Hollow Fiber Ultrafiltration Market Growth Outlook and Key Insights

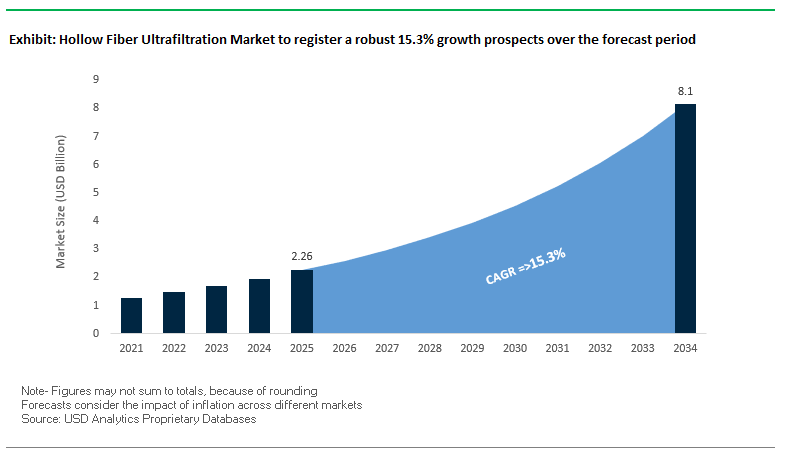

The Hollow Fiber Ultrafiltration Market is projected to grow from $2.26 billion in 2025 to $8.1 billion by 2034, registering a strong CAGR of 15.3%. This rapid expansion reflects rising demand for advanced water purification technologies, industrial wastewater reuse, and high-purity bioprocessing applications.

Key Market Insights Driving Growth:

- Public Awareness & Environmental Concerns: Rising global concern over microplastics, waterborne diseases, and emerging contaminants is positioning hollow fiber ultrafiltration as a frontline solution for safe drinking water.

- Industrial Wastewater Reuse: Regulatory pressures on sustainable industrial practices are pushing industries toward closed-loop water systems using ultrafiltration as a critical step.

- Pharmaceutical & Bioprocessing Growth: High-purity processes for biologics, gene therapies, and plasma-derived products are driving demand for precision separation and purification technologies.

- Aging Water Infrastructure: Municipalities in North America and Europe are upgrading outdated infrastructure with ultrafiltration-based systems to ensure regulatory compliance and water safety.

Market Analysis: Recent Developments Shaping the Hollow Fiber Ultrafiltration Market

The hollow fiber ultrafiltration industry has seen a surge of strategic partnerships, product launches, and sustainability-driven initiatives in 2025 that are reshaping the competitive landscape.

In July 2025, SUEZ commissioned China’s largest industrial membrane-based seawater desalination plant, where hollow fiber ultrafiltration plays a vital role as a pre-treatment step to support industrial water supply. In the same month, Asahi Kasei’s Microza® hollow fiber membrane received a Gold rating in the EcoVadis sustainability assessment, placing the company among the top 5% in environmental responsibility. Meanwhile, SUEZ and the Senegalese government were recognized by the United Nations for their PPP water project in Africa, demonstrating the global expansion of ultrafiltration solutions in developing regions.

In June 2025, Koch Technology Solutions (KTS) reported the successful full-capacity operation of a major PTA production line licensed to a petrochemical company. This development highlights the use of advanced process technologies, including membrane-based separations, in large-scale industrial operations. Earlier, in March 2025, DuPont Water Solutions launched WAVE PRO, a digital modeling tool enabling water Stakeholders to optimize ultrafiltration designs for drinking water, industrial utilities, and wastewater treatment.

The second half of 2025 continued with significant momentum. In May 2025, Asahi Kasei unveiled its medium-term growth plan, “Trailblaze Together,” prioritizing its life science division with a strong focus on ultrafiltration technologies like Planova™ filters. In August 2025, a peer-reviewed scientific study reinforced the role of hollow fiber ultrafiltration in treating radioactive and heavy metal wastewater, citing superior efficiency and prevention of secondary pollution.

Emerging Trends and Market Opportunities in the Hollow Fiber Ultrafiltration Market

Increasing Global Demand for Advanced Water and Wastewater Treatment

A dominant trend shaping the hollow fiber ultrafiltration market is the escalating demand for advanced water and wastewater treatment technologies. Municipalities and industries worldwide are under mounting pressure to comply with stringent drinking water standards and implement sustainable water reuse practices. Hollow fiber UF membranes are increasingly deployed as a pre-treatment step for reverse osmosis (RO) systems, particularly in municipal drinking water plants and industrial reuse applications. This trend is further fueled by rising water scarcity concerns and government mandates for wastewater recycling, making UF systems a cornerstone of modern water infrastructure.

Rising Adoption of High-Value Biopharmaceutical Applications

The biotechnology and pharmaceutical industries represent a rapidly expanding area for hollow fiber ultrafiltration technology. Hollow fiber UF is essential for critical processes such as protein purification, virus removal, and cell harvesting. The global surge in biologics production, including monoclonal antibodies and vaccines, has significantly expanded demand for high-performance UF membranes. Since this sector prioritizes regulatory compliance, sterility, and product purity over cost, manufacturers of UF membranes see strong growth opportunities in supplying validated, premium-grade solutions tailored to biopharmaceutical workflows.

Opportunities in Food, Beverage, and High-Performance Industrial Sectors

Another key opportunity lies in the food and beverage sector, where hollow fiber UF is increasingly applied for whey protein recovery, juice clarification, and alcohol stabilization. Unlike wastewater treatment, these applications generate direct economic value by enabling producers to recover valuable proteins and extend product shelf life while maintaining quality. Additionally, niche opportunities are emerging in the chemical, petrochemical, and power industries, where hollow fiber UF membranes provide reliable separation in oil-water processing, catalyst recovery, and pre-treatment for power plant boilers. While smaller in scale, these segments highlight the versatility of UF technology and its growing role in specialized industrial operations.

Market Share Analysis of the Hollow Fiber Ultrafiltration Market

Market Share by Material Composition

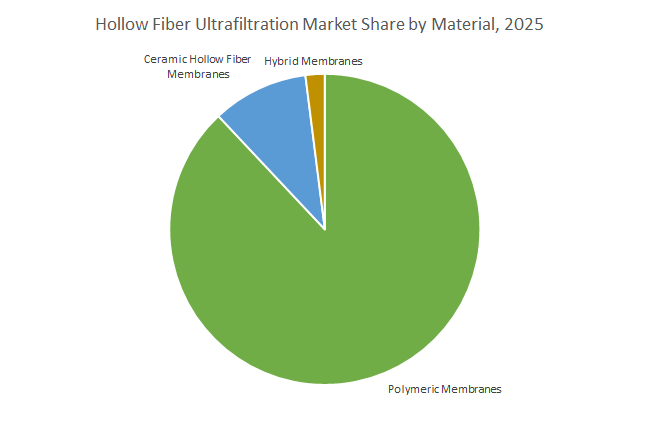

Polymeric membranes dominate the hollow fiber ultrafiltration market with an estimated 88% share by 2025, driven by their cost-effectiveness, versatility, and proven performance across large-scale water and wastewater treatment facilities. Materials such as PVDF and PES have become industry standards due to their balance of durability, manufacturability, and fouling resistance. Ceramic hollow fiber membranes, projected at 10% share, are the fastest-growing category, as industries requiring long lifespans, aggressive chemical cleaning, and high-temperature resistance increasingly favor them despite higher upfront costs. Hybrid membranes, still in an emerging stage at around 2% share, are attracting research and pilot projects for their ability to combine polymeric flexibility with ceramic-like durability and antifouling properties, positioning them as a future disruptive force.

Market Share by Application Areas

Water and wastewater treatment accounts for the largest share of the hollow fiber UF market at approximately 65% by 2025, fueled by the global push for water reuse, potable water quality compliance, and UF’s role as a critical pre-treatment for RO systems. Biotechnology and pharmaceutical applications, while smaller at 15%, represent the highest-value segment, as UF membranes are indispensable for purifying proteins, concentrating biologics, and ensuring regulatory compliance in drug manufacturing. The food and beverage sector, at 12%, is steadily expanding with applications in whey protein concentration, milk processing, and juice clarification, aligning with consumer demand for high-value nutritional products. Chemical and petrochemical processing, with a 5% share, leverages UF for oil-water separation and catalyst recovery, while the remaining 3% encompasses power, pulp and paper, and niche industrial uses, where UF membranes deliver consistent reliability in sidestream and process water treatment.

China: Regulatory Compliance and Industrial Expansion Driving Hollow Fiber Ultrafiltration Adoption

China’s hollow fiber ultrafiltration (UF) market is propelled by stringent regulatory frameworks, technological innovations, and rapid industrial and municipal growth. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, pushing companies to adopt advanced hollow fiber ultrafiltration membranes to comply with environmental regulations. In 2024, Chinese researchers developed new UF membranes with enhanced antifouling properties, significantly improving the long-term efficiency and reducing maintenance costs of membrane bioreactors (MBRs), where microfiltration and ultrafiltration are key components. The country’s expanding wastewater treatment sector, including treatment of radioactive and heavy metal effluents, further drives demand for hollow fiber UF membranes in multi-stage water treatment systems. Additionally, government investments outlined in the 14th Five-Year Plan (2021-2025) to expand natural gas infrastructure are increasing adoption of ultrafiltration technologies in the oil and gas industry, positioning China as a crucial market for hollow fiber ultrafiltration solutions.

United States: Government Funding and Private Sector Initiatives Accelerating Market Growth

The United States hollow fiber ultrafiltration market is strengthened by substantial government funding, cutting-edge academic research, and private-sector innovation. The Bipartisan Infrastructure Law allocates over $50 billion to the Environmental Protection Agency (EPA) to modernize drinking water, wastewater, and stormwater infrastructure, including treatment of emerging contaminants like PFAS, which necessitates advanced ultrafiltration membranes. Research centers funded by the National Science Foundation (NSF) are developing next-generation hollow fiber UF membranes for water purification, chemical separations, and biopharmaceutical applications, providing continuous technological innovation. Private companies, such as Veolia Water Technologies, are deploying hollow fiber ultrafiltration systems as pretreatment steps to deliver safe water with regulated PFAS levels to over 140,000 Americans. The synergy between government support, academic research, and corporate deployment positions the U.S. as a leading market for hollow fiber ultrafiltration solutions.

India: Government Programs and Infrastructure Investments Fueling Hollow Fiber UF Adoption

India’s hollow fiber ultrafiltration market is witnessing robust growth driven by government programs, strategic infrastructure investments, and industrial adoption. The Jal Jeevan Mission, along with the Department of Science & Technology’s Water Technology Initiative, promotes R&D in advanced filtration technologies to ensure safe and affordable drinking water in rural areas. The Ghaziabad Nagar Nigam, India’s first Certified Green Municipal Bond issuer, raised ₹150 crore to develop a state-of-the-art Tertiary Sewage Treatment Plant (TSTP) utilizing hollow fiber UF membranes for wastewater reuse, reducing reliance on freshwater. Furthermore, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, highlights industrial-scale adoption of hollow fiber ultrafiltration technology, reinforcing India’s growing significance in the global UF membrane market.

Germany: Industrial Leadership and Technological Advancements in Ultrafiltration

Germany is a key market for hollow fiber ultrafiltration, driven by industrial wastewater treatment expertise and technological innovation. Companies such as PWT Wassertechnik specialize in ultrafiltration processes for industrial water reuse, ensuring compliance with stringent European environmental regulations. MANN+HUMMEL focuses on developing innovative hollow fiber UF membranes, filtration solutions, and digital technologies to address global water challenges, particularly in industrial and green energy applications. Germany’s integrated approach of regulatory compliance, industrial focus, and technological advancement positions it as a leader in the hollow fiber ultrafiltration sector.

Japan: Academic Research and Global Technological Leadership

Japan is a prominent player in hollow fiber ultrafiltration innovation, fueled by academic research and corporate technology development. Kobe University’s Membrane Engineering Group highlighted in 2024 its work on functional, biomimetic, and highly porous hollow fiber membranes for water and atmospheric applications. Toray Industries, a global leader in membrane technologies, continues to develop high-performance RO and ultrafiltration membranes for large-scale projects, including Saudi Arabian desalination plants where hollow fiber UF membranes are used as pretreatment. Japan’s focus on research excellence and global deployment underscores its pivotal role in advancing hollow fiber ultrafiltration technologies worldwide.

Australia: Water Recycling and Academic Research Driving Sustainable UF Solutions

Australia, a country facing significant water stress, is leveraging hollow fiber ultrafiltration in water recycling and reuse initiatives. The Sydney Water Wollongong Water Resource Recovery Facility employs a combination of microfiltration and ultrafiltration alongside reverse osmosis to treat wastewater for irrigation and industrial reuse. Academic research at the Institute for Sustainable Industries and Liveable Cities (ISILC), Victoria University, focuses on enhancing water recovery from desalination and mitigating membrane fouling and scaling, addressing critical challenges in sustainable water treatment. These efforts position Australia as a strategic adopter of hollow fiber ultrafiltration solutions for resilient and efficient water management.

Competitive Landscape of the Hollow Fiber Ultrafiltration Market

The competitive dynamics of the hollow fiber ultrafiltration industry are shaped by leading global players who combine material science expertise, digital innovation, sustainability initiatives, and large-scale project execution. Companies are strengthening their portfolios through R&D, partnerships, and facility expansions to capture demand across municipal, industrial, pharmaceutical, and bioprocessing applications.

DuPont Water Solutions Strengthens Market with Digital Tools and Sustainability Initiatives

DuPont Water Solutions is advancing market leadership by integrating digital solutions with sustainable membrane technologies. Its launch of WAVE PRO in March 2025 allows water Stakeholders to model and optimize ultrafiltration systems, ensuring both technical efficiency and cost-effectiveness. The company’s Sustainability Navigator further supports customers in evaluating environmental footprints across carbon emissions, chemical use, and waste reduction. With a comprehensive portfolio spanning municipal water treatment, seawater desalination, and industrial applications, DuPont remains a frontrunner in meeting the world’s growing demand for sustainable water solutions.

SUEZ Expands Global Presence with Mega-Scale Ultrafiltration Projects

SUEZ Water Technologies & Solutions continues to expand its global presence with large-scale infrastructure projects. In July 2025, it commissioned China’s largest seawater desalination plant, where hollow fiber ultrafiltration is central to operations. The company has also partnered with CNRS for long-term research in sustainable water management and is leveraging its UK Smart Operations Centre to digitize and automate ultrafiltration monitoring. By combining infrastructure expertise with circular economy initiatives such as biochar production, SUEZ demonstrates its leadership in next-generation water management solutions.

Toray Industries Innovates with Energy-Efficient Ultrafiltration Modules

Toray Industries, Inc. brings unmatched polymer science expertise to the hollow fiber ultrafiltration market. Its PVDF-based membranes offer superior durability and chemical resistance, making them suitable for high-turbidity and high-viscosity water treatment. Recently, Toray developed energy-efficient ultrafiltration modules for the food and beverage industry, cutting CO2 emissions by over 80% compared to thermal concentration methods. With a diverse product portfolio covering pressurized and submerged UF modules, Toray is actively collaborating with global engineering firms to expand its applications in industrial, municipal, and F&B sectors.

Asahi Kasei Strengthens Life Sciences Focus with Sustainable Growth Strategy

Asahi Kasei Corporation is consolidating its position in the biopharmaceutical ultrafiltration segment with its flagship Planova™ virus removal filters, widely used in biologics and plasma therapy production. In May 2025, the company announced its “Trailblaze Together” growth plan, positioning life sciences at the core of its expansion strategy. Its Microza® membranes received global recognition with a Gold EcoVadis rating, highlighting sustainable manufacturing excellence. The company is also constructing a new spinning plant for Planova™ filters, further enhancing its supply chain resilience in the global bioprocessing sector.

Koch Membrane Systems (KMS) Delivers Custom Ultrafiltration Solutions Across Industries

Koch Membrane Systems (KMS) leverages more than 50 years of engineering expertise to deliver custom-designed ultrafiltration solutions across water treatment, life sciences, and food and beverage applications. Its TARGA® II Hollow Fiber UF system is designed for high packing density, reducing capital costs and system footprint for end-users. KMS is actively deploying commercial-scale projects, including its role in lithium extraction processes, highlighting its technical depth in highly demanding industrial applications. The company continues to position itself as a trusted provider of efficient, long-lasting hollow fiber ultrafiltration membranes.

Hollow Fiber Ultrafiltration Market Report Scope

Hollow Fiber Ultrafiltration Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.26 Billion

|

|

Market Size (2034)

|

$8.1 Billion

|

|

Market Growth Rate

|

15.3%

|

|

Segments

|

By Material (Polymeric Membranes, Ceramic Hollow Fiber Membranes, Hybrid), By Module Design (Inside-Out Filtration, Outside-In Filtration), By Application (Water & Wastewater Treatment, Food & Beverage Processing, Biotechnology & Pharmaceutical Processing, Chemical & Petrochemical Processing, Power Generation, Pulp & Paper Industry, Others), By End-User (Municipal Utilities, Industrial, Commercial, Residential)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, DuPont de Nemours, Inc., SUEZ, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Koch Industries, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, W. L. Gore & Associates, Inc., Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hollow Fiber Ultrafiltration Market Segmentation

By Material

- Polymeric Membranes

- Polyvinylidene Fluoride

- Polyethersulfone

- Polysulfone

- Cellulose Acetate

- Ceramic Hollow Fiber Membranes

- Hybrid

By Module Design

- Inside-Out Filtration

- Outside-In Filtration

By Application

- Water & Wastewater Treatment

- Food & Beverage Processing

- Biotechnology & Pharmaceutical Processing

- Chemical & Petrochemical Processing

- Power Generation

- Pulp & Paper Industry

- Others

By End-User

- Municipal Utilities

- Industrial

- Commercial

- Residential

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Hollow Fiber Ultrafiltration Industry include-

- Veolia

- DuPont de Nemours, Inc.

- SUEZ

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Koch Industries

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- W. L. Gore & Associates, Inc.

- Merck KGaA

*- List not Exhaustive

Research Coverage

This report investigates the hollow fiber ultrafiltration (UF) market, delivering analysis reviews on demand shifts from safe drinking water and industrial reuse to high-purity bioprocessing. It highlights breakthroughs in PVDF/PES module engineering, outside-in/inside-out flow optimization, and digital design tools that lower energy use, cleaning frequency, and footprint while safeguarding downstream RO and critical biologics steps. The study further highlights how aging municipal assets, microplastics awareness, and pathogen/PFAS compliance are pulling UF into the core of new build and retrofit programs across North America, Europe, and fast-growing Asian markets. Mapping project pipelines, module preferences, and end-user qualification criteria, USDAnalytics provides decision-grade evidence on cost curves, reliability metrics, and validation practices making this report an essential resource for utilities, EPCs, membrane OEMs, and bioprocess leaders planning scalable, regulation-ready UF deployments. Scope Includes-

- Segmentation: By Material (Polymeric: PVDF, PES, PS, Cellulose Acetate; Ceramic Hollow Fiber; Hybrid), By Module Design (Inside-Out Filtration, Outside-In Filtration), By Application (Water & Wastewater Treatment; Food & Beverage Processing; Biotechnology & Pharmaceutical Processing; Chemical & Petrochemical Processing; Power Generation; Pulp & Paper; Others), By End-User (Municipal Utilities; Industrial; Commercial; Residential)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic 2021–2024; Forecast 2025–2034.

- Companies: Profiles of 15+ companies

Methodology

We combine primary interviews (utilities, EPCs, OEMs, bioprocess engineers, QA/validation leads) with secondary validation (standards, filings, peer-reviewed technical literature) to triangulate market size and growth. Top-down models link municipal/industrial capex, retrofits, and reuse mandates to installed UF capacity; bottom-up bill-of-materials models account for module area, flux (LMH), trans-membrane pressure, cleaning intervals (CIP/SIP), and integrity-test regimes to derive lifetime cost and replacement cycles. Forecasts apply learning curves for polymeric/ceramic lines, sensitivity to energy/chemistry prices, and scenario stress-tests for pathogen log-removal and microplastics rules. Competitive benchmarking evaluates membrane chemistry, hydrodynamics (outside-in vs. inside-out), fouling/cleanability, and digital design/monitoring tools. All numbers undergo cross-checks against announced projects, qualification timelines in bioprocessing, and historical commissioning rates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Hollow Fiber Ultrafiltration Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Hollow Fiber Ultrafiltration Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $2.26 Billion

2.2.2. Forecasted Market Size (2034): $8.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 15.3%

2.3. Key Market Trends and Opportunities

2.3.1. Increasing Global Demand for Advanced Water Treatment

2.3.2. Rising Adoption of High-Value Biopharmaceutical Applications

2.3.3. Opportunities in Food, Beverage, and Industrial Sectors

2.4. Drivers, Restraints, and Challenges

2.4.1. Drivers: Public Awareness, Industrial Reuse, Biopharma Growth

2.4.2. Restraints: High Capital Expenditure and Maintenance

2.4.3. Challenges: Membrane Fouling and Supply Chain Vulnerabilities

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Digitalization and Optimization

3.1.1. DuPont Launches WAVE PRO Digital Tool

3.1.2. SUEZ’s UK Smart Operations Centre

3.2. Market Trend: Sustainability and ESG Integration

3.2.1. Asahi Kasei’s Gold EcoVadis Rating

3.2.2. Hollow Fiber UF for Radioactive Wastewater

3.3. Market Opportunity: Global Infrastructure and Partnerships

3.3.1. SUEZ Commissions China’s Largest Desalination Plant

3.3.2. SUEZ and Senegalese Government UN Recognition

3.3.3. Koch Technology Solutions’ Full-Capacity Operation

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Innovators to Solution Providers

4.2. Key Competitive Factors

4.2.1. Product Portfolio and Customization Capabilities

4.2.2. R&D Investment in New Materials and Systems

4.2.3. Strategic Partnerships and Global Project Execution

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ Water Technologies & Solutions

4.3.3. Toray Industries, Inc.

4.3.4. Asahi Kasei Corporation

4.3.5. Koch Membrane Systems (KMS)

5. Hollow Fiber Ultrafiltration Market – Segmentation Insights

5.1. By Material Composition

5.1.1. Polymeric Membranes

5.1.2. Ceramic Hollow Fiber Membranes

5.1.3. Hybrid Membranes

5.2. By Application Areas

5.2.1. Water & Wastewater Treatment

5.2.2. Biotechnology & Pharmaceutical Processing

5.2.3. Food & Beverage Processing

5.2.4. Chemical & Petrochemical Processing

5.2.5. Others (Power, Pulp & Paper, etc.)

6. Country Analysis and Outlook: Hollow Fiber Ultrafiltration Market

6.1. China: Regulatory Compliance and Industrial Expansion

6.2. United States: Government Funding and Private Sector Initiatives

6.3. India: Government Programs and Infrastructure Investments

6.4. Germany: Industrial Leadership and Technological Advancements

6.5. Japan: Academic Research and Global Technological Leadership

6.6. Australia: Water Recycling and Academic Research

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Hollow Fiber Ultrafiltration Market Size Outlook by Region (2025-2034)

7.1. North America Hollow Fiber Ultrafiltration Market Size Outlook to 2034

7.1.1. By Material

7.1.2. By Application

7.2. Europe Hollow Fiber Ultrafiltration Market Size Outlook to 2034

7.2.1. By Material

7.2.2. By Application

7.3. Asia Pacific Hollow Fiber Ultrafiltration Market Size Outlook to 2034

7.3.1. By Material

7.3.2. By Application

7.4. South America Hollow Fiber Ultrafiltration Market Size Outlook to 2034

7.4.1. By Material

7.4.2. By Application

7.5. Middle East and Africa Hollow Fiber Ultrafiltration Market Size Outlook to 2034

7.5.1. By Material

7.5.2. By Application

8. Company Profiles: Additional Leading Players

8.1. Veolia

8.2. DuPont de Nemours, Inc.

8.3. SUEZ

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Koch Industries

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. LG Chem

8.14. W. L. Gore & Associates, Inc.

8.15. Merck KGaA

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures