Graphene Nanoplatelets Market Overview: Growth Drivers & Trends

Market Valuation and Growth Projections (2025-2034)

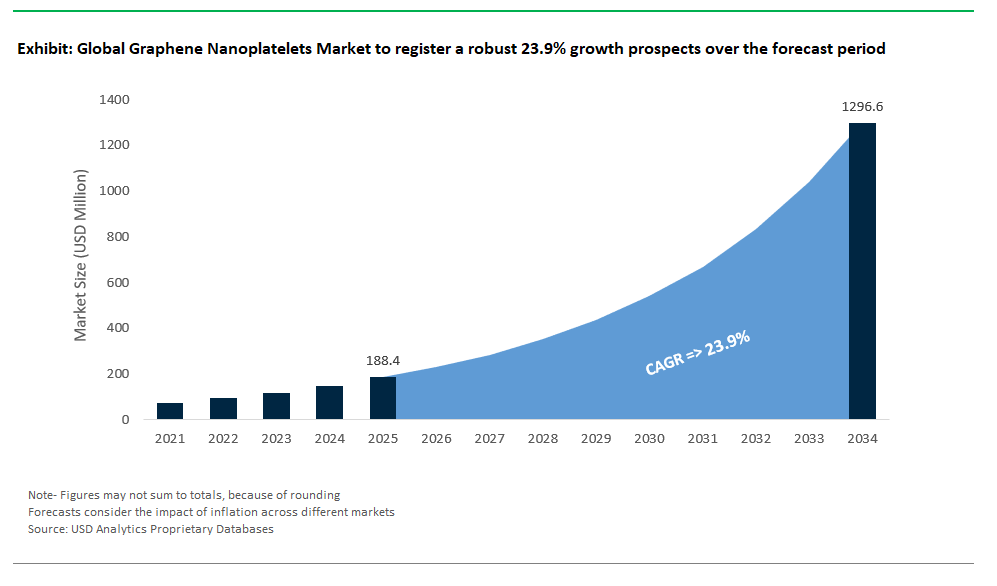

The graphene nanoplatelets (GNPs) market is poised for significant expansion between 2025 and 2034, driven by accelerating demand across industries such as aerospace, automotive, energy storage, electronics, and high-performance coatings. Industry analysts project the market to grow at a robust CAGR of 32.1%, potentially reaching a valuation of USD 188.4 million in 2025 to USD 1296.4 million by 2034. GNPs are emerging as a crucial nanomaterial bridging the gap between the exceptional properties of single-layer graphene and the cost-effectiveness and scalability required for industrial applications.

Building on USDAnalytics’ proprietary datasets, the eighth edition of the Graphene nanoplatelets market delivers a comprehensive analysis and outlook of the graphene industry, spanning 21 countries and 14 companies- By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents), By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial), By Form (Powder, Dispersions, Masterbatches), By Grade (M-Grade, C-Grade, H-Grade, Others), By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets).

This report provides a comprehensive analysis of the graphene nanoplatelets market, exploring the intricate relationship between GNP structural and physical properties and their commercial adoption across diverse sectors. It delivers critical insights into market dynamics, competitive landscapes, emerging application trends, and strategic opportunities for stakeholders seeking to capitalize on GNPs’ transformative potential in advanced materials markets through 2034.

Key Properties and Advantages of GNPs for Industrial Applications

Graphene nanoplatelets (GNPs) feature thicknesses of 3–100 nanometers and lateral sizes of 1–25 micrometers, resulting in high aspect ratios that boost mechanical, thermal, and electrical properties in composites. While GNPs have less surface area than monolayer graphene, they offer an optimal mix of performance and affordability for industrial use. In energy storage, GNPs enable lithium-ion battery anodes with capacities up to 500 mAh/g and supercapacitor electrodes with capacitances around 200 F/g, outperforming standard materials. For coatings, GNPs provide up to 99% better corrosion resistance and significantly extend UV protection in paints and barriers. The market’s main challenges include achieving uniform dispersion in polymers, managing potential health risks, and lowering production costs, which are still higher than alternatives like carbon black.

Market Analysis: Graphene Nanoplatelets (GNPs) Industry Developments & Innovations

The graphene nanoplatelets (GNPs) market is rapidly evolving into a crucial segment of the advanced materials landscape, fueled by significant production scale-ups and a surge of commercial applications spanning composites, energy storage, coatings, and construction. Between 2024 and 2025, GNPs have firmly transitioned from niche research materials to industrial-scale solutions, underpinned by technological breakthroughs and growing confidence in their performance benefits.

GNP Production Scale-Ups & Cost Reduction Initiatives (2023-2025)

On the production and scalability front, multiple manufacturers have expanded capacity to meet growing demand across sectors. NanoXplore in Canada ramped up its operations in 2024, achieving an impressive production milestone of 10,000 tonnes per year of GNPs at its Quebec facility. This strategic expansion positions NanoXplore as one of the largest commercial producers globally, focused on supplying high-volume markets such as polymer composites and lithium-ion batteries. In Australia, First Graphene increased the scale of its PureGRAPH® GNPs production in 2023, targeting applications in concrete, coatings, and polymer manufacturing. Meanwhile, Graphene Leaders Canada (GLC) has advanced a low-cost electrochemical exfoliation method for producing high-quality GNPs, a development in 2023 that aims to lower barriers to large-scale adoption by reducing manufacturing costs and ensuring consistent material quality.

Expanding Commercial Applications of GNPs Across Industries

Commercial applications of GNPs have expanded substantially across diverse industries. In composites and polymers, Versarien in the UK introduced GNP-enhanced thermoplastics in 2023 for aerospace and automotive lightweighting, capitalizing on GNPs’ ability to significantly improve mechanical strength and thermal conductivity without adding substantial weight.

Graphene Nanoplatelets for Enhanced Energy Storage: Batteries & Supercapacitors

In the realm of energy storage, GNPs are increasingly recognized as key additives for enhancing electrode performance. Skeleton Technologies, operating between Estonia and Germany, has incorporated GNPs into its “Curved Graphene” supercapacitors, achieving power densities reportedly four times higher than conventional devices by 2023. This leap in performance is vital for sectors requiring rapid charge-discharge cycles and high power bursts, including grid stabilization and heavy-duty transport. Talga Group, with operations in Sweden and Australia, developed GNP-based conductive additives in 2024 for lithium-ion batteries, aiming to improve conductivity and energy efficiency, which is crucial for the growing electric vehicle market.

Advanced Coatings & Thermal Management Solutions with GNPs

Coatings and thermal management are also proving fertile ground for GNP innovation. In 2023, Graphene Manufacturing Group (GMG) commercialized its GNP-based THERMAL-XR® coatings, designed to enhance HVAC energy efficiency by improving heat transfer and reducing operational energy consumption. Directa Plus in Italy is active in supplying GNPs for advanced coatings, including those with properties relevant for automotive and aerospace applications like anti-corrosion and potential anti-icing functionalities.

GNP-Reinforced Concrete & Sustainable Building Materials

GNP-reinforced concrete solutions are being deployed globally, with demonstrated capabilities of achieving significant increases in compressive strength, such as 30% increase in compressive strength a significant development for infrastructure resilience and longevity. Similarly, Graphenstone in Spain has brought eco-friendly, GNP-enhanced paints to market in 2024, combining antimicrobial properties with environmental sustainability, thus catering to both health-conscious consumers and green building initiatives.

Emerging Research & Breakthroughs in Graphene Nanoplatelet Technologies

Beyond commercial deployment, research breakthroughs between 2024 and 2025 have continued to unlock new frontiers for GNPs. At MIT in the United States, researchers demonstrated GNP-infused epoxy composites capable of self-healing, representing a transformative step forward in extending the lifespan of structural components in various industries. The University of Manchester in the UK, in 2023, made strides in improving GNP dispersion techniques, a critical factor for maximizing mechanical reinforcement in polymer composites. Meanwhile, the Fraunhofer Institute in Germany leveraged GNPs in printed electronics during 2024, developing flexible sensors that promise new applications in wearable devices, automotive interiors, and smart packaging.

Competitive Landscape of the Global Graphene Nanoplatelets (GNPs) Market

The graphene nanoplatelets (GNPs) market has matured into one of the most commercially viable segments within the broader graphene industry, as manufacturers across sectors—from batteries and composites to coatings and thermal management—seek advanced materials offering exceptional conductivity and mechanical reinforcement. GNPs strike a balance between performance and scalability, making them attractive for industrial-scale applications where cost and consistency are crucial. Industry players are increasingly focused on developing specialized GNP grades tailored for different end uses, fueling competition and technological differentiation in the market.

North America GNP Market: Leading Manufacturers & Strategic Partnerships

The North American landscape is prominently shaped by NanoXplore Inc. in Canada. NanoXplore is a leading producer of GrapheneBlack® GNPs, focusing on high-volume applications in industries like automotive. The company's significant production capacity, which reached 4,000 metric tons per year in 2023 with plans for expansion to 20,000 tons per year by 2027 at its Montreal facility, positions it as a major global supplier. NanoXplore's strategic partnerships, notably with Martinrea International for automotive parts and its announced collaboration with Volkswagen to develop graphene-enhanced plastic parts, highlight its deep integration into the EV and high-volume manufacturing sectors. Regarding XG Sciences, it was acquired by Cabot Corporation in 2021, and its operations were integrated. While Cabot now offers a portfolio of conductive carbon additives, the original XG Sciences standalone entity effectively ceased independent operations following the acquisition and integration. This has indeed left a more consolidated market, with NanoXplore as a dominant North American player.

European GNP Players: Specialization & Commercialization

In Europe, Directa Plus in Italy and Avanzare Innovación Tecnológica in Spain are pushing GNPs into high-value, specialized markets. Directa Plus is notable for its G+® nanoplatelets, which enhance conductive inks, coatings, and textiles. They have established partnerships with brands like Colmar for sportswear and Versalis for rubber and plastic compounds, showcasing successful commercialization in consumer and industrial goods. Avanzare Innovación Tecnológica focuses on a range of advanced materials, including graphene, for industrial applications. While they engage in various collaborative projects, a specific, directly verifiable collaboration with the European Space Agency for leveraging GNPs for demanding aerospace environments, as a distinct 2023-2024 development, was not explicitly detailed in recent public information. However, their focus on high-performance materials makes such applications highly plausible. The UK’s Thomas Swan complements this landscape with its Elicarb® GNPs, which are indeed used in diverse applications, including sports equipment and automotive components, showcasing how European firms are translating graphene research into commercial products with niche, high-performance applications.

Asia-Pacific & Australia GNP Market Dynamics: Key Innovations

Meanwhile, First Graphene in Australia and Global Graphene Group (G3), spanning the US and Asia, add further depth to the competitive landscape. First Graphene's PureGRAPH® GNPs target sustainable construction and battery applications. Their efforts in reducing CO₂ emissions in concrete through graphene integration are well-documented, and they continue to expand their focus on energy storage applications. Global Graphene Group (G3) remains a significant player, particularly in the US and Asian markets, supplying various GNP products, including powders and films for batteries, conductive inks, and flexible electronics, leveraging its early pioneering work in GNP production.

Market Dynamics – Graphene Nanoplatelets (GNPs) Market: Key Trends & Opportunities

Trend: Rising Adoption of Graphene Nanoplatelets in Lightweight Composite Materials

The Graphene Nanoplatelets (GNPs) market is witnessing rapid growth as industries seek stronger, lighter, and more cost-effective materials. GNPs are transforming how composites are designed, delivering performance benefits across aerospace, automotive, electronics, and packaging. Their unique properties are positioning them as indispensable additives for next-generation high-performance materials.

-

Graphene nanoplatelets improve the strength-to-weight ratio of composites, where adding just 1–5% GNPs can boost tensile strength by 30–50%, driving interest from aerospace leaders like Boeing and Airbus and automotive innovators like Tesla for lightweight structures and battery enclosures.

-

GNPs offer exceptional thermal conductivity, enhancing heat dissipation in materials by up to 200%, supporting safer EV battery housings and advanced thermal management in electronics.

-

Thin graphene nanoplatelet coatings serve as effective barriers against oxygen and moisture for extended food shelf life, while GNPs remain cost-efficient ($50–200/kg) compared to carbon fiber, expanding their adoption in diverse industries including automotive, aerospace, electronics, and packaging.

Opportunity: Scalable, Sustainable Production of Graphene Nanoplatelets (GNPs)

The production landscape for Graphene Nanoplatelets (GNPs) is rapidly evolving toward scalability and sustainability, unlocking new pathways for mass-market adoption. Advances in greener production methods and circular economy applications are transforming GNPs from niche materials into widely viable solutions. Companies and researchers alike are driving breakthroughs that promise significant cost reductions and environmental benefits.

-

Sustainable production methods, such as using biomass and waste carbon sources by Graphene Leaders Canada and Versarien, are targeting GNP costs below $20/kg, while NanoXplore’s liquid-phase exfoliation achieves ton-scale output with lower energy consumption.

-

Innovative applications like smart concrete with self-sensing capabilities for structural health monitoring and GNP-reinforced polymers that maintain performance over multiple recycling cycles are supporting sustainability goals, particularly in green construction and circular economy initiatives.

-

Market potential for green GNPs is significant, with projections that even a 5% share of the global carbon additives market by 2030 could generate over $1 billion in annual revenues, driven by demand in construction, automotive electrification, and advanced consumer products.

Graphene Nanoplatelets (GNPs) Market Share & Segmentation Analysis

Composites Dominate GNP Applications; Energy & Power Lead Growth

Composites represent the leading application for graphene nanoplatelets, capturing an estimated 34.8% of the market in 2025. This dominance is propelled by the push for lightweight, high-strength materials across aerospace and automotive manufacturing, where GNPs offer exceptional reinforcement and conductivity. However, the fastest growth is observed in the energy & power segment, where applications in lithium-ion batteries and supercapacitors are driving a rapid shift toward high-performance, graphene-enhanced storage solutions. Thermal management solutions also draw attention as a strategic growth area, supporting the advancement of heat dissipation systems in electronics and electric vehicles.

Automotive Sector Leads GNP End-User Demand, Electronics & Energy Gaining Ground

Automotive applications stand at the forefront of GNP consumption, accounting for 33% of total demand in 2025. The integration of GNPs into tires, composites, and electronic systems is supporting the industry’s priorities for improved efficiency, durability, and reduced weight. The aerospace & defense sector is also a key end-user, leveraging GNPs for advanced composites and next-generation defense materials. Meanwhile, electronics and telecommunication, along with renewable energy and grid storage, are rapidly expanding their use of GNPs, reflecting ongoing trends toward electrification, smart infrastructure, and enhanced connectivity.

Market Share By End-User (2025).png)

China Dominates Global GNPs Market with Scale, R&D, and Battery Breakthroughs

China stands as the world’s top producer and innovator in the graphene nanoplatelets (GNPs) industry, accounting for over 60% of global supply. Government-led investments, such as the Chinese Academy of Sciences and Tsinghua University’s research into GNP composites, drive advancements across sectors. GNPs are widely deployed in conductive coatings, polymer composites, and next-generation Li-ion battery anodes, with commercial scaleups accelerating. Ningbo Morsh Tech’s 2023 launch of high-purity GNPs for battery applications set new industry standards, while The Sixth Element Materials has ramped up production capacity to 5,000 tons annually—one of the largest in the world (Sixth Element Annual Report 2023). Innovation is also evident in end-use: Huawei is now testing GNPs in thermal management solutions for 5G electronics, signaling expansion into consumer tech. These developments, underpinned by state support and continuous capacity expansions, ensure China’s enduring leadership in the GNP supply chain, from industrial to high-tech applications.

United States Scales GNP Innovation for Aerospace, Automotive, and Advanced Composites

The United States is rapidly expanding its footprint in the GNP industry through a potent mix of federal funding, university R&D, and commercial rollouts. Agencies like the DOE and NSF support projects targeting GNP-enhanced composites and energy storage, while leading research at MIT and Rice University explores GNP-based conductive inks for flexible electronics. U.S. manufacturers are pushing boundaries in aerospace (with NASA), automotive (GM), and corrosion-resistant coatings. Notably, XG Sciences—now part of Cabot Corporation—commercialized GNP-reinforced plastics in 2023, enabling lighter, stronger materials for diverse industrial uses. First Graphene USA is also scaling GNP production in Texas, catering to surging domestic demand. Lockheed Martin’s ongoing tests of GNPs for lightweight armor in 2024 reflect strong military and security interest. With public and private sectors aligned, the U.S. is leveraging GNPs for next-gen composites, EVs, and advanced protective solutions.

South Korea Advances GNPs for High-Tech Electronics and EV Batteries

South Korea is at the forefront of integrating GNPs into high-tech products, propelled by a strong R&D network and electronics manufacturing expertise. KRICT is developing GNP-based EMI shielding materials for the electronics sector, supporting giants like Samsung in the rollout of advanced devices. Key applications include high-performance battery thermal pastes for EVs and flexible heaters, as seen in Graphene Square’s 2023 launch. Industrial leaders such as Posco Chemical are investing in GNP-coated battery materials, further embedding graphene in the e-mobility value chain. KAIST’s 2024 development of ultra-thin GNP films for foldable displays marks a leap in both durability and miniaturization of next-generation electronics. South Korea’s ability to transfer GNP innovation from lab to commercial product underlines its rising influence in global graphene technology supply.

Germany Targets Automotive Lightweighting and Industrial GNP Applications

Germany’s GNP sector is distinguished by deep R&D and industrial partnerships focused on mobility and materials. The Fraunhofer Institute is at the center of efforts to optimize GNPs for lightweight automotive components, aiming to meet stringent efficiency and emissions targets. Major automakers like BMW and materials leaders such as BASF are actively testing GNPs in carbon-fiber composites to create lighter, stronger structures. SGL Carbon’s 2023 launch of GNP-reinforced graphite foils addresses both automotive and industrial needs, enabling enhanced performance in thermal and conductive applications. Mercedes-Benz’s current exploration of GNPs for next-generation brake pads (2024) highlights the broadening scope of graphene in mobility solutions. Backed by industrial expertise and technological rigor, Germany is positioning GNPs as a core enabler of future transportation and advanced manufacturing.

United Kingdom Drives Functionalized GNPs for Advanced Manufacturing and Sports Tech

The United Kingdom is harnessing functionalized GNPs for a diverse array of applications, from 3D printing to high-performance sports equipment. Research led by the University of Manchester and Haydale Graphene is advancing the use of GNPs in specialized composites and filaments. The sports industry, including Formula 1 and cycling, benefits from GNPs’ lightweight and strength properties. In 2023, Versarien introduced GNP-enhanced textiles for wearable technology, bridging advanced materials with consumer applications. Recent investments from BP into GNP-based lubricant additives (2024) signal entry into the automotive and industrial maintenance sectors. This blend of academic prowess and industrial innovation keeps the UK at the leading edge of value-added GNP applications, supporting both manufacturing competitiveness and technology leadership.

Japan Pioneers GNPs in Electronics, Adhesives, and Fuel Cell Technologies

Japan’s approach to the GNP market is marked by collaborative R&D and rapid industrialization. AIST’s work on GNP coatings for corrosion resistance is driving adoption across manufacturing and construction. Leading electronics companies, Panasonic and Sony, are trialing GNPs in flexible electronics, highlighting the push for lightweight, durable devices. In 2023, Hitachi Chemical released GNP-doped conductive adhesives that offer improved electrical connectivity for industrial assembly lines. Notably, Toyota’s 2024 patents on GNP-reinforced fuel cells underscore Japan’s commitment to next-generation automotive technologies. Supported by strong intellectual property and manufacturing scale, Japan remains a vital hub for innovative GNP applications in both consumer and industrial markets.

Canada Ramps Up GNP Production for EV Batteries and Construction Markets

Canada is quickly scaling its GNP sector through aggressive manufacturing and cross-industry adoption. NanoXplore in Montreal leads the market, producing over 20,000 tons of GNPs annually for customers in automotive (including GM partnerships) and infrastructure. Grafoid’s commercialization of GNP-enhanced concrete in 2023 is catalyzing the use of advanced materials in construction, offering increased strength and durability. The National Research Council’s (NRC) 2024 collaboration with VoltaXplore targets the integration of GNPs into battery materials for EVs, aiming to improve performance and lifecycle. Canada’s approach combines mass production, sectoral integration, and government support, positioning the country as a leading North American supplier for both energy and construction industries.

Australia Develops GNPs for Industrial, Energy, and Environmental Solutions

Australia is emerging as a force in GNP research and commercialization, leveraging strong institutions and industrial demand. CSIRO and Graphene Manufacturing Group (GMG) are pioneering GNP-based solutions for energy storage, mining, and heavy industry. In 2023, GMG launched GNP thermal sprays for industrial equipment, boosting wear resistance and operational efficiency. The University of Adelaide’s 2024 development of GNP filters for water purification illustrates the expansion into environmental technologies. Australia’s unique position as both a raw material supplier and technology innovator enables it to address a wide range of applications, from resource extraction to clean energy and environmental management.

Graphene Nanoplatelets Market Report Scope

Graphene Nanoplatelets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$188.4 Million

|

|

Market Size (2034)

|

$1296.4 Million

|

|

Market Growth Rate

|

23.9%

|

|

Segments

|

By Type (Bar Cookies, Drop Cookies, Fried Cookies, Molded Cookies, Refrigerator Cookies, Others), By Ingredient (Chocolate Chips, Butter, Peanut Butter, Others), By Sales Channel (Online, Retail Store, Bakeries and Specialty Stores, Supermarkets/Hypermarkets, Independent Retailers, Convenience Stores, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ACS Materials, CVD Equipment Corporation, Directa Plus S.p.A., Global Graphene Group, Graphene Laboratories Inc., Haydale Graphene Industries Plc, NanoXplore Inc., Thomas Swan & Co. Ltd., XG Sciences, Inc., Xiamen Knano Graphene Technology Co., Ltd., and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene Nanoplatelets Market Segmentation

- Composites

- Energy & Power

- Conductive Inks & Coatings

- Thermal Management Solutions

- Electrodes

- Sensors

- Catalysis

- Lubricants

- Adsorbents

By End-User

- Automotive

- Aerospace & Defense

- Electronics & Telecommunication

- Energy

- Building & Construction

- Sports & Consumer Goods

- Healthcare & Medical Devices

- Industrial

By Form

- Powder

- Dispersions

- Masterbatches

By Grade

- M-Grade

- C-Grade

- H-Grade

- Others

By Thickness

- Single-Layer Graphene Nanoplatelets

- Few-Layer Graphene Nanoplatelets

- Multi-Layer Graphene Nanoplatelets

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Nanoplatelets Market: Profiles & Strategies

- ACS Materials

- CVD Equipment Corporation

- Directa Plus S.p.A.

- Global Graphene Group

- Graphene Laboratories Inc.

- Haydale Graphene Industries Plc

- NanoXplore Inc.

- Thomas Swan & Co. Ltd.

- XG Sciences, Inc.

- Xiamen Knano Graphene Technology Co., Ltd.

* List Not Exhaustive

Methodology: Graphene Nanoplatelets Market Research Approach

This report on the Graphene Nanoplatelets (GNPs) market utilizes a comprehensive and rigorous research methodology combining secondary and primary data sources. Extensive secondary research was conducted using peer-reviewed scientific literature, industry association reports, company filings, and trade data to establish market size, key trends, and the competitive landscape. To validate and enrich these findings, primary research involved structured interviews and surveys with executives from leading GNP producers, material scientists, application engineers, and key end-users across sectors such as automotive, energy storage, aerospace, and electronics. Market sizing and forecasts are built using a blend of bottom-up and top-down models, cross-validated through proprietary datasets and iterative expert consultations. This robust approach ensures that the report delivers actionable insights, reliable segmentation, and future-looking growth projections for all major geographies and market segments.

Research Coverage and Deliverables

- Market Segmentation: By Application, By End-User, By Form, By Grade, By Thickness

- Geographic Coverage: Detailed analysis of 21+ countries across North America, Europe, Asia-Pacific, South America, and Middle East & Africa

- Competitive Intelligence: In-depth profiles of 14+ leading GNP manufacturers, covering product portfolios, production capacities, partnerships, R&D, and strategic initiatives

- Technology & Innovation Analysis: Coverage of production scale-ups, cost reduction strategies, advances in dispersion and functionalization, and application breakthroughs

- Market Sizing & Forecasts (2025–2034): Revenue, volume, and CAGR projections for all major segments and regions

- Strategic Insights: Analysis of trends, opportunities, regulatory environment, and sustainability initiatives

- Deliverables: Full PDF report, Excel data sheets, segment-wise charts and tables, country and company snapshots, and ongoing analyst support

Table of Contents: Graphene Nanoplatelets (GNPs) Market Overview (2021-2034)

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Graphene Nanoplatelets (GNPs) Market Landscape & Outlook (2025-2034)

2.1. Introduction to Graphene Nanoplatelets (GNPs)

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Properties and Advantages of GNPs for Industrial Applications

3. Graphene Nanoplatelets (GNPs) Industry Developments & Innovation Ecosystem

3.1. GNP Production Scale-Ups & Cost Reduction Initiatives

3.1.1. Manufacturing Capacity Expansions (e.g., NanoXplore, First Graphene)

3.1.2. Advancements in Low-Cost Production Methods (e.g., Electrochemical Exfoliation)

3.2. Expanding Commercial Applications of GNPs Across Industries

3.2.1. Composites & Polymers (Aerospace, Automotive, Lightweighting)

3.2.2. Energy Storage: Batteries & Supercapacitors

3.2.3. Advanced Coatings & Thermal Management Solutions

3.2.4. GNP-Reinforced Concrete & Sustainable Building Materials

3.3. Emerging Research & Breakthroughs in Graphene Nanoplatelet Technologies

3.3.1. Self-Healing Composites

3.3.2. Improved Dispersion Techniques

3.3.3. Flexible & Printed Electronics

4. Competitive Landscape of the Global Graphene Nanoplatelets (GNPs) Market

4.1. Key Players and Market Concentration

4.2. North America GNP Market: Leading Manufacturers & Strategic Partnerships (e.g., NanoXplore, Cabot Corporation (XG Sciences))

4.3. European GNP Players: Specialization & Commercialization (e.g., Directa Plus, Avanzare Innovación Tecnológica, Thomas Swan, Versarien)

4.4. Asia-Pacific & Australia GNP Market Dynamics: Key Innovations (e.g., First Graphene, Global Graphene Group, Ningbo Morsh Tech, The Sixth Element Materials)

5. Market Dynamics – Graphene Nanoplatelets (GNPs) Market: Key Trends & Opportunities

5.1. Trend: Rising Adoption of Graphene Nanoplatelets in Lightweight Composite Materials

5.1.1. Impact on Aerospace & Automotive (Fuel Efficiency, Durability)

5.1.2. Enhancement of Thermal Conductivity

5.1.3. Barrier Properties in Packaging

5.2. Opportunity: Scalable, Sustainable Production of Graphene Nanoplatelets (GNPs)

5.2.1. Biomass & Waste Carbon Feedstocks

5.2.2. Energy-Efficient Production Techniques (Liquid-Phase Exfoliation)

5.2.3. Green Construction & Circular Economy Initiatives

6. Graphene Nanoplatelets (GNPs) Market Share & Segmentation Analysis (2021-2034)

6.1. Market Share Analysis By Application

6.1.1. Composites (Dominant Segment Analysis)

6.1.2. Energy & Power (Fastest Growing Segment Analysis)

6.1.3. Conductive Inks & Coatings

6.1.4. Thermal Management Solutions

6.1.5. Electrodes

6.1.6. Sensors

6.1.7. Catalysis

6.1.8. Lubricants

6.1.9. Adsorbents

6.2. Market Share Analysis By End-User

6.2.1. Automotive (Leading Segment Analysis)

6.2.2. Aerospace & Defense

6.2.3. Electronics & Telecommunication

6.2.4. Energy

6.2.5. Building & Construction

6.2.6. Sports & Consumer Goods

6.2.7. Healthcare & Medical Devices

6.2.8. Industrial

6.3. Market Share Analysis By Form

6.3.1. Powder

6.3.2. Dispersions

6.3.3. Masterbatches

6.4. Market Share Analysis By Grade

6.4.1. M-Grade

6.4.2. C-Grade

6.4.3. H-Grade

6.4.4. Others

6.5. Market Share Analysis By Thickness

6.5.1. Single-Layer Graphene Nanoplatelets

6.5.2. Few-Layer Graphene Nanoplatelets

6.5.3. Multi-Layer Graphene Nanoplatelets

7. Country Analysis and Outlook of Graphene Nanoplatelets (GNPs) Market, 2021- 2034

7.1. United States: Scaling GNP Innovation for Aerospace, Automotive, and Advanced Composites

7.2. Canada: Ramping Up GNP Production for EV Batteries and Construction Markets

7.3. Mexico: Emerging applications in composites and coatings due to growing manufacturing sector.

7.4. Germany: Targeting Automotive Lightweighting and Industrial GNP Applications

7.5. United Kingdom: Driving Functionalized GNPs for Advanced Manufacturing and Sports Tech

7.6. France: Strong focus on aerospace, automotive, and electronics industries driving GNP adoption.

7.7. Spain: Increasing investments in energy storage and eco-friendly building materials, with a specialized manufacturing base.

7.8. Italy: Leveraging GNPs in advanced textiles, conductive inks, and specialized industrial applications.

7.9. Russia: Government initiatives and increasing demand from electronics and automotive sectors propelling GNP research and adoption.

7.10. Rest of Europe: Analysis of other key European markets and their contribution to GNP growth.

7.11. China: Dominance in Global GNPs Market with Scale, R&D, and Battery Breakthroughs

7.12. India: Growing demand from electronics, energy storage, and biomedical sectors, supported by government initiatives.

7.13. Japan: Pioneering GNPs in Electronics, Adhesives, and Fuel Cell Technologies

7.14. South Korea: Advancements in High-Tech Electronics and EV Batteries

7.15. Australia: Developing GNPs for Industrial, Energy, and Environmental Solutions

7.16. South East Asia: Increasing adoption in lightweight materials, electronics, and sustainable technologies across the region.

7.17. Rest of Asia: Other significant Asian markets contributing to GNP growth, including emerging manufacturing hubs.

7.18. Brazil: Rising demand from automotive and energy sectors, coupled with increasing investments in R&D for advanced materials.

7.19. Argentina: Expanding applications in composites and advanced materials, driven by industrial development.

7.20. Rest of South America: Overview of other South American countries and their evolving GNP market.

7.21. Middle East and Africa: Growing interest in GNPs for automotive, aerospace, and energy applications, with increasing R&D investments.

8. Graphene Nanoplatelets (GNPs) Market Size Outlook by Region (2025-2034)

8.1. North America Graphene Nanoplatelets (GNPs) Market Size Outlook to 2034

8.1.1. By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents)

8.1.2. By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial)

8.1.3. By Form (Powder, Dispersions, Masterbatches)

8.1.4. By Grade (M-Grade, C-Grade, H-Grade, Others)

8.1.5. By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets)

8.2. Europe Graphene Nanoplatelets (GNPs) Market Size Outlook to 2034

8.2.1. By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents)

8.2.2. By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial)

8.2.3. By Form (Powder, Dispersions, Masterbatches)

8.2.4. By Grade (M-Grade, C-Grade, H-Grade, Others)

8.2.5. By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets)

8.3. Asia Pacific Graphene Nanoplatelets (GNPs) Market Size Outlook to 2034

8.3.1. By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents)

8.3.2. By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial)

8.3.3. By Form (Powder, Dispersions, Masterbatches)

8.3.4. By Grade (M-Grade, C-Grade, H-Grade, Others)

8.3.5. By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets)

8.4. South America Graphene Nanoplatelets (GNPs) Market Size Outlook to 2034

8.4.1. By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents)

8.4.2. By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial)

8.4.3. By Form (Powder, Dispersions, Masterbatches)

8.4.4. By Grade (M-Grade, C-Grade, H-Grade, Others)

8.4.5. By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets)

8.5. Middle East and Africa Graphene Nanoplatelets (GNPs) Market Size Outlook to 2034

8.5.1. By Application (Composites, Energy & Power, Conductive Inks & Coatings, Thermal Management Solutions, Electrodes, Sensors, Catalysis, Lubricants, Adsorbents)

8.5.2. By End-User (Automotive, Aerospace & Defense, Electronics & Telecommunication, Energy, Building & Construction, Sports & Consumer Goods, Healthcare & Medical Devices, Industrial)

8.5.3. By Form (Powder, Dispersions, Masterbatches)

8.5.4. By Grade (M-Grade, C-Grade, H-Grade, Others)

8.5.4. By Thickness (Single-Layer Graphene Nanoplatelets, Few-Layer Graphene Nanoplatelets, Multi-Layer Graphene Nanoplatelets)

9. Company Profiles: Leading Players in the Graphene Nanoplatelets Market

9.1. ACS Materials

9.2. CVD Equipment Corporation

9.3. Directa Plus S.p.A.

9.4. Global Graphene Group

9.5. Graphene Laboratories Inc.

9.6. Haydale Graphene Industries Plc

9.7. NanoXplore Inc.

9.8. Thomas Swan & Co. Ltd.

9.9. Xiamen Knano Graphene Technology Co., Ltd.

9.10. Additional Prominent Players

10. Methodology

10.1. Research Scope

10.2. Market Research Approach

10.3. Data Sources (Primary and Secondary)

10.4. Market Estimation and Forecasting Model

10.5. Assumptions and Limitations

11. Appendix

11.1. Acronyms and Abbreviations

11.2. List of Tables

11.3. List of Figures