Market Overview: Smart, Sustainable, and High-Performance Cold Chain Solutions

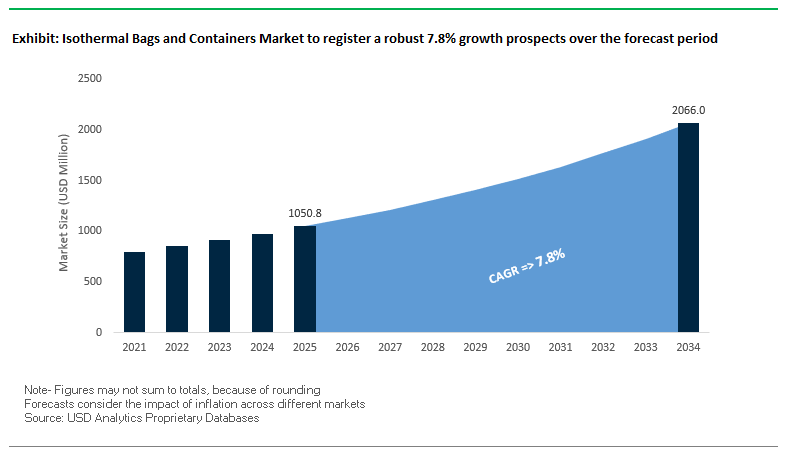

The Isothermal Bags and Containers Market is projected at USD 1050.8 million in 2025 and expected to reach USD 2065.8 million by 2034, growing at a CAGR of 7.8%. This segment plays a critical role in modern cold chain logistics, ensuring that temperature-sensitive products including pharmaceuticals, vaccines, fresh food, and biologics arrive intact and compliant with regulatory standards. For buyers and industry professionals, the key questions are: How to balance thermal efficiency, sustainability, and cost optimization while meeting diverse sectoral needs?

Key Insights for Industry Professionals

- Market growth trajectory: USD 1050.8M (2025) → USD 2065.8M (2034) at 7.8% CAGR, driven by healthcare, food delivery, and biologics.

- E-commerce driver: Surging demand for last-mile delivery insulation for meal kits, groceries, and ready-to-eat solutions.

- Sustainability transition: Shift away from EPS foam toward biodegradable liners, reusable bags, and recyclable fiber-based designs.

- Healthcare resilience: Biologics, vaccines, and specialty drugs fueling validated high-performance insulated packaging.

- Digital edge: Adoption of smart packaging (sensors, data loggers, RFID/QR) for compliance and shipment traceability.

Market Analysis: Recent Developments in Isothermal Packaging

The Global Isothermal Bags and Containers Industry is consolidating around eco-design, smart tracking, and cold chain validation. In August 2025, DNP showcased mono-material, recyclable packaging at Medical Fair Thailand, expanding sustainable solutions for pharmaceuticals. Just a month earlier, in July 2025, a report highlighted the uptake of smart packaging (QR, NFC, RFID), underscoring the market’s pivot toward traceable and interactive cold chain solutions.

On the materials front, innovations are accelerating. A June 2025 report outlined improvements in paper-based production efficiency, reducing cost while maintaining insulation. In May 2025, ProAmpac introduced FiberCool, a patent-pending insulated curbside bag with improved insulation and reduced material waste. This innovation reflects the dual demand for thermal efficiency and recyclability. Similarly, April 2025 analysis flagged the role of digital printing in customizing labels for short runs and regulatory compliance enhancing both branding and safety.

Strategic shifts are evident among global packaging leaders. In February 2025, Amcor launched its AmFiber Performance Paper pouch, cutting carbon footprint by 73% compared to standard packs. Reports from December 2024 emphasized industry-wide movement toward mono-material adoption. Cold-chain innovation is visible too: October 2024, Pelican BioThermal unveiled Crēdo Vault™ for bulk pharma shipments, integrating efficiency with compliance. In September 2024, Shiseido adopted kraft honeycomb wrap, illustrating the wider retail shift toward recyclable protective packaging.

Trends and Opportunities Reshaping the Isothermal Bags and Containers Market

Integration of Phase Change Materials (PCMs) for Precision Temperature Control

A major shift is taking place from passive insulation toward engineered Phase Change Materials (PCMs) that maintain precise and consistent temperature ranges. These materials are especially critical for pharmaceuticals, specialty foods, and diagnostic samples, where even minor fluctuations can compromise integrity.

A scientific study published by RSC Publishing highlighted a shape-stabilized PCM composite with a melting point between 0°C and 10°C that sustained stability over 500 heating and cooling cycles, demonstrating its potential for long-term cold chain applications. Companies like Pelton Shepherd Industries emphasize PCMs’ unique ability to absorb heat during warmer conditions and release it when temperatures drop, ensuring reliable buffering against environmental extremes.

The benefits extend directly to product safety and cost reduction. For example, FedEx’s Cold Shipping Package can maintain temperatures between 2°C and 8°C for up to 96 hours, offering a cost-effective alternative to gel packs and dry ice. Moreover, PCMs can be customized organic, inorganic, or eutectic making them adaptable for refrigerated, frozen, and ultra-cold logistics. By minimizing spoilage, reducing reliance on traditional refrigerants, and enhancing operational flexibility, PCMs are becoming a cornerstone technology for next-generation isothermal packaging solutions.

Corporate Sustainability Mandates Driving Adoption of Recyclable and Bio-Based Materials

The push for eco-friendly isothermal packaging is accelerating as multinational corporations set ambitious sustainability targets. Nestlé, for instance, aims to make 95% of its packaging recyclable, reusable, or compostable by 2025, and reported a 14.9% cut in virgin plastic use between 2018 and 2024. Unilever and UPS are also advancing commitments to reduce single-use plastic waste, directly pressuring packaging providers to innovate.

Material science companies are responding with curbside recyclable and bio-based alternatives. Ranpak’s RecyCold® climaliner™, a recyclable paper-based liner, eliminates the use of plastics or harmful chemicals. Similarly, Cruz Foam has introduced compostable foam derived from agricultural waste, designed as a “drop-in-place” solution that integrates seamlessly into existing production systems.

Logistics leaders are embedding sustainability into their supply chains as well. UPS has highlighted circular economy programs such as its coffee pod recycling partnership with Nespresso to reduce waste and increase closed-loop systems. These developments mark a paradigm shift from single-use foams and plastics toward scalable, renewable solutions, aligning with consumer preferences for biodegradable, recyclable, and circular packaging formats in the cold chain sector.

Development of Reusable Packaging Pooling Systems for Urban Delivery

The surge in e-commerce grocery and meal kit delivery in urban areas is unlocking a significant opportunity for reusable insulated container pooling systems. Instead of relying on single-use bags, logistics providers are shifting toward durable containers designed for hundreds of reuse cycles, creating both cost savings and new service-based business models.

Manufacturers like Tempack are producing robust polyurethane-based systems that transform ordinary vehicles into multi-temperature delivery fleets, enhancing efficiency. Similarly, Thermo Future Box offers reusable expanded polypropylene (EPP) containers that are dishwasher-safe, withstand -40°C to +120°C, and last three to five years, making them suitable for professional reuse.

Beyond durability, the model delivers logistical efficiency and waste reduction. IPC has highlighted the cost-saving benefits of compact, stackable insulated solutions, which further improve warehouse storage and transportation efficiency. For providers, the biggest transformation is shifting from a transactional packaging sales model to recurring service revenue, with companies like Tempack emphasizing modular designs adaptable for long-term pooling systems. This opportunity positions reusable containers as both a sustainability solution and a cost-optimization strategy for high-volume urban delivery.

Product Innovation for At-Home Diagnostic and Biometric Sample Collection

The rapid rise of direct-to-consumer healthcare including at-home diagnostic kits, genetic testing, and biometric sample collection has created a strong demand for small-format, user-friendly, and certified isothermal mailers that protect sample integrity during transport.

Healthcare packaging providers such as Sodibox are developing solutions that comply with ADR P650 regulations for Category B biological substances, ensuring safety and regulatory compliance. Their lightweight, easy-to-close designs are specifically engineered for consumer usability. Likewise, ELITE BAGS and similar manufacturers are offering compact, compartmentalized insulated bags tailored to carry multiple sample types securely.

This innovation is supported by the growing adoption of telemedicine and home diagnostics, which A.G. Diagnostics notes is particularly beneficial for elderly patients and those with limited mobility. By providing reliable thermal protection for samples, isothermal containers safeguard diagnostic accuracy while expanding healthcare accessibility. With the market moving toward consumer-facing healthcare models, insulated packaging companies are well-positioned to capture value through specialized, certified, and patient-friendly designs for home-based medical applications.

Competitive Landscape: Leaders in Isothermal Bags and Containers

The market is shaped by companies focusing on thermal validation, sustainable materials, and scalable logistics. These firms are building resilience in food, healthcare, and life sciences cold chains.

Sonoco Products Company: Expanding protective and cold-chain portfolios

Sonoco leverages materials science and cleanroom-certified designs to serve healthcare and food sectors. In July 2025, it announced a USD 30M investment in adhesives and sealants capacity and in April 2025, it sold thermoformed/flexibles to Toppan, sharpening focus on core businesses. Its insulated shippers and temperature-controlled containers ensure compliance for sensitive products. Strategic priority: refining portfolios while scaling sustainable temperature-assurance solutions.

Pelican BioThermal: Bulk pharma-ready reusable solutions

Pelican BioThermal dominates life sciences cold chain with validated reusable designs. In October 2024, it launched Crēdo Vault™ for bulk pharma shipments, and since 2020, it has scaled frozen shipping for COVID-19 vaccines. With Crēdo™ and CoolGuard™ lines, Pelican delivers durability and extended performance. Strategic direction: reducing emissions and reinforcing validated reusable systems for pharma and biotech.

Sealed Air Corporation: Sustainable insulation innovation

Sealed Air builds on foam/air-filled expertise with new materials. In May 2024, it launched Cryovac ICETech, a sustainable insulation material that reduces emissions and waste. Its Instapak® PUR foams and TempGuard® insulated bags offer 72-hour protection, supporting just-in-time food logistics. Strategy: enabling a waste-minimized global food chain, while integrating smart, digital-ready packaging (prismiq™ brand, 2022).

TemperPack Technologies, Inc.: Curbside recyclable insulation disruptor

TemperPack champions EPS replacement with its curbside recyclable insulation. Following its September 2022 acquisition of KTM Industries (Green Cell Foam), it has expanded starch-based alternatives. January 2024 commentary from its CEO reinforced the vision of an e-commerce world free from styrofoam. Flagship lines ClimaCell™ and WaveKraft™ deliver paper-based liners with certified recyclability. Strategy: scaling eco-friendly cold chain packaging to meet consumer ESG preferences.

DS Smith Plc: Circular corrugated insulated packaging

DS Smith extends its corrugated and paper-based innovation into insulated formats. Its box-to-box recycling model closes the loop in two weeks, reducing virgin fiber use. Recent research highlights its efforts to replace plastics in e-commerce packaging, particularly in apparel and food. By providing collapsible, space-saving insulated designs, DS Smith positions itself as a fiber-based alternative provider, aligning with circular economy standards. Strategy: innovate through paper-based alternatives that replace hard-to-recycle plastics.

Isothermal Bags and Containers Market Share Insights

Soft Bags Dominate Market Share by Product Type in Isothermal Bags and Containers

Soft bags account for nearly two-thirds of the isothermal bags and containers market in 2025, underlining their position as the most widely adopted packaging format. Their dominance is attributed to flexibility, lightweight handling, and cost-effectiveness, making them the preferred solution for last-mile delivery and e-commerce fulfillment. Soft bags not only reduce shipping costs and storage space when not in use but also meet the operational needs of meal kit providers, online grocery platforms, and pharmaceutical distributors seeking scalable and consumer-friendly thermal packaging. By contrast, hard containers continue to play a specialized role in high-value, high-risk shipments such as biologics, vaccines, premium food delivery, and industrial samples. Their rigidity provides longer thermal retention and crush resistance, which justifies their higher cost in applications where uncompromised product integrity is critical. This segmentation highlights how soft bags dominate through volume and efficiency, while hard containers remain indispensable in regulated and premium logistics channels.

Last-Mile Delivery Leads Market Share by Application in Isothermal Bags and Containers

Last-mile delivery commands the largest share of the isothermal packaging market in 2025, reflecting its central role in the modern delivery economy. With on-demand food delivery services, meal kit subscriptions, and pharmaceutical home delivery booming worldwide, maintaining temperature stability in the final leg of logistics has become non-negotiable. Soft isothermal bags are the workhorse of this segment, offering portability, scalability, and reliable performance for perishable products. E-commerce further reinforces this dominance, as the surge in online grocery shopping and specialty food shipping continues to elevate the need for dependable insulated packaging. Commercial and household users add steady volume, with restaurants, caterers, and consumers utilizing these solutions for safe food transport and personal use. Meanwhile, the industrial segment, although smaller, is highly specification-driven, requiring validated hard containers to transport sensitive samples, chemicals, and electronics. This breakdown emphasizes that last-mile delivery drives the bulk of market demand, while e-commerce and industrial niches push innovation in design and performance requirements.

United States Isothermal Bags and Containers Market Driven by Regulatory Compliance and Smart Packaging Innovations

The U.S. isothermal bags and containers market is strongly influenced by a fragmented regulatory environment at both state and federal levels. Regulations from the FDA and DOT ensure the safety and integrity of perishable goods during transit, while the Drug Supply Chain Security Act (DSCSA) mandates unique identifiers on pharmaceutical packaging, boosting demand for smart packaging solutions with real-time tracking capabilities.

Technological advancements are reshaping the industry, including eco-friendly, reusable insulated packaging solutions, such as those launched by The Packaging Company in March 2024. The growing adoption of IoT-enabled smart packaging for real-time temperature monitoring addresses critical concerns in the transportation of pharmaceuticals and perishable foods. Corporate investments are expanding sustainable production, with Cold Chain Technologies upgrading its isothermal product lines in September 2022 to include improved insulation and eco-friendly materials. Key applications remain concentrated in e-commerce, pharmaceuticals, and food delivery, where the “Amazon Effect” has increased consumer expectations for fresh, high-quality, and temperature-controlled goods.

Germany Isothermal Packaging Market Accelerates Through Circular Economy and Industry 4.0 Integration

Germany’s isothermal bags and containers market is governed by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This mandates that all packaging be fully recyclable or reusable by 2030, driving adoption of sustainable solutions. The Single-Use Plastics levy further incentivizes reusable or recyclable isothermal containers to reduce compliance costs.

Technological innovation is a key focus, supported by Germany’s Industry 4.0 initiatives, which integrate digital manufacturing technologies to enhance efficiency and sustainability. Leading companies such as Pelican BioThermal are driving high-performance solutions in the market. The Packaging Act (VerpackG) encourages designs optimized for recycling through modulated fees, favoring reusable over single-use containers. Corporate investments from domestic and international players continue to expand product portfolios to meet growing demand for eco-friendly, high-performance isothermal packaging solutions.

China Isothermal Packaging Market Expanding with Green Policies and Advanced Automation

China’s government initiatives supporting the “dual carbon” goal are catalyzing a green transformation in the isothermal packaging industry. The March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages the use of sustainable materials and recycling practices. Regulatory reforms, including GB/T 31268 effective November 2024, target excessive packaging in e-commerce, a key channel for isothermal products.

Technological advancements such as AI and “5G plus industrial internet” integration optimize production efficiency and flexible capacity. Companies like Greif have implemented real-time tracking technology, GCube Connect, to enhance performance and visibility in the supply chain. The trend toward domestic manufacturing is prominent, with local firms investing in advanced insulation materials and circular packaging solutions to meet the surging domestic demand.

India Isothermal Packaging Market Gaining Traction from Circular Economy Policies and Cold Chain Expansion

India’s government initiatives are promoting a circular economy, creating growth opportunities in the isothermal packaging market. Programs such as the Pradhan Mantri Kisan Sampada Yojana (PMKSY), with INR 4600 Cr allocated until March 2026, aim to build integrated cold chain infrastructure, supporting the need for advanced insulated packaging from farm to consumer.

Technological advancements include the adoption of advanced materials and development of specialized products, supported by Production Linked Incentive (PLI) schemes for pharmaceuticals and medical devices. Corporate investments are increasing to meet demand from India’s expanding food processing and cold chain sectors. The country’s rising exports of pharmaceuticals and perishable goods further drive the need for high-performance isothermal packaging that meets global safety and quality standards.

Japan Isothermal Bags and Containers Market Leading in Advanced Materials and High-Performance Packaging

Japan’s isothermal packaging market benefits from the country’s leadership in precision manufacturing and next-generation production ecosystems. Innovation is focused on vacuum-insulated panels (VIPs) and paper-based thermal wraps, gaining traction in Asia and Europe for their thermal performance and sustainability benefits.

Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes “Design for the Environment” and reduction of single-use plastics. Major players are pivoting toward specialty and value-added products with superior functional properties, such as self-sealing packaging and enhanced barrier performance. The emphasis on high-performance and aesthetically robust solutions supports the industry’s growth across pharmaceuticals, food, and temperature-sensitive logistics sectors.

Brazil Isothermal Packaging Market Accelerating with Sustainable Practices and Last-Mile Delivery Innovation

Brazil’s isothermal bags and containers market is shaped by the National Solid Waste Policy, amended in April 2022, which promotes sustainable waste management and recycling practices. The EU-Mercosur trade agreement is expected to further enhance market diversification and attract investment.

Technological innovation is evident in the food delivery sector, with retailers implementing shuttle systems that integrate frozen, chilled, and ambient items into insulated totes for improved last-mile delivery. The market sees strong demand in frozen foods, fresh produce, and ready-to-eat meals, while domestic and international corporate investments continue to expand high-performance and eco-friendly packaging solutions to meet logistical and regulatory requirements.

Isothermal Bags and Containers Market Report Scope

Isothermal Bags and Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1050.8 Million

|

|

Market Size (2034)

|

$2065.8 Million

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Product Type (Hard Containers, Soft Bags), By Material (EPS, PUR, PP, VIPs, Others), By End-Use (Pharmaceuticals & Healthcare, Food & Beverages, Chemicals, Other Applications), By Application (Last-Mile Delivery, E-commerce, Industrial, Commercial, Household)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Sonoco Products Company, Cold Chain Technologies, Inc., Amcor plc, DS Smith Plc, Cool Logistics Group, Pelican BioThermal LLC, Sofrigam Group, Cryopak Industries Inc., CSafe Global, Peli BioThermal, Exeltainer SL, Placon Corporation, Marko Foam Products Inc., Thermal Packaging Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Isothermal Bags and Containers Market Segmentation

By Product Type

- Hard Containers

- Soft Bags

By Material

By End-Use

- Pharmaceuticals & Healthcare

- Food & Beverages

- Chemicals

- Other Applications

By Application

- Last-Mile Delivery

- E-commerce

- Industrial

- Commercial

- Household

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Isothermal Bags and Containers Market

- Sealed Air Corporation

- Sonoco Products Company

- Cold Chain Technologies, Inc.

- Amcor plc

- DS Smith Plc

- Cool Logistics Group

- Pelican BioThermal LLC

- Sofrigam Group

- Cryopak Industries Inc.

- CSafe Global

- Peli BioThermal

- Exeltainer SL

- Placon Corporation

- Marko Foam Products Inc.

- Thermal Packaging Solutions

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and systematic research methodology to analyze the Isothermal Bags and Containers Market, integrating primary and secondary research, industry validation, and advanced analytical modeling. Our approach begins with the collection of qualitative and quantitative data from trusted sources, including corporate filings, press releases, regulatory reports, patent databases, and expert interviews with key stakeholders across cold chain logistics, pharmaceuticals, food, and e-commerce sectors. USDAnalytics triangulates insights through competitor benchmarking, technological trend mapping, and market adoption analysis to capture emerging opportunities such as phase change materials (PCMs), smart packaging, and reusable container systems. Advanced modeling techniques, including CAGR projections, regional demand forecasting, and product-type segmentation, ensure precise estimation of market growth trajectories, from USD 1,050.8 million in 2025 to USD 2,065.8 million by 2034 at a CAGR of 7.8%. The methodology also incorporates sustainability and regulatory compliance assessments, highlighting material innovations, digital tracking adoption, and last-mile delivery trends. By combining comprehensive data sources, in-depth trend evaluation, and market validation with industry experts, USDAnalytics delivers actionable, high-confidence insights for decision-makers aiming to optimize operations, innovate product offerings, and capture high-value opportunities in isothermal packaging markets globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.