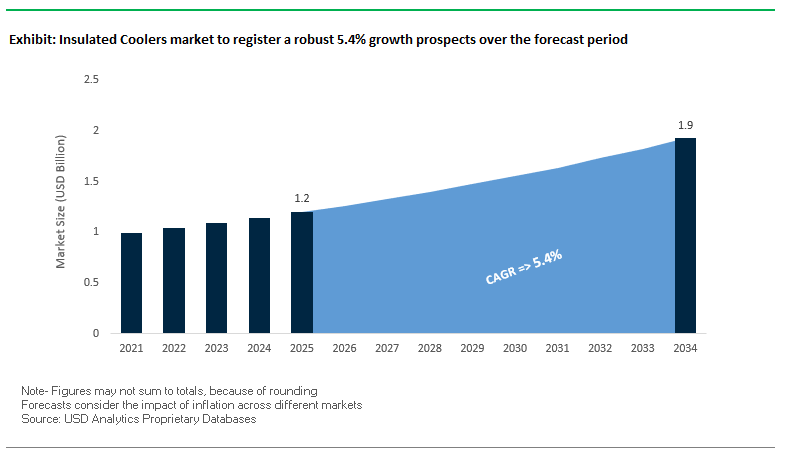

Market Overview: Insulated Coolers Market to Reach $1.9 Billion by 2034 on Multi-Day Ice Retention, Smart Features, and Portability

The global insulated coolers market is valued at $1.2 billion in 2025 and is projected to reach $1.9 billion by 2034, growing at a CAGR of 5.4%. Buyers ranging from specialty retail to big-box and DTC prioritize ice retention, durability, and portability to serve use cases from multi-day camping and offshore fishing to tailgates and beach trips. Technology and materials are the core differentiators: rotomolded polyethylene shells, closed-cell foam, and emerging vacuum insulated panels (VIPs) are raising thermal performance while holding weight and footprint in check. A second growth engine is feature-rich smart coolers with USB power, LED lighting, and Bluetooth audio plus the fast-growing wheeled cooler segment that removes the friction of transport.

Key Insights for Industry Stakeholders

- Thermal performance leads conversion: Multi-day ice retention is the #1 driver of premium adoption for backcountry and pelagic users.

- Materials race: Rotomolded PE + closed-cell foams remain the insulation standard; VIPs are emerging for compact, high-R-value designs.

- Smart + connected: USB/solar charging, LEDs, speakers and ruggedized power management expand AOV and attach rates.

- Portability premium: Wheeled models are the fastest-growing subsegment, unlocking casual and family occasions (beach, tailgate, events).

Market Analysis: Product News and Strategic Moves Signal Premiumization and Brand Reach (2024–2025)

The category’s recent cadence underscores premiumization, brand storytelling, and supply-chain resilience. In August 2025, Igloo launched a Make It Cooler customization program personalized graphics and finishes that deepen DTC engagement and giftability. Also in August 2025, YETI reported Q2 2025 results indicating a 4% net sales decline amid a more promotional drinkware backdrop, yet highlighted innovation momentum, global expansion, and supply-chain diversification key hedges for its premium cooler franchise.

Brand-building and audience expansion accelerated through campaigns and collaborations. Igloo’s “The Cooler Brand” campaign (June 2025) widened lifestyle positioning beyond elite outdoors, while earlier co-branded drops e.g., Igloo × Minecraft (October 2024) activated new fandoms. Portfolio investment also continued at YETI: in May 2025, the company reported Q1 sales up 3% to $351.1M and guided ~$60M in capex for product innovation and supply-chain diversification supporting pipeline velocity and international growth.

Materials and portability innovation remain front and center. RTIC (October 2024) introduced Ultra-Light Hard Coolers, engineered to be up to 30% lighter than comparable rotomolded units answering demand for easier carry and car-to-site mobility. Upstream, the Smurfit Kappa–WestRock merger (July 2025) forms Smurfit WestRock, a fiber-packaging scale player whose recyclable consumer-packaging advances can enhance shipping, display, and protective packaging around coolers in retail and e-commerce channels. Meanwhile, Igloo (August 2024) debuted its first golf-inspired cooler line, signaling deeper penetration into sport-specific occasions.

Trends and Opportunities Driving the Insulated Coolers Market

Integration of Portable Power and Active Temperature Management Systems

The insulated coolers market is undergoing a technological transformation as manufacturers evolve beyond passive insulation to integrate portable power, thermoelectric modules, and smart connectivity. This shift is redefining insulated coolers as multifunctional devices for both consumer leisure and critical logistics applications. For instance, a leading portable power brand recently launched a 298Wh battery-powered cooler, enabling long-duration temperature control without compromising storage capacity an essential feature for outdoor activities and extended trips.

Precision cooling is emerging as a decisive factor, with thermoelectric systems delivering up to 0.1°C accuracy, meeting the needs of pharmaceuticals and lab-sensitive products. Unlike traditional models, these systems offer dual functionality cooling and heating which dramatically expands application scope from camping and outdoor recreation to catering and medical transport. The addition of Bluetooth connectivity and mobile app control is further enhancing the value proposition, enabling real-time monitoring and adjustments that elevate both consumer convenience and professional reliability. Collectively, these innovations are positioning insulated coolers as active, intelligent tools for temperature management rather than passive storage boxes.

Adoption of Advanced Sustainable Materials and Circular Design Principles

Sustainability is becoming a central competitive lever in the insulated coolers industry, with brands actively investing in recycled inputs, biodegradable foams, and waste-based insulation materials. For example, YETI has introduced new lines incorporating recycled polymers, aligning with corporate carbon reduction targets and consumer expectations for eco-conscious products. Parallel to this, material scientists are developing biodegradable EPS foams that maintain equivalent thermal performance but biodegrade by up to 94% in four years in natural environments, offering a viable alternative to legacy petroleum-based insulation.

Circular innovation is also extending to the use of waste paper-based insulation, which has been successfully piloted by meal kit providers. This material not only reduces carbon emissions but also lowers shipping costs due to its lighter and thinner profile while maintaining comparable insulation efficiency. With governments tightening single-use plastic bans and consumers demanding responsible design, sustainable coolers are no longer niche offerings but mainstream competitive requirements in the global insulated coolers market.

Development of Lightweight, High-Performance Solutions for the Home Delivery Meal Kit Sector

The surge in meal kit and prepared food delivery services presents a compelling growth opportunity for lightweight, customized insulated packaging solutions. Generic bulky coolers are giving way to slim, recyclable liners and shippers designed specifically for portioned meals. For example, one provider’s adoption of paper-based insulation allowed for a 25% reduction in shipping case size, while maintaining interior space translating into lower freight costs and reduced material consumption.

The opportunity lies in scaling tailored insulation formats that integrate seamlessly with corrugated outers, refrigerants, and inner trays. These solutions meet consumer expectations for sustainability and convenience, addressing concerns about packaging waste without compromising food safety. Market research consistently shows that eco-friendly packaging strongly influences subscription retention in the meal kit sector. As such, suppliers that pioneer lightweight, recyclable, or compostable insulation formats are well-positioned to capture share in this fast-growing vertical.

Expansion into Pharmaceutical and Last-Mile Critical Logistics

Another major opportunity for insulated coolers is the regulated pharmaceutical and healthcare logistics segment, particularly in last-mile delivery. The World Health Organization (WHO) estimates that over 50% of vaccines are wasted globally due to cold chain failures. High-performance insulated coolers equipped with Phase Change Materials (PCMs) and validated performance standards provide a proven solution to maintain strict ranges (e.g., 2°C to 8°C) for periods exceeding 72 hours.

The last mile is widely recognized as the weakest link in cold chain logistics, with power disruptions and handling inconsistencies frequently causing thermal excursions. Insulated coolers, especially advanced passive models, eliminate dependency on external power while ensuring reliability. This capability extends beyond vaccines to diagnostic reagents, blood samples, insulin, and high-value biologics, where product loss translates to significant financial and patient safety risks. Companies specializing in pre-qualified insulated shippers are setting benchmarks by validating their systems for compliance with healthcare regulations, underscoring the strategic importance of insulated coolers in the future of temperature-sensitive logistics.

Competitive Landscape: Ice Retention Engineering, Lifestyle Branding, and Price-Value Define Share Battles

The insulated coolers market is concentrated around a handful of scale brands plus value challengers. Differentiation stems from thermal engineering (foam chemistry, wall thickness, gaskets), impact resistance, portability features (wheels, handles), and brand equity. Lifestyle content and DTC strength amplify pricing power, while accessibility and weight-saving designs expand TAM. Premium leaders monetize multi-day performance and lifestyle cachet; value innovators press lighter constructions and aggressive pricing; legacy mass brands leverage channel breadth and trusted functionality.

YETI Holdings, Inc. Premium performance with global lifestyle pull

Overview: YETI anchors the high end with rotomolded hard coolers, rugged soft coolers, and accessories often bear-resistant certified. In H1 2025, it doubled down on R&D and supply-chain diversification to sustain innovation cycles and international growth.

YETI’s strategy is to scale direct-to-consumer (DTC) and flagship wholesale while defending pricing through brand desirability and proven ice-retention leadership. Q2 2025 DTC sales of ~$248.6M underscore channel strength and data feedback loops for product iteration. Ongoing investment (~$60M capex, May 2025) targets new designs and logistics resilience. The brand’s expansion in the UK/EU broadens seasonality and category penetration. YETI’s equity allows premium ASPs while protecting margins despite promotional pressure in adjacent drinkware.

Igloo Coolers Mainstream scale with sustainability and customization

Overview: Igloo spans hard-sided and soft-sided coolers and drinkware, balancing affordability with high-performance lines. Sustainability shows in ECOCOOL® (recycled plastic content).

August 2025 saw Igloo’s Make It Cooler customization program personal design at scale for DTC differentiation. June 2025 “The Cooler Brand” campaign repositions Igloo for everyday fun beyond hardcore outdoor expanding occasions and demographics. Licensed collaborations (October 2024 Minecraft) and sports tie-ins (August 2024 golf collection) create fresh demand spikes and retail theater. Portfolio heroes include Trailmate Journey (oversized wheels) and the iconic Playmate products that reinforce portability + nostalgia.

RTIC Outdoors, LLC “Premium performance without the premium price”

Overview: RTIC targets the value–performance sweet spot with hard/soft coolers and drinkware that benchmark against top-tier specs at accessible prices.

October 2024 launch of Ultra-Light Hard Coolers delivered ~30% weight reduction vs. rotomolded peers at the same capacity addressing the biggest consumer friction: carry burden. RTIC’s injection-molded approaches and tuned foam densities aim at high ice-retention per pound. The brand’s proposition durable, dependable, better-priced wins budget-conscious buyers without severe performance tradeoffs. Positive head-to-head reviews sustain organic word-of-mouth and digital conversion.

Pelican Products, Inc. Extreme-duty coolers for professional use

Overview: Pelican translates its protective case DNA into coolers designed for military, industrial, and expedition environments.

Flagships like Pelican ProGear Elite feature 2-inch polyurethane insulation, freezer-grade gaskets, and robust latches/handles for harsh duty cycles. Many SKUs achieve bear-resistant status, reinforcing reliability in predator country. While corporate activity spans other verticals, the cooler line stays focused on extreme durability and thermal stability under abuse. Core customer sets include hunters, anglers, guides, and field technicians who equate longevity with value.

The Coleman Company, Inc. Mass-market breadth and family affordability

Overview: Coleman leverages deep outdoor heritage and Newell Brands scale to offer hard coolers, soft coolers, and electric units priced for families and casual campers.

Innovation threads include recyclable and recycled-content coolers that align with retailer sustainability scorecards. Coleman’s mission “connecting friends and families with the best of the outside” maps to practical features and dependable performance over trophy specs. A vast distribution network ensures availability across mass, hardware, and online, underpinning share in entry and mid tiers. The brand’s value + ubiquity strategy maintains category relevance through cycles.

Insulated Coolers Market Share Insights

Hard Coolers Dominate Insulated Coolers Market Share by Product Type

In 2025, hard coolers account for 40% of the insulated coolers market, reflecting their unmatched durability, ice retention, and large-volume storage capacity. They remain the preferred choice for fishing, hunting, camping, and marine activities where rugged performance and extended thermal control are essential. Premium rotomolded models, despite their higher cost, enjoy strong consumer loyalty as they offer five to seven days of ice retention, making them indispensable for outdoor enthusiasts and commercial users. Soft coolers follow with 30% share, driven by demand for portability and collapsibility, especially for day trips and urban consumers with storage constraints. Insulated bags represent the everyday, high-volume segment, sustaining demand through grocery transport, local delivery, and personal use. Meanwhile, insulated containers, though a smaller niche, serve critical roles in scientific transport and premium beverage storage where precision temperature control is non-negotiable. The segmentation highlights how hard coolers lead through performance, soft coolers grow through convenience, and insulated bags sustain mass-market volumes.

Food & Beverage Storage Leads Insulated Coolers Market Share by Application

Food and beverage storage represents 35% of the insulated coolers market in 2025, making it the single largest application. This dominance spans both consumer and commercial channels from household grocery runs and family outings to catering and food delivery services creating consistent, high-volume demand across cooler types. Outdoor recreation, including camping, hiking, and fishing, collectively drives the second-largest share, with specialized needs fueling product differentiation. For example, fishing coolers must withstand saltwater conditions and serve dual functions such as seating or storage. The medical and pharmaceutical transport segment, though smaller in unit volume, commands high value by requiring certified, temperature-validated coolers that safeguard vaccines and biologics within precise ranges (2–8°C). Other applications such as meal-kit delivery, agricultural produce logistics, and industrial processes reflect the expanding ecosystem of use cases. Together, these dynamics show how consumer lifestyle demand anchors volume, while medical and industrial applications drive value-intensive innovation.

United States: Outdoor Lifestyle Trends and Technological Innovations Driving Market Expansion

The U.S. insulated coolers market is primarily driven by evolving consumer lifestyles, with increasing participation in outdoor activities such as camping, hiking, and fishing. The demand for portable and durable cooling solutions is rising to meet recreational needs, while technological innovations are reshaping product offerings. Companies like Coleman have introduced lightweight rotomolded coolers up to 30% lighter than traditional models, enhancing portability and user convenience. Multifunctional coolers featuring built-in speakers, USB charging ports, and advanced insulation materials are increasingly popular. Sustainability is also a key driver, with manufacturers focusing on durable, long-lasting coolers and exploring energy-efficient insulation materials. Additionally, branding and customization strategies, such as YETI’s limited-edition color releases and Igloo’s co-branded Minecraft collections, are strengthening consumer engagement and expanding market reach.

Germany: Circular Economy Focus and Advanced Insulation Materials Shaping Market Development

Germany’s insulated coolers market is influenced by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) and national initiatives promoting green cooling solutions. The German government encourages energy-efficient, climate-friendly cooling systems using natural refrigerants, which is shaping product design and material selection. The country’s focus on a circular economy drives manufacturers to develop durable coolers with extended lifespans, reducing waste and promoting sustainability. Technological advancements in thermal insulation materials are enhancing performance and efficiency, aligning with the growing consumer and industrial demand for environmentally responsible cooling solutions.

China: Urbanization, Rising Temperatures, and Design Innovations Fuel Market Growth

China’s insulated coolers market is propelled by rapid urbanization and increasing temperatures, which boost demand for affordable and effective cooling solutions for both residential and commercial applications. Chinese manufacturers leverage cost-effective production capabilities while maintaining compliance with international quality standards, driving strong export potential. The market also emphasizes innovative designs and portability, with sleek, space-efficient coolers tailored for urban lifestyles with limited storage space. These trends position China as a competitive hub for affordable, functional, and visually appealing insulated coolers.

India: Outdoor Recreation and Technologically Advanced Coolers Driving Market Expansion

India’s insulated coolers industry is experiencing robust growth due to increasing interest in outdoor activities such as camping, hiking, and fishing. The market is witnessing a trend toward multifunctional coolers with features like built-in speakers, USB charging ports, and solar charging capabilities to cater to active and tech-savvy consumers. Rising disposable incomes are enabling households to invest in high-quality cooling solutions, enhancing convenience and lifestyle quality. Manufacturers are focusing on portability, durability, and affordability, ensuring products meet the evolving demands of Indian consumers in both urban and semi-urban areas.

Brazil: Eco-Friendly Refrigeration and Cold Chain Logistics Driving Market Innovation

The Brazilian insulated coolers market is influenced by the push for eco-friendly refrigeration, with initiatives from UNIDO and Brazil’s Ministry of Environment to phase out environmentally harmful refrigerants. Companies like Eletrofrio have developed chillers that reduce refrigerant use by 93%, which may influence smaller cooler designs. Growth in cold chain logistics is a major market driver, as temperature-sensitive transportation for pharmaceuticals and food products requires reliable insulated solutions. Technological advancements such as IoT-enabled coolers and remote-controlled systems are expanding product functionality and improving consumer experience, aligning with modern retail and e-commerce demands.

Japan: Cold Chain Investments and Quality-Driven Market Development

Japan’s insulated coolers market prioritizes quality and safety, adhering to strict regulations to ensure hygienic, contamination-free products. Investment in the cold chain infrastructure is a key driver, supporting temperature-sensitive goods across food, pharmaceutical, and agricultural sectors. Companies like Cold Chain Technologies are innovating with reusable pallet shippers and IoT-enabled tracking systems, improving product integrity and transport reliability. These technological advancements influence the design and features of insulated coolers, driving innovation in both consumer and industrial segments.

Insulated Coolers Market Report Scope

Insulated Coolers market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.2 Billion

|

|

Market Size (2034)

|

$1.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Hard Coolers, Soft Coolers, Insulated Bags, Insulated Containers), By Material Type (Plastic, Metal, Fabric, Other Materials), By Application (Camping & Hiking, Fishing & Marine Activities, Medical & Pharmaceutical Transport, Food & Beverage Storage, Other Applications), By Distribution Channel (Online Retail, Supermarkets & Hypermarkets, Specialty Stores, Other Channels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

YETI Holdings, Inc., The Coleman Company, Inc., Igloo Products Corp., Pelican Products, Inc., ORCA Coolers, Cooler Master Co., Ltd., Arctic Zone, Coolbox, RovR Products, Grizzly Coolers, Lifetime Products, Inc., Engel Coolers, Dometic Group AB, K2 Coolers, Thermos L.L.C.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Insulated Coolers Market Segmentation

By Product Type

- Hard Coolers

- Soft Coolers

- Insulated Bags

- Insulated Containers

By Material Type

- Plastic

- Metal

- Fabric

- Other Materials

By Application

- Camping & Hiking

- Fishing & Marine Activities

- Medical & Pharmaceutical Transport

- Food & Beverage Storage

- Other Applications

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Stores

- Other Channels

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Insulated Coolers Market

- YETI Holdings, Inc.

- The Coleman Company, Inc.

- Igloo Products Corp.

- Pelican Products, Inc.

- ORCA Coolers

- Cooler Master Co., Ltd.

- Arctic Zone

- Coolbox

- RovR Products

- Grizzly Coolers

- Lifetime Products, Inc.

- Engel Coolers

- Dometic Group AB

- K2 Coolers

- Thermos L.L.C.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global insulated coolers market, capturing breakthroughs in materials, thermal performance, and smart-enabled features that are shaping the industry landscape. Analysis reviews historical trends from 2021 to 2024 and projects market growth through 2034, highlighting strategic innovations, product differentiation, and the evolving preferences of end-users across recreational, commercial, and critical logistics applications. The study also emphasizes developments in sustainable materials, lightweight designs, and multifunctional technologies such as thermoelectric cooling, USB-powered systems, and Bluetooth connectivity, underscoring the market’s pivot toward performance, convenience, and eco-conscious solutions. This report is an essential resource for manufacturers, suppliers, investors, and supply chain stakeholders seeking insights into market drivers, competitive positioning, regulatory impact, and opportunities across premium, mid-tier, and value segments. USDAnalytics delivers an in-depth perspective on competitive strategies, geographic expansion, and technological trends that define market leadership and future adoption pathways.

Scope Highlights

- Segmentation: By Product Type (Hard Coolers, Soft Coolers, Insulated Bags, Insulated Containers), By Material Type (Plastic, Metal, Fabric, Other Materials), By Application (Camping & Hiking, Fishing & Marine Activities, Medical & Pharmaceutical Transport, Food & Beverage Storage, Other Applications), By Distribution Channel (Online Retail, Supermarkets & Hypermarkets, Specialty Stores, Other Channels).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Temporal Coverage: Historical data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Analysis: Profiles and strategic insights of 15+ key players, including YETI Holdings, The Coleman Company, Igloo Products, Pelican Products, and other global leaders.

Methodology

The research methodology underpinning this report combines both qualitative and quantitative approaches to ensure robust and actionable insights. USDAnalytics leveraged primary data collection through interviews with industry executives, product managers, and distributors, supplemented by secondary sources including company filings, government regulations, trade publications, and sustainability reports. Market sizing and forecasts were developed using a bottom-up approach for each product, material, application, and distribution channel segment, incorporating historical trends, growth drivers, and macroeconomic factors. Competitive benchmarking was performed through the analysis of product portfolios, patents, R&D expenditure, and distribution networks. Scenario analysis and sensitivity testing were applied to model potential disruptions in supply chain, materials, and regulatory frameworks. This systematic methodology ensures accurate projections, highlights emerging opportunities, and delivers a granular understanding of market dynamics tailored to the strategic needs of industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.