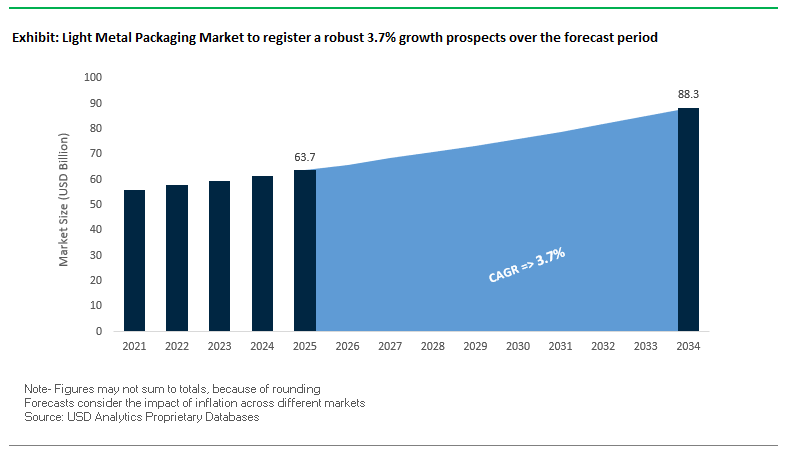

Light Metal Packaging Market Overview: Recycling, Sustainability, and High-Barrier Performance (MV: USD 63.7 Bn in 2025 → USD 88.3 Bn by 2034, CAGR 3.7%)

The global light metal packaging market continues to gain traction as brand owners, regulators, and consumers demand recyclable, high-performance, and visually appealing packaging. Aluminum and steel remain the dominant substrates, valued for their infinite recyclability, strong barrier protection against light, oxygen, and moisture, and compatibility with high-speed canning and filling lines. Beverage cans, food cans, and aerosol formats are witnessing strong adoption, with growing demand for lightweight, high-recycled-content alloys that reduce carbon footprints without compromising strength.

Industry professionals evaluating sourcing strategies must align with corporate ESG targets, regional deposit-return systems, and consumer-driven sustainability preferences. Advanced coatings and digital printing are further transforming metal packaging into premium marketing assets, helping brands differentiate while enhancing product safety.

Key insights

- Circular economy backbone: Aluminum cans achieve some of the highest recycling rates globally, supporting closed-loop systems.

- Sustainability premium: Lightweight, high-recycled-content alloys are becoming a procurement standard for food and beverage companies.

- Barrier superiority: Light metal packaging eliminates light and oxygen ingress, significantly extending shelf life compared to plastics.

- Brand differentiation: Advanced coatings, textured finishes, and high-resolution printing boost retail impact and consumer engagement.

Market Analysis: Recent Industry Developments Strengthen Circularity and Regional Manufacturing

The light metal packaging industry has seen notable corporate restructuring, sustainability commitments, and capacity expansions. In August 2025, Ball Corporation offloaded a 41% stake in its Saudi joint venture while retaining a 10% interest—freeing resources to focus on its core aluminum can portfolio. Also in August 2025, Crown Holdings secured SBTi validation for its net-zero target, underlining its ESG leadership, while Novelis and DRT Holdings formalized a joint development agreement to accelerate adoption of high-recycled-content alloys for can ends.

Capacity expansion and efficiency were central themes in August 2025, with Golden Aluminum commissioning a new strip caster in Colorado and Century Aluminum announcing a $50M restart of production at its Mt. Holly, South Carolina smelter. In parallel, Can-Pack S.A. unveiled an ultra-lightweight aluminum can design, showcasing its technical leadership in down-gauging while maintaining durability.

Earlier in the year, February 2025, Ball Corporation acquired Florida Can Manufacturing to strengthen its North American footprint. Prior to that, in October 2024, Silgan Holdings expanded into dispensing and specialty closures via the acquisition of Weener Plastics, diversifying its presence in packaging adjacencies.

Emerging Trends and Strategic Opportunities in the Light Metal Packaging Market

Strategic Investment in Aluminum Can Production Capacity to Capture Share from Plastic

The light metal packaging market is witnessing significant investment as beverage brands shift toward aluminum to meet sustainability and consumer-driven goals. Companies like Ball Corporation have invested $290 million to expand their Nevada aluminum can facility, while Hindalco Industries commissioned a new production plant in Maharashtra, India, in 2023. Global players such as Can Pack Group are also establishing new production bases in the U.S. and Czech Republic, highlighting a worldwide commitment to scale aluminum production. This trend is driven by the superior recyclability of aluminum, with over 75% of all U.S.-produced aluminum still in use, according to the Aluminum Association. Consumer preferences are a strong motivator, as a Boston Consulting Group study found that 44% of consumers avoid products in “harmful” packaging. These investments not only align with corporate ESG strategies but also strengthen aluminum’s position against plastic alternatives in beverages and beyond.

Adoption of Next-Generation Recycled Aluminum Alloys and DWI Technology

To further decarbonize packaging, manufacturers are developing advanced recycled aluminum alloys and implementing Draw-and-Wall-Iron (DWI) technology for lightweighting. Producing secondary aluminum uses only about 5% of the energy required for primary production, making high post-consumer recycled (PCR) content alloys a key strategy for energy reduction. Research into “recycling-friendly” alloys ensures tolerance to impurities like iron and silicon, improving scrap utilization. DWI technology allows for thinner, lightweight cans without compromising structural integrity, lowering material use and reducing transportation-related carbon emissions. Collectively, these advancements contribute to significant carbon footprint reduction, preventing over 90 million tons of CO2 emissions annually. This trend underscores the convergence of alloy innovation, energy-efficient manufacturing, and lightweight design in modern aluminum can production.

Expansion into Specialty Food and Health & Wellness Applications with Shaped and Printed Cans

Beyond beverages, the high-end food, pet food, and supplement sectors present growth opportunities for differentiated aluminum packaging. Companies like Trivium Packaging offer uniquely shaped metal bottles and cans for vitamins, supplements, and wet foods, allowing brands to stand out on crowded shelves. Advanced printing technologies, including digital printing and textured finishes, enable premium branding and high-resolution graphics, which are essential for specialty products. Light metal packaging also provides superior barrier properties against light, gas, and moisture, critical for maintaining freshness and efficacy in health and wellness products, such as powdered infant formula or supplements. These developments position aluminum as a preferred choice for premium, value-added packaging applications.

Development of Smart and Connected Metal Packaging for Consumer Engagement

The integration of digital technologies into aluminum packaging transforms it from a passive container into an interactive platform. NFC tags, such as those developed by TOPPAN, can overcome metal interference challenges and enable authenticity verification, consumer engagement, and tracking of grey market products. QR codes printed directly on cans provide traceability and connect consumers to product information, supply chain data, or sustainability initiatives. Thermochromic inks offer functional benefits by changing color with temperature, indicating optimal beverage consumption conditions. Smart packaging also enables interactive marketing campaigns, such as “scan & win” programs, allowing brands to directly engage consumers and collect actionable insights. This opportunity highlights the potential for aluminum packaging to serve as a platform for enhanced brand interaction, supply chain transparency, and anti-counterfeiting measures.

Competitive Landscape: Leading Companies Driving Light Metal Packaging Innovation

The global light metal packaging industry is consolidated around a few key players, each scaling recycling integration, lightweighting, and advanced decoration to strengthen their market positions.

Ball Corporation: Recycling-driven aluminum packaging leadership

Ball Corporation specializes in beverage cans, aerosols, and aluminum cups, with a strategic pivot toward local-for-local manufacturing and higher recycled content integration. In August 2025, Ball divested part of its Saudi JV stake while retaining strategic interest, enabling sharper focus on its North American and European core markets. Its strength lies in its global manufacturing footprint of over 60 facilities and its strong recycling partnerships, making it a central force in closed-loop aluminum ecosystems.

Crown Holdings Inc.: Net-zero target aligned with Twentyby30 ESG roadmap

Crown Holdings is a key supplier of beverage, food, and aerosol cans, serving leading FMCG brands. In August 2025, its net-zero target was validated by the SBTi, reinforcing its Twentyby30 sustainability program. Crown focuses heavily on lightweighting and decorative innovation, offering enhanced designs and surface finishes that boost shelf appeal. Its wide global presence and integrated offerings position it as a preferred partner for sustainability-driven brands.

Ardagh Group S.A.: Pioneering low-carbon furnaces for sustainable packaging

Ardagh, through Ardagh Metal Packaging (AMP), supplies cans for beer, wine, and spirits alongside food applications. Its NextGen Furnace in Germany achieved over a 60% carbon reduction by adopting electrical heating—demonstrating leadership in low-carbon manufacturing processes. Ardagh’s offerings span standard cans to unique bottle shapes with premium finishes like sculptured embossing and screen printing, catering to high-value branding requirements.

Silgan Holdings Inc.: Expanding into dispensing and closures

Silgan Holdings remains a major supplier of food and pet food cans while expanding into closures. The October 2024 acquisition of Weener Plastics strengthened its dispensing and specialty closures portfolio. With 124 facilities globally, Silgan has unmatched reach and provides integrated rigid packaging solutions that combine metal containers with closure systems, allowing customers to streamline procurement.

Can-Pack S.A.: Innovating with ultra-lightweight cans

Can-Pack serves both food and beverage markets, known for its high-quality can manufacturing and decoration expertise. In August 2025, it introduced an ultra-lightweight aluminum can design at a European trade show, highlighting its role in down-gauging innovation. The company’s focus on gloss, matte, and textured finishes enhances brand differentiation. With a growing global presence, Can-Pack positions itself as a partner for sustainable, visually distinctive packaging solutions.

Light Metal Packaging Market Share Insights

Cans Dominate Market Share by Product Type in the Light Metal Packaging Industry

Cans account for the largest share at 48% of the light metal packaging industry in 2025, overwhelmingly driven by the beverage sector’s reliance on aluminum beverage cans. Their lightweight nature, superior recycling rates (with many brands committing to >70% recycled content), and compatibility with high-speed digital printing make them the go-to solution for both global soft drink giants and rapidly expanding categories like hard seltzers and canned wines. Beyond sustainability, cans are prized for their light and oxygen barrier properties, ensuring longer shelf life and product integrity. Closures hold the second-largest share, serving as a high-margin niche for beverages and pharmaceuticals with innovations in tamper-evidence, child resistance, and lightweighting. Tubes and aerosols represent specialty growth areas, particularly in cosmetics, personal care, and food products, while drums and barrels remain a stable industrial backbone for chemicals and paints. Smaller “others” categories, such as trays and foils, face share erosion as multifunctional cans and closures increasingly absorb their roles. Collectively, this segmentation underscores how cans dominate consumer-facing volume while closures and aerosols secure higher-value innovation opportunities.

Food & Beverages Lead Market Share by Application in the Light Metal Packaging Industry

Food and beverages represent the largest application, capturing 55% of the light metal packaging industry’s share in 2025, making this segment the undisputed leader. The dominance stems from surging demand for canned beverages and ready-to-eat products, with aluminum packaging providing unmatched barrier properties, rapid chilling capability, and infinite recyclability. Urban lifestyles and the growth of convenience consumption reinforce this position, while global regulations phasing out single-use plastics are accelerating substitution in favor of lightweight metal solutions. Personal care and cosmetics follow as the premium growth driver, leveraging aluminum tubes, aerosols, and compacts for luxury branding and recyclable credentials, with anodized finishes and airless spray technology setting new benchmarks. Household and industrial uses remain stable, focused on paints, lubricants, and cleaners where enhanced protective linings are essential for chemical safety. Pharmaceuticals form a smaller but high-value share, using light metal packaging for absolute moisture, oxygen, and light protection in aerosols, inhalers, and pill containers. Together, these dynamics confirm that food and beverages anchor the sector’s scale, while premium personal care and regulated pharma secure high-margin value growth.

United States Light Metal Packaging Market Expands Through Regulatory Alignment and Sustainable Innovations

The U.S. light metal packaging market is shaped by a fragmented regulatory environment, with FDA regulations ensuring food and beverage safety. State-level Extended Producer Responsibility (EPR) laws are promoting recyclable packaging, driving demand for sustainable aluminum and steel containers. Government recognition of aluminum as a critical mineral underpins strategic support for domestic manufacturing, reinforcing the role of light metal packaging in the clean energy transition.

Technological innovations, such as ultra-lightweight aluminum and steel cans, maintain structural integrity while reducing material consumption, catering to high-performance applications in the beverage and food sectors. Corporate investments focus on advanced recycling technologies to enhance the quality and closed-loop recyclability of metal packaging. The industry emphasizes sustainable production, with recycled content and improved recyclability as central imperatives, saving over 90 million barrels of oil equivalent annually and reinforcing the eco-friendly credentials of light metal packaging.

Germany Leads Light Metal Packaging Market With Circular Economy and Industry 4.0 Innovations

Germany’s light metal packaging market operates under strict regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging by 2030. This drives the adoption of sustainable aluminum and steel packaging solutions.

The market emphasizes high-performance coatings for metal cans to improve barrier properties and food safety. Germany’s Industry 4.0 initiatives are revolutionizing manufacturing, integrating automation and digital technologies. The Packaging Act (VerpackG) incentivizes designs for recycling, reinforcing demand for infinitely recyclable metals. Corporate investments focus on sustainable product development and high-performance solutions, positioning Germany as a global leader in eco-friendly light metal packaging technology.

China Light Metal Packaging Market Driven by Green Policies and Smart Manufacturing

China’s light metal packaging industry is undergoing a green transformation under the dual carbon goal, encouraging recycling and sustainable material usage. The Action Plan for Promoting Large-Scale Equipment Updates fosters eco-friendly production, while revised standards like GB/T 31268 regulate excessive packaging.

Technological advancements focus on automation, AI, and 5G industrial internet integration, optimizing production efficiency and flexible manufacturing for light metal packaging solutions. Local manufacturers are expanding capacity to meet the growing domestic demand for high-quality, circular aluminum and steel packaging, fueled by booming e-commerce, electronics, and food & beverage sectors.

India Light Metal Packaging Market Accelerates With Circular Economy Policies and Industrial Upgrades

India’s light metal packaging market is benefiting from the government’s circular economy initiatives, including the Make in India program and the Ministry of Steel’s Greening the Steel Sector roadmap, promoting sustainable steel recycling. Advanced materials and techniques, such as degauging to reduce steel thickness without compromising strength, are gaining traction.

Corporate investments are increasing, with companies like Tata Steel establishing recycling plants and championing circularity initiatives. The market is particularly strong in the food and beverage and industrial sectors, where metal packaging enhances product quality, shelf life, and perceived value, particularly for high-value items like spices, chocolates, and fresh produce.

Japan Light Metal Packaging Market Innovates With Lightweight Alloys and Specialty Packaging

Japan’s light metal packaging industry leverages precision manufacturing to produce next-generation, high-performance packaging. Regulatory guidance, including the Plastic Resource Circulation Act, encourages environmentally responsible designs and reduces single-use plastics. Revised food contact material regulations further drive compliance and innovation.

Manufacturers such as Nippon Light Metal focus on high-purity aluminum and advanced alloys to create specialty, value-added packaging with superior barrier properties. The market emphasizes lightweighting, self-sealing designs, and enhanced functionality, meeting the specialized needs of food, beverage, and industrial applications while maintaining sustainability standards.

Brazil Light Metal Packaging Market Expands With Sustainable Waste Management and Strategic Investments

Brazil’s light metal packaging market is evolving under the National Solid Waste Policy, modernizing waste management and promoting recycling. Provisional antidumping duties on PE imports may boost demand for metal packaging as a sustainable alternative.

Technological advancements focus on metal-to-metal recycling loops for aluminum and steel, complementing the country’s growing food, beverage, and agricultural sectors. Corporate investments are robust, with leading companies executing brownfield and greenfield expansion projects, reflecting confidence in the market’s growth. The industry is increasingly prioritizing sustainable production, closed-loop recycling, and high-performance metal packaging solutions.

Light Metal Packaging Market Report Scope

Light Metal Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$63.7 Billion

|

|

Market Size (2034)

|

$88.3 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Material (Aluminum, Steel, Others), By Product Type (Cans, Closures, Tubes & Aerosol Containers, Drums & Barrels, Others), By Application (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Household & Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., Silgan Holdings Inc., Toyo Seikan Group Holdings, Ltd., CAN-PACK S.A., Sonoco Products Company, TATA Steel, Nippon Light Metal Holdings Co., Ltd., Rexam (a part of Ball Corporation), Universal Can Corporation, Huber Packaging Group GmbH, BWAY Corporation, Exal Corporation, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Light Metal Packaging Market Segmentation

By Material

By Product Type

- Cans

- Closures

- Tubes & Aerosol Containers

- Drums & Barrels

- Others

By Application

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Household & Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Light Metal Packaging Market

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- CAN-PACK S.A.

- Sonoco Products Company

- TATA Steel

- Nippon Light Metal Holdings Co., Ltd.

- Rexam (a part of Ball Corporation)

- Universal Can Corporation

- Huber Packaging Group GmbH

- BWAY Corporation

- Exal Corporation

- Greif, Inc.

* List Not Exhaustive

Methodology

The research methodology for the Light Metal Packaging Market adopted by USDAnalytics is based on a combination of primary and secondary approaches, ensuring high data reliability and industry relevance. Primary research involved in-depth interviews with manufacturers, distributors, suppliers, and regulatory bodies to gain firsthand insights into evolving trends, sustainability mandates, and technological advancements shaping the sector. Secondary research incorporated company annual reports, government regulations, trade journals, industry white papers, and verified databases to validate market dynamics and forecast accuracy. Our analytical framework integrates macroeconomic indicators, regional demand patterns, ESG-driven procurement strategies, and investment flows to provide a holistic market outlook. The use of both top-down and bottom-up estimation techniques ensures precise market sizing, while scenario-based modeling evaluates future growth under different regulatory and sustainability-driven scenarios. This robust methodology positions USDAnalytics as a trusted source for industry professionals seeking actionable intelligence on the light metal packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.