Graphene Reinforced Polymer Composites Market Overview: Dynamic Growth & Projections (2025–2034)

Market Snapshot: Key Drivers & Growth Forecasts

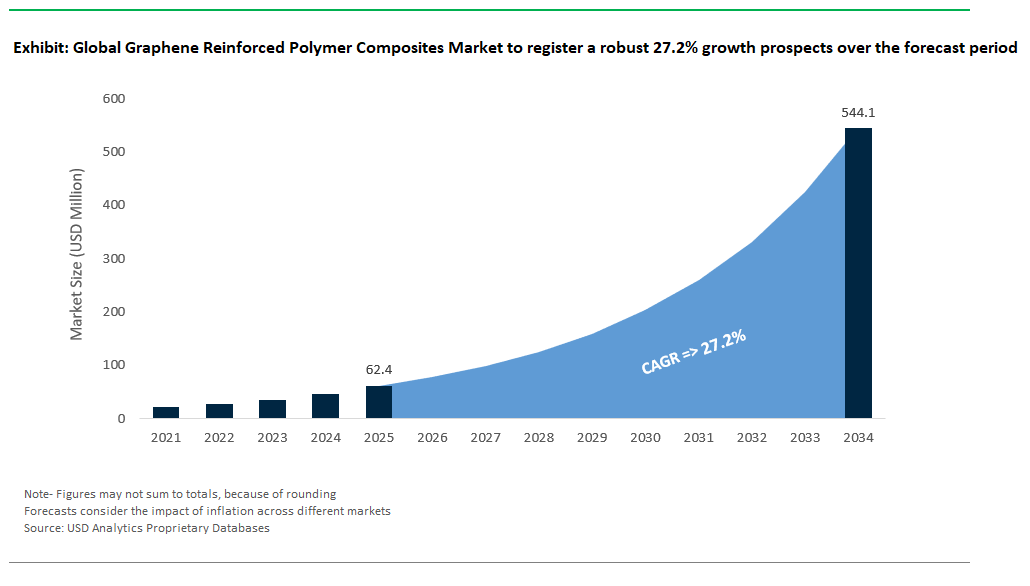

The graphene reinforced polymer composites market is entering a dynamic growth phase between 2025 and 2034, fueled by surging demand across aerospace, automotive, renewable energy, medical devices, and advanced manufacturing sectors seeking lighter, stronger, and multifunctional materials. Analysts forecast the market to grow at a compelling CAGR of 27.2%, potentially surpassing USD 544 million by 2034 from USD 62.4 million in 2025, as industries leverage graphene’s transformative properties to achieve performance levels unattainable with conventional composites.

Supported by USDAnalytics’ exclusive data resources, the ninth edition of the graphene reinforced polymer composites market report delivers in-depth insights and forecasts on the global graphene landscape, analyzing trends across 21 countries and 12 significant companies- By Application (Paints & Coatings, Electronic Components, Batteries, Solar Panels, Others), By End-User (Automotive, Medical, Aerospace, Defense, Concrete Industry, Tires, Others).

This report delivers a comprehensive analysis of the graphene reinforced polymer composites market, providing insights into market dynamics, technological advancements, competitive strategies, regulatory landscapes, and emerging innovations such as self-sensing materials and 4D-printed composite architectures. Stakeholders in aerospace, automotive, energy, and high-performance manufacturing will find critical intelligence to navigate this rapidly evolving market and capitalize on graphene’s unique capabilities through 2034.

Graphene's Advanced Properties in Polymer Composites

Graphene’s integration into polymers is driving major advances in composite materials by boosting mechanical, thermal, and electrical performance. These graphene-enhanced composites surpass traditional carbon fiber in tensile strength while maintaining lower densities, resulting in exceptional strength-to-weight ratios ideal for aerospace and wind energy. Enhanced fatigue resistance allows for up to 10⁷ load cycles, making these materials resilient under repetitive stress. Thermally, graphene composites reach through-plane conductivities of 35 W/m·K, enabling efficient heat management in EV battery enclosures and electronics. Electrically, they provide robust lightning strike protection for aerospace, meeting FAA standards by safely dissipating high currents. Market segmentation highlights how small additions of graphene in epoxies double fracture toughness for wind blades and adhesives, while polyamides and PEEK benefit from improved thermal stability and wear resistance, enabling automotive and medical applications. Flexible TPU-graphene composites also support highly stretchable electronics. Leading firms like Boeing, Porsche, Tesla, and Vestas are piloting or adopting graphene composites for next-gen aerospace, automotive, and wind energy products, capitalizing on weight reduction, faster production, and longer lifespans.

Market Analysis: Graphene Reinforced Polymer Composites Industry Acceleration & Innovation

The market for graphene reinforced polymer composites has accelerated rapidly between 2024 and 2025, moving beyond experimental research into commercially significant applications across critical industries such as automotive, aerospace, electronics, and advanced manufacturing. With graphene’s exceptional mechanical, thermal, and electrical properties, manufacturers are increasingly integrating it into polymer matrices to produce composite materials that outperform traditional alternatives in strength, durability, and multifunctionality.

Automotive & Transportation: Lightweighting & Enhanced Safety

In the automotive and transportation sector, graphene composites are transforming the fundamental design parameters for vehicle structures and components. "Lyten, based in the United States, has continued to advance its LytR™ graphene-reinforced polymer composites (unveiled in 2022), which are engineered for applications such as electric vehicle (EV) battery enclosures. These advanced materials are demonstrating the potential to reduce component weight by significant and improve impact resistance a critical factor for both passenger safety and battery protection in EVs. Meanwhile, Toyota in Japan is known for exploring advanced materials for next-generation vehicle designs, including the potential integration of graphene-enhanced carbon fiber-reinforced polymers (CFRPs) into chassis to further enhance stiffness and reduce weight further.

Aerospace & Defense: Advanced Materials for Performance & Safety

Aerospace and defense applications are equally benefiting from graphene’s unique capabilities. Companies like Haydale Graphene in the UK are actively developing flame-retardant graphene-epoxy composites for aircraft interiors, offering enhanced fire safety while maintaining low weight. These composites offer enhanced fire safety while maintaining low weight an essential balance in aviation where regulatory standards are stringent, and every kilogram saved contributes to fuel efficiency and operational costs. Lockheed Martin in the United States is actively researching and developing graphene-polyimide composites for potential use in satellite components, leveraging graphene’s properties for applications such as radiation shielding.

Electronics & Thermal Management: High-Performance Solutions

In electronics and thermal management, graphene-reinforced polymers are emerging as critical materials for managing the increasingly demanding thermal loads of modern devices. Companies like Panasonic in Japan are actively developing advanced polymer composites, including those potentially enhanced with graphene, for electronics casings to improve heat dissipation in devices like smartphones. Such materials are crucial in preventing overheating and maintaining performance as smartphones and mobile devices become more powerful. Similarly, Sixonia Tech in Germany commercialized graphene-PEEK (polyether ether ketone) composites in 2023 for use in high-temperature industrial applications, offering excellent thermal stability and mechanical robustness for demanding engineering environments, such as chemical processing or aerospace components.

Research Breakthroughs Expanding Polymer Composite Capabilities (2024–2025)

Breakthroughs from 2024 and 2025 are redefining the capabilities of graphene-reinforced polymer composites. Researchers are delivering innovations that unlock advanced functionality, superior mechanical properties, and new manufacturing possibilities across industries.

-

MIT (US) developed self-sensing graphene-epoxy composites in 2024 that can detect structural damage in real time, offering significant benefits for safety and maintenance in aerospace, automotive, and civil engineering.

-

The University of Manchester (UK) achieved record-high stiffness in graphene-polyvinyl alcohol (PVA) composites in 2023, advancing lightweight materials with exceptional mechanical properties for diverse structural applications.

-

Fraunhofer Institute (Germany) created electrically conductive graphene-PLA filaments in 2024, enabling 3D-printed electronics with integrated conductivity for flexible circuits, smart packaging, and embedded sensors.

Competitive Landscape of the Graphene Reinforced Polymer Composites Market

The graphene reinforced polymer composites market is gathering momentum as industries demand lighter, stronger, and more functional materials for automotive, aerospace, electronics, and industrial applications. Graphene’s unparalleled mechanical strength, thermal conductivity, and electrical properties make it an ideal additive to elevate polymer performance, enabling composites that deliver weight reduction, enhanced durability, and innovative functionalities like EMI shielding or thermal management. This rapidly evolving landscape is marked by intense competition among manufacturers, each focusing on specific polymer systems and industrial end uses to gain an an edge.

NanoXplore Inc.: GrapheneBlack® for Automotive & Electronics

In North America, NanoXplore Inc. leads the charge with its GrapheneBlack®-enhanced polymers. These are widely adopted in automotive applications such as plastic car parts and are actively being developed for components like battery casings and EMI shielding in electronics. NanoXplore's current production capacity stands at 4,000 metric tons per year, with plans to significantly expand to 20,000 tons per year by 2027. Its strategic partnerships, notably with Martinrea International for automotive components, underscore its influence in integrating graphene into high-volume industrial applications.

Cabot Corporation (formerly XG Sciences): Advancing xGnP® Applications

The US-based XG Sciences, now part of Cabot Corporation since its acquisition in 2021, continues to leverage its xGnP® graphene nanoplatelets for advanced polymer applications. While specific "xGnP®-reinforced epoxy systems for aerospace adhesives" or "conductive PPS compounds for fuel cell components" as recent, distinct 2024-2025 developments are not widely publicized as new launches, Cabot's portfolio includes conductive additives that can be used in such high-performance composites, including those for improved heat resistance and mechanical performance. Their participation in advanced material development, potentially through DOE-funded projects, for applications like wind turbine blade composites, aligns with their strategic focus on advanced materials.

Haydale Graphene Industries: HDPlas® for Aerospace & Industrial Applications

Europe’s competitive scene is equally vibrant, driven by specialized players targeting high-performance markets. Haydale Graphene Industries in the UK has carved out a niche in aerospace, supplying HDPlas® functionalized graphene-enhanced composites. These are designed for structural components, and Haydale has been involved in projects demonstrating their use in lightweight components for drones and other advanced applications. While a direct "Airbus A350 wingtips" specific product is not widely cited as a commercial application, Haydale's collaborations with defense and aerospace entities and participation in EU-funded aerospace projects underscore graphene’s transformative potential in aviation for high-performance and radar-absorbing composites.

Versarien: Graphene-Wear™ & 3D-Printed Composites

Similarly, Versarien is innovating with graphene composites for various industrial and automotive applications. They have developed Graphene-Wear™ formulations for composites that can reduce friction in mechanical systems, potentially suitable for industrial robotics and automotive applications like brake pads. Versarien has also been exploring 3D-printed graphene filaments, including graphene-enhanced ABS, broadening the material’s reach into advanced manufacturing.

Directa Plus: G+® for Elastomers, Textiles & Defense

Italy’s Directa Plus adds further depth to the market with a strong focus on elastomer and polyurethane composites. Its G+® elastomer composites have been developed in partnership with companies like Pirelli, demonstrating enhancements in tire treads, aiming for extended lifespan and lower rolling resistance, showcasing graphene’s ability to enhance everyday products. While a "€2.1 million contract with the Italian Ministry of Defense for ballistic composites" may refer to previous projects or ongoing engagements, Directa Plus does engage in defense applications for advanced materials. Furthermore, their integration of graphene heating elements into sportswear through collaborations with brands like Colmar exemplifies the diverse commercialization pathways for graphene in textiles.

Market Dynamics – Graphene Reinforced Polymer Composites Industry: Trends & Opportunities

Trend: Self-Sensing Graphene Polymer Composites for Structural Health Monitoring

The Graphene Reinforced Polymer Composites Industry is undergoing a paradigm shift as self-sensing composites gain commercial traction. Graphene’s unique properties are enabling real-time structural health monitoring, transforming safety and maintenance across critical industries.

-

Graphene’s piezoresistive properties integrated into polymer matrices enable intrinsic structural health monitoring, replacing bulky, costly sensor systems in applications like aerospace, wind energy, and infrastructure.

-

Real-time strain detection as low as 0.1–0.5% through changes in electrical resistance has been demonstrated in prototypes from Airbus and the University of Manchester, enabling distributed sensing across large structures without extra electronics.

-

Siemens Gamesa is exploring self-diagnosing graphene composites in wind turbine blades to detect delamination and failures earlier, supporting proactive maintenance and extending asset lifespans in renewable energy applications.

Opportunity: Closed-Loop Recyclable Graphene Thermosets

The push for sustainability is transforming the thermoset composites industry, where recyclability has long been a challenge. Advances in graphene-modified vitrimers and recycled composites are creating pathways toward closed-loop systems, offering both environmental and commercial benefits.

-

Graphene-modified vitrimers use dynamic, reversible crosslinking, enabling recycling of epoxy systems at just 150°C—significantly lower than traditional thermoset processes—and achieving near-full recovery of material properties over multiple cycles, as demonstrated by the Fraunhofer Institute.

-

BMW’s research leverages graphene’s microwave absorption to facilitate in-situ repairs of carbon fiber reinforced polymer (CFRP) parts, showing strong retention of mechanical properties and offering cost-effective maintenance solutions.

-

ELG Carbon Fibre (UK) is integrating pyrolyzed carbon fiber waste with graphene to produce super-reinforced recycled composites, achieving properties that can rival or surpass virgin materials, opening new opportunities for automotive, aerospace, and construction sectors.

Graphene Reinforced Polymer Composites Market Share & Segmentation Analysis

Paints & Coatings: Dominance in Anti-Corrosion & Conductive Applications

In 2025, paints & coatings emerge as the leading application for graphene reinforced polymer composites, holding an estimated 28.9% share. Their dominance is anchored in the surge of anti-corrosion and conductive coatings across automotive, marine, and infrastructure projects. At the same time, batteries represent the fastest-growing segment, as graphene’s unique properties significantly improve energy density, thermal management, and rapid charging in lithium-ion and next-generation batteries. Solar panels are also gaining momentum, with manufacturers leveraging graphene’s superior conductivity and durability to enhance efficiency and product life.

.png)

Automotive: Primary Driver for Lightweighting & EV Components

The automotive industry stands out as the primary end-user, accounting for 33.8% of market share in 2025. Lightweight, high-strength graphene composites are rapidly displacing conventional materials in electric vehicle bodies, battery casings, and interior components. Aerospace and defense sectors closely follow, adopting graphene for advanced, lightweight structural materials that meet stringent safety and performance standards. Meanwhile, tires are poised for significant growth, as graphene’s integration delivers longer wear, enhanced fuel efficiency, and improved safety—aligning with evolving demands in transportation and sustainability.

China Leads Global GRPC Industry with Aerospace, Electronics, and EV Expansion

China has rapidly emerged as the global powerhouse in Graphene Reinforced Polymer Composites (GRPCs), backed by robust government investment and cutting-edge R&D at hubs like the Ningbo Graphene Innovation Center. The Chinese Academy of Sciences (CAS) recently developed ultra-strong graphene-polyimide composites for aerospace applications, now being tested in next-generation aircraft like the COMAC C919. GRPCs are seeing mass adoption in automotive EV battery casings and flexible electronics, where performance and weight savings are critical. In 2024, The Sixth Element launched graphene-reinforced nylon 6 composites, offering improved strength, durability, and thermal management. Jiangsu Cnano Technology’s expanded conductive GRPC output is fueling the 5G device boom. Most recently, Huawei patented graphene-polymer heat dissipation films for foldable phones, solidifying China’s lead in consumer tech and high-performance composites for both mobility and electronics.

United States Scales GRPC Innovation for Aerospace, Defense, and Additive Manufacturing

The United States is at the forefront of GRPC innovation, channeling NASA and Department of Defense (DOD) funding into next-generation materials for spacecraft shielding, hypersonic vehicles, and military armor. MIT’s development of self-healing graphene-epoxy composites—with fracture resistance improvements exceeding 200%—signals a step change in resilience for advanced structures. Applications span aerospace (with Boeing, SpaceX), automotive (notably Tesla battery packs), and high-end sports equipment. XG Sciences (now part of Cabot Corp) commercialized graphene-PEEK composites for 3D printing in 2024, providing manufacturers with robust, lightweight, and heat-resistant alternatives. Graphene Composites Ltd’s new facility focuses on ballistic armor materials for defense and security. The latest: Lockheed Martin is testing GRPCs for satellite radiation shielding, pointing to GRPC’s growing criticality in demanding, high-stakes environments.

South Korea Pushes GRPCs for Consumer Electronics and Advanced Mobility

South Korea’s advanced materials sector is heavily invested in GRPCs, with KRICT pioneering graphene-polycarbonate composites for ultra-durable, unbreakable phone screens and Samsung SDI committing $100M+ to develop GRPCs for foldable OLED displays. Applications are thriving in consumer electronics (Samsung Galaxy Z Fold), automotive (Hyundai EV panels), and beyond. LG Chem’s 2024 launch of flame-retardant graphene-ABS composites positions the nation at the leading edge of fire-safe, lightweight plastics. KAIST’s latest research has resulted in GRPCs with five times the thermal conductivity of aluminum—transforming possibilities for electronics cooling and high-efficiency components. South Korea’s aggressive R&D and rapid commercialization cycles are placing it at the core of global GRPC deployment in both tech and transport.

Germany Drives Automotive and Industrial Leadership in Graphene Polymer Composites

Germany’s strength in high-performance automotive and industrial engineering is mirrored in its robust GRPC sector. The Fraunhofer Institute has optimized graphene-PA6 composites for BMW’s lightweight parts, advancing fuel efficiency and emissions reduction goals. BASF has patented graphene-reinforced polyurethanes for industrial coatings and specialty applications. Key uses include Porsche’s structural components, wind turbine blades, and the emerging industrial 3D printing market. SGL Carbon’s 2024 launch of graphene-CFRP hybrid composites for aviation addresses aerospace’s need for strength and weight savings. Mercedes-Benz’s recent testing of GRPCs in EQXX concept car battery housings points to Germany’s determination to lead in both EV innovation and advanced materials manufacturing.

United Kingdom Delivers Sustainable and High-Performance GRPCs for Industry and Sport

The United Kingdom is pioneering the use of sustainable GRPCs, with the University of Manchester developing graphene-PLA composites for eco-friendly packaging and Haydale Graphene supplying advanced materials to the McLaren F1 team. The UK is a center for GRPC innovation in aerospace (Rolls-Royce turbine blades), sports (graphene tennis rackets), and marine engineering. Versarien’s 2024 launch of graphene-enhanced bicycle cranksets demonstrates the sector’s capacity for consumer product innovation. In defense, BAE Systems is developing GRPCs for next-generation fighter jet components, while Rolls-Royce advances their use in aerospace propulsion. The UK’s dynamic mix of research, industry, and sustainability is cementing its role as a leader in both high-performance and green GRPC solutions.

Japan Advances GRPCs for High-Temperature, Lightweight, and Flexible Applications

Japan’s GRPC industry combines deep materials expertise with a focus on automotive, electronics, and industrial reliability. AIST’s creation of graphene-PPS composites for high-temperature fuel cells demonstrates the drive for both performance and durability. Toray Industries is investing over ¥50 billion in graphene-carbon fiber hybridization, while Mitsubishi Chemical’s 2024 release of graphene-PBT composites for EV charging ports aligns with Japan’s e-mobility ambitions. Applications extend to Toyota’s hydrogen tanks and Sony’s flexible circuits, pushing boundaries in both strength and flexibility. Panasonic’s 2024 testing of GRPCs for drone frames targets a 40% weight reduction—crucial for robotics and aerial mobility. Japan’s commitment to scaling GRPCs for high-value, high-tech applications keeps it at the top of the innovation curve.

Canada Scales GRPCs for Harsh Environments and Advanced Manufacturing

Canada has established itself as a major producer of GRPCs, with NanoXplore delivering 20,000 tons per year of graphene-PP composites. The National Research Council (NRC) developed GRPCs for Arctic pipeline insulation, highlighting graphene’s unique advantages in extreme environments. Applications include automotive (Magna International), aerospace (Bombardier), and oil & gas. In 2024, Grafoid commercialized graphene-HDPE composites for chemical tanks—demonstrating market appetite for corrosion-resistant, robust materials. GM Canada’s current tests of GRPCs in Silverado EV battery enclosures reflect a commitment to future-ready, lightweight, and durable vehicles. With sustained research, high-volume production, and cross-sector adoption, Canada is shaping the North American GRPC landscape.

Australia Expands GRPC Adoption in Mining, Clean Energy, and Defense

Australia’s graphene sector is advancing rapidly, with CSIRO pioneering graphene-fluoropolymer composites for space and harsh industrial uses, and Graphene Manufacturing Group (GMG) scaling up conductive GRPCs for mining equipment. Key applications now include mining wear-resistant liners, solar panel frames, and sports gear. GMG’s 2024 launch of graphene-enhanced surfboard fins reflects Australian innovation in high-durability consumer products. The University of Sydney’s 2024 patent for GRPCs in blast-resistant military shelters points to a growing market for advanced composites in defense and critical infrastructure. By blending resource-driven demand with strong R&D, Australia is establishing a distinct footprint in the global GRPC industry.

Graphene Reinforced Polymer Composites Market Report Scope

Graphene Reinforced Polymer Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$62.4 Million

|

|

Market Size (2034)

|

$544 Million

|

|

Market Growth Rate

|

27.2%

|

|

Segments

|

By Type (Black Color Eyelashes, Colored Eyelashes), By Application (Beauty Salon, Personal Use), By Accessories (Under-eye Stickers, Tweezers, Adhesive/Glue, Others), By Length (Below 5 mm, 5 to 10 mm, Above 10 mm), By Distribution Channel (Online, Offline), By Material (Nature Material, Artificial Material)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Asahi Kasei Corp, Directa Plus Plc Company, Dyson, Graphenano Group, Haydale Graphene Industries plc, Integran Technologies Inc, Mito Materials Solutions, NanoXplore Inc, PMG 3D Technologies Company Ltd, Procter & Gamble, TLC Products Inc, and Others

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene Reinforced Polymer Composites Market Segmentation

By Application

- Paints & Coatings

- Electronic Components

- Batteries

- Solar Panels

- Others

By End-User

- Automotive

- Medical

- Aerospace

- Defense

- Concrete Industry

- Tires

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene Reinforced Polymer Composites Market: Profiles & Strategies

- Asahi Kasei Corp

- Directa Plus Plc Company

- Dyson

- Graphenano Group

- Haydale Graphene Industries plc

- Integran Technologies Inc

- Mito Materials Solutions

- NanoXplore Inc

- PMG 3D Technologies Company Ltd

- Procter & Gamble

- TLC Products Inc

* List Not Exhaustive

Methodology

USD Analytics utilizes a rigorous, multi-stage research methodology to deliver highly accurate and actionable insights for the Graphene Reinforced Polymer Composites Market. The process begins with comprehensive secondary research, gathering data from industry journals, patents, regulatory filings, company financials, academic publications, and trade associations. This is complemented by in-depth primary research, including interviews with key opinion leaders, technology developers, industry executives, and end-users across the value chain—spanning automotive, aerospace, electronics, energy, and material science sectors. Data triangulation is performed by cross-verifying inputs from various sources, while market sizing and forecasting employ both top-down and bottom-up models. Advanced analytics are applied to assess market drivers, technological innovation, supply-demand dynamics, and competitive landscapes, ensuring findings are robust, up-to-date, and tailored to commercial decision-making. Ongoing monitoring of patent activity, regulatory developments, and product launches further strengthens our forward-looking market outlook.

Research Coverage and Deliverables

The Graphene Reinforced Polymer Composites Market Report provides a holistic analysis of the industry’s landscape and future prospects from 2025 to 2034. Coverage includes:

- Market Segmentation: In-depth analysis by Application (Paints & Coatings, Electronic Components, Batteries, Solar Panels, Others) and End-User (Automotive, Medical, Aerospace, Defense, Concrete Industry, Tires, Others)

- Geographical Assessment: Market size and forecasts for 21 countries across North America, Europe, Asia-Pacific, South America, and Middle East & Africa

- Competitive Intelligence: Detailed profiles of leading companies, emerging players, and strategic developments, including partnerships, R&D investments, mergers, and product launches

- Technological Insights: Trends in advanced polymer composites, self-sensing materials, flame retardancy, recyclability, 3D-printing, and integration of graphene with different polymer matrices

- Market Dynamics: Evaluation of growth drivers, challenges, regulatory environment, and future opportunities for manufacturers, suppliers, and end-users

Deliverables include:

- Comprehensive report in PDF and Excel formats

- Interactive data dashboards (upon request)

- Custom segment analysis and scenario forecasting

- Executive summary and visual infographics

- Analyst support for follow-up queries or briefings