Market Overview: High-Performance Materials and Patient-Centric Design Driving Growth

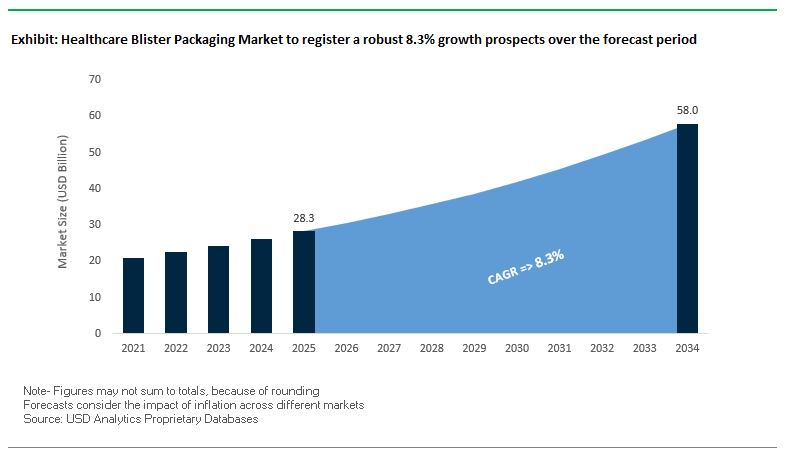

The global healthcare blister packaging market is valued at USD 28.3 billion in 2025 and is projected to reach USD 58 billion by 2034, expanding at a CAGR of 8.3%. This growth is primarily driven by the demand for efficient drug delivery systems, superior barrier properties, and sustainable packaging alternatives. For industry professionals and buyers, the critical questions center on how blister packaging can enhance patient adherence, how material innovations are reshaping the supply chain, and how companies are balancing sustainability with regulatory compliance.

Thermoforming remains the dominant manufacturing process, preferred for its faster production speeds and lower costs compared to cold forming. Meanwhile, aluminum foil continues to be the leading lidding material, providing unmatched protection against moisture, oxygen, and light for sensitive drugs and medical devices. The industry is undergoing a significant transition toward sustainability, with over 40% of pharmaceutical companies exploring mono-material plastics and paper-based alternatives to reduce their environmental footprint. Additionally, patient-centric features, such as calendar-based reminders, child-resistant yet senior-friendly designs, and tamper-evident seals, are becoming standard to enhance medication adherence and safety.

Key Insights for Industry Professionals:

- Thermoforming dominates due to speed and cost advantages in high-volume drug packaging.

- Aluminum foil is critical for extending product shelf life and ensuring drug efficacy.

- 40% of pharma companies shifting to sustainable blister formats like mono-material PE and paper-based solutions.

- Patient-centric packaging designs are enhancing usability and improving compliance rates.

Market Analysis: Strategic Investments and Sustainability-Centric Innovations

The healthcare blister packaging industry is in the midst of technological innovation, regional expansions, and material diversification, all of which are reshaping the competitive dynamics. In August 2025, Constantia Flexibles announced an investment exceeding €100 million to strengthen its pharmaceutical packaging and closures portfolio, underlining the shift toward sustainable and advanced solutions. During the same month, Ball Corporation optimized its operations by divesting part of its Saudi Arabia joint venture, signaling a strategic focus on its core aluminum packaging businesses.

Packaging ecosystem synergies are also notable. In July 2025, Ardagh Glass Packaging-Europe introduced a lightweight glass wine bottle, indirectly stimulating demand for compatible aluminum closures and reinforcing the integrated packaging value chain. Meanwhile, Amcor is deepening its global presence, having opened a new aluminum closures facility in Ohio, USA, in February 2025, dedicated to sustainable healthcare packaging formats.

On the product innovation front, Closure Systems International (CSI) showcased its Defender-Lok™ closure line in April 2025, delivering child-resistant and senior-friendly features for nutraceuticals. Similarly, Bayer’s October 2024 introduction of PET blister packaging for its Aleve brand eliminated PVC, representing a significant step toward eco-friendly pharmaceutical blister solutions.

Emerging Trends and Opportunities Defining the Healthcare Blister Packaging Market

Accelerated Adoption of High-Barrier and Advanced Polymer Materials

The healthcare blister packaging market is experiencing a decisive transition from conventional PVC-based packs to advanced multi-layer polymers and high-barrier films designed to safeguard increasingly complex drug formulations. Sensitive biologics, vaccines, and specialty pharmaceuticals are highly vulnerable to degradation from moisture, oxygen, and UV exposure, making material innovation a necessity rather than an option. Recent studies in the Journal of Pharmaceutical Sciences confirm that monoclonal antibodies and other biologics require barrier properties beyond the capacity of standard PVC. To address this, manufacturers are incorporating EVOH layers, cyclic olefin copolymers (COC), and thin aluminum foils into their structures. Bayer’s collaboration with Liveo Research on PET-based blister packaging for Aleve exemplifies this trend, reducing the product’s carbon footprint by 38% while maintaining high barrier performance. These material advancements not only extend shelf life and reduce waste but also align with global sustainability mandates by phasing out PVC. The shift underscores how innovation in material science is directly influencing drug stability, compliance with sustainability goals, and pharmaceutical supply chain resilience.

Integration of Smart Packaging and Serialization for Patient Adherence and Supply Chain Security

Blister packaging is evolving into an interactive, technology-enabled platform that enhances both patient safety and regulatory compliance. Smart blister packs equipped with sensors and conductive inks now allow healthcare providers to monitor medication adherence by recording the exact time and date a dose is taken. This technology, increasingly adopted in chronic disease trials, creates real-time data streams that improve patient outcomes. At the regulatory level, global serialization mandates such as the U.S. DSCSA and the EU’s Falsified Medicines Directive are driving adoption of unique identifiers on every blister pack, ensuring track-and-trace functionality across the pharmaceutical supply chain. To combat counterfeiting and improve patient trust, closures now feature QR codes, NFC tags, and tamper-evident seals that allow instant verification of product authenticity. Beyond security, these features enhance engagement: patients can scan blister packs for dosage reminders, educational content, or direct links to telemedicine platforms. This integration of smart features positions blister packaging as a critical enabler of digital healthcare transformation.

Development of Sustainable and Recyclable Mono-Material Structures

Sustainability mandates and ESG commitments are opening a significant growth pathway for recyclable blister packs. Traditionally composed of PVC and aluminum laminates, blister packs are notoriously difficult to recycle. Industry innovators are now investing in mono-material solutions that balance recyclability with the stringent barrier requirements of pharmaceutical packaging. SÜDPACK’s mono-PP blister concept is a key example, designed to integrate seamlessly into existing polypropylene recycling streams while preserving moisture and oxygen protection. Meanwhile, companies are exploring paper-based barrier packaging concepts, adapting technologies originally used in food applications for medical and pharmaceutical contexts. These innovations are being accelerated by regulatory deadlines such as the EU’s PPWR, which mandates all packaging placed on the market must be recyclable at scale by 2035. Brands and suppliers that commercialize scalable, recyclable mono-material blister formats will gain first-mover advantage in a market where sustainability is quickly becoming a procurement criterion.

Expansion into Home-Use Medical Device and Diagnostic Test Kitting

The rise of home-based healthcare and diagnostics is creating a fast-growing opportunity for blister packaging solutions that combine sterility, usability, and convenience. With patients increasingly self-administering injectables, using continuous monitoring devices, and conducting at-home diagnostic tests, packaging must simplify complex medical processes while ensuring safety. Blister packs are ideally suited to this shift, offering the ability to kit multiple components such as swabs, reagents, and instructions into a single sterile unit. Their tamper-evident design provides protection against contamination, while medical-grade paper backings offer both sterility and breathability. For diagnostics, blister packaging ensures proper organization and enhances patient compliance, reducing the likelihood of errors in home-use tests. As adoption of self-care models accelerates, blister packs are transitioning from basic pill containers to multifunctional systems that support broader healthcare delivery. This evolution positions blister packaging as a strategic enabler in expanding healthcare access and lowering treatment costs through home-based solutions.

Competitive Landscape: Leading Players in Healthcare Blister Packaging

The competitive environment of the healthcare blister packaging market is shaped by large multinational packaging companies and specialized healthcare divisions, each leveraging material expertise, global reach, and sustainability-driven innovation to expand their market share.

Amcor plc: Sustainability Through AmSky Blister Innovation

Amcor has emerged as a pioneer in healthcare blister packaging with its AmSky Blister System, a recyclable, mono-material PE solution designed to replace traditional vinyl and aluminum-based formats. The company’s acquisitions such as MDK (Shanghai) Packaging Technology in late 2024 and investments in new coating facilities in Malaysia (early 2025) highlight its expansion in healthcare packaging. With a strategic focus on making all products recyclable or reusable by 2025, Amcor is positioning itself at the forefront of sustainable healthcare packaging.

WestRock Company: Fiber-Based Alternatives to Plastic Blisters

WestRock is advancing the transition away from plastic with NatraPak and Blisterless Cartons, which replace traditional plastic blisters with paper-based solutions. The company’s **integrated model from paper production to packaging conversion **gives it strong control over quality and supply chains. Its strategy emphasizes patient-centric design, with packaging that improves adherence while reducing environmental impact, making WestRock a key innovator in sustainable healthcare blister packaging.

Sonoco Products Company: Leadership in Temperature-Controlled Healthcare Packaging

Through its Sonoco ThermoSafe division, Sonoco provides temperature-assurance packaging for pharmaceuticals, biologics, and vaccines, ensuring cold-chain integrity. While known for industrial packaging, Sonoco’s healthcare division specializes in solutions across refrigerated, frozen, and room-temperature applications. Following its late 2024 acquisition of Alucan, Sonoco continues to diversify into sustainable aluminum and paper packaging, reinforcing its multi-segment healthcare focus.

Berry Global Inc.: Advanced Plastic Healthcare Solutions

Berry Global delivers a wide portfolio of pharma bottles, ophthalmic containers, closures, and dispensing systems. Its recent launch of a recyclable clarified PP bottle line and an easy-squeeze ophthalmic bottle compatible with Aptar Pharma’s OSD dispenser demonstrates its commitment to combining sustainability with patient usability. The company’s strategy focuses on developing innovative, safe, and recyclable plastics while maintaining rigorous compliance with healthcare industry standards.

Constantia Flexibles GmbH: Pharmaceutical Foil and Barrier Film Specialist

Constantia Flexibles is a global leader in aluminum-based blister lidding foils and barrier films for pharmaceutical applications. The company’s REGULA CIRC foil underscores its focus on recyclability and barrier performance, while investments in digital printing and interactive packaging technologies add value for brand owners. With a strong focus on the circular economy, Constantia Flexibles provides high-barrier, sustainable blister solutions that meet stringent healthcare requirements.

Healthcare Blister Packaging Market Share Insights

Plastic-Based Films Lead Healthcare Blister Packaging Market Share by Product Type

Plastic-based films command 45% of the healthcare blister packaging market in 2025, establishing themselves as the most widely used format due to their versatility, formability, and cost-effectiveness. Polyvinyl chloride (PVC) and PCTFE (Aclar) dominate this space, enabling high-volume production of blister packs for solid oral dosages such as tablets and capsules. Their clarity enhances patient trust by allowing visual inspection of the medication, while their scalability ensures competitive manufacturing costs. Aluminum foils remain indispensable as the global barrier protection standard, especially for moisture- and oxygen-sensitive drugs, while multilayer laminates are gaining momentum in specialty applications like biologics, where PVC-free, high-barrier packaging is increasingly demanded. Paper-based blister packs, though currently a niche, are growing as part of the sustainability narrative, with applications in nutraceuticals and OTC segments where recyclability is prioritized. The dominance of plastic-based films highlights the industry’s reliance on cost-effective, high-output solutions, but the simultaneous growth of laminates and sustainable paper-based solutions reflects a market adapting to regulatory scrutiny and sustainability mandates.

Tablets Drive Healthcare Blister Packaging Market Share by Application

Tablets account for 50% of the global healthcare blister packaging market in 2025, making them the dominant application by a wide margin. This overwhelming share stems from their unparalleled volume in global pharmaceutical production, where blister packaging ensures patient safety, dosage compliance, and unit-level protection from contamination. The popularity of calendar packs, particularly in chronic therapies, further reinforces this demand by simplifying adherence and reducing medication errors. Capsules follow closely, representing 25% of demand, but they require higher barrier films due to their moisture sensitivity, often driving the adoption of multilayer laminates or Aclar-based materials. Parenteral packaging, including ampoules, vials, and pre-filled syringes, reflects the high-value, high-specification segment of the market, where blister packs provide secondary protection for fragile or sterile drug delivery systems. Smaller niches, including diagnostic strips, transdermal patches, and surgical tools, highlight the versatility of blister packaging beyond pharmaceuticals. The continued dominance of tablets underscores the centrality of oral solid dosage forms in global healthcare, while injectables and devices signal future growth in high-value therapeutic areas.

United States: Rising Health Awareness and Smart Packaging Driving Market Expansion

The U.S. healthcare blister packaging market is witnessing significant growth due to increasing health and wellness awareness, driving demand for over-the-counter (OTC) medications and nutraceuticals. Consumers and healthcare providers are emphasizing convenient, secure, and tamper-evident packaging solutions. Technological advancements, particularly the integration of smart packaging technologies such as RFID tags, sensors, and printed electronics, are enabling real-time monitoring of medication adherence and enhancing patient safety.

Sustainability is also a critical focus in the U.S., with companies like Tekni-Plex introducing recyclable polyester-based films and lidding systems to reduce environmental impact. Strategic expansions, such as Amcor’s new facility in Ohio for aluminum closures serving pharmaceutical and beverage sectors, are meeting growing market demand. Strict FDA regulations ensure material compatibility, child-resistant features, and tamper-evident seals, reinforcing the role of blister packaging in maintaining product integrity and patient safety.

Germany: Circular Economy Leadership and Digitally Advanced Blister Packaging

Germany’s healthcare blister packaging market is shaped by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which emphasizes eco-friendly, highly recyclable packaging. Manufacturers in Germany are integrating recycled content into products, aligning with national and EU targets for sustainability and the circular economy.

Technological innovation is a key driver, with companies like Uhlmann Packaging Group leading the development of flexible and digitally advanced blister packaging lines optimized for pharmaceutical production. Governmental mandates under the PPWR are accelerating waste reduction, recyclability improvements, and the incorporation of recycled materials, positioning Germany as a benchmark for sustainable healthcare packaging in Europe.

China: Government Initiatives and Technological Integration Fuel Healthcare Packaging Demand

China’s healthcare blister packaging market is being propelled by the Healthy China 2030 plan, which is driving substantial investments in healthcare infrastructure and pharmaceutical production. Rising disposable incomes, a large population base, and strong healthcare investments are fueling the demand for secure and tamper-proof packaging.

Technological advancements, including automation, AI, and “5G plus industrial internet” integration, are optimizing production efficiency and enabling flexible manufacturing capacities. The e-commerce boom further accelerates demand, providing widespread accessibility for pharmaceutical products and medical devices. This combination of governmental initiatives, technological innovation, and e-commerce growth is strengthening China’s position as a key growth market for healthcare blister packaging.

India: Pharmaceutical Growth and Sustainability Initiatives Expanding Market Reach

India’s healthcare blister packaging industry is experiencing rapid expansion due to government schemes like Ayushman Bharat, which are increasing access to health insurance and fueling pharmaceutical demand. The Indian pharmaceutical sector, ranked third globally by volume, is a major driver for oral dosage blister packaging.

Sustainability is gaining prominence, supported by GST reforms reducing taxes on paper pulp molded trays to 5%, making eco-friendly packaging more cost-effective. Technological investments in modern machinery, alternative raw materials like rice husk and bagasse, and strategic partnerships with multinational and local players are enhancing production efficiency and market reach. These factors collectively enable Indian manufacturers to expand their presence in regulated and emerging healthcare markets.

Brazil: Legislative Support and Technological Innovation Driving Sustainable Packaging

Brazil’s healthcare blister packaging market benefits from stringent environmental regulations, including the National Solid Waste Policy, promoting a shift toward reusable and durable packaging alternatives. Companies are increasingly adopting sustainable materials to align with circular economy objectives and reduce environmental pollution.

Technological advancements, such as AI and robotics for automated sorting, quality control, and defect detection, are improving production accuracy and operational efficiency. Strategic investments, including Canpack Group’s new facility in Minas Gerais, further enhance capacity for eco-friendly healthcare packaging. Collectively, these developments are positioning Brazil as a leading market for sustainable and technologically advanced blister packaging solutions in Latin America.

Japan: Advanced Recycling and Bio-Based Innovations Enhancing Healthcare Packaging

Japan’s healthcare blister packaging market leverages advanced recycling systems under the Containers and Packaging Recycling Law, enabling efficient collection and repurposing of waste materials. The industry is increasingly adopting bio-based materials, exemplified by innovations like Spiber’s Brewed Protein™, which provide sustainable alternatives to conventional plastics.

Innovation in functionality is a hallmark of the Japanese market, with a focus on high dimensional stability and deformation-resistant products for high-value applications. Continuous research and development, supported by institutions like Yamagata University, is driving breakthroughs such as printable, UV-densified barrier films for high-performance packaging. Japan’s approach integrates sustainability, innovation, and functionality, making it a global leader in advanced healthcare blister packaging solutions.

Healthcare Blister Packaging Market Report Scope

Healthcare Blister Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.3 Billion

|

|

Market Size (2034)

|

$58 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Product Type (Paper-based Blisters, Plastic-based Films, Aluminum Foils, Multilayer Laminates), By Technology (Thermoforming, Cold Forming), By Application (Tablets, Capsules, Ampoules, Syringes, Vials, Other Applications), By End-Use Industry (Pharmaceutical, Medical Devices, Cosmetics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Constantia Flexibles Group GmbH, WestRock Company, Tekni-Plex, Inc., Klöckner Pentaplast, Sonoco Products Company, Huhtamaki Oyj, Winpak Ltd., ACG Group, Uhlmann Pac-Systeme GmbH & Co. KG, Romaco Group, Bilcare Limited, Perlen Packaging AG, Blisterpak, Inc., Abhinav Enterprises

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Healthcare Blister Packaging Market Segmentation

By Product Type

- Paper-based Blisters

- Plastic-based Films

- Aluminum Foils

- Multilayer Laminates

By Technology

- Thermoforming

- Cold Forming

By Application

- Tablets

- Capsules

- Ampoules

- Syringes

- Vials

- Other Applications

By End-Use Industry

- Pharmaceutical

- Medical Devices

- Cosmetics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Healthcare Blister Packaging Market

- Amcor plc

- Constantia Flexibles Group GmbH

- WestRock Company

- Tekni-Plex, Inc.

- Klöckner Pentaplast

- Sonoco Products Company

- Huhtamaki Oyj

- Winpak Ltd.

- ACG Group

- Uhlmann Pac-Systeme GmbH & Co. KG

- Romaco Group

- Bilcare Limited

- Perlen Packaging AG

- Blisterpak, Inc.

- Abhinav Enterprises

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global healthcare blister packaging market, highlighting breakthroughs in high-barrier materials, patient-centric design, and sustainable mono-material structures that are reshaping pharmaceutical and medical device packaging. The analysis reviews evolving manufacturing technologies, including thermoforming and cold forming, innovations in aluminum foils, multilayer laminates, and paper-based alternatives, and emerging trends such as smart blister packs, serialization, and interactive packaging for improved patient adherence. It highlights opportunities in home-use diagnostics, e-commerce healthcare kits, and temperature-controlled packaging, emphasizing how sustainability initiatives and regulatory mandates are accelerating adoption across key regions. This report is an essential resource for packaging engineers, pharmaceutical manufacturers, healthcare providers, and sustainability professionals seeking actionable insights on material innovation, regulatory compliance, supply chain resilience, and competitive positioning. By incorporating historical data from 2021–2024 alongside forecasts through 2025–2034, and profiling 15+ leading companies, it delivers a comprehensive overview of market dynamics, regional growth patterns, and strategic initiatives driving high-value and sustainable blister packaging solutions.

Scope Highlights:

- Segmentation: By Product Type (Paper-based Blisters, Plastic-based Films, Aluminum Foils, Multilayer Laminates), By Technology (Thermoforming, Cold Forming), By Application (Tablets, Capsules, Ampoules, Syringes, Vials, Other Applications), By End-Use Industry (Pharmaceutical, Medical Devices, Cosmetics, Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ key players including Amcor plc, Constantia Flexibles Group, WestRock Company, Sonoco Products Company, Tekni-Plex, Klöckner Pentaplast, and Uhlmann Pac-Systeme

Methodology

USDAnalytics conducted this study using a comprehensive combination of primary and secondary research. Primary research included interviews with packaging engineers, pharmaceutical manufacturers, healthcare providers, and regulatory authorities to capture market trends, material adoption, and patient-centric requirements. Secondary research incorporated analysis of corporate reports, scientific publications, regulatory filings, and industry databases to validate production capacities, technology adoption, and sustainability initiatives. Market sizing and forecasts were derived from historical consumption, production trends, and regional healthcare expansion, while scenario modeling accounted for regulatory impacts, smart packaging integration, and sustainability mandates. Competitive benchmarking and innovation analysis provided insights into product development, mergers, capacity expansions, and global market positioning. This robust methodology ensures actionable intelligence for industry professionals seeking to optimize manufacturing, regulatory compliance, and sustainable healthcare packaging strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.