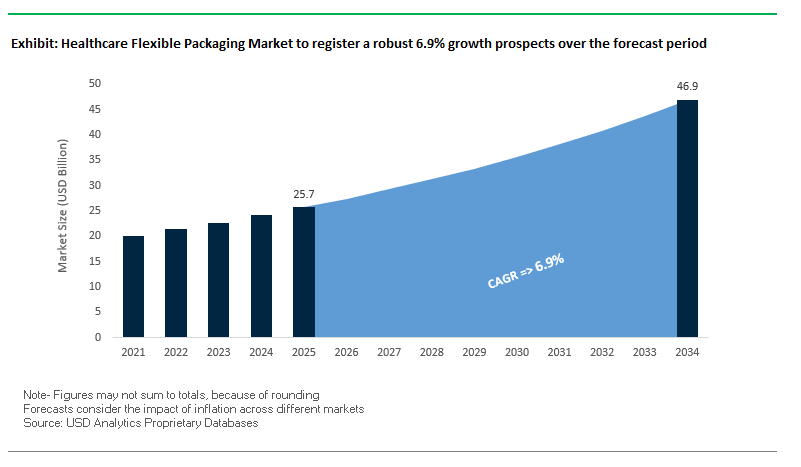

Market Overview: $25.7B Healthcare Flexible Packaging in 2025, Scaling to $46.9B by 2034

The Global Healthcare Flexible Packaging Market is valued at USD 25.7 billion in 2025 and is projected to reach USD 46.9 billion by 2034, reflecting a CAGR of 6.9%. Growth is propelled by lightweighting (up to ~60% lower product-to-package ratios vs. rigid), the dominance of pouches and high-barrier films as sterile barriers, and the pervasive role of plastics (over 73% market revenue in 2023) for moisture/oxygen protection and sterilization compatibility. In parallel, anti-counterfeiting technologies holographic films, security inks, tamper-evident seals have become table stakes to protect patient safety and brand equity. For procurement teams, the buying center is prioritizing materials that meet sterilization methods (EtO, gamma, e-beam), deliver microbial barrier integrity, and enable recycle-ready mono-material designs without compromising performance.

Key Insights for industry professionals

- Lightweighting advantage: Flexible formats can cut product-to-package weight by ~60%, lowering freight cost and CO₂.

- Pouches & high-barrier films lead: Effective microbial barriers for sterile medical products.

- Plastics at 73%+ share (2023): Versatility for barrier, durability, and sterilization drives adoption.

- Security-first packaging: Holograms, security inks, tamper-evidence deter counterfeits and support chain of custody.

Market Analysis: 2025 Momentum Capacity Adds, Recycle-Ready Medical Laminates, and Premium Flexibles

The sector’s 2025 cadence underscores capacity expansion and circular-ready innovation. In August 2025, Amcor reported strong FY results and expanded its healthcare network in Costa Rica, tightening lead times for regional device and pharma customers. That same month, Constantia Flexibles disclosed €100M+ investments into its global footprint for food and pharma flexibles, while the Glass Packaging Institute convened a coalition on small-format recovery a signal of broader packaging circularity that influences healthcare portfolios.

ESG credibility and market outlook strengthened mid-year. In July 2025, Huhtamaki earned EcoVadis Gold for the fifth straight year, and a new market report projected medical flexible packaging to USD 46.1B by 2035. Earlier, in March 2025, Constantia Flexibles and Aluflexpack AG joined forces to accelerate premium flexible innovation, targeting higher-value, high-barrier healthcare use cases.

On the technology front, February 2025 saw Amcor launch recycle-ready high-shield medical laminates for devices such as diagnostic sensors, catheters, and wound care, while January 2025 brought WorldStar awards for Constantia’s EcoPeelCover and EcoLamHighPlus. Macro conditions remained mixed: June 2025 commentary on a DACH renovation recovery hints at wider industrial cost normalization that can ease energy/logistics pressure across material inputs and sterile-pack operations.

Transformative Trends and Strategic Growth Opportunities Shaping the Healthcare Flexible Packaging Market

Adoption of High-Barrier Transparent Films for Blister Packaging

The healthcare flexible packaging market is witnessing a strategic transition from traditional PVC and PCTFE (Aclar) films to advanced multi-layer polyamide and polyester-based transparent films. This trend is driven by the critical need to protect moisture-sensitive biologics and specialty drugs while reducing material usage and improving sustainability. Multi-layer films combining PET (polyester) and PA (polyamide) offer superior moisture and oxygen barrier performance, ensuring drug stability and efficacy. Sustainability benefits include thinner, lighter films, which lower carbon emissions and support corporate environmental goals. Honeywell’s Aclar® Accel™ demonstrates a cost-effective alternative to PVdC films, balancing high barrier performance with improved supply chain efficiency, underscoring the market's drive for performance and sustainability synergy.

Integration of Smart Packaging Features to Combat Counterfeiting

Rising concerns over drug counterfeiting and stricter track-and-trace regulations, such as the U.S. Drug Supply Chain Security Act (DSCSA), are accelerating the integration of smart packaging features into healthcare flexible packaging. These include digital watermarks, cryptographically secured QR codes, and covert taggants detectable by specialized scanners. Effective anti-counterfeiting strategies employ a layered approach overt features like holograms, covert UV-visible inks, and forensic microscopic markers to enhance security. Blockchain integration further allows tamper-proof, end-to-end traceability across the supply chain, boosting consumer trust and ensuring compliance with regulatory mandates for serialization and electronic tracking.

Development of Patient-Centric, Accessible Packaging for an Aging Population

An important opportunity lies in designing flexible packaging that caters to elderly patients and those with dexterity or visual impairments. Innovations such as easy-tear notches, tactile indicators, braille labeling, large-print text, and easy-open reclosable systems can improve medication adherence and patient safety. Research highlights that packaging difficulties contribute significantly to non-adherence and accidental injuries among older adults. Hermes Pharma’s child-resistant stick pack with laser-cut openings exemplifies how safety and accessibility can coexist, providing a competitive edge for pharmaceutical brands addressing the aging demographic.

Advanced Cold Chain Flexibles for Cell and Gene Therapies

The rapid growth of cell and gene therapies (CGT) presents a high-value opportunity for next-generation flexible insulated packaging. These therapies require ultra-low temperature maintenance (-80°C to -150°C) over extended transit periods. Advanced solutions integrate phase change materials (PCMs) and insulated flexible liners to replace rigid boxes and traditional dry ice shipping, enhancing safety and logistical efficiency. Cryoport Systems and similar biopharma-focused providers are developing purpose-built ultra-cold shipping systems, demonstrating strong market demand for specialized, reliable cold chain solutions in this highly temperature-sensitive segment.

Competitive Landscape: High-Barrier Science, Cleanroom Scale, and Recycle-Ready Platforms Define Leadership

The competitive field is led by global converters and material specialists scaling sterile barrier systems, cleanroom converting, and recycle-ready mono-material platforms, while backing them with security features and global quality systems.

Amcor plc Recycle-ready sterile laminates plus global capacity expansion

Amcor’s healthcare portfolio spans flexible films, pouches, and bags for medical devices and pharmaceuticals. In August 2025, it expanded its network in Costa Rica and earlier (April 2025) commissioned an advanced coating facility in Selangor, Malaysia, the first in Asia to produce top and bottom substrates for sterile packs on one campus. Strategy centers on sustainability by design (all packaging recyclable/reusable by 2025). Flagships include AmSky® (vinyl- and aluminum-free, all-PE blister) and HealthCare Recycle-Ready Medical Laminates (mono-PE high-shield), enabling circularity without sacrificing sterility assurance.

Constantia Flexibles Group GmbH Premium flexibles with award-winning sterile barriers

Constantia delivers films, foils, and laminates tailored to pharma/drug delivery and medical device needs. In January 2025, it won WorldStar awards for EcoPeelCover and EcoLamHighPlus, evidencing leadership in sustainable, easy-open, high-barrier systems. The company’s strategy focuses on resource-efficient, recyclable structures for healthcare. In August 2025, Constantia announced €100M+ network upgrades and, in March 2025, partnered with Aluflexpack to scale premium innovation for sterile, compliance-critical applications.

Huhtamaki Oyj ESG-verified healthcare films, laminates, and pouches

Huhtamaki supplies films/laminates/pouches for medical devices and pharma with a design ethos around recyclable/compostable solutions where feasible. In July 2025, it achieved EcoVadis Gold for the fifth consecutive year, reinforcing supply-chain ESG credentials valued by healthcare procurement. Strategic focus: become the first choice in sustainable packaging, lowering environmental impact while preserving hygiene, safety, and sterility requirements fundamental to regulated healthcare channels.

Tekni-Plex, Inc. Materials science depth in moisture/oxygen barrier systems

Tekni-Plex develops blister barrier films, sterile-barrier materials, flexible films, and lidding foils with cleanroom manufacturing. Its portfolio includes Aclar® PCTFE and Vaposhield™ laminations that deliver superior MVTR/OTR control for sensitive molecules and devices. Strategy emphasizes patient-outcome-oriented design supporting safer drug delivery and minimally invasive therapies backed by custom engineering and a global footprint for validated, specification-driven supply.

Sonoco Products Company End-to-end healthcare flexibles and cold-chain assurance

Sonoco provides high-barrier films, pouches, and medical-grade components fabricated in cleanrooms, with quality systems aligned to regulated markets. Its ThermoSafe® platform offers temperature-assurance packaging that safeguards biologics and temperature-sensitive pharmaceuticals through the supply chain. Strategic focus: performance plus sustainability, investing in new technologies and continuous improvement to meet device, pharma, and clinical logistics requirements worldwide.

Healthcare Flexible Packaging Market Share Insights

Blister Packs Dominate Market Share by Product Type in the Healthcare Flexible Packaging Industry

Blister packs hold the largest share at around 30%, cementing their position as the unit-dose standard in pharmaceutical packaging. Their dominance is closely linked to global regulatory requirements and patient compliance trends, which mandate precise, tamper-evident, and moisture-resistant formats for oral solid dosages. Blister packaging offers a clear visibility of the drug, facilitates adherence monitoring, and supports child-resistant yet senior-friendly designs. Their compatibility with high-speed filling lines makes them indispensable for mass-scale pharmaceutical production. Pouches follow with a significant 25% share, serving multi-dose packs, sterile medical device kits, and liquid formulations. Bags and sachets, while smaller, are essential for IV fluids, bulk APIs, and precision-dose applications. Strip packs and high-barrier wraps remain niche but critical, providing lower-cost alternatives for OTC drugs and protective layers for logistics. Collectively, the market segmentation illustrates how healthcare flexible packaging balances sterility, compliance, and cost efficiency across diverse use cases.

Pharmaceutical Companies Secure the Largest Share by End-Use in the Healthcare Flexible Packaging Market

Pharmaceutical companies dominate with an estimated 60% share, underscoring their role as the primary demand driver in healthcare flexible packaging. Every unit of drug produced requires compliant packaging ranging from blister packs and sachets for retail distribution to pouches and bags for bulk and sterile applications. Regulatory frameworks such as FDA’s CFR 21 and EMA’s Annex 1 mandate barrier integrity, tamper evidence, and sterility assurance, making packaging a non-negotiable component of pharmaceutical product design. Medical device companies, with around 25% share, represent the high-value specialist segment where sterile barrier systems like Tyvek® pouches and header bags are integral to product safety and ISO 11607 compliance. Hospitals and clinics, retail pharmacies, and home healthcare contribute smaller shares, reflecting their role as end-users rather than specifiers. The fastest growth is expected in home healthcare, driven by decentralization of care and rising demand for convenient compliance packs and sterile kits designed for at-home therapies.

United States: Regulatory Oversight and Patient-Centric Innovations Drive Healthcare Flexible Packaging

The United States healthcare flexible packaging market is heavily influenced by stringent FDA regulations and federal policies such as the Inflation Reduction Act of 2022, which incentivizes energy-efficient upgrades and adoption of high-performance materials. The market is witnessing significant technological advancements, including AI-powered automated recycling systems that enhance the identification, sorting, and processing of recyclable materials with remarkable efficiency.

Corporate initiatives are also shaping the market, with companies like Georgia-Pacific introducing water-based barrier coatings for corrugated boxes, offering sustainable alternatives to traditional packaging. Patient-centric design is becoming a core trend, emphasizing features such as easy-open closures, clear dosage markings, and intuitive designs to improve medication adherence, especially for elderly and visually impaired patients. The rise of e-commerce and home healthcare services is driving demand for durable, lightweight, and eco-friendly packaging solutions, while ongoing investments in R&D focus on advanced barrier films, tamper-evident features, and smart packaging incorporating RFID tags and QR codes for enhanced traceability and anti-counterfeiting measures.

Germany: Circular Economy Leadership and Smart Packaging Innovations Enhance Market Growth

Germany’s healthcare flexible packaging industry is characterized by a stringent regulatory framework, notably the EU Packaging and Packaging Waste Regulation (PPWR), effective from February 2025. This regulation mandates full recyclability or reuse of all packaging by 2030, with minimum targets for recycled content. The country leads in circular economy initiatives, with the Packaging Act (Verpackungsgesetz) holding producers accountable for the full lifecycle of their packaging, thereby driving innovation in recyclability.

Technological innovation is central to Germany’s market growth, with companies developing mono-material films, high-strength recycled fibers, and smart packaging solutions featuring embedded sensors for humidity, temperature, and real-time tracking. These innovations not only reduce spoilage and waste but also support sustainability goals. Corporate consolidation is also occurring, exemplified by Palm’s 2025 acquisition of corrugated box plants from International Paper to strengthen market position and align with EU environmental standards.

China: Government Initiatives and Regulatory Reforms Propel Sustainable Packaging Demand

China’s healthcare flexible packaging market is being transformed by the government’s “dual carbon” strategy and sustainability-focused policies promoting eco-friendly and reusable materials. Technological advancements, including automation and AI integration with “5G plus industrial internet,” are optimizing production processes and enhancing flexible production capacity.

Regulatory reforms, such as the release of the Chinese Pharmacopoeia 2025 edition, introduce new standards, testing methods, and international harmonization via ICH Q4B, increasing demand for high-quality packaging compliant with these requirements. Sustainability efforts are further emphasized through policies restricting non-degradable plastics, creating demand for paper-based and recyclable alternatives. Market consolidation is underway as smaller, less-efficient mills close, favoring larger producers. Data exclusivity measures by the NMPA, including streamlined QMS requirements for localized manufacturing, encourage foreign investment while maintaining stringent safety standards.

India: Policy Support and Growing Healthcare Needs Fuel Flexible Packaging Adoption

India’s healthcare flexible packaging sector is supported by government initiatives like “Make in India” and “Zero Effect Zero Defect,” which enhance domestic production quality and infrastructure. The Production Linked Incentive (PLI) Scheme incentivizes standardized, high-quality packaging solutions, while regulatory amendments to the Plastic Waste Management Rules mandate traceability through barcodes or QR codes for plastic and multilayered packaging.

The market benefits from a rising urbanized population and increasing disposable income, fueling demand for convenient, single-serve, and on-the-go healthcare products. Rapid growth in India’s pharmaceutical and healthcare sectors, driven by an aging population and increasing chronic disease prevalence, is generating strong demand for secure, tamper-evident, and child-resistant packaging. Additionally, joint ventures such as that between Indorama Ventures, Dhunseri Ventures, and Varun Beverages are driving improvements in recycling rates, reflecting a growing focus on sustainability in packaging practices.

Brazil: Regulatory Compliance and Technological Advancements Strengthen Market Position

Brazil’s healthcare flexible packaging market is influenced by the National Solid Waste Policy, which promotes a circular economy and encourages the adoption of reusable and durable packaging solutions. Technological advancements, including AI and robotics, are being incorporated to enhance efficiency, quality control, and sophisticated operations such as automated sorting and defect detection.

Sustainability remains a key focus, reinforced by policies banning the import of solid waste, including plastics, to encourage domestic waste management. Strategic investments by ANVISA aim to modernize regulatory controls for herbal medicines and other healthcare products, ensuring safe and effective packaging. Compliance with the revised positive list of substances for food contact plastics ensures that flexible packaging materials meet updated health and safety standards, while data privacy regulations under the Brazilian General Data Protection Law (LGPD) impact smart packaging solutions that collect patient information.

Japan: Aging Population and E-commerce Growth Drive Functional and Sustainable Packaging

Japan’s healthcare flexible packaging market is propelled by an aging population, projected to reach 38 million people aged 65 and above by 2025. This demographic trend drives demand for easy-to-open, child-resistant, and integrity-assured packaging. Technological advancements are enabling the production of high-performance materials with specialized properties for enhanced functionality.

Regulatory updates from the Ministry of Health, Labour and Welfare (MHLW), including migration limits for synthetic resin materials, are ensuring safer packaging. Sustainability is a priority, with recyclable and reusable materials gaining preference among eco-conscious consumers. Functional innovations, including high dimensional stability and resistance to deformation, are critical for high-performance applications. The rapid growth of e-commerce further accelerates demand for durable, customizable, and branded flexible packaging solutions, integrating advanced printing and technology to meet the evolving healthcare market needs.

Healthcare Flexible Packaging Market Report Scope

Healthcare Flexible Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.7 Billion

|

|

Market Size (2034)

|

$46.9 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Product Type (Blister Packs, Pouches, Bags, Sachets, Strip Packs, Wraps), By Material (PE, PP, PVC, PET, Aluminum, Paper & Paperboard), By Application (Pharmaceutical Manufacturing, Medical Device Manufacturing, Contract Packaging, Drug Delivery Systems, In Vitro Diagnostic Products), By End-Use (Hospitals & Clinics, Pharmaceutical Companies, Medical Device Companies, Retail Pharmacies, Home Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamäki Oyj, Constantia Flexibles, Sealed Air Corporation, Berry Global Group, Inc., Tekni-Plex, Inc., Sonoco Products Company, Mondi Group, Printpack, WestRock Company, Winpak Ltd., Klöckner Pentaplast, Uflex Ltd., Albéa S.A., Reynolds Consumer Products

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Healthcare Flexible Packaging Market Segmentation

By Product Type

- Blister Packs

- Pouches

- Bags

- Sachets

- Strip Packs

- Wraps

By Material

- PE

- PP

- PVC

- PET

- Aluminum

- Paper & Paperboard

By Application

- Pharmaceutical Manufacturing

- Medical Device Manufacturing

- Contract Packaging

- Drug Delivery Systems

- In Vitro Diagnostic Products

By End-Use

- Hospitals & Clinics

- Pharmaceutical Companies

- Medical Device Companies

- Retail Pharmacies

- Home Healthcare

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Healthcare Flexible Packaging Market

- Amcor plc

- Huhtamäki Oyj

- Constantia Flexibles

- Sealed Air Corporation

- Berry Global Group, Inc.

- Tekni-Plex, Inc.

- Sonoco Products Company

- Mondi Group

- Printpack

- WestRock Company

- Winpak Ltd.

- Klöckner Pentaplast

- Uflex Ltd.

- Albéa S.A.

- Reynolds Consumer Products

* List Not Exhaustive

Methodology

USDAnalytics applies a comprehensive research methodology to provide actionable insights into the Healthcare Flexible Packaging Market. Our approach combines primary interviews with packaging engineers, procurement leaders, and R&D specialists, alongside extensive secondary research from regulatory filings, corporate reports, and verified industry databases. We analyze trends in high-barrier films, blister packs, pouches, anti-counterfeiting technologies, patient-centric designs, and cold chain solutions across pharmaceuticals, medical devices, and home healthcare sectors. Quantitative modeling integrates historical market performance, material adoption, regulatory impact, and emerging trends such as recycle-ready mono-materials and smart packaging integration. Competitive analysis examines capacity expansions, technological innovations, ESG compliance, and global regional growth drivers, producing forecasts for 2025–2034. USDAnalytics synthesizes these findings to highlight strategic opportunities, regulatory influences, and market segmentation by product type, material, application, and end-use, offering industry professionals a data-driven foundation to inform investment, product development, and compliance strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.