Market Overview: Sustainability and Smart Cold Chain Solutions Driving Growth

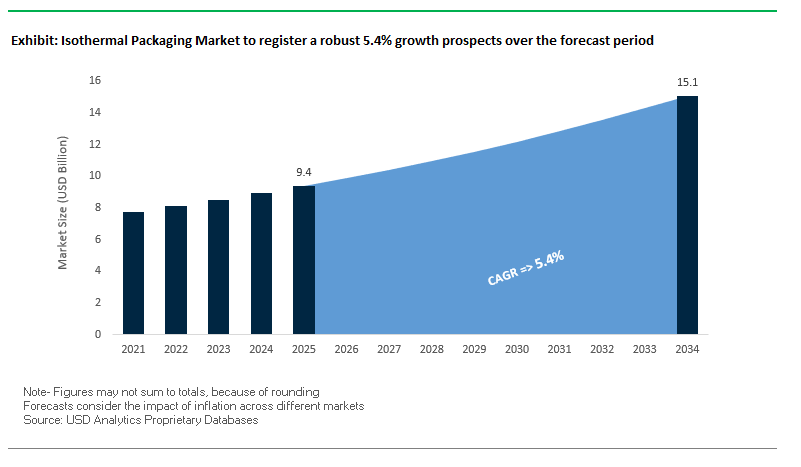

The Isothermal Packaging Market is valued at USD 9.4 billion in 2025 and is projected to reach USD 15.1 billion by 2034, growing at a CAGR of 5.4%. This market plays a critical role in supporting global cold chain logistics for pharmaceuticals, biologics, food, and industrial products, ensuring product integrity and compliance across increasingly complex supply chains. Industry professionals and buyers are asking: How can packaging balance thermal performance, cost-efficiency, and sustainability in high-demand sectors like healthcare and e-commerce?

Key Insights for Industry Professionals

- Market Expansion: From USD 9.4B (2025) → USD 15.1B (2034) at a CAGR of 5.4%, driven by e-commerce, food delivery, and healthcare logistics.

- E-commerce boom: Rising demand for insulated packaging in meal kits, groceries, and home-delivery models.

- Sustainable shift: Strong transition from EPS foam to biodegradable liners, paper-based solutions, and reusable containers.

- Healthcare demand: Growth in biologics and vaccine distribution requiring validated, high-performance isothermal solutions.

- Smart packaging adoption: Integration of sensors, RFID, and data loggers for real-time traceability in cold chain shipments.

Market Analysis: Recent Developments in Isothermal Packaging Industry

The global Isothermal Packaging Industry has seen significant consolidation and innovation, underscoring a shift toward sustainability, advanced insulation, and smart monitoring technologies.

In August 2025, DNP showcased mono-material, recyclable medical packaging at Medical Fair Thailand, signaling increased momentum in sustainable healthcare packaging. Just a month earlier, in July 2025, the merger of Amcor and Berry Global created a consumer packaging giant, strengthening global capabilities in flexibles and rigid packaging solutions. Around the same time, reports emphasized smart packaging adoption (QR codes, NFC, RFID) for traceability and engagement.

Innovation in insulation materials remains central. In May 2025, Sealed Air launched Cryovac ICETech, a sustainable insulation technology that lowers emissions and minimizes waste in perishable shipments. In April 2025, Sonoco restructured by selling its thermoformed and flexibles packaging business to Toppan Holdings, sharpening its focus on core temperature-assurance solutions. Earlier in February 2025, Amcor introduced AmFiber Performance Paper pouches, achieving a 73% carbon footprint reduction versus standard packs.

Sustainability milestones were also prominent. A December 2024 report emphasized the rising adoption of mono-material solutions, while October 2024 saw Pelican BioThermal unveil Crēdo Vault™, designed for bulk pharma shipments. Meanwhile, September 2024 highlighted Shiseido’s transition to kraft honeycomb wrap to replace plastic bubble wrap in e-commerce a strong indicator of cross-sector adoption of recyclable solutions.

Key Trends and Opportunities Driving the Isothermal Packaging Market

Strategic Pivot to 100% Recycled PET (rPET) Content

The isothermal packaging market is witnessing a decisive shift toward 100% recycled PET (rPET), fueled by consumer sustainability expectations, regulatory pressure, and corporate environmental commitments. Leading beverage corporations are moving beyond voluntary pledges, investing heavily to secure food-grade rPET supplies for large-scale operations. Coca-Cola HBC, for instance, targets 50% rPET in EU countries and Switzerland by 2025, aiming for 100% recycled or renewable PET by 2030 where feasible, supported by over €50 million in dedicated rPET facilities across Italy, Poland, and Romania. Switzerland became the first country to transition Coca-Cola’s local PET portfolio entirely to rPET in 2022, followed by Italy, Austria, Romania, and the Republic of Ireland in 2023. Similarly, PepsiCo has introduced its first 100% rPET carbonated beverage bottle in Taiwan and an rPET energy drink bottle in India, reflecting a global brand strategy to reduce virgin plastic use. Regulatory alignment also propels this trend, with the EU Packaging and Packaging Waste Regulation (PPWR) and U.S. state mandates, such as California’s 2032 recyclability requirements, incentivizing brands to adopt higher recycled content.

Policy-Driven Push for Extended Producer Responsibility (EPR)

Extended Producer Responsibility (EPR) policies are transforming packaging accountability by mandating financial and operational responsibility for end-of-life product management. The EU’s revised Waste Framework Directive and the 2025 PPWR establish national registers to monitor compliance and introduce modulated EPR fees based on packaging recyclability, linking economic costs directly to sustainable design. In the U.S., Maine and Minnesota have implemented state-level EPR legislation, with producers required to cover substantial portions of recycling costs by 2029. This financial pressure drives brands to design packaging for recyclability and incorporate recycled content, minimizing fees while supporting sustainability objectives. Industry responses include collaborations like PepsiCo’s participation in the Digital Watermarks Initiative HolyGrail 2.0, aiming to enhance packaging waste sorting and boost recycling quality, ultimately reducing future EPR-related expenses.

Scaling Advanced Recycling Technologies

Advanced (chemical) recycling presents a strategic opportunity to overcome the limitations of mechanical recycling, particularly for food-grade applications. By breaking plastics down to molecular building blocks, this technology enables the production of virgin-quality rPET from a broader range of waste streams. Investment in chemical recycling is accelerating, with Plastics Europe projecting growth from €2.6 billion in 2025 to €8 billion by 2030, aimed at expanding high-quality recycled feedstock production. Strategic partnerships are emerging, such as Eastman’s $2 billion global investment in molecular recycling facilities capable of processing mixed plastic waste to create materials identical to virgin PET. This technology also addresses hard-to-recycle plastics, including colored bottles and multi-layer films, reducing landfill contributions. Companies like Loop Industries are expanding internationally, with a 70kta facility planned in India by 2027, demonstrating efforts to build the infrastructure necessary to meet the surging global rPET demand.

Lightweighting and Material Reduction via Design Innovation

The rising costs of resin (virgin and recycled) and EPR fees are driving innovation in material reduction and lightweight packaging design. Coca-Cola has redesigned small PET bottles in the US and Canada, reducing weight from 21 to 18.5 grams, targeting a 3 million metric ton reduction in PET usage by 2025. These lighter bottles maintain structural integrity and product quality, preventing CO₂ loss while optimizing performance. Packaging solution providers are supporting these efforts; Sidel’s StarLITE®-R STILL bottle base allows for 100% rPET integration and reduces blowing pressure by 20%, cutting energy consumption and costs. Lightweighting extends beyond bottles, as evidenced by ALPLA Group’s “The Simple One” bag, which reduces material use by up to 60% compared to standard HDPE bottles, signaling a broader industry movement toward sustainable, resource-efficient packaging designs.

Competitive Landscape: Key Players in Global Isothermal Packaging

The Isothermal Packaging Market is defined by global players combining sustainability, thermal validation, and advanced designs to meet diverse industry needs.

Sonoco Products Company: Optimizing portfolios for sustainable packaging

Sonoco continues to leverage its protective and temperature-assurance expertise across healthcare and food. In April 2025, it sold its thermoformed/flexibles division to Toppan, refocusing on its core operations. Its insulated shippers and cleanroom-certified packaging maintain reliability for sensitive goods. Sonoco’s 2030 sustainability goals reinforce its strategic direction to deliver scalable and environmentally friendly cold chain solutions.

Pelican BioThermal: Reusable thermal systems for life sciences

Pelican BioThermal remains a leader in validated reusable cold chain solutions. In October 2024, it launched Crēdo Vault™, optimized for bulk pharma shipments, and in November 2024, it appointed Sam Herbert as CEO to drive innovation. With reusable products like Crēdo™ and CoolGuard™, Pelican supports high-performance pharma logistics. Its focus remains on reducing emissions and scaling sustainability in life sciences cold chains.

Sealed Air Corporation: Driving insulation efficiency with Cryovac ICETech

Sealed Air leverages its foam-in-place and air-filled insulation expertise to deliver performance packaging. In May 2024, it launched Cryovac ICETech, designed to reduce emissions in perishable shipments. Its Instapak® PUR foams and TempGuard® insulated bags provide up to 72 hours of thermal assurance for last-mile delivery. Sealed Air’s strategy centers on e-commerce and sustainability, reducing food waste with smart and efficient packaging.

TemperPack Technologies, Inc.: Curbside recyclable EPS alternatives

TemperPack is disrupting EPS with paper-based insulation liners. In 2024, its products helped eliminate 21 million cubic feet of plastic packaging waste, proving its impact on sustainability. With flagship lines ClimaCell™ and WaveKraft™, the company enables curbside recyclable cold chain packaging. Its strategy emphasizes eco-friendly innovation, protecting both temperature-sensitive goods and environmental goals.

DS Smith Plc: Fiber-based insulated solutions for circular economy

DS Smith delivers paper-based collapsible insulation as an alternative to rigid formats. In 2024, it reported 2% volume growth and achieved its target of replacing 1 billion plastic packs with fiber-based alternatives a year ahead of schedule. With a circular “box-to-box” recycling model, DS Smith is aligning cold chain packaging with sustainability mandates while reducing reliance on hard-to-recycle plastics.

Isothermal Packaging Market Share Insights

Soft Bags Maintain Leadership in the Isothermal Packaging Market by Product Type

Soft bags represent 70% of the global isothermal packaging market in 2025, extending their dominance from isothermal bags and containers into broader packaging applications. Their scalability and low material costs make them the go-to choice for retailers, logistics companies, and food service operators managing large delivery volumes. The combination of recyclability, reusability, and adaptability to diverse product categories from groceries to pharmaceuticals cements their role as the backbone of the thermal packaging industry. Hard containers, while smaller in share, remain critical for industries requiring premium performance, particularly in pharmaceuticals and high-value perishables. Their robustness ensures prolonged cold-chain compliance, better stackability, and resilience against damage in long-haul transit, maintaining strong adoption in regulated logistics sectors. The segmentation illustrates how soft bags dominate high-volume consumer-driven demand, while hard containers retain their foothold in specialized professional and industrial applications.

Last-Mile Delivery Continues to Anchor Market Share by Application in Isothermal Packaging

Last-mile delivery accounts for 45% of the global isothermal packaging market in 2025, securing its role as the most critical application. The ongoing expansion of direct-to-consumer models in grocery, meal kits, and pharmaceutical delivery highlights how insulated packaging has become a strategic enabler of customer satisfaction and food safety. As urbanization and digital commerce accelerate, logistics providers rely on cost-effective soft bags and liners to maintain temperature integrity across millions of small-volume deliveries. E-commerce reinforces this share by driving the bulk of online perishable goods shipments, while commercial applications from restaurants and caterers provide a steady professional demand base. Household adoption continues to grow, particularly among health-conscious and convenience-focused consumers seeking reusable thermal bags. Industrial demand, though niche, is highly valuable, with validated containers supporting sensitive material transport across chemicals and electronics. Overall, last-mile delivery dominates by volume, while e-commerce and specialized industrial logistics drive premium innovation within the isothermal packaging ecosystem.

United States Isothermal Packaging Market Expands on Regulatory Compliance and Smart Packaging Innovations

The U.S. isothermal packaging market is significantly shaped by a fragmented regulatory landscape at state and federal levels. The Food and Drug Administration (FDA) and Department of Transportation (DOT) enforce stringent guidelines to ensure the safe transit of perishable goods, while the Drug Supply Chain Security Act (DSCSA) mandates unique identifiers on pharmaceutical packaging, driving the adoption of smart packaging solutions with real-time tracking and temperature monitoring.

Technological advancements are fueling market growth, including the development of eco-friendly, reusable insulated packaging solutions, such as those launched by The Packaging Company in March 2024. The adoption of IoT-enabled smart packaging solutions is increasing, ensuring the safe delivery of high-value biologics and perishable foods. Corporate investments, including Cold Chain Technologies’ upgraded isothermal packaging with enhanced insulation and sustainable materials, further strengthen the market. Key applications are concentrated in e-commerce, pharmaceutical, and food delivery sectors, with the “Amazon Effect” driving demand for temperature-controlled packaging. Sustainability remains a primary focus, with recyclable paper-based insulation and non-toxic gel packs gaining popularity across industries.

Germany Leads in Sustainable Isothermal Packaging through Circular Economy and Industry 4.0

Germany’s isothermal packaging market is governed by strict regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates that all packaging be fully recyclable or reusable by 2030. The Single-Use Plastics levy incentivizes companies to adopt reusable and recyclable alternatives, further boosting sustainable isothermal container adoption.

Technological innovation is a cornerstone of the German market, with Industry 4.0 initiatives integrating digital manufacturing technologies to optimize production. Market leaders like Pelican BioThermal are driving high-performance, temperature-controlled packaging solutions. Germany’s Packaging Act (VerpackG) encourages designs optimized for recycling through modulated fees, favoring reusable over single-use solutions. Corporate investments by domestic and international players are expanding product portfolios to meet the growing demand for sustainable, high-performance isothermal packaging.

China’s Isothermal Packaging Market Accelerates with Green Policies and Advanced Manufacturing

China’s isothermal packaging market is driven by governmental “dual carbon” initiatives promoting sustainable industrial practices. The March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages recycling and sustainable material adoption across industries. Regulatory reforms, including the GB/T 31268 standard effective November 2024, address excessive packaging, particularly in e-commerce, which is a key distribution channel for isothermal products.

Technological advancements, including AI and “5G plus industrial internet” integration, enhance production efficiency and flexible manufacturing for high-performance isothermal packaging. Companies like Greif are implementing real-time tracking technology, GCube Connect, to improve performance and visibility in cold chain logistics. The domestic manufacturing push encourages local firms to invest in advanced insulation materials and circular packaging solutions, meeting growing demand for eco-friendly, high-quality packaging.

India’s Isothermal Packaging Market Booms with Cold Chain Expansion and Circular Economy Initiatives

India’s government initiatives are promoting a circular economy and driving growth in the isothermal packaging market. The Pradhan Mantri Kisan Sampada Yojana (PMKSY), with an allocation of INR 4600 Cr until March 2026, focuses on building integrated cold chain infrastructure from farm to consumer, fostering demand for innovative insulated packaging.

Technological advancements include the adoption of advanced materials and specialized products for safe and hygienic transportation of perishable goods. The Production Linked Incentive (PLI) scheme for pharmaceuticals and medical devices further supports domestic manufacturing and technological upgrades. Corporate investments are increasing to meet demand from India’s expanding food processing and cold chain sectors. Rising exports of pharmaceuticals and perishable goods also fuel the need for high-performance isothermal packaging that meets global safety and quality standards.

Japan’s Isothermal Packaging Market Drives Innovation with VIPs and High-Performance Solutions

Japan’s isothermal packaging market benefits from the country’s leadership in precision manufacturing and next-generation production ecosystems. Innovation focuses on vacuum-insulated panels (VIPs) and paper-based thermal wraps, which are gaining traction across Asia and Europe due to their performance and sustainability benefits.

Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes “Design for the Environment” and the reduction of single-use plastics. Market players are pivoting toward specialty, value-added products with superior aesthetic and functional properties, including self-sealing and high-barrier packaging, to meet specific industry requirements. This focus on high-performance solutions supports growth across pharmaceuticals, food, and temperature-sensitive logistics sectors.

Brazil’s Isothermal Packaging Market Strengthens with Sustainable Waste Management and Last-Mile Innovation

Brazil’s isothermal packaging market is shaped by the National Solid Waste Policy, amended in April 2022, which sets long-term goals for sustainable waste management. The EU-Mercosur trade agreement is expected to further stimulate investment and market diversification.

Technological advancements in the food delivery industry include shuttle systems that combine frozen, chilled, and ambient items into insulated totes for efficient last-mile delivery. Demand is strong in frozen foods, fresh produce, and ready-to-eat meals. Corporate investments by domestic and international players continue to expand sustainable and high-performance packaging solutions, ensuring compliance with regulatory and international safety standards.

Isothermal Packaging Market Report Scope

Isothermal Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.4 Billion

|

|

Market Size (2034)

|

$15.1 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Hard Containers, Soft Bags), By Material (EPS, PUR, PP, VIPs, Others), By End-Use (Pharmaceuticals & Healthcare, Food & Beverages, Chemicals, Other Applications), By Application (Last-Mile Delivery, E-commerce, Industrial, Commercial, Household)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Sonoco Products Company, Cold Chain Technologies, Inc., Amcor plc, DS Smith Plc, Cool Logistics Group, Pelican BioThermal LLC, Sofrigam Group, Cryopak Industries Inc., CSafe Global, Peli BioThermal, Exeltainer SL, Placon Corporation, Marko Foam Products Inc., Thermal Packaging Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Isothermal Packaging Market Segmentation

By Product Type

- Hard Containers

- Soft Bags

By Material

By End-Use

- Pharmaceuticals & Healthcare

- Food & Beverages

- Chemicals

- Other Applications

By Application

- Last-Mile Delivery

- E-commerce

- Industrial

- Commercial

- Household

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Isothermal Packaging Market

- Sealed Air Corporation

- Sonoco Products Company

- Cold Chain Technologies, Inc.

- Amcor plc

- DS Smith Plc

- Cool Logistics Group

- Pelican BioThermal LLC

- Sofrigam Group

- Cryopak Industries Inc.

- CSafe Global

- Peli BioThermal

- Exeltainer SL

- Placon Corporation

- Marko Foam Products Inc.

- Thermal Packaging Solutions

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise insights into the Isothermal Packaging Market, integrating primary and secondary research techniques with a strong focus on industry validation. Our analysts collect data from trusted sources including company annual reports, regulatory filings, trade publications, and government databases, while conducting in-depth interviews with packaging manufacturers, cold chain operators, sustainability experts, and logistics professionals. Market sizing and forecasts are built using top-down and bottom-up approaches, ensuring alignment with historical data and current demand dynamics across pharmaceuticals, food, e-commerce, and industrial sectors. Competitive benchmarking, policy mapping, and technology assessment provide a detailed view of innovation trends such as rPET adoption, EPR regulations, and smart packaging integration. USDAnalytics further enhances accuracy through scenario modeling, evaluating drivers like sustainability transitions, regulatory compliance, and cold chain infrastructure growth, ensuring industry professionals gain actionable intelligence for strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.