Lignans Market 2025–2034: Pharmaceutical-Grade Botanicals and Clean-Label Extraction Driving $1,073.4 Million Outlook at 7.7% CAGR

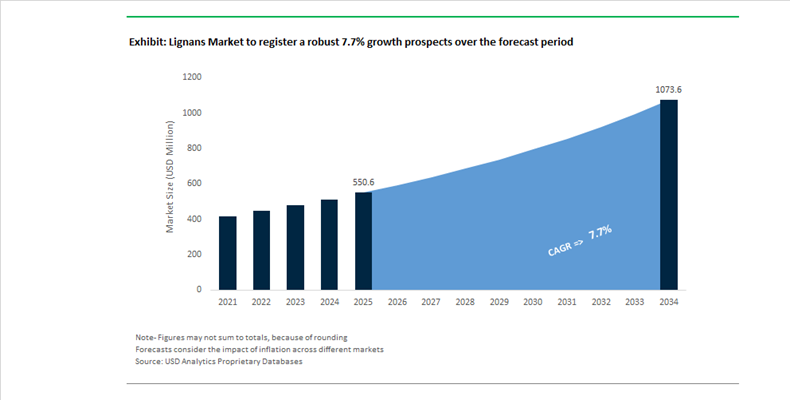

The Lignans Market is projected to expand from $550.6 Million in 2025 to $1,073.4 Million by 2034, registering a CAGR of 7.7%. Market acceleration is underpinned by rising demand for standardized flaxseed lignans, spruce-derived HMRlignan (7-hydroxymatairesinol), and high-purity enterolactone precursors across dietary supplements, functional foods, hormone-support formulations, and pharmaceutical-grade botanical applications. Increasing clinical validation of lignans in metabolic syndrome management, prostate health, estrogen metabolism modulation, and adipogenesis inhibition is reshaping their positioning from generic phytoestrogens to targeted bioactive compounds with defined therapeutic relevance.

In October 2024, Life Extension updated its prostate health clinical protocols to emphasize combined usage of ActiFlax and HMRlignan, citing evidence that these lignans modulate estrogen metabolism and reduce tumor cell proliferation in aging male populations. In 2024, the Flax Lignan Association was formally organized to standardize labeling, safety protocols, and differentiation between whole flaxseed and concentrated lignan extracts, reinforcing regulatory clarity within nutraceutical channels. Scientific reviews published across late 2024 and 2025 further strengthened clinical support for HMRlignan, confirming its metabolite enterolactone reduces metabolic imbalance and inhibits adipocyte formation in metabolic syndrome models. These developments elevate lignans into higher-margin, clinically substantiated botanical ingredient categories.

Corporate consolidation and extraction technology upgrades are redefining competitive structure. In March 2025, Vivalto Partners acquired Linnea SA, the global leader in pharmaceutical-grade HMRlignan production, signaling intensified capital deployment into standardized spruce-derived lignans. In July 2025, Nexira completed its ATLAS automation project at Serqueux, enhancing production efficiency for botanical powders relevant to fiber-rich lignan sources, while reaffirming sustainable sourcing initiatives under its Trees of Life program in December 2025. Throughout 2025, manufacturers including BioGin Biochemicals and Naturalin Bio-Resources transitioned toward Supercritical CO2 extraction, aligning with clean-label, solvent-free supplement demand. In January 2026, ADM closed government investigations related to intersegment sales, stabilizing its oilseed and flaxseed supply chain operations critical for SDG lignan precursors. In the same month, Linnea secured a Swissmedic narcotics license, reinforcing its pharmaceutical-grade compliance framework. In early 2026, functional food brands introduced advanced flax lignan-based weight management protocols positioned around hormonal balance and metabolic health optimization, further expanding application scope beyond traditional fiber supplementation.

Strategic Trends and High-Value Opportunities Reshaping the Global Lignans Market

Trend: Vertical Integration and Soil-to-Supplement Traceability Redefine Lignan Supply Chains

The lignans market is undergoing a structural shift as nutraceutical and functional food brands move away from fragmented spot-market sourcing toward vertically integrated, traceable supply chains. This transition is driven by the need to guarantee consistent concentrations of secoisolariciresinol diglucoside, eliminate pesticide contamination risks, and meet organic and regenerative agriculture certifications increasingly demanded by premium consumers. For manufacturers, control over upstream oilseed processing has become a strategic lever to stabilize quality, margins, and regulatory compliance in a volatile agricultural environment.

In North America, this strategy has translated into direct infrastructure investments. Scoular operationalized its high-speed flax processing facility in Regina, Canada, specifically engineered to handle both whole and milled flax at scale. The facility supports lignan-rich feedstock production for functional foods, dietary supplements, and pet nutrition, reinforcing regional supply security. Digitalization is further strengthening resilience. By mid-2025, leading oilseed processors embedded artificial intelligence into procurement and inventory systems, enabling real-time quality monitoring and dynamic sourcing decisions to offset flaxseed price volatility linked to climate events and geopolitical disruptions. Parallel to this, multi-year sourcing agreements with regenerative agriculture cooperatives are gaining traction. These contracts mandate harvesting techniques that preserve the flaxseed coat, where lignan concentrations are highest, improving extraction yields by an estimated 12% and reinforcing soil-to-supplement traceability as a competitive differentiator.

Trend: Regulatory Alignment with FDA Healthy Labeling and Global Food Policy Frameworks

Regulatory developments are acting as a powerful demand catalyst for lignans, particularly in fortified foods and beverages. The updated Healthy labeling rule issued by the Food and Drug Administration is reshaping formulation strategies across cereals, snacks, and bakery products. Set to take effect for early adopters in April 2025, the rule prioritizes whole-grain equivalents and imposes strict limits on added sugars, creating a strong incentive to incorporate flaxseed and cereal-derived lignans to meet foundational food criteria. Under the final guidance released in December 2024, products must contain at least three quarters of an ounce equivalent of whole grains per serving, accelerating R&D activity around lignan-fortified offerings positioned for cardiovascular and metabolic wellness.

Regulatory momentum is not limited to the United States. In September 2024, the European Food Safety Authority published updated guidance on novel and traditional foods, providing greater clarity for the approval of concentrated bioactive compounds. This is streamlining market entry for lignan-enriched functional beverages and supplements in Europe, reducing time to commercialization while reinforcing safety and substantiation requirements. Public health frameworks are also reinforcing adoption. The Dietary Guidelines for Americans emphasize nutrient-dense dietary patterns, allowing ingredient suppliers to position lignans within permissible structure and function claims related to heart health and glycemic control, further embedding lignans into mainstream food and nutrition strategies.

Opportunity: Pharma-Grade Lignan Isolates as Adjuncts in Oncology and Metabolic Health

Emerging clinical evidence is expanding the lignans market beyond dietary supplementation into pharma-grade applications, particularly as adjuncts in oncology and metabolic disease management. Research published between 2024 and 2025 highlights the role of flaxseed-derived lignans as bioactive polyphenols capable of interacting with key carcinogenic pathways. These compounds are increasingly viewed as candidates for combination therapies that may enhance treatment efficacy while maintaining favorable toxicity profiles, improving patient quality of life during chemotherapy.

In metabolic health, clinical reviews released in mid-2025 underscore the role of plant polyphenols in regulating gut microbiota balance and downstream metabolic signaling. Lignans have been shown to influence metabolites associated with AMPK and NF-kB pathways, providing a mechanistic rationale for their use in managing obesity, insulin resistance, and chronic inflammation. To unlock these opportunities, ingredient manufacturers are investing in advanced delivery technologies. Microencapsulation and nano-emulsion systems are being developed to overcome historically low bioavailability, improving systemic absorption of lignans such as schisandrin and gomisin. These innovations are broadening the clinical potential of lignans into neurodegenerative and hepatoprotective applications, supporting higher-margin pharmaceutical and medical nutrition segments.

Opportunity: Standardized Spruce Lignans Drive Non-Hormonal Women’s Health Solutions

Women’s health represents one of the most commercially attractive growth avenues for the lignans market as demand accelerates for non-hormonal alternatives to traditional hormone replacement therapy. Standardized extracts derived from Norwegian spruce are gaining clinical and commercial momentum, particularly for the management of menopausal symptoms. Lignans such as 7-hydroxymatairesinol demonstrate high bioavailability and are efficiently metabolized into enterolactone, a key phytoestrogen associated with symptom relief and cardiometabolic benefits.

Clinical studies indicate that a daily intake of 72 milligrams of 7-hydroxymatairesinol can reduce the frequency of hot flashes by approximately 50% in post-menopausal women, positioning spruce lignans as a credible, evidence-backed option in this category. The broader phytoestrogen supplement market is expected to expand steadily through 2034, with North America currently leading adoption due to strong consumer preference for plant-based solutions supporting bone, heart, and hormonal health. Proprietary ingredient development is accelerating commercialization. Linnea SA has pioneered standardized spruce extracts such as HMRlignan, containing up to 70% 7-hydroxymatairesinol. These clinician-preferred ingredients are being incorporated into premium supplements designed to deliver efficacy without the side-effect profiles associated with synthetic hormone therapies, reinforcing lignans as a cornerstone of next-generation women’s health formulations.

Lignan Market Share and Segmentation Insights

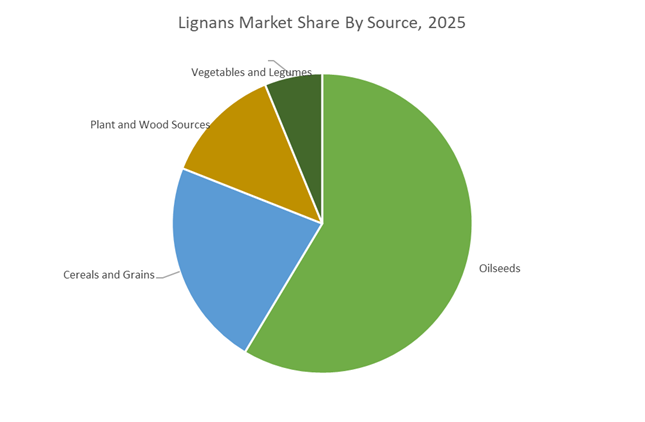

Oilseeds Lead Lignan Production Through High Natural SDG Content and Established Flaxseed Supply Chains

Oilseeds represented 58.60% of the Lignans Market share in 2025, making them the dominant raw material source for commercial lignan extraction. Among oilseeds, flaxseed (linseed) is the richest natural source of lignans, particularly secoisolariciresinol diglucoside (SDG), a phytoestrogen compound widely used in nutraceutical and functional food formulations. The high lignan concentration in flaxseed, combined with well-established agricultural production and oilseed processing infrastructure, enables efficient extraction and purification of lignan-rich ingredients for dietary supplements and health-focused food products. Oilseed-derived lignans are widely incorporated into capsules, powders, fortified foods, and plant-based nutrition products, where they are valued for antioxidant and phytoestrogen properties. In 2025, lignan producers increasingly focus on sustainable flaxseed sourcing and supply chain transparency, implementing certifications such as organic labeling, non-GMO verification, and traceable agricultural sourcing programs. These initiatives support premium product positioning and respond to consumer demand for ethically sourced, environmentally responsible nutraceutical ingredients.

Dietary Supplements Drive the Largest Demand for Lignans in Health and Wellness Products

Dietary supplements accounted for 52.80% of the Lignans Market share in 2025, establishing them as the largest application segment for lignan-based ingredients. Lignans are widely marketed as bioactive plant compounds with antioxidant, anti-inflammatory, and hormone-balancing properties, making them popular ingredients in nutraceutical products targeting women’s health, cardiovascular wellness, and metabolic support. Supplement formulations commonly utilize flaxseed-derived lignan extracts standardized for SDG concentration, allowing consistent dosing and bioactive delivery in capsule, tablet, and powdered supplement formats. In 2025, growing global awareness of perimenopause and menopause health management has significantly increased consumer interest in natural hormone-support supplements. Lignan-based formulations are increasingly positioned as plant-derived alternatives to conventional hormone therapies, addressing symptoms such as hormonal imbalance, hot flashes, and metabolic changes associated with midlife health transitions. Nutraceutical manufacturers are also developing targeted hormonal wellness products tailored to specific life stages, expanding the market beyond traditional menopause support toward broader preventive health and longevity-focused supplementation strategies.

Lignans Market Competitive Landscape

The lignans market in 2026 is driven by SDG standardization, bioavailability optimization, and clean-label nutraceutical demand. Competition is shifting toward high-purity lignan extracts, clinically positioned metabolic health ingredients, and vertically integrated supply chains ensuring traceability, regulatory compliance, and functional efficacy across food, supplement, and pharmaceutical applications.

ADM scales flax lignan production through vertically integrated nutrition strategy

Archer Daniels Midland (ADM) is leveraging its oilseeds infrastructure to dominate flax-derived lignan concentrates, particularly secoisolariciresinol diglucoside (SDG) for functional foods and nutraceuticals. Its $500–$750 million cost optimization program is reallocating capital toward high-margin Nutrition segment ingredients, including lignan-rich plant extracts. With vertically integrated sourcing and molecular distillation capabilities, ADM ensures supply chain transparency and sustainability assurance across 71% of exports. Capacity optimization in North America positions the company to capture renewed demand for clean-label, plant-based functional ingredients in 2026.

BASF enhances lignan stability and application through AI-driven R&D integration

BASF SE is strengthening its position in specialty phytonutrients by applying chemical engineering and AI-enabled research to improve lignan stability, formulation compatibility, and synergistic antioxidant performance. Its “Winning Ways” strategy prioritizes high-value nutrition and care applications while divesting non-core assets to protect margins. The Hyderabad Digital Hub accelerates discovery of lignan-antioxidant interactions, supporting advanced nutraceutical and packaging solutions with low product carbon footprint (PCF). Strategic price adjustments reflect a broader shift toward premium, performance-enhancing lignan ingredients over commoditized supply.

BioGin advances high-purity flax lignans for functional foods and gut health

BioGin Biochemicals is emerging as a key innovator in natural lignan extracts, focusing on high-concentration flaxseed derivatives rich in alpha-linolenic acid (ALA) and SDG. Its refined extracts are tailored for performance nutrition products such as energy bars and bakery applications, emphasizing cardiovascular and gut barrier health benefits. Backward integration ensures contaminant-free sourcing aligned with FDA and DSHEA standards, while AI-driven R&D initiatives aim to accelerate custom lignan blend development for functional beverages and targeted nutraceutical formulations.

TCI dominates pharmaceutical-grade lignans with high-purity analytical standards

Tokyo Chemical Industry Co., Ltd. (TCI) is the benchmark supplier for high-purity (>98%) lignans used in pharmaceutical R&D and clinical trials. Its portfolio includes SDG, sesamin, and schisandrin A, supporting research into neurodegenerative, antiviral, and antibacterial applications. Advanced chemical modification techniques, such as Mitsunobu-type reactions, enable development of water-soluble lignan derivatives with improved bioavailability. TCI’s investment in digital SDS access and traceable purity data aligns with the growing demand for tech-enabled compliance in global research ecosystems.

Kikkoman leverages fermentation to improve lignan bioavailability in functional foods

Kikkoman Corporation is differentiating through fermentation-driven biotransformation, enhancing the bioavailability and metabolic conversion of lignans into enterolactone. Its academic collaborations focus on improving consistency of gut microbiome interactions, positioning lignans as clinically relevant phytoestrogens for metabolic health. Strategic portfolio rebalancing toward high-value phytochemicals supports the development of lignan-fortified functional beverages targeting aging populations in Asia-Pacific, where demand for preventive healthcare ingredients is accelerating.

Hebei Xinqidian scales traceable lignan extraction for global nutraceutical supply chains

Hebei Xinqidian Biotechnology is a leading large-scale producer of flax and sesame lignans, focusing on cost-efficient extraction and export-oriented supply. Investments in localized production near oilseed cultivation zones improve raw material freshness and reduce logistics costs. Enhanced traceability systems address stringent EU regulations by providing batch-level phytochemical and pesticide data. Its high-volume lignan offerings target immunity-focused nutraceuticals and energy bar applications in North America, balancing scalability with increasing regulatory compliance requirements.

United States Lignans Market: Functional Ingredient Upscaling and Biomedical Validation

The United States lignans market is evolving from commodity botanical extracts toward higher-value, evidence-backed functional ingredients integrated into preventive health and nutrition platforms. In August 2025, Archer Daniels Midland announced the streamlining of its soy and specialty protein network, leveraging the recommissioned Decatur East plant to integrate oilseed-derived lignans into its Health and Well-being portfolio. This operational pivot reflects rising demand for phytoestrogens and antioxidant compounds across cereals, bars, and fortified foods. Regulatory continuity has reinforced confidence, as the U.S. Food and Drug Administration retained GRAS status for specific flaxseed lignan concentrates in 2025, accelerating formulation activity in breakfast cereals and energy bars where lignans are positioned for estrogen-modulating and oxidative stress reduction benefits.

Beyond food applications, the U.S. market is seeing increasing pharmaceutical and nutraceutical pull. The National Institutes of Health allocated new grants in late 2025 to study enterolactone and enterodiol in hormone-related cancer prevention, stimulating demand for pharmaceutical-grade lignans with validated purity and bioavailability. On the supply side, ESG alignment is becoming a procurement requirement. Linnea SA, a major supplier to U.S. brands, updated its ESG and human rights policies in December 2025 to meet 2026 clean-label transparency expectations. Simultaneously, U.S. nutraceutical firms are deploying AI-driven nutrient mapping to optimize lignan and omega-3 synergies in high-bioavailability softgels, reinforcing the shift toward data-backed formulation science.

Canada Lignans Market: Feedstock Security and Solvent-Free Extraction Leadership

Canada’s lignans market is structurally advantaged by flaxseed abundance, policy-backed farm stability, and early adoption of advanced extraction technologies. In 2025, Agriculture and Agri-Food Canada increased AgriStability compensation to 90%, significantly de-risking flaxseed cultivation and ensuring consistent feedstock availability for lignan processors despite climatic volatility. Parallel to this, the University of Saskatchewan reported successful pilots of lignan-optimized flax cultivars yielding up to 12% higher secoisolariciresinol diglucoside content per gram of hull, directly improving extraction economics.

Processing infrastructure is scaling to meet export-grade specifications. In 2025, Manitoba commissioned new supercritical CO2 extraction facilities, enabling solvent-free lignan isolation aligned with stringent EU organic requirements effective in 2026. Regulatory tightening is shaping competitive dynamics, as Health Canada’s updated Natural Health Products regulations require molecular-level safety and pharmacokinetics data for concentrated polyphenols. This favors established Canadian manufacturers with validated clinical and toxicological dossiers, positioning Canada as a premium supplier of traceable, high-purity lignans to Europe and Asia.

China Lignans Market: High-Purity Scale-Up and Functional Beverage Adoption

China’s lignans market is transitioning rapidly toward high-purity extracts and consumer-facing functional formats. BioGin Biochemicals showcased purification milestones for sesame-derived lignans such as sesamin and sesamolin at Vitafoods Europe 2025 and is expanding high-purity extraction lines in Chengdu to meet 2026 export targets. This aligns with the Ministry of Industry and Information Technology 2025 work plan, which designates high-end botanical extracts as a priority sector and incentivizes circular models that upcycle oilseed press cakes into value-added lignans.

Domestic consumption is also accelerating. Clinical observations conducted by the Chinese Academy of Medical Sciences in 2025 linked lignan intake with breast health outcomes, driving strong uptake of lignan-fortified functional beverages in Tier-1 cities. To support consumer acceptance, manufacturers are scaling micro-encapsulation technologies to mask bitterness, enabling integration into dairy-based beauty-from-within drinks and ready-to-consume wellness formats.

Germany Lignans Market: Preventive Nutrition and Regulatory-Led Differentiation

Germany represents one of Europe’s most evidence-driven lignans markets, anchored in preventive nutrition and strict regulatory oversight. In 2025, the German Cancer Research Center published findings linking high lignan consumption in postmenopausal women to reduced breast cancer risk. This research has catalyzed demand across Germany’s preventive nutrition and pharmacy channels, elevating lignans from niche supplements to clinically referenced ingredients.

Regulatory pressure is intensifying product differentiation. From August 2026, German producers must comply with EU Regulation 2025/40 on sustainable packaging and clean-label claims, while European Food Safety Authority has introduced stricter verification standards for plant-based health claims. In response, German pharmaceutical firms are piloting 2026-targeted formulations combining lignans with calcidiol monohydrate, newly approved under EU 2025/352, to support bone density and hormonal balance. These initiatives underscore Germany’s focus on science-led, compliance-ready lignan applications.

Lignans Market: Country-Level Strategic Summary

Lignans Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Lignan Focus

|

Strategic Implication

|

|

United States

|

Functional foods and biomedical research

|

Flaxseed lignans, enterolactone

|

Data-backed nutraceutical and pharma demand

|

|

Canada

|

Feedstock security and extraction tech

|

SDG-rich flax lignans

|

Premium, solvent-free export positioning

|

|

China

|

High-purity scale and functional beverages

|

Sesamin, sesamolin

|

Consumerized lignans with circular sourcing

|

|

Germany

|

Preventive nutrition and regulation

|

Clinically validated lignans

|

Science-led differentiation under strict EU compliance

|

Lignans Market Report Scope

Lignans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$550.6 Million

|

|

Market Size (2034)

|

$1073.4 Million

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Source (Oilseeds, Cereals and Grains, Plant and Wood Sources, Vegetables and Legumes), By Product Type (Plant-Derived Lignans, Mammalian Lignans), By Grade (Pharmaceutical Grade, Food Grade, Cosmetic Grade), By Application (Dietary Supplements, Functional Foods, Functional Beverages, Cosmetics and Personal Care, Animal Nutrition), By Distribution Channel (Business-to-Business, Business-to-Consumer)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archer Daniels Midland, Linnea, BioGin Biochemicals, TSI Group, Hebei Xinqidian Biotechnology, FarmaSino Pharmaceuticals, Naturalin Bio-Resources, Kingherbs, Prairie Tide Diversified, Biosearch Life, Bioriginal Food and Science, Plamed Green Science Group, Xi’an Sost Biotech, Acatris, Huzhou South-North Trading

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lignans Market Segmentation

By Source

- Oilseeds

- Cereals and Grains

- Plant and Wood Sources

- Vegetables and Legumes

By Product Type

- Plant-Derived Lignans

- Mammalian Lignans

By Grade

- Pharmaceutical Grade

- Food Grade

- Cosmetic Grade

By Application

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Cosmetics and Personal Care

- Animal Nutrition

By Distribution Channel

- Business-to-Business

- Business-to-Consumer

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Lignans Market

- Archer Daniels Midland

- Linnea

- BioGin Biochemicals

- TSI Group

- Hebei Xinqidian Biotechnology

- FarmaSino Pharmaceuticals

- Naturalin Bio-Resources

- Kingherbs

- Prairie Tide Diversified

- Biosearch Life

- Bioriginal Food and Science

- Plamed Green Science Group

- Xi’an Sost Biotech

- Acatris

- Huzhou South-North Trading

*- List not Exhaustive