Market Overview: Ready-to-Use IV Containers, Smart Packaging, and Eco-Design Reshape Sterile Delivery

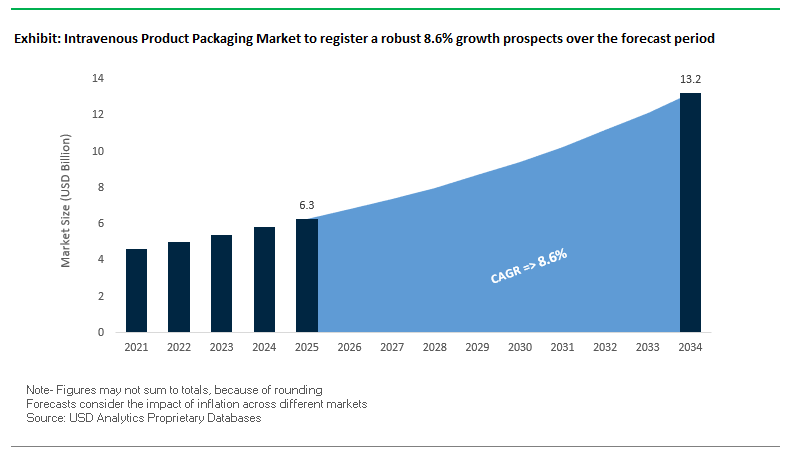

The Intravenous (IV) Product Packaging Market is valued at USD 6.3 billion in 2025 and is forecast to reach USD 13.2 billion by 2034, registering a robust CAGR of 8.6%. For procurement and device leaders, the core question is how to combine sterility assurance, regulatory compliance, and user safety with sustainable, cost-efficient formats across vials, IV bags, cartridges, and prefilled syringes. Growth is propelled by the shift to ready-to-use (RTU) formats that minimize medication errors, digital features that authenticate and track products, and material innovations that stabilize biologics and high-viscosity drugs while advancing ESG goals.

Key insights for Industry Buyers and Professionals

- Growth vector: USD 6.3B (2025) → USD 13.2B (2034) at 8.6% CAGR led by prefilled syringes, IV bags, and RTU components.

- Patient-safety premium: RTU vials/syringes/IV bags reduce compounding steps and lower error risk in clinical and home settings.

- Sustainability shift: Momentum toward lightweight, single-material polymers and recyclable IV containers aligns with ESG mandates.

- Digital traceability: QR, RFID, NFC enable end-to-end visibility, anti-counterfeiting, and recall readiness for injectables.

- Biologics-ready design: Advanced coatings, borosilicate glass, and container/closure systems preserve stability for complex, high-viscosity formulations.

Market Analysis: Recent Developments Smart, Sustainable, and Patient-Centric (dated for recency clarity)

The competitive playbook is consolidating around localization of critical components, active packaging, and connected drug delivery. In August 2025, SCHOTT launched a new syringe/cartridge glass-tubing line in India, expanding regional access to Type I borosilicate for surging injectable demand. Also in August 2025, DNP showcased mono-material, recyclable sterile-packaging concepts at Medical Fair Thailand, reinforcing the pivot to circular healthcare materials, while Aptar CSP announced N-Sorb technology to reduce nitrosamines, ahead of regulatory deadlines spotlighting active packaging as a quality safeguard.

Digitization continues to move from pilot to platform. A July 2025 report highlighted accelerating adoption of smart packaging (QR/NFC/RFID) for IV and injectable workflows, enabling item-level authentication and cold-chain telemetry. Materials policies are also tightening: June 2025 analysis underscored mono-material adoption for better recyclability. In May 2025, Gerresheimer and partner reported tentative FDA approval for an on-body drug delivery device with a micropump for controlled at-home dosing evidence that connected, wearable infusion is entering mainstream care.

Commercial momentum remains firm. March 2025, B. Braun reported €9.1B FY2024 sales and continued investments in digital and modern technologies. February 2025, Baxter launched five new injectables (US), including ready-to-use anti-infectives. Cold-chain scale-ups support bulk movements: October 2024, Pelican BioThermal unveiled Crēdo Vault™ for pharma bulk shipments, lowering weight and environmental impact. And in August 2024, Aptar CSP received an IndiaStar Award, reflecting the region’s strategic relevance for innovative, compliance-ready packaging.

Emerging Trends and Opportunities Shaping the Intravenous Product Packaging Market

Accelerated Adoption of Ready-to-Use (RTU) Vials and Prefilled Syringes

The intravenous product packaging market is witnessing a strong shift toward Ready-to-Use (RTU) vials and prefilled syringes, driven primarily by the critical need to minimize medication errors. Prefilled syringes offer exact dosing at the manufacturing stage, effectively eliminating human errors during manual dose preparation in hospitals and clinical settings. This accuracy is especially vital for high-value and sensitive drugs, where even minor deviations can lead to serious clinical consequences. Beyond safety, RTU packaging significantly enhances hospital workflow and operational efficiency. Healthcare professionals save valuable time by avoiding manual preparation, which is particularly beneficial in high-pressure environments such as emergency rooms and operating theaters. For instance, Amneal Pharmaceuticals’ July 2024 FDA approval of its potassium phosphates IV solution in a ready-to-use bag underscored the product’s design focus on both safety and efficiency in hospital operations. Additionally, the rise of home healthcare has propelled the adoption of prefilled syringes, simplifying self-administration for patients with chronic conditions. This convenience not only promotes adherence to prescribed therapies but also reduces treatment gaps, further cementing RTU packaging as a key Market Trend.

Integration of Advanced Polymer Films for Flexible IV Bags with Enhanced Barrier Properties

Pharmaceutical manufacturers are increasingly leveraging advanced polymer films to enhance the barrier properties of flexible IV bags, a trend propelled by the need to protect high-value, sensitive drug formulations such as biologics and parenteral nutrition. These multi-layer films provide superior protection against moisture, oxygen, and light, extending product shelf life while ensuring drug integrity. Polycine, for instance, offers specialty films designed for optimal moisture, light, and gas barrier performance, highlighting the technological advances in this segment. Another critical advantage of these films is the potential to reduce cold chain dependency. By stabilizing drugs at room temperature, manufacturers can minimize the logistical complexity and costs associated with temperature-controlled supply chains. Innovations are particularly evident in multi-chamber IV bags, where drugs must remain separate until point-of-use. The multi-chamber and specialty bags segment is poised for robust growth between 2025 and 2034, reflecting rising demand for versatile packaging solutions for complex intravenous formulations.

Development of In-Line Sensor Technology for Real-Time Integrity Testing

The intravenous product packaging industry is moving toward deterministic, non-destructive, in-line integrity testing, replacing traditional probabilistic approaches like the blue dye test. This opportunity emphasizes ensuring 100% quality control by enabling the inspection of every vial or IV bag on the production line. Modern sensor technologies, such as vacuum decay systems, are recognized by the FDA as standards for detecting even microscopic defects or pinholes that could compromise sterility. According to guidance from the U.S. Pharmacopeia (USP), validated container-closure systems are critical, and integrating real-time sensors ensures compliance while maintaining product safety. Emerging systems are designed to handle the increasing complexity of packaging formats, including flexible IV bags with intricate seals and port regions, which are vulnerable during manufacturing and transit. This innovation represents a significant leap in quality assurance and regulatory compliance in IV product packaging.

Standardization of Connected Packaging for Smart Inventory Management

Connected packaging presents a substantial opportunity to enhance hospital efficiency, reduce wastage, and improve patient safety. By embedding RFID or NFC tags directly into IV bags and vials, hospitals can automate drug inventory management, enabling real-time tracking from pharmacy storage to the patient’s bedside. This technology reduces manual inventory checks and mitigates drug wastage caused by expiration, translating into both financial savings and improved patient safety. For example, collaborations between pharmaceutical services companies and smart packaging providers have resulted in systems that automatically track expiration dates of IV products, ensuring timely use and minimizing risk. Additionally, RFID-enabled IV syringes, such as those launched by GENIXUS Corp. in August 2023, demonstrate the dual benefit of operational efficiency and patient safety by reducing medication errors while optimizing hospital workflow. Connected packaging is therefore emerging as a critical growth opportunity for stakeholders aiming to integrate smart, traceable, and safer intravenous drug delivery systems.

Competitive Landscape: Leaders in Glass, Polymers, Active Packaging, and Drug-Device Integration

A handful of global specialists are scaling cleanroom capacity, primary containment excellence, and connected delivery systems. The winning play is an ecosystem approach: container/closure + active materials + digital ID + device.

B. Braun Melsungen AG: Vertically integrated IV systems with digital upgrades

B. Braun combines IV bags/containers, infusion pumps, and services to deliver end-to-end infusion therapy. In 2024, it reported €9.1B sales and stepped up AI/data-driven solutions. Its Ecoflac® Plus and Ecobag® portfolios emphasize safety, usability, and lower environmental impact, while the company advances additive manufacturing and digital hospital workflows. Strategy: “B. Braun the next decade,” integrating sustainability, informatics, and device-packaging convergence to raise therapy quality and operational efficiency.

Baxter International Inc.: RTU injectables and global platform scale

Baxter’s strength spans Viaflex® IV bags, infusion systems (Sigma Spectrum), and sterile solutions. In February 2025, it launched five new US injectables, including ready-to-use anti-infective formulations, supporting hospital throughput and safety. Its strategic roadmap streamlines the portfolio (including planned separations) to focus on high-growth medication delivery segments. Baxter’s priority is operational excellence + innovation to ensure reliable supply and error-reducing RTU formats.

SCHOTT AG: Regionalized borosilicate capacity for surging biologics

SCHOTT anchors Type I borosilicate expertise (e.g., FIOLAX®) for vials, syringes, and cartridges, optimizing chemical resistance and dimensional precision. In August 2025, it invested in Indian production for syringe/cartridge tubing supporting regional supply security and biologics (e.g., GLP-1s/high-viscosity) growth. Strategy: expand global glass-tubing capacity and partner with pharma to ensure sterility, machinability, and long-term stability of sensitive injectables.

AptarGroup Inc.: Active packaging and patient-centric drug delivery

Aptar provides vial/syringe components, containment systems, and connected health devices. In August 2025, Aptar CSP introduced N-Sorb to mitigate nitrosamines, illustrating leadership in Active Material Science (moisture/oxygen control). With an IndiaStar 2024 recognition, Aptar advances digital health and connected packaging to improve adherence, pairing component performance with data-enabled user experience.

Gerresheimer AG: Primary packaging plus on-body delivery innovation

Gerresheimer spans glass/plastic primary containers (e.g., Gx RTF vials) and drug-device systems (pen and auto-injectors). In 2024, it earned a Red Dot for the Gx Inbeneo® autoinjector, designed for high-viscosity biologics, and in May 2025 its on-body micropump platform obtained tentative FDA approval for home-use dosing. Strategy: fuse sustainable primary packaging with connected delivery, targeting 50% CO₂ reduction by 2030 and better patient adherence via smart features.

Intravenous Product Packaging Market Share Insights

IV Bags Hold the Largest Market Share by Product Type in Intravenous Packaging

IV bags represent 50% of the intravenous product packaging market in 2025, solidifying their position as the standard container for large-volume parenteral solutions. Their widespread adoption is driven by advantages over glass bottles, including reduced weight, safer handling, ease of disposal, and improved storage efficiency. IV bags are used extensively for saline, dextrose, electrolyte solutions, and drug infusion therapies, making them indispensable in modern hospitals. The transition to non-PVC and DEHP-free materials reflects regulatory and safety-driven innovation, ensuring long-term relevance. Vials and syringes remain critical, with vials supporting long-term stability for biologics and vaccines, and syringes especially prefilled formats gaining traction for precision dosing and patient safety. Bottles, once the standard, now occupy a declining niche, while ampoules and other specialized containers cater to emerging drug delivery needs. This segmentation reflects how IV bags dominate by volume, while vials and syringes anchor high-value pharmaceutical packaging applications.

Hospitals Dominate Market Share by Application in Intravenous Product Packaging

Hospitals account for 70% of the intravenous packaging market in 2025, reflecting their central role in global healthcare delivery. They perform the bulk of surgeries, emergency treatments, inpatient therapies, and intensive care interventions, all of which require high volumes of IV fluids, antibiotics, anesthetics, and nutritional solutions. This dominance is reinforced by hospitals’ scale, where procurement strategies demand bulk, reliable, and cost-effective IV packaging formats. Ambulatory surgical centers (ASCs) represent a fast-growing segment, reflecting the healthcare industry’s shift toward outpatient surgeries and cost reduction, with significant demand for vials, IV bags, and prefilled syringes in high-throughput environments. Homecare is another rapidly expanding application, fueled by aging populations and chronic disease management, where user-friendly, safe, and portable IV packaging formats enable treatment outside hospitals. Clinics and smaller healthcare centers remain minor consumers, with usage focused on immunizations and limited outpatient therapies. This segmentation illustrates how hospitals anchor volume consumption, while ASCs and homecare drive diversification in IV packaging demand.

United States: Regulatory Pressure and Innovation Driving IV Packaging Growth

The United States intravenous product packaging market is strongly influenced by the Food and Drug Administration (FDA) and the Drug Supply Chain Security Act (DSCSA), which mandates unique identifiers, RFID tags, and 2D barcodes to secure the supply chain. These regulations are accelerating the adoption of track-and-trace IV packaging technologies to ensure both patient safety and product integrity. Hospitals, clinics, and home healthcare providers represent the largest demand base, particularly for IV bags, pre-filled syringes, and cannulas.

Technological innovation is reshaping the market, with companies like West Pharmaceutical Services launching sterile, high-performance IV containers in February 2024, designed for both safety and workflow efficiency. Corporate investment also plays a pivotal role, as Becton, Dickinson and Company (BD) introduced an IV packaging system with tamper-evident and recyclable features in 2022, while ICU Medical’s acquisition of Smiths Medical in 2021 expanded its IV therapy portfolio. The U.S. market is also seeing strong momentum in eco-friendly IV packaging, where antimicrobial and recyclable materials are being prioritized for sustainable healthcare operations.

Germany: Circular Economy Compliance and Advanced IV Packaging Solutions

The German intravenous product packaging market operates under a rigorous regulatory environment shaped by the EU Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be fully recyclable or reusable by 2030. This has pushed German companies to adopt sustainable materials like polyolefin for IV solutions while adhering to the broader goals of the German Packaging Act (VerpackG), which incentivizes design-for-recycling practices.

Germany is also a hub of technological innovation in infusion therapy and IV packaging, led by companies such as B. Braun Melsungen AG, which specializes in advanced infusion solutions. Similarly, Gerresheimer AG is investing heavily in vials, ampoules, and next-generation packaging formats to address both regulatory compliance and hospital demand. Germany’s leadership in the circular economy has positioned its IV product packaging industry as a model for integrating sustainability with pharmaceutical-grade safety and performance.

China: Dual-Carbon Strategy and Domestic Expansion in IV Packaging

The China IV product packaging market is closely tied to the government’s “dual carbon” goal, which is driving greener production processes and sustainable material adoption across healthcare packaging. The March 2024 “Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement” is designed to promote recycling and eco-friendly medical packaging. Additionally, the updated GB/T 31268 standard on restricting excessive packaging (effective November 2024) directly impacts IV packaging by limiting wasteful material use.

China is rapidly integrating automation, AI, and 5G-enabled smart factories to increase IV packaging efficiency. Domestic manufacturers like SSY Group Limited and Forlong Medical Co., Ltd. are scaling up operations to replace imported technologies with locally manufactured high-performance IV packaging. With rising demand in hospitals and expanding government initiatives, the Chinese market is expected to lead in AI-driven production and sustainable medical packaging solutions over the next decade.

India: Government Incentives and Rising Demand for Sustainable IV Packaging

The India intravenous product packaging market is advancing under the government’s Production Linked Incentive (PLI) scheme for Pharmaceuticals and Medical Devices, which promotes domestic manufacturing and sustainable innovation. India’s commitment to a circular economy has increased opportunities for companies offering eco-friendly IV packaging solutions. Regulatory oversight by the Central Drugs Standards Control Organisation (CDSCO) enforces high safety standards, compelling manufacturers to supply hygienic and compliant packaging.

Technological advancement is also evident, as demonstrated by Gufic Biosciences’ June 2022 launch of dual-chamber IV bags that allow safe and efficient drug delivery. Investment in new production facilities is expanding, driven by the country’s fast-growing pharmaceutical exports and healthcare infrastructure. Rising demand from both hospitals and home healthcare has positioned India as one of the fastest-growing IV packaging markets in Asia-Pacific, with sustainability and compliance as its cornerstones.

Japan: Precision Manufacturing and High-Performance IV Packaging Innovations

The Japan IV product packaging market benefits from the country’s strengths in precision engineering and advanced material science. Companies like Nipro and Otsuka Pharmaceutical Co., Ltd. are leading with next-generation medical devices and packaging formats that emphasize both safety and efficiency. Japan’s Plastic Resource Circulation Act (April 2022) has further guided manufacturers toward eco-friendly packaging designs, reducing reliance on single-use plastics.

Japanese companies are also prioritizing functional innovation, developing IV packaging with self-sealing, tamper-proof, and advanced barrier properties to meet specialized medical needs. With strong support from the Ministry of Economy, Trade, and Industry (METI), Japan continues to push for sustainable, high-performance IV product packaging that meets the needs of both hospitals and advanced home healthcare services.

Brazil: Sustainable Waste Management and Expanding IV Packaging Applications

The Brazil intravenous product packaging market is underpinned by the National Solid Waste Policy (PNRS), updated in April 2022, which aims to modernize solid waste management and promote sustainability over the next two decades. These initiatives are directly influencing material choices in the IV packaging industry, encouraging eco-friendly and recyclable solutions.

The market is particularly strong in hospital and clinical sectors, where there is a rising demand for ready-to-use IV packaging and high-value pharmaceutical applications. Technological advancement in cold chain logistics and last-mile delivery is also enabling safer distribution of IV products across Brazil’s vast geography. Moreover, the EU-Mercosur trade agreement is expected to expand investment and diversify packaging solutions, attracting both domestic and international manufacturers to the Brazilian healthcare packaging market.

Intravenous Product Packaging Market Report Scope

Intravenous Product Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.3 Billion

|

|

Market Size (2034)

|

$13.2 Billion

|

|

Market Growth Rate

|

8.6%

|

|

Segments

|

By Product Type (IV Bags, Bottles, Vials, Syringes, Others), By Material (PVC, Non-PVC, Glass, Others), By Packaging Type (Single-Chamber Bags, Multi-Chamber Bags, Dual-Chamber Bags), By Application (Hospitals, Clinics, ASCs, Homecare, Other Healthcare Centers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Baxter International Inc., B. Braun Melsungen AG, ICU Medical, Inc., Fresenius Kabi AG, Terumo Medical Corporation, Otsuka Pharmaceutical Co., Ltd., Grifols, S.A., West Pharmaceutical Services, Inc., Nipro Corporation, Amcor plc, SGD Pharma, Gerresheimer AG, Becton, Dickinson and Company (BD), Technoflex, PolyCine GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Intravenous Product Packaging Market Segmentation

By Product Type

- IV Bags

- Bottles

- Vials

- Syringes

- Others

By Material

By Packaging Type

- Single-Chamber Bags

- Multi-Chamber Bags

- Dual-Chamber Bags

By Application

- Hospitals

- Clinics

- ASCs

- Homecare

- Other Healthcare Centers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Intravenous Product Packaging Market

- Baxter International Inc.

- B. Braun Melsungen AG

- ICU Medical, Inc.

- Fresenius Kabi AG

- Terumo Medical Corporation

- Otsuka Pharmaceutical Co., Ltd.

- Grifols, S.A.

- West Pharmaceutical Services, Inc.

- Nipro Corporation

- Amcor plc

- SGD Pharma

- Gerresheimer AG

- Becton, Dickinson and Company (BD)

- Technoflex

- PolyCine GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-source research methodology to deliver a comprehensive analysis of the global Intravenous (IV) Product Packaging Market. Our approach combined both primary and secondary research, with primary insights gathered through consultations with senior executives, procurement heads, R&D managers, and regulatory affairs specialists across hospitals, clinics, and pharmaceutical manufacturing facilities. Secondary research included extensive review of industry reports, regulatory frameworks (FDA, EU PPWR, CDSCO), corporate filings, press releases, and scientific publications related to IV packaging materials, smart packaging, and ready-to-use delivery systems. Quantitative modeling and market forecasting were performed using bottom-up and top-down approaches, factoring in product types, material innovations, geographical trends, adoption of digital and connected packaging solutions, and regulatory influences. USDAnalytics applied cross-validation techniques to ensure accuracy of CAGR projections, market sizing, and segment growth estimates. Trends in RTU vials, prefilled syringes, advanced polymer films, in-line sensor technology, and connected packaging solutions were carefully analyzed for technological and commercial feasibility. Competitive benchmarking assessed market positioning of leading players such as B. Braun, Baxter, Gerresheimer, and SCHOTT, integrating insights from mergers, acquisitions, capacity expansions, and product innovation. Regional market analysis for the U.S., Germany, China, India, Japan, and Brazil incorporated country-specific regulatory, sustainability, and technological dynamics. This methodology ensures that stakeholders receive actionable, data-driven intelligence to guide investment, procurement, and strategic decisions in the evolving IV product packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.