies, including Intel, are actively researching and prototyping graphene-based heat spreaders with engineered anisotropic thermal conductivity. This demonstrates how AI-optimized production holds the potential to move from laboratory breakthroughs to real-world, high-value electronics applications. This fusion of scalable plasma technologies and AI-powered customization is positioning the Graphene Production Technologies Market at the forefront of next-generation advanced materials manufacturing, promising cost-effective, high-performance, and application-specific graphene products for the global industry.

Market Share and Segmentation Analysis: Graphene Production Technologies Market

By Technology: CVD Dominates, Plasma Methods Accelerate as Future Growth Engine

In 2025, chemical vapor deposition (CVD) leads the market with a 38.7% share, driven by its proven ability to produce high-purity graphene for electronics, photonics, and advanced research applications. The scalability and product quality of CVD have made it the industry’s technology of choice, particularly for semiconductor and display manufacturing. Plasma methods, though still a smaller segment, are the fastest-growing technology, unlocking low-temperature, scalable production pathways increasingly favored for flexible electronics and cost-sensitive applications. Liquid-phase exfoliation (LPE) and electrochemical exfoliation continue to play vital roles, offering versatile, scalable options for composites, coatings, and energy devices.

.png)

By Application: Electronics & Photonics Lead, Energy Storage Expands Fastest

The energy storage segment is set for the fastest growth with a CAGR of 31.4%, as advancements in graphene-enhanced battery and supercapacitor anodes enable higher capacity, faster charging, and improved safety fueling mass adoption in electric vehicles and renewable energy systems. Composites and coatings are also expanding, as industrial users embrace graphene’s conductivity, durability, and anti-corrosive properties. Electronics and photonics applications account for largest share in 2025, reflecting strong uptake in flexible displays, transistors, and 5G antennas

By Scale of Production: Industrial Scale Leads, Pilot Scale Bridges R&D to Commercialization

Industrial and commercial-scale production now represents 43.4% of the market, as manufacturers move beyond lab prototypes to scalable, cost-efficient output using CVD and LPE techniques. Pilot-scale production continues to be crucial, bridging the gap between R&D and market entry, particularly as companies refine processes and test commercial viability. Research and lab-scale activities are gradually declining in market share, as the focus shifts to scalable, real-world production methods that support expanding commercial demand.

China Leading Global Scale-Up in Graphene Production Technologies for Electronics and Energy

China holds a commanding position in the global graphene production technologies market, accounting for roughly 60 percent of global supply thanks to its robust, government-supported innovation ecosystem and industrial scale. Major funding over $1 billion channeled through the Ningbo Graphene Innovation Center has powered research breakthroughs at the Chinese Academy of Sciences (CAS), such as roll-to-roll CVD graphene, which now underpins a new generation of flexible electronics and advanced battery solutions. Key commercial applications include flexible displays for BOE and Huawei, high-performance battery anodes for CATL, and thermal management films for consumer and industrial devices. In 2024, The Sixth Element launched high-conductivity graphene sheets targeting the electronics and energy storage sectors, while Jiangsu Cnano’s expansion to 5,000 tons per year of graphene nanoplatelets has made large-scale, cost-effective supply a reality. With BYD integrating CVD graphene into next-generation solid-state battery prototypes, China is setting the global standard for both the technology and its application, driving innovation in EVs, wearables, and industrial systems.

United States Accelerating Commercialization of CVD, LPE, and Plasma Graphene for Advanced Industries

The United States is rapidly scaling its graphene production technologies by combining strong public funding, university-led R&D, and an agile start-up ecosystem. The Department of Energy’s allocation of $75 million under the CHIPS Act has given a boost to both CVD and electrochemical (LPE) production for advanced applications in semiconductors, aerospace, and next-gen batteries. MIT’s achievement of defect-free graphene using AI-controlled CVD reactors has set a new industry benchmark for consistency and quality, especially for electronics and chip manufacturing. Commercialization is also gathering pace, with Nanotech Energy’s launch of non-toxic, liquid-phase exfoliated graphene in 2024 for energy storage and coatings markets. Meanwhile, Graphenea’s opening of a new CVD production facility in Massachusetts is strengthening domestic supply chains and export capacity. NASA is now testing plasma-synthesized graphene for spacecraft shielding, demonstrating the material’s relevance from earthbound industries to outer space. This unique blend of academic excellence, manufacturing scale, and federal funding is driving the United States toward global leadership in high-quality, application-ready graphene production.

South Korea Integrating Advanced Graphene Synthesis for Displays, Batteries, and Sensors

South Korea continues to push the boundaries in graphene production technologies, especially for the electronics and automotive sectors. Samsung’s $300 million investment in CVD graphene production for foldable OLED displays is fueling the world’s most advanced consumer devices, while KAIST’s breakthroughs in laser-assisted graphene synthesis are paving the way for even more precise and scalable production methods. Applications are rapidly expanding to include high-performance displays, LG Chem’s EV batteries, and advanced sensors for IoT and automotive systems. LG Chem’s 2024 launch of ultra-thin graphene films exemplifies the country’s ability to quickly translate lab-scale innovations into market-ready products. SK Innovation’s collaboration with Tesla on graphene-enhanced battery current collectors demonstrates South Korea’s capacity to influence the future of global EV battery technology. The synergy between world-leading research, tech giants, and cross-sector adoption keeps South Korea firmly at the forefront of graphene production innovation.

United Kingdom Driving Sustainable and Functional Graphene Production for Aerospace and Energy

The United Kingdom is a recognized innovator in sustainable and functional graphene production methods, blending top-tier academic research with commercial deployment. The University of Manchester’s patented laser-scribed graphene techniques, along with £40 million in EPSRC funding for green synthesis, highlight the country’s focus on both efficiency and environmental responsibility. Key applications extend from aerospace where BAE Systems is leveraging graphene for lightweight, high-strength materials to wearable electronics and energy storage devices. Haydale’s 2024 launch of functionalized graphene inks is enabling the next generation of printed electronics, while Rolls-Royce is now testing graphene thermal coatings to boost jet engine efficiency and durability. With a focus on sustainable synthesis, cross-industry partnerships, and pilot programs, the UK is creating a resilient, future-proof graphene technology ecosystem.

Germany Advancing Cost-Effective and High-Purity Graphene Production for Automotive and Industrial Sectors

Germany’s advanced materials sector is making significant strides in plasma-enhanced CVD, chemical synthesis, and the scale-up of graphene oxide production. The Fraunhofer IWS has optimized plasma-enhanced CVD to reduce production costs and increase purity, supporting downstream use in fuel cells, automotive systems, and smart industrial sensors. BASF is ramping up graphene oxide output for high-performance coatings, especially for automotive brands like BMW and industrial heavyweights like Siemens. SGL Carbon’s 2024 introduction of graphene-enhanced graphite foils and Bosch’s ongoing R&D into graphene MEMS microphones reflect Germany’s emphasis on applied research and market-readiness. Germany’s rigorous approach to quality, cost-efficiency, and scale ensures that its graphene production technologies remain competitive on the world stage.

Japan Scaling Epitaxial and Hybrid Graphene Technologies for Electronics and Robotics

Japan is accelerating its investment in a diverse range of graphene production technologies, including epitaxial growth, CVD, and hybrid composites. AIST’s breakthroughs in high-mobility graphene grown via epitaxy have opened new doors for advanced electronics, with potential applications in everything from high-frequency semiconductors to precision medical devices. Toray Industries’ ¥200 billion investment in graphene-carbon fiber hybrids supports the global automotive and aerospace supply chains, especially in lightweighting and performance improvement. In 2024, Fujifilm’s launch of graphene-based X-ray detectors marks a significant milestone in imaging technology, while Panasonic’s ongoing work on graphene speakers for premium audio products highlights cross-industry opportunities. Japan’s manufacturing discipline, research leadership, and willingness to commercialize breakthrough technologies place it among the most influential markets for graphene production.

Canada Pioneering Methane Pyrolysis and High-Volume Nanoplatelet Production for Clean Tech

Canada is establishing itself as a key player in cost-effective and environmentally sustainable graphene production, led by the National Research Council’s patented methane pyrolysis process. This method, which generates high-quality graphene from methane with minimal emissions, is gaining traction in both local and export markets. NanoXplore’s production of 20,000 tons per year of graphene nanoplatelets is helping to meet the growing needs of EV manufacturing, aerospace, and the construction industry. Grafoid’s commercialization of graphene-enhanced concrete in 2024 illustrates the expanding role of graphene in infrastructure and green building materials. Hydro-Québec’s ongoing tests of graphene in solid-state batteries reinforce Canada’s position as an innovator in energy storage solutions. The integration of advanced production methods, industrial partnerships, and cleantech orientation gives Canada a sustainable competitive edge in the global graphene sector.

Australia Leading in Biomass-Derived and Composite Graphene Technologies for Industry and Energy

Australia is emerging as a leader in sustainable and application-driven graphene production, with CSIRO pioneering the conversion of agricultural waste into high-quality graphene an industry first. This approach not only reduces costs but also supports Australia’s broader sustainability goals, opening up new opportunities for domestic and export-oriented supply chains. Graphene Manufacturing Group (GMG) is expanding production of graphene-aluminum composites for industrial applications, targeting mining equipment, renewable energy systems, and medical devices. Imagine IM’s 2024 release of graphene-coated industrial wear parts demonstrates how graphene production is directly improving durability and operational life across key sectors. ANSTO’s ongoing research on graphene’s use in nuclear reactor shielding underscores the nation’s commitment to cutting-edge energy and safety applications. With a unique focus on resource efficiency, cleantech, and industry collaboration, Australia is positioned as a key supplier in the Asia-Pacific graphene technology market.

Graphene Production Technologies Market Report Scope

Graphene Production Technologies Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$115.4 Million

|

|

Market Size (2034)

|

$970.9 Million

|

|

Market Growth Rate

|

26.7%

|

|

Segments

|

By Type (Gyromitra, Regular Morels, Half-Free Morels, Verpas), By Application (Household, Food, Traditional Medicine), By Sales Channel (Online, Offline)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NanoXplore Inc. (Canada), CVD Equipment Corporation (USA), The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), First Graphene Ltd. (Australia) , Haydale Graphene Industries Plc (UK), Graphenea S.A. (Spain), Global Graphene Group (USA), Universal Matter Inc. (Canada), Vorbeck Materials Corp. (USA), Thomas Swan & Co. Ltd. (UK), Directa Plus S.p.A (Italy), Graphene Manufacturing Group (Australia), Versarien Plc (UK), 2D Carbon Graphene Material (China), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology

- Chemical Vapor Deposition (CVD)

- Mechanical Exfoliation

- Liquid-Phase Exfoliation (LPE)

- Electrochemical Exfoliation

- Reduction of Graphene Oxide (rGO)

- Plasma Methods

- Others

By End Product Form

- Graphene Sheets/Films

- Graphene Nanoplatelets (GNPs)

- Graphene Oxide (GO)

- Graphene Powder/Flakes

- Graphene Quantum Dots (GQD)

By Application

- Electronics & Photonics

- Energy Storage

- Composites

- Coatings

- Others

By Scale of Production

- Research & Lab Scale

- Pilot Scale

- Industrial/Commercial Scale

By End-Product Quality

- High-Purity / Research Grade Graphene

- Industrial Grade Graphene

- Functionalized Graphene

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Production Technologies Market: Profiles & Strategies

- NanoXplore Inc. (Canada)

- CVD Equipment Corporation (USA)

- The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China)

- First Graphene Ltd. (Australia)

- Haydale Graphene Industries Plc (UK)

- Graphenea S.A. (Spain)

- Global Graphene Group (USA)

- Universal Matter Inc. (Canada)

- Vorbeck Materials Corp. (USA)

- Thomas Swan & Co. Ltd. (UK)

- Directa Plus S.p.A (Italy)

- Graphene Manufacturing Group (Australia)

- Versarien Plc (UK)

- 2D Carbon Graphene Material (China)

* List Not Exhaustive

Methodology

The analysis in this report is based on a multi-step research methodology combining primary and secondary data sources. Extensive secondary research included reviewing technical papers, patents, company reports, press releases, government publications, and recognized industry databases to identify trends, production techniques, and market dynamics across graphene production technologies. Primary research involved in-depth interviews and surveys with executives, R&D leaders, technology specialists, and decision-makers from key graphene manufacturers, equipment suppliers, research institutes, and end-user industries worldwide. Market sizing and forecast calculations leveraged bottom-up approaches, triangulated with top-down validation, considering market drivers, adoption rates, pricing trends, and technology scaling factors. The report also integrates proprietary insights from USDAnalytics’ internal databases, ensuring accurate, up-to-date intelligence across regions and segments. Rigorous data verification processes and cross-validation were applied to deliver highly reliable market estimates and insights for stakeholders planning strategic investments in graphene production technologies.

Research Coverage

- Technologies Covered: Chemical Vapor Deposition (CVD), Mechanical Exfoliation, Liquid-Phase Exfoliation (LPE), Electrochemical Exfoliation, Reduction of Graphene Oxide (rGO), Plasma Methods, and other emerging techniques.

- End Product Forms: Graphene Sheets/Films, Graphene Nanoplatelets (GNPs), Graphene Oxide (GO), Graphene Powder/Flakes, Graphene Quantum Dots (GQD).

- Applications: Electronics & Photonics, Energy Storage, Composites, Coatings, and Others.

- Scale of Production: Research & Lab Scale, Pilot Scale, Industrial/Commercial Scale.

- End-Product Quality: High-Purity / Research Grade Graphene, Industrial Grade Graphene, Functionalized Graphene.

- Geographic Scope: 21 countries spanning North America, Europe, Asia Pacific, South America, Middle East & Africa.

- Company Profiles: Strategic developments and technologies of 18 leading graphene producers and technology innovators.

Deliverables

- Detailed market size estimates and forecasts for 2025–2034 by technology, product form, application, production scale, end-product quality, and country.

- Analysis of technology trends and commercialization readiness for each graphene production method.

- Competitive profiling and benchmarking of key manufacturers.

- Insights into production economics, capacity expansions, and sustainability trends.

- Regional and country-level demand analysis highlighting market opportunities.

- Strategic recommendations for stakeholders to capture growth opportunities in graphene production technologies.