Bags & Containers Market Overview: Circular Design, E-commerce Fulfillment, and Material Mix Push Steady Growth

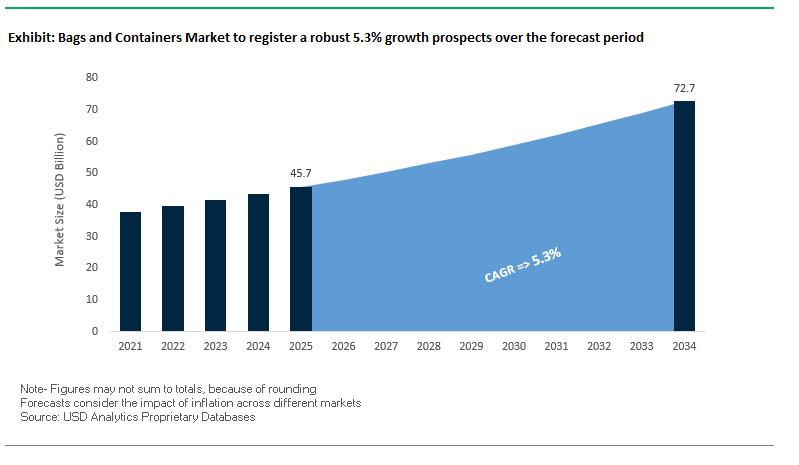

The Global Bags and Containers Market is projected to expand from $45.7 billion in 2025 to $72.7 billion by 2034, registering a CAGR of 5.3%. Growth is anchored in three structural shifts: (1) circular-economy packaging with rising PCR (post-consumer recycled) content, (2) surging e-commerce fulfillment requiring protective, automation-ready formats, and (3) a pragmatic material mix where plastics retain share while paper/fiber and mono-materials scale for recyclability. For buyers and packaging strategists, the near-term priorities are clear: secure recycled feedstocks, design for automated distribution, and redesign SKUs toward mono-material, lightweight constructions without compromising barrier performance or brandability.

Key Insights for Industry Professionals

- Recycled content integration accelerates: leading suppliers are commercializing packs with ≥50% PCR to meet brand ESG targets and retailer scorecards.

- Food & beverage drives volume: bag-in-box and specialized liquid containment account for ~44% share (2025) within that niche, favored for tamper-evidence and cost-to-serve advantages.

- E-commerce lifts protection demand: logistics providers report ~25% YoY increases in air pillows and paper void fill, tying parcel growth to inside-the-box protection.

- Plastics remain essential: 42.3% material share (2024) driven by versatility, sealing, and durability across retail, foodservice, and healthcare.

- Backpacks dominate consumer carry: 41.2% category share (2024) on the strength of student, commuter, and travel use cases, informing retail assortment and channel strategy.

Market Analysis: Where Growth, Capex, and M&A Are Re-Shaping Bags & Containers

Strategic portfolio actions remain brisk. In January 2025, International Paper completed its > $7B acquisition of DS Smith, consolidating containerboard and corrugated capacity aligned with fiber-based secondary packaging. In April 2025, TOPPAN finalized its $1.8B purchase of Sonoco’s thermoformed and flexibles businesses, sharpening focus on higher-growth flexible formats and geographic reach. These moves tighten upstream substrate supply and broaden downstream converting capabilities critical for bags, liners, pouches, and protective mailers.

Innovation is equally active. Smurfit Kappa launched a lightweight Bag-in-Box (February 2025) engineered with enhanced oxygen/light barriers to extend wine and juice shelf life while reducing transport emissions. Liqui-Box (January 2025) unveiled next-gen recyclable films for Bag-in-Box systems, advancing mono-material recyclability without sacrificing toughness. Amcor (August 2025) announced a healthcare packaging expansion in Costa Rica and a UK recycling-facility upgrade for flexibles, reinforcing both medical-grade capability and circular infrastructure. A cross-industry example: Amcor + Flügger (August 2025) introduced a paint container with 50% recycled material, signaling how PCR resin streams are scaling beyond food to industrials.

Portfolio optimization continues on the plastics side. Berry Global (December 2024) agreed to divest its Specialty Tapes unit (≈$540M), simplifying the portfolio toward consumer-oriented, higher-growth lines and strengthening the balance sheet for focused investment. On the consumer bags front, Targus (December 2024) launched a Made-in-India backpack with water-resistant materials and anti-theft features, mirroring the 41.2% share dominance of backpacks and the premiumization of commuter gear.

Emerging Trends and Strategic Opportunities Shaping the Bags and Containers Market

Accelerated Regulatory Phase-Out of Single-Use Plastics Driving Material Transition

The bags and containers market is undergoing a compliance-driven transformation as governments worldwide accelerate the phase-out of single-use plastics. The European Union’s Single-Use Plastics Directive, enforced since 2021, bans items such as plastic plates, cutlery, straws, and cotton buds, while imposing mandatory recycling targets requiring plastic beverage bottles to contain 25% recycled plastic by 2025 and 30% by 2030. In North America, Extended Producer Responsibility (EPR) laws in states like California, Colorado, Maine, Minnesota, and Oregon, along with Canada’s national zero-plastic-waste goal for 2030, are driving similar shifts. Corporations are actively responding to these regulations by adopting paper-based alternatives for products such as chocolate packaging and e-commerce mailers, highlighting that regulatory compliance, rather than voluntary sustainability, is the primary catalyst for material transitions in the market.

Strategic Corporate Investment in Reusable and Refillable Packaging Systems

A parallel trend in the market is the strategic investment by FMCG brands and retailers in reusable and refillable packaging systems, representing a fundamental shift from linear to circular business models. Leading beverage companies, including Coca-Cola and PepsiCo, are committing to ambitious targets for reusable packaging by 2030, already executing initiatives across multiple markets. Retailers like Unilever are pioneering refill stations under programs like “Refill Revolution” and partnerships with Loop by TerraCycle, enabling consumers to return and reuse containers for household products. This transition necessitates significant investment in durable container manufacturing, reverse logistics, and consumer engagement strategies, underscoring a systemic redefinition of packaging operations and business models in response to circular economy imperatives.

Development of High-Performance Paper-Based Barriers for Flexible Packaging

A major market opportunity lies in the development of high-performance, paper-based bags and pouches with bio-based functional barriers to replace traditional plastic laminates while maintaining essential moisture and oxygen protection. Academic and corporate research is focusing on materials such as chitosan, cellulose, and starch to enhance barrier performance, with studies reporting up to a 90% reduction in oxygen permeation. Packaging companies like Mondi are scaling production of ultra-high-barrier paper solutions, such as “FunctionalBarrier Paper Ultimate,” boasting an oxygen transmission rate (OTR) below 0.5 cm³, suitable for products like muesli and bouillon cubes. Overcoming the natural hydrophilicity of paper remains a technical challenge, but water-based barrier coatings from companies like H.B. Fuller are enabling fully recyclable, moisture- and oil-resistant packaging that aligns with sustainability mandates while meeting performance expectations for sensitive goods.

Competitive Landscape: Strategies of Leading Bags & Containers Players

The competitive field is defined by scale, substrate breadth, and circularity roadmaps. Leaders are pairing recycled feedstock access with converting know-how and automated fulfillment capabilities.

Amcor plc scaling circular flexibles and PCR infrastructure

Overview: Amcor’s broad platform in flexible and rigid solutions spans food, beverage, personal care, and healthcare. In August 2025, it expanded healthcare packaging in Costa Rica to serve high-spec customers in LATAM and upgraded a UK recycling facility to boost flexible-film circularity. A joint launch with Flügger (August 2025) delivered a 50% PCR paint container, exemplifying cross-industry PCR uptake. Strategically, Amcor’s “fund-and-build” posture (e.g., Lift-Off startup support) and mono-material/ recycle-ready laminates position it as a go-to partner for brands transitioning SKUs to lower-carbon, retailer-approved formats.

Berry Global Group, Inc. portfolio focus toward consumer growth

Overview: Berry is a scale player in plastic packaging and engineered materials. In late 2024, Berry announced the $540M sale of its Specialty Tapes business (closing expected 1H 2025), part of a program that generated ~$1.3B cash to reduce debt and sharpen focus on consumer end-markets (targeting >80% of volume). This optimization supports investment in light-weighted rigid containers, films, and closures used across food, retail, and e-commerce, while aligning with brand owners’ PCR content goals.

Sealed Air Corporation automation and inside-the-box protection leadership

Overview: Sealed Air (“SEE”) combines materials science with automation to protect goods and extend food shelf life. Its portfolio spans BUBBLE WRAP® cushioning, air systems, on-demand foams, and food solutions under CRYOVAC®. Recent innovations include automated void sensing and paper insertion systems that reduce material use and labor per parcel vital as e-commerce volumes keep rising. SEE’s strategy to create a touchless, digitally driven fulfillment environment aligns squarely with the sector’s shift to efficient, low-waste operations.

Silgan Holdings Inc. diversified rigid packaging with dispensing scale

Overview: Silgan supplies dispensing & specialty closures, metal containers, and custom plastics across food, personal care, and healthcare. Acquisitions such as Unicep Packaging expanded precision-dosing dispensing for healthcare and diagnostics, while the earlier Weener Plastics deal bolstered dispensing growth (driving a notable uplift in segment sales). Silgan’s metal containers also post mid-single-digit growth in pet food an indicator of resilient, value-add rigid formats coexisting with flexible bags.

Smurfit Kappa Group plc fiber systems for liquids and secondary packaging

Overview: Smurfit Kappa’s integrated model (forestry → paper → converting) underpins a wide fiber portfolio, from corrugated containers and paper bags to Bag-in-Box. In February 2025, it launched a lightweight Bag-in-Box tailored for wine/juice, improving barrier performance and transport efficiency. The company’s sustainability commitments and in-house recycling loops make it a preferred partner for retailers and beverage brands accelerating plastic replacement in secondary/tertiary packaging while maintaining product protection and shelf presence.

Bags and Containers Market Share Insights

Flexible Bags Lead Market Share by Product Type in Bags and Containers Industry

Flexible bags dominate the bags and containers industry with a commanding 50% share, reflecting their unmatched material efficiency, cost-effectiveness, and adaptability across sectors. From stand-up pouches for snacks and pet food to woven sacks for fertilizers and chemicals, flexible bags have become the backbone of high-volume applications where weight reduction and logistics efficiency drive decisions. Their dominance is also amplified by e-commerce, where lightweight, space-saving packaging directly reduces freight costs and carbon emissions. While rigid formats offer superior protection, flexible bags remain the preferred option in cost-sensitive and high-turnover categories, with ongoing innovation in mono-material laminates and recyclable films strengthening their position against rising sustainability regulations.

Food and Beverages Dominate Market Share by End-Use Industry in Bags and Containers Industry

Food and beverages account for nearly 45% of all demand in the bags and containers industry, underscoring their role as the sector’s primary driver. This dominance spans diverse formats, from flexible pouches for snacks, sauces, and frozen meals to rigid PET bottles for beverages and semi-rigid tubs for dairy products. The segment’s scale is reinforced by global consumption growth, strict requirements for product preservation, and intense competition for shelf visibility, all of which push continuous innovation in barrier materials, resealable closures, and lightweight rigid formats. The F&B sector is also central to packaging sustainability, with leading brands committing to higher recycled content and recyclable structures making it the most scrutinized and innovation-led end-use category in the industry.

United States: Regulatory Compliance and Sustainable Innovations Driving Bags and Containers Market

The U.S. bags and containers market is being significantly shaped by evolving regulations and sustainability trends. States like California are implementing stringent mandates, such as the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), which requires a shift toward recyclable and reusable packaging, including bags and containers. In response, companies are investing heavily in automation technologies, deploying right-sizing machinery that custom-cuts corrugated blanks for each order, reducing material use by up to 30% while optimizing shipping costs.

Sustainability remains a key focus, with the Department of Energy allocating over $52 million toward cellulose-based films as next-generation substrates for eco-friendly packaging. Corporate initiatives further reinforce this trend; for instance, Amazon has replaced 95% of plastic air pillows in its North American fulfillment network with recycled paper alternatives. Additionally, regulatory pressures from the EPA, including updated rules on PFAS in packaging, are prompting manufacturers to reformulate grease-resistant papers and food-contact materials. The rise of e-commerce continues to drive demand for lightweight, durable, and protective packaging solutions, including inflatable bags and cushioning materials that minimize product damage and shipping costs.

Germany: Circular Economy and High-Precision Manufacturing Transforming Bags and Containers

The German bags and containers market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective from February 2025. This legislation fosters demand for eco-friendly and highly recyclable packaging, while Germany’s leadership in the circular economy ensures that producers are responsible for the entire packaging lifecycle, incentivizing innovations in mono-material solutions and fiber-based alternatives.

Technological advancements are driving new product developments. For example, SIG introduced alu-layer-free full barrier aseptic cartons for Austrian dairy companies, showcasing innovations in barrier technology applicable to bags and containers. The PPWR also sets ambitious targets for reuse and recyclability by 2030, compelling manufacturers to adopt high-speed, high-precision filling and sealing machinery. This combination of regulatory compliance, circular economy practices, and advanced manufacturing positions Germany as a hub for sustainable, high-quality bags and containers.

China: Green Transformation and E-Commerce Expansion Fuel Market Growth

China’s bags and containers market is being propelled by the government’s dual carbon goal, which promotes the use of eco-friendly and reusable materials. Policies restricting non-degradable plastics in express delivery by 2025 are accelerating demand for paper-based and sustainable alternatives. The integration of automation, AI, and “5G plus industrial internet” technologies enhances production efficiency and flexibility, enabling manufacturers to meet the growing requirements of both domestic and export markets.

The expansion of e-commerce platforms is a significant growth driver, leading to a high demand for secure, lightweight, and tamper-proof packaging. Innovations are evident, such as the collaboration between Mespack and Fuji Seal to replace plastic bottles with pre-made spouted pouches, reflecting the market’s shift toward flexible packaging solutions. Furthermore, China’s “Made in China 2025” initiative is promoting high-tech manufacturing, aiming to increase domestic content of core materials to 70%, thereby boosting the technological capabilities and sustainability of bags and containers.

India: Government Initiatives and Eco-Friendly Packaging Adoption Accelerate Market Expansion

India’s bags and containers industry is benefiting from government programs such as “Make in India” and “Zero Effect Zero Defect”, which support quality domestic production and industrial infrastructure development. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, drives demand for standardized, high-quality packaging solutions, particularly in food and retail applications.

Regulatory developments, including the Plastic Waste Management (Amendment) Rules, are promoting eco-friendly alternatives, while initiatives by FSSAI encourage innovative and sustainable packaging materials. Rising disposable incomes and urbanization are changing consumer preferences toward convenient, single-serve, on-the-go packaging, increasing the adoption of pouches and ready-to-use containers. Strategic partnerships and investments in PET bottle-to-bottle recycling support compliance with Extended Producer Responsibility (EPR) rules, enabling manufacturers to produce packaging with higher recycled content, reinforcing the sustainability and growth of the Indian bags and containers market.

Bags and Containers Market Report Scope

Bags and Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$45.7 Billion

|

|

Market Size (2034)

|

$72.7 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Type (Rigid Containers, Flexible Bags, Semi-Rigid Packaging), By Packaging Material (Plastics, Glass, Metal, Paper & Paperboard, Bioplastics), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Homecare & Household, E-commerce & Logistics, Industrial Goods), By Application (Retail Bags, Shopping Bags, Pouches, Trays, Bottles, Jars, Cans, Crates & Boxes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Berry Global Inc., Sonoco Products Company, Huhtamaki Oyj, WestRock Company, DS Smith plc, Smurfit Kappa Group plc, AptarGroup, Inc., Silgan Holdings Inc., Greif, Inc., Sealed Air Corporation, International Paper Company, Crown Holdings, Inc., Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bags and Containers Market Segmentation

By Product Type

- Rigid Containers

- Flexible Bags

- Semi-Rigid Packaging

By Packaging Material

- Plastics

- Glass

- Metal

- Paper & Paperboard

- Bioplastics

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Homecare & Household

- E-commerce & Logistics

- Industrial Goods

By Application

- Retail Bags

- Shopping Bags

- Pouches

- Trays

- Bottles

- Jars

- Cans

- Crates & Boxes

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bags and Containers Market

- Amcor plc

- Mondi Group

- Berry Global Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- WestRock Company

- DS Smith plc

- Smurfit Kappa Group plc

- AptarGroup, Inc.

- Silgan Holdings Inc.

- Greif, Inc.

- Sealed Air Corporation

- International Paper Company

- Crown Holdings, Inc.

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to deliver an in-depth analysis of the global Bags and Containers Market, integrating primary and secondary research to provide actionable insights for industry professionals. The study leveraged interviews with packaging manufacturers, brand owners, logistics providers, and regulatory authorities, alongside extensive review of corporate announcements, M&A activity, product innovations, and sustainability initiatives. Market sizing and growth projections were derived from historical trends, emerging regulatory frameworks, material transitions toward circularity, e-commerce fulfillment demands, and shifting consumer preferences. Segmentation was carried out by product type, material, application, and end-use industries, while regional insights cover major markets including the U.S., Germany, China, and India. Competitive intelligence highlights leading players such as Amcor, Berry Global, Smurfit Kappa, Silgan Holdings, and Sealed Air, analyzing their strategies in sustainable, reusable, high-barrier, and automation-ready packaging solutions. By combining insights on technological innovation, regulatory compliance, material optimization, and circular economy initiatives, USDAnalytics provides stakeholders with a detailed understanding of market dynamics, growth drivers, and strategic investment opportunities across the global bags and containers landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.