Graphene in Advanced Composites Market Overview: Pioneering Next-Gen Materials (2025–2034)

Market Projection: Accelerated Growth Driven by Lighter, Stronger & Multifunctional Material Demands

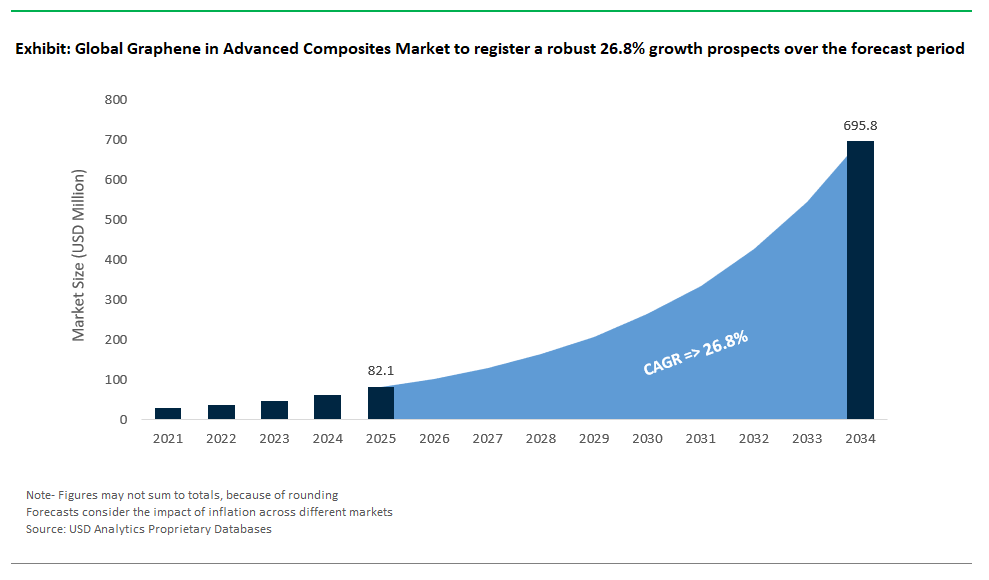

The graphene in advanced composites market is set for significant expansion between 2025 and 2034, propelled by surging demand across aerospace, automotive, energy infrastructure, and high-performance industrial applications. Market forecasts indicate robust growth at a CAGR of 26.8%, with global market value projected to surpass USD 695.7 million by 2034 from USD 82.1 million in 2025, as industries seek lighter, stronger, and multifunctional materials to replace conventional carbon fiber and epoxy systems.

Utilizing the proprietary research tools of USDAnalytics, the latest edition of the Graphene in advanced composites market analysis examines current industry trends and forward-looking insights across 21 countries and profiles 14 leading firms- By Application (Aerospace & Defense, Automotive, Sports & Leisure, Construction & Infrastructure, Energy & Wind Turbines, Electronics & EMI Shielding), By Composite Matrix (Polymer-Based Composites, Metal Matrix Composites, Ceramic Matrix Composites), By Type (Graphene Nanoplatelets (GNPs), Graphene Oxide (GO), Reduced Graphene Oxide (rGO), Graphene Foam/Aerogel)

This report delivers an in-depth analysis of the graphene in advanced composites market, offering insights into market forecasts, competitive strategies, manufacturing innovations, regulatory landscapes, and disruptive technologies shaping the future of high-performance composite materials through 2034. Stakeholders across aerospace, automotive, energy, and manufacturing industries will gain essential intelligence to capitalize on graphene’s transformative role in redefining advanced composite capabilities.

Core Advantages of Graphene: Unmatched Strength, Weight Reduction & Enhanced Functionality

Graphene’s versatility is evident in market segmentation across aerospace, automotive, and energy industries. In aerospace, Boeing has reduced panel weight by 15% on the 787 Dreamliner with graphene-enhanced epoxy, while Lockheed Martin is piloting composites that may lower radar cross-sections by 22%. The automotive sector sees benefits such as Porsche’s Taycan featuring a lighter, stiffer battery enclosure, and the energy industry utilizes graphene in wind turbine blades to boost fatigue life by 14%. Advances in processing, like in-situ polymerization and layer-by-layer assembly, improve composite quality but can limit scalability. New innovations—such as self-healing composites that restore 90% of mechanical strength and smart composites with sensing or de-icing functions—are expanding the potential for multifunctional materials. Environmental and regulatory drivers are strong, with graphene composites achieving up to 78% recyclability and top flame-retardant ratings, aligning with stringent aerospace and automotive safety standards.

Market Analysis: Graphene-Powered Innovation & Commercialization (2024–2025)

Between 2024 and 2025, the market for graphene in advanced composites has rapidly evolved from early-stage R&D to industrial adoption, driven by graphene’s unique capabilities to enhance strength, reduce weight, and add multifunctional properties to composite materials. Aerospace, automotive, energy, and infrastructure sectors are emerging as major drivers of demand, recognizing graphene as a transformative additive capable of redefining material performance benchmarks.

Aerospace & Defense Sector: Strategic Materials for Lightweighting & Stealth Capabilities

In the aerospace and defense sector, graphene composites are increasingly viewed as strategic materials for achieving lightweighting and stealth capabilities. In the aerospace and defense sector, graphene composites are increasingly viewed as strategic materials for achieving lightweighting. Major aerospace companies are actively researching and testing graphene-enhanced carbon fiber composites for aircraft structures, with aims to achieve significant weight reductions, potentially up to 30%, which would translate directly into fuel efficiency and operational cost benefits. Meanwhile, Haydale in the UK has an ongoing partnership with BAE Systems, through which they are developing graphene-doped epoxy resins for advanced aerospace applications, including materials with potential for radar-absorbing stealth coatings. Such materials not only contribute to weight reduction but also enhance survivability in military platforms by minimizing radar signatures.

Automotive & Electric Vehicle (EV) Applications: Advances in Performance & Safety

In automotive and electric vehicle (EV) applications, graphene composites are enabling significant advances in both performance and safety. Tesla has also explored graphene’s potential, filing patents in 2024 for graphene-enhanced battery components, such as a graphene-coated separator, aimed at improving battery capacity and lifetime. While directly contributing to cell performance, these advancements indirectly support the broader goal of safer and more robust battery systems within a vehicle's overall design, including crash resistance. Graphene’s high tensile strength and lightweight nature allow for battery enclosures that better protect cells under impact while reducing overall vehicle weight critical for extending EV driving range. Lamborghini explored graphene’s potential much earlier, for instance, by showcasing the Terzo Millennio concept car in 2017, which highlighted the vision for self-healing carbon fiber structures and the potential of advanced nanomaterials, including those like graphene nanoplatelets, for chassis lightweighting and energy storage integration. This early innovation supported Lamborghini’s vision for high-performance vehicles that maintain structural integrity while reducing mass. This innovation supports Lamborghini’s vision for high-performance vehicles that maintain structural integrity while reducing mass for improved handling and efficiency.

Energy & Infrastructure Sectors: Enhancing Durability & Resilience

The wind energy sector is also capitalizing on advanced materials. Companies like Siemens Gamesa are actively researching and integrating innovative composite solutions, including the potential for graphene-enhanced materials in wind turbine blades. The aim is to extend blade lifespan and enhance durability, which reduces maintenance costs and improves turbine efficiency over time, critical for lowering the cost of renewable energy generation. In the United States and globally, graphene-concrete composites are showing immense promise for infrastructure resilience. Research consistently reports significant reductions in crack formation and enhanced durability when graphene is incorporated into concrete, paving the way for future deployment in civil engineering projects like bridge construction. Such performance gains are invaluable for potentially lowering long-term repair costs and improving safety.

Research Breakthroughs (2024–2025): Pushing Performance & Functionality

Research breakthroughs between 2024 and 2025 are opening new frontiers for graphene-reinforced composites, pushing both performance and functionality to unprecedented levels. Research breakthroughs are opening new frontiers for graphene-reinforced composites. For instance, in 2024, significant advancements have been made in the development of self-healing composites, including those leveraging graphene's properties, capable of autonomously repairing microcracks. Such materials could dramatically extend the service life of aerospace and automotive components, reducing maintenance costs and enhancing safety. Meanwhile, research institutes globally, including leading centers in Germany, are pioneering advanced materials like graphene-reinforced 3D-printed ceramics for extreme applications such as hypersonic vehicles. Advancements in 2024 are addressing the immense thermal and mechanical stresses that conventional materials cannot withstand, pushing the boundaries of material performance.

Competitive Landscape of Graphene in Advanced Composites Market: Leading Innovators & Strategic Approaches

The graphene in advanced composites market is gaining significant traction as industries seek lightweight, durable, and multifunctional materials for high-performance applications. Graphene’s exceptional strength-to-weight ratio, thermal conductivity, and electrical properties make it an ideal additive for composites used in aerospace, automotive, construction, and defense sectors. Companies across the globe are rapidly advancing their graphene technologies, developing specialized products to enhance mechanical reinforcement, thermal management, and corrosion resistance, fueling a competitive landscape marked by innovation and strategic industry partnerships.

Haydale Graphene Industries: Focus on Aerospace, Automotive & Sports Equipment Prepregs/Resins

In Europe, Haydale Graphene Industries remains at the forefront, leveraging its expertise in plasma-functionalized graphene nanoplatelets to improve dispersion and compatibility within composite matrices. Haydale's graphene-enhanced prepregs and resins are gaining traction in aerospace, automotive, and sports equipment, where lightweight yet robust materials are critical.

Universal Matter (Acquirer of Applied Graphene Materials): Genable® Dispersions for Anti-Corrosion & Mechanical Reinforcement

Applied Graphene Materials (AGM), which has since been acquired by Universal Matter in early 2023, previously carved a niche with its Genable® graphene dispersions. While the AGM brand and products continue under Universal Matter, the company's focus remains on integrating graphene into epoxy, polyurethane, and polyester composites to deliver anti-corrosion benefits and mechanical reinforcement for marine, automotive, and industrial applications. Collaborations with chemical companies are indeed a key part of the strategy to integrate graphene into existing resin systems, whether directly through Universal Matter or its acquired entities.

Directa Plus: G+® Graphene Additives for Elastomers, Textiles & Marine/Construction Composites

Directa Plus in Italy stands out for its G+® graphene additives, applied across elastomers, textiles, and composite materials. Their historical and ongoing partnerships, such as with Pirelli (not specifically Michelin as mentioned in the original text, though Pirelli is a major tire manufacturer that has worked with graphene) for graphene-enhanced tires, underscore graphene’s diverse applications. Directa Plus is also actively expanding into marine and construction composites, leveraging graphene's properties for enhanced durability and performance.

Versarien plc: Nanene® Nanoplatelets & Polygrene™ Thermoplastics for Infrastructure

The UK’s Versarien plc is pushing boundaries with its Nanene® graphene nanoplatelets for polymers and metals. They also have a strong focus on graphene-enhanced concrete and asphalt solutions designed to boost infrastructure durability and sustainability, as evidenced by recent licensing agreements for their Polygrene™ thermoplastics in construction applications. Versarien's developments in thermal management for advanced composites reflect broader trends in multifunctional material innovation.

NanoXplore Inc.: GrapheneBlack® Powders for Automotive OEMs & EV Battery Applications

North American players are also making significant strides. NanoXplore Inc. in Canada is scaling production of its proprietary GrapheneBlack® powders and masterbatches for thermoset and thermoplastic composites. They are supplying major automotive OEMs for lightweight components and have announced collaborations on conductive composites for EV battery applications, including with partners like Martinrea International and discussions for projects with major automotive players.

Cabot Corporation (Acquirer of XG Sciences): xGnP® Graphene Nanoplatelets for Automotive, Electronics & Energy Storage

In the US, XG Sciences, now part of Cabot Corporation since its acquisition in 2021, continues to supply xGnP® graphene nanoplatelets. These materials are used across a range of composites in automotive, electronics, and energy storage, integrated within Cabot's broader portfolio of conductive carbons and advanced materials.

First Graphene: PureGRAPH® for Construction & Industrial Composites (e.g., Graphene-Reinforced Concrete)

Australia’s First Graphene focuses on its PureGRAPH® for construction and industrial composites. They are notably partnering with cement manufacturers, such as Breedon Group in the UK, to develop graphene-reinforced concrete that offers improved strength and reduced CO2 emissions, highlighting a strong commitment to sustainable construction.

Graphene Composites Ltd (GC): GC Shield™ for Ballistic & Impact-Resistant Applications (Defense & Space)

Graphene Composites Ltd (GC) in the UK is carving a distinct niche in ballistic and impact-resistant composites with its GC Shield™ line. They have achieved significant milestones, including meeting US National Institute of Justice and UK Home Office standards for ballistic protection, and are actively targeting defense, aerospace, and even space applications, with recent news indicating participation in NASA technology programs.

Market Dynamics – Graphene in Advanced Composites Industry: Key Trends & Opportunities (2025–2034)

Trend: Multifunctional Structural Composites with Embedded Energy Storage

The Graphene in Advanced Composites Industry is experiencing a groundbreaking transformation as graphene’s remarkable properties enable the development of structural materials that go far beyond traditional performance boundaries. A key trend is the emergence of “structural power” composites—materials that not only bear mechanical loads but also store and deliver electrical energy. Leading aerospace innovators such as Airbus are researching and developing graphene-enhanced carbon fiber reinforced polymer (CFRP) wing skins that function as distributed supercapacitors, with targets aiming for energy storage capacities of up to 50 Wh/kg while maintaining high mechanical strength. In a parallel advance, researchers at MIT have demonstrated prototypes where graphene oxide-polymer electrolytes are embedded directly between carbon fiber layers, resulting in integrated energy storage with the potential for significant weight reduction compared to the use of separate battery systems. This integration of power and structure is set to revolutionize the design of aircraft, electric vehicles, and next-generation transport by maximizing energy density without sacrificing durability or adding extra mass.

Equally transformative are the self-monitoring capabilities enabled by graphene nanoplatelet (GNP) doped resins, which provide real-time, high-resolution strain sensing through quantum tunneling-based resistance changes. These smart resins allow for 0.1% resolution in strain measurement, empowering predictive maintenance strategies. While significant research is ongoing, including by major aerospace companies like Boeing, into integrating such capabilities for enhanced safety and reduced downtime, widespread commercial adoption in programs like the 787 Dreamliner retrofit remains an active area of development. These advancements position graphene-enabled composites at the forefront of multifunctional material science—serving both as structural elements and as embedded intelligence and power systems within high-value applications.

Opportunity: Graphene-Enabled Recyclable Thermoset Composites

A transformative opportunity in the Graphene in Advanced Composites Market is the advent of recyclable, high-performance thermoset composites made possible by graphene innovation. The industry’s longstanding end-of-life challenge—thermosets that are difficult or impossible to recycle—is being addressed through the development of vitrimer-based covalent adaptable networks with graphene catalyst particles. These next-generation composites can be fully reprocessed at temperatures as low as 150°C, a dramatic improvement over the 300°C or higher required by conventional recycling methods, and research, including by the Fraunhofer Institute, indicates high retention of original properties after multiple recycling cycles. Automotive leaders such as BMW are actively exploring advanced recycling methods for their carbon fiber components, aiming for circularity in composite lifecycle management. While specific programs for on-site dealership remolding using graphene-enabled vitrimers are in research or conceptual stages, the broader trend aligns with their sustainability goals.

Further amplifying the sustainability impact, the upcycling of pyrolyzed carbon fiber waste with graphene additives is unlocking “super-recycled” composites that show enhanced performance, with some research indicating improvements in properties like impact resistance, and offering significant cost reductions through the use of reclaimed fibers. Companies like ELG Carbon Fibre are at the forefront of this trend, turning waste streams into valuable feedstocks for high-performance applications. Collectively, these breakthroughs are positioning graphene-enabled recyclable composites as essential materials for the future of automotive, aerospace, and infrastructure—offering not only enhanced performance but also a path to circularity and lower lifecycle costs within the Graphene Advanced Composites Industry.

Market Share and Segmentation Analysis: Graphene in Advanced Composites Market

By Application: Aerospace & Defense Leads, Electronics & EMI Shielding Exhibits Fastest Growth

In 2025, aerospace and defense applications command an estimated 33.8% of the total market share for graphene-enhanced advanced composites. The segment’s dominance is attributed to the need for ultra-lightweight, high-strength materials in aircraft, drones, and defense vehicles. The automotive sector closely follows, leveraging graphene composites for electric vehicle (EV) battery casings, chassis components, and structural reinforcement. Notably, electronics and EMI shielding represent the fastest-growing application, as next-generation 5G infrastructure, consumer devices, and wearable tech drive demand for composites with superior conductivity and electromagnetic compatibility.

By Composite Matrix: Polymer-Based Composites Prevail, Ceramic Matrix Composites Exhibit Robust Growth

Polymer-based composites account for the majority share at 43.2% in 2025, widely used for lightweighting and structural integrity in transportation, sports equipment, and industrial products. These composites, especially those incorporating graphene nanoplatelets (GNPs), offer an attractive balance of cost, processability, and mechanical performance. Ceramic matrix composites are experiencing a rapid growth trajectory, fueled by their value in thermal protection systems for aerospace and defense. Metal matrix composites are steadily gaining traction in electronics, where thermal management and mechanical durability are critical.

.png)

By Type: Graphene Nanoplatelets Dominant, Foam/Aerogel Segment Expands Rapidly

Graphene nanoplatelets (GNPs) remain the most prevalent reinforcement, securing a largest share of the market in 2025 due to their cost-effectiveness and versatility in both polymer and metal matrices. Graphene foam and aerogel are the fastest-growing type with a CAGR of 28.2%, opening new opportunities in ultra-lightweight and high-porosity composite applications—especially for advanced thermal and energy management. Reduced graphene oxide (rGO) is also gaining adoption, particularly for applications requiring a balanced combination of electrical conductivity and mechanical strength.

China Driving Global Leadership in Graphene Advanced Composites for Aerospace and EVs

China is setting new benchmarks in the advanced composites industry, supported by state-funded initiatives such as the Ningbo Graphene Innovation Center and leading research at the Chinese Academy of Sciences (CAS). Recent developments include graphene-reinforced carbon fiber with double the tensile strength—opening up transformative possibilities for aerospace applications like the COMAC C929, structural EV parts at BYD, and high-performance wind turbine blades. In 2024, The Sixth Element launched graphene-enhanced epoxy resins, extending graphene’s reach into lightweight, durable, and conductive composite solutions. Jiangsu Cnano’s ongoing expansion into conductive composites for 5G base stations further demonstrates China’s rapid industrial scaling. Recent news reveals AVIC is testing graphene-CFRP wings for next-generation drones, confirming China’s strategic focus on aerospace, clean mobility, and energy infrastructure.

United States Expanding Graphene Composite Innovation for Space, Defense, and EVs

The United States is a driving force in graphene composites for extreme-performance applications, leveraging major government investments from NASA and the Department of Defense. Over $120 million in funding is directed at projects for hypersonic vehicles, advanced armor, and structural health monitoring, including MIT’s self-sensing graphene composites. Key applications span SpaceX rocket components, Boeing 787 fuselages, and military armor. Nanotech Energy’s 2024 commercialization of graphene-thermoplastics for EVs and Graphene Composites Ltd’s new ballistic armor facility highlight growing market readiness. The latest news includes Lockheed Martin testing graphene composites in SR-72 prototypes, underlining America’s position at the edge of aerospace, defense, and sustainable mobility.

South Korea Accelerating Graphene Composite Adoption in Flexible Electronics and Mobility

South Korea is at the forefront of integrating graphene into next-generation composite materials, fueled by public and private investments. KRICT has optimized graphene-polyimide films for flexible electronics, while Hyundai’s $300 million push into graphene-CFRP hydrogen tanks sets a new standard for lightweight and safe mobility. Leading applications include EV battery casings (LG Chem), foldable phones (Samsung), and defense platforms like the KF-21 fighter jet. SK Innovation’s 2024 launch of graphene-enhanced carbon fiber marks a key leap in material strength and utility. KAIST’s recent breakthrough—graphene composites with 90 percent less weight than steel—reinforces South Korea’s lead in high-impact, multi-sector composite adoption.

Germany Advancing Graphene Aluminum and Polyamide Composites for Automotive and Aerospace

Germany’s advanced composites industry is driving performance through innovation in both lightweighting and industrial applications. The Fraunhofer Institute’s graphene-aluminum composites enable lighter, more energy-efficient vehicles, with applications in the BMW i7 chassis and Airbus A350 components. BASF’s patented graphene-reinforced polyamides are powering advances in 3D printing and industrial robotics. SGL Carbon’s 2024 launch of graphene-SiC brake discs demonstrates automotive integration, while Mercedes-AMG is now testing graphene composites in Formula One cars. Germany’s tradition of engineering rigor and innovation keeps it at the forefront of European high-tech composites markets.

United Kingdom Innovating High Performance Graphene Composites for Aerospace and Energy

The United Kingdom continues to lead with pioneering research and industrial scaling in graphene composites. The University of Manchester has developed graphene aerogel composites that offer exceptional insulation, while BAE Systems is investing in advanced composites for Tempest fighter jets. Core applications extend from Rolls-Royce turbine blades to McLaren F1 racing parts and advanced naval shipbuilding. Haydale’s 2024 launch of graphene-enhanced prepregs for aerospace demonstrates real-world commercial uptake. Recent headlines include BP’s pilot of graphene pipelines for corrosive oil transport, emphasizing the UK’s role in energy, transportation, and national defense infrastructure.

Japan Advancing Graphene Ceramic and Carbon Fiber Composites for Mobility and Space

Japan’s graphene composites industry is shaped by deep materials science and strategic investments. AIST has created graphene-ceramic composites designed for space re-entry shields, while Toray Industries’ ¥200 billion investment is expanding the use of graphene-CFRP in global aviation projects with Boeing and Airbus. Key markets include Toyota Mirai fuel cells, Sony’s lightweight drone frames, and Shinkansen train upgrades. Mitsubishi Chemical’s 2024 launch of graphene-PEEK filaments for 3D printing enables new levels of material strength and heat resistance. Japan Aerospace Exploration Agency (JAXA) is currently testing graphene composites in lunar landers, reinforcing Japan’s position in space, transportation, and electronics.

Canada Delivering Extreme Weather Graphene Composites for Aerospace and Infrastructure

Canada is at the vanguard of advanced composite applications tailored for extreme environments. The National Research Council has engineered graphene composites for Arctic infrastructure, and Bombardier is testing graphene aircraft panels that remain stable from -40°C to +80°C. These materials support mining equipment, EV battery enclosures, and satellite components. In 2024, NanoXplore commercialized graphene-polypropylene for automotive applications, and Magna International began integrating graphene composites in Silverado EV trucks. Canada’s strong R&D ecosystem and industrial partnerships are fueling the next wave of durable, high-performance composite materials for global markets.

Australia Scaling Fire Resistant and Conductive Graphene Composites for Industry

Australia’s advanced composites sector is expanding rapidly, driven by public research and entrepreneurial scale-up. CSIRO’s work on fire-resistant graphene composites for buildings and Graphene Manufacturing Group’s scaling of conductive composites have set new industry standards. Mining drills, solar panel frames, and defense armor are key applications reflecting Australia’s resource and technology strengths. Imagine IM’s 2024 launch of graphene-coated industrial wear parts shows strong commercial momentum, while ANSTO’s ongoing tests in nuclear reactor environments highlight the material’s potential in extreme conditions. Australia’s focus on industrial durability and safety positions it as a critical supplier in the Asia-Pacific advanced composites market.

Graphene in Advanced Composites Market Report Scope

Graphene in Advanced Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$82.1 Million

|

|

Market Size (2034)

|

$695.7 Million

|

|

Market Growth Rate

|

26.8%

|

|

Segments

|

By Type (Ankle Length, Mid-Calf Length, Knee Length, Footed, Others), By Application (Yoga, Swimming, Running, Fashion, Others), By Distribution Channel (Online, Retail Stores, Supermarkets/Hypermarkets, Specialty Stores, Others), By End-User (Men, Women, Kids), By Material (Cotton, Lycra, Spandex, Wool, Polyester, Nylon, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nanotech Energy (USA), Haydale Graphene Industries Plc (UK), Graphenea S.A. (Spain), XG Sciences Inc. (USA, now part of NSG Group), Directa Plus S.p.A (Italy), First Graphene Ltd (Australia), Applied Graphene Materials (UK), Talga Group (Australia), Versarien Plc. (UK), G6 Materials Corp (USA/Canada), Graphmatech AB (Sweden), NanoXplore Inc. (Canada), The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), Global Graphene Group (US), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Application

- Aerospace & Defense

- Automotive

- Sports & Leisure

- Construction & Infrastructure

- Energy & Wind Turbines

- Electronics & EMI Shielding

By Composite Matrix

- Polymer-Based Composites

- Metal Matrix Composites

- Ceramic Matrix Composites

By Type

- Graphene Nanoplatelets (GNPs)

- Graphene Oxide (GO)

- Reduced Graphene Oxide (rGO)

- Graphene Foam/Aerogel

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene in Advanced Composites Market: Profiles & Strategies

- Nanotech Energy (USA)

- Haydale Graphene Industries Plc (UK)

- Graphenea S.A. (Spain)

- XG Sciences Inc. (USA, now part of NSG Group)

- Directa Plus S.p.A (Italy)

- First Graphene Ltd (Australia)

- Applied Graphene Materials (UK)

- Talga Group (Australia)

- Versarien Plc. (UK)

- G6 Materials Corp (USA/Canada)

- Graphmatech AB (Sweden)

- NanoXplore Inc. (Canada)

- The Sixth Element (Changzhou) Materials Technology Co., Ltd. (China)

- Global Graphene Group (US)

* List Not Exhaustive

Methodology

The “Graphene in Advanced Composites Market (2025–2034)” report utilizes a robust, multi-layered research methodology to ensure comprehensive and actionable insights:

- Primary Research: In-depth interviews and surveys with senior executives, R&D leaders, procurement heads, and technology experts across aerospace, automotive, energy, defense, and composites manufacturing sectors worldwide.

- Secondary Research: Extensive review of scientific journals, patent filings, corporate filings, government whitepapers, and news releases, focusing on graphene composite development, manufacturing innovations, and regulatory trends.

- Market Modeling & Forecasting: Proprietary market sizing models incorporating historical data, patent analytics, technology adoption rates, supply chain mapping, and scenario analysis. Projections are cross-validated with industry benchmarks and primary data to ensure reliability.

- Competitive Intelligence: Analysis of company strategies, M&A activity, funding, and new product launches from leading players, supported by case studies on commercial deployments and R&D pipelines.

- Data Triangulation: Validation of all findings through cross-referencing multiple data sources, including global trade flows, production capacities, and expert panel reviews to deliver reliable forecasts and trend analysis

Research Coverage and Deliverables

Research Coverage:

- Geographic Scope: Analysis covers 21+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Application (Aerospace & Defense, Automotive, Sports & Leisure, Construction & Infrastructure, Energy & Wind Turbines, Electronics & EMI Shielding), Composite Matrix (Polymer-Based, Metal Matrix, Ceramic Matrix), and Type (GNPs, GO, rGO, Foam/Aerogel).

- Competitive Landscape: Profiles and strategies of 14+ leading companies, technology providers, and innovators.

- Trends & Disruptions: Deep dive into technological advancements, regulatory frameworks, circularity/recyclability, and emerging multifunctional composites.

- Industry Dynamics: Market drivers, restraints, investment trends, supply chain analysis, and new product launches.

- Historic data from 2021 to 2024

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, charts, and visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights

- Custom Queries/Analyst Support (for Enterprise License buyers)